This article is excerpted from a letter by Zeke Ashton, managing partner of Centaur Capital Partners, based in Southlake, Texas.

We view Facebook’s ~20% stock price decline in late July as sort of a “sequel” to its initial decline earlier this year when the stock suffered a similar fall. We had taken the Fund’s position in Facebook to as high as 20,000 shares back in March as the data usage controversy reached its most intense level. As the stock rallied into the summer and the world’s attention moved to other subjects, we trimmed the position at incrementally higher prices such that we had reduced the Fund’s position to 13,000 shares going into the late July Q2 earnings report.

We believe that Facebook’s management has elected the path of absorbing some short term pain in order to protect the longer term value of the business. Facebook’s biggest risk factors appear to be reputational and regulatory in nature, and the company needs to show that it takes responsibility for the potential negative societal impacts introduced by its products in order to mitigate these risks.

If Facebook is successful in its efforts to the extent that both users and advertisers perceive that its services are less prone to societal harm, then the business will likely be far healthier and better insulated from these hard-to- quantify risk factors in the future.

However, it is also apparent that Facebook will be investing heavily to better monitor the 2.5 billion users and many millions of advertisers across its platform. As a result, the company’s near term financial outlook seems somewhat less attractive than it did prior to the recent controversies, and our estimated value range for the stock is also somewhat lower today than it was six months ago.

Importantly, in our view Facebook’s business remains immensely strong and user behavior has largely been unchanged by the recent negative events and corresponding media coverage. Now that expectations for the business have been re-set, we hope that the company can move forward with less drama and the stock price will move higher as the market regains comfort with the company’s strategic direction. As of this writing the Fund’s position of 15,000 shares is roughly a 4% portfolio weighting with the stock trading at around $175 per share.

Challenges of Investing in an Expensive Market

While the Fund has made money on its Facebook investment so far in 2018, we feel somewhat fortunate to have done so because the stock itself has not produced a gain. Our experience has been somewhat better only because we bought shares on weakness and sold shares on strength.

However, I think Facebook is a good case study in the difficulties of investing in a market in which nearly all high quality businesses trade at extremely full valuations, and in most cases one can really only hope to find relative (not absolute) value. The problem is that when prices are full, stocks are vulnerable to sudden changes in future expectations.

In the case of Facebook, we can make a strong argument for relative value at prices we paid, but we know that the margin of safety in the event we are too optimistic in our estimates is much lower than we’d like.

While most of the Fund’s investments aren’t in high growth companies like Facebook and therefore aren’t quite as sensitive to changes in expected future growth rates and profit margins, we still have less room for error than we’d like on the valuation side across the portfolio.

This means we have to be very diligent with respect to watching for emerging risk factors that could affect our portfolio companies. It also means we need to be aware of how the potential risk/reward pay-offs for our securities change as prices move around, and take reasonable action to increase or decrease exposure when opportunities present themselves.

Disclaimer: This report is being furnished by Centaur Capital Partners (“Centaur”) on a confidential basis and does not constitute an offer, solicitation or recommendation to sell or an offer to buy any securities, investment products or investment advisory services. This report is being provided to existing limited partners for informational purposes only, and may not be disseminated, communicated or otherwise disclosed by the recipient to any third party without the prior written consent of Centaur. An investment in the Fund (“CVF”) involves a significant degree of risk, and there can be no assurance that its investment objectives will be achieved or that its investments will be profitable. Certain of the performance information presented in this report are unaudited estimates based upon the information available to Centaur as of the date hereof, and are subject to subsequent revision as a result of the CVF’s audit. The performance results of CVF include the reinvestment of dividends and other earnings. Past performance is not necessarily a reliable indicator of future performance of CVF. An investment in CVF is subject to a wide variety of risks and considerations as detailed in the confidential memorandum of CVF. References to the S&P 500, NASDAQ Composite and other indices herein are for informational and general comparative purposes only. There are significant differences between such indices and the investment program of CVF. CVF does not invest in all or necessarily any significant portion of the securities, industries or strategies represented by such indices. References to indices do not suggest that CVF will or is likely to achieve returns, volatility or other results similar to such indices. This presentation and the accompanying discussion include forward-looking statements. All statements that are not historical facts are forward-looking statements, including any statements that relate to future market conditions, results, operations, strategies or other future conditions or developments and any statements regarding objectives, opportunities, positioning or prospects. Forward-looking statements are necessarily based upon speculation, expectations, estimates and assumptions that are inherently unreliable and subject to significant business, economic and competitive uncertainties and contingencies. Forward-looking statements are not a promise or guaranty about future events. The information in this presentation is not intended to provide, and should not be relied upon for, accounting, legal, or tax advice or investment recommendations. Each recipient should consult its own tax, legal, accounting, financial, or other advisors about the issues discussed herein.

.@WarrenBuffett once said, “What the wise man does in the beginning, the fool does in the end.” This tells you 80% of what you have to know about #MarketCycles and their impact. I consider this the number-one piece of #investment wisdom. –HM

This article is authored by MOI Global instructor Steven Kiel, chief investment officer of Arquitos Capital Management.

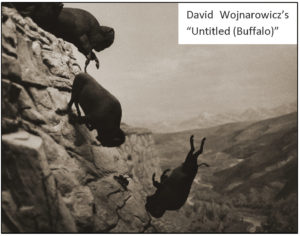

Thousands of years ago, before the use of horses, Native Americans utilized a hunting technique that preyed on animalistic instincts. This technique was called the buffalo jump. Hundreds of buffalo could be killed at a time without the use of weapons.

Tribesmen would set up a path lined with piles of rocks and tree stumps, creating a “road” towards the cliff. Hunters would then frighten a lead buffalo in a herd onto the path and cause a stampede.

Stampedes are not unique to buffalo and happen with humans as well, even today.

Psychological stampedes are more widespread than physical stampedes, though. The dot com bubble was a psychological stampede. The run-up in housing prices prior to 2008 was a psychological stampede. So were Beanie Babies, the Salem witch trials, tulips, the nifty-fifty, and too many more examples to list.

Stampedes (or bubbles or manias) are a staple of human nature. We have a fear of missing out. We are greedy and fearful. Like the buffalo, we feel safer in the crowd. As Keynes has said, “Worldly wisdom teaches that it is better for reputation to fail conventionally than to succeed unconventionally.”

Sometimes it takes courage simply to be a bystander. We don’t have to be Michael Burry betting against sub-prime mortgages. During the housing bubble, we could have succeeded by simply sitting it out, not investing in lenders, homebuilders, and other ancillary businesses, staying away from AIG, Lehman Brothers, Bear Stearns. If we can be the hunter, then great, but we can also win by not being the prey.

How does that apply to our portfolio? I avoid companies in industries that attract risk-takers. It is very difficult for a company to go bankrupt if they don’t have debt, so I avoid margin leverage in the portfolio, and I avoid companies that rely on debt.

As a passive owner in a business, we want the decision-maker at the company to like vanilla ice cream and The Andy Griffith Show, and we want him or her to drive a Toyota Corolla. The more boring the better. Sure, we can get rich riding along with a daredevil, but how would we know when to get off the ride? We know compounding works in our favor, so why take the risk?

Ideal CEOs for us are people like Brian Moynihan at Bank of America and Mike Falcone at MMA Capital. Both are focused on creating long-term value for their shareholders and not taking unnecessary risks. Ironically, it can be unconventional to be a boring CEO!

There is both wisdom and madness in crowds. The point is to be thoughtful about who we follow, what companies we own, and how we go about making decisions. Without that thoughtfulness, we would have no chance of beating the markets.

Disclaimer: This letter is for informational purposes only and does not reflect all of the positions bought, sold, or held by Arquitos Capital Offshore Master, Ltd. or its feeder funds, Arquitos Capital Partners, LP and Arquitos Capital Offshore, Ltd. Any performance data is historical in nature and is not an indication of future results. All investments involve risk, including the loss of principal. We disclaim any duty to provide updates or changes to the information contained in this letter. Performance returns presented above are for Arquitos Capital Partners, LP and reflect the fund’s total return, net of fees and expenses since its April 10, 2012 inception. They are net of the high water mark and the 20% performance fee, applied after a 4% hurdle, as detailed in the confidential private offering memorandum. Arquitos Capital Offshore, Ltd. was launched on March 1, 2018. Returns from Arquitos Capital Offshore, Ltd. may differ slightly and are not presented here. Performance returns for 2018 are estimated by our third-party administrator, pending the year-end audit. Actual returns may differ from the returns presented. Positions reflected in this letter do not represent all the positions held, purchased, or sold. This letter in no way constitutes an offer or solicitation to buy an interest in Arquitos Capital Partners, LP, Arquitos Capital Offshore, Ltd. or any of Arquitos Capital Management’s other funds or affiliates. Such an offer may only be made pursuant to the delivery of an approved confidential private offering memorandum to an investor.

This article by MOI Global instructor Robert Leitz has been excerpted from a letter of iolite Partners, a value-oriented investment firm based near Zurich, Switzerland.

In 2007, a man started to play the violin at a metro station in Washington DC on a cold January morning. He played six Bach pieces for about 45 minutes. During that time, since it was rush hour, thousands of people went through the station.

Three minutes went by until somebody noticed there was a musician playing. A middle-aged man slowed his pace and stopped for a few seconds — and then hurried up to meet his schedule. A minute later, the violinist received his first dollar tip: a woman threw money into the player’s violin case and continued to walk. A few minutes later, a man leaned against the wall to listen to him, but then looked at his watch and started to walk again. Clearly, he was late for work.

The one who paid the most attention was a 3-year-old boy. His mother hurried him along, but the kid stopped to look at the violinist. Finally, the mother pushed hard and the child continued to walk, turning his head all the time. This action was repeated by several other children. All the parents, without exception, forced them to move on.

In the 45 minutes the musician played, only 6 people stopped and stayed for a while. About 20 gave him money but continued to walk their normal pace. He collected $32. When he finished playing and silence took over, no one noticed. No one applauded, nor did anyone recognize him.

The violinist was Joshua Bell, one of the best musicians in the world. He played one of the most intricate pieces ever written, with a violin worth $3.5 million. Two days before his playing in the subway, Joshua Bell sold out at a theater in Boston and the seats averaged $100. His performance in the metro was a social experiment by the Washington Post about the perception, taste and priorities of people.

If we do not notice one of the best musicians in the world playing the best music ever written, what else are we missing? The story tells us that we tend to see only what we expect, and that our perception is heavily driven by social conditioning.

Members, log in below to access the restricted content.

Not a member?

Thank you for your interest. Please note that MOI Global is closed to new members at this time. If you would like to join the waiting list, complete the following form:

This article is excerpted from a letter by MOI Global instructor Jim Roumell, partner and portfolio manager of Roumell Asset Management (RAM), based in Chevy Chase, Maryland. Jim is a valued participant in The Zurich Project.

RUBI reported a very strong quarter indicating that the company has successfully leveraged its legacy ad-tech strengths to position itself to be one of the leaders in the programmatic buying and selling of online advertisements. RUBI has steadily gained market share over the past several months. In March 2017, Michael Barrett implemented a number of key initiatives when he became the company’s second CEO, building upon decisions made in 2016, that are working. The evidence is increasingly clear that those initiatives have turned around the company’s fortunes since its dramatic fall from grace two years ago when the protocols for online ad-buying changed and RUBI was caught flat-footed.

Members, log in below to access the restricted content.

Not a member?

Thank you for your interest. Please note that MOI Global is closed to new members at this time. If you would like to join the waiting list, complete the following form:

Disclosure: The specific securities identified and described do not represent all of the securities purchased, sold, or recommended for advisory clients, and the reader should not assume that investments in the securities identified and discussed were or will be profitable.

Niraj Gupta of GCI Partners presented his in-depth investment thesis on Facebook (Nasdaq: FB) at Wide-Moat Investing Summit 2018.

The full session is available exclusively to members of MOI Global.

Members, log in below to access the full session.

Not a member?

Thank you for your interest. Please note that MOI Global is closed to new members at this time. If you would like to join the waiting list, complete the following form:

About the instructor:

Niraj Gupta has over 25 years of experience analyzing and investing in publicly traded companies as a buy-side analyst/portfolio manager and a sell-side research analyst, with particular expertise in the technology, media and telecom industries. Prior to starting GCI Partners in 2008, Niraj was associated with Pequot Capital, Citigroup, Schroders and Goldman Sachs.

Michael Lee of Hypotenuse Capital Management shared his wisdom and insights into the nature and features of moats at Wide-Moat Investing Summit 2018.

The full session is available exclusively to members of MOI Global.

Members, log in below to access the full session.

Not a member?

Thank you for your interest. Please note that MOI Global is closed to new members at this time. If you would like to join the waiting list, complete the following form:

About the instructor:

Michael J. Lee is the founder of Hypotenuse Capital Management, an investment management firm based in Los Angeles, CA. Hypotenuse seeks to invest intelligently in exceptional leaders running extraordinary companies that deserve to win. Prior to founding Hypotenuse, Michael was a partner at Royal Capital Management in New York, a private equity associate at Parthenon Capital in Boston, and an investment banking analyst at Bear Stearns. He sits on the board of directors of the P.F. Bresee Foundation, a non-profit organization devoted to breaking the cycle of poverty and violence in Central Los Angeles. Outside of investing and philanthropy, Michael enjoys rock climbing, swimming and playing board games with his wife and two children.

Thomas Bushey of Sunderland Capital Partners presented his in-depth investment thesis on TripAdvisor (Nasdaq: TRIP) at Wide-Moat Investing Summit 2018.

The full session is available exclusively to members of MOI Global.

Members, log in below to access the full session.

Not a member?

Thank you for your interest. Please note that MOI Global is closed to new members at this time. If you would like to join the waiting list, complete the following form:

About the instructor:

Thomas Bushey has over fifteen years of experience managing and investing capital. Prior to founding Sunderland, he was a portfolio manager at Blackrock. Prior to Blackrock, Mr. Bushey was a Senior Analyst for Mayo Capital Partners from 2010 to 2012. Before that, he served a Senior Analyst at Millennium Partners from 2008 to 2009, where he was part of a global industrial investment team. Mr. Bushey began his career as an analyst for Credit Suisse First Boston (“CSFB”) and later moved to HCI Equity Partners (Thayer Capital). At CSFB, he executed and analyzed mergers, acquisitions, leveraged buyouts, divestitures, takeover defenses, restructurings and debt and equity financing for corporate clients and financial sponsors. At HCI, he was a member of the investment team responsible for private equity funds focused on industrial products and services. Mr. Bushey has a BS in Economics from the Wharton School of the University of Pennsylvania.

Kaushal Majmudar and Sam Namiri of Ridgewood Investments presented their in-depth investment thesis on BofI Holding (Nasdaq: BOFI) at Wide-Moat Investing Summit 2018.

Thesis summary:

BofI Holding, based in San Diego, is a branchless pure-play internet bank that began operations as a private company in 2000. In the last eighteen years, BOFI has built a fast-growing nationwide banking platform that should continue to generate high returns on equity and assets for some time to come. BOFI’s low-cost business model is differentiated and underappreciated and not correctly valued by the market, partially due to periodic short attacks that are based on a misguided understanding of their business model or even misrepresentations.

The management team has done a great job with capital allocation, growing the bank profitably by developing new products, adding distribution channels, and via acquisitions. The bank completed its IPO in March 2005 at a split-adjusted price of $2.88 per share and recently traded at $43 per share. A price-based CAGR of ~23% annualized over the thirteen years since its IPO, over the same period of time the bank compounded BV per share at an annualized rate of ~17% per year and EPS by ~20% per year. BOFI is a compounding machine that can continue to grow EPS and BV per share at above-market rates for many years.

Trading at a forward P/E of 18x, the quality and consistency of BOFI’s differentiated model, low-cost position, quality of execution, and growth prospects offer patient investors an attractive opportunity to compound capital.

The following transcript has been edited for space and clarity.

Ken Majmudar: We love being part of this community, and we’re happy to have an opportunity to share our thoughts. By way of standard disclosure, let me note we own the idea at the center of this presentation.

Allow me to offer some background on myself and Sam. We started a micro-cap strategy on April 1, 2018. It’s called the Ridgewood Select Value Fund and focuses on small- and micro-cap equities. We are implementing a strategy for other investors that we’ve been doing inside the firm and Sam has done in his previous positions for many years.

The idea is to take concentrated positions in a handful of small- and micro-cap companies we see as having exceptional potential. We distinguish ourselves by taking quite a long-term investment view. Similar to Warren Buffett’s approach to being a businessman and an investor, we like to think like owners, which goes along with taking a long-term view. In addition, we look at it as taking a private equity approach even though we are investing in public companies. A big part of that is doing comprehensive due diligence, including Phil Fisher’s idea of scuttlebutt as presented in his great book “Common Stocks and Uncommon Profits” – talk to various people and try to develop multiple sources for validating ideas. We emphasize company visits and like to see managements and companies in their home environment. Capital allocation ability is also among our important criteria.

I’d like to touch on something we consider topical, namely active versus passive. Passive investing has gotten an incredible amount of fund flows more recently, but the trend has been going on for many years. One implication of this trend is that a lot of active managers have been losing assets – over $200 billion in 2017 in U.S. equities alone went from active managers or active funds to passive managers or passive index funds. The growth of ETFs has also been a part of this trend. In this relation, the question on our minds is whether this is affecting price discovery because with all of these assets moving from the active side to the passive side, the result has been less research and work on trying to find value. We have also had momentum taking over in big segments of the market. ETFs provide an “automatic bid.” One thing that goes part and parcel of this trend towards indexing is that the greater the ownership in a given security of indexes and ETFs, the less reactive to new information and events it is, as some studies have shown. With stocks that have the highest proportion from indexes, new events seem to affect them less than stocks with a greater proportion of active managers and owners. It’s an interesting observation. Since there’s less capital in active funds, there’s also less money in the aggregate available through fees and other channels to fund the cost of research, which has overall reduced price discovery in the marketplace.

Another interesting thing is that ETFs, by the nature of their structure, have to emphasize the liquidity of the positions. There is a little-known change Standard and Poor’s made to the calculation methodology of the S&P 500. Over ten years ago, it used to be based just on market cap, but then S&P float-adjusted the market cap. This is interesting because it means that in securities where the insider ownership is high and going higher, their representation in the index would go in the exact opposite direction, and the vice-versa is also true. That’s fascinating, and a lot of people seem to be unaware of this change. The credit for noticing goes to some of the folks at Horizon Asset Management, as well as Howard Marks in one of his recent papers. They noted a lot of the stuff is going on in indexing and some elements of it are pretty interesting to look at but also somewhat troubling.

By the way, we are big believers in indexing, so the point of this is not to say indexing is a problem but that there are things going on that are troubling in various aspects. There is a saying that goes “What the wise man does in the beginning, the fool does in the end,” so it’s interesting to note that the increase in fund flows creates a self-sustaining cycle. George Soros has a interesting model he calls reflexivity, meaning the decisions of investors affect reality and vice-versa. What’s going on now in this indexing trend is that fund flows are reinforcing the validity of indexing, which is, in turn, reinforcing the fund flows. It’s a positive feedback loop, but it could also lead to extremes and has already done so in some of these assets. An interesting question to ask is what the limit to these fund flows will be. An engaging talk from the folks at Horizon suggested that since most of the fund flows are coming from active to passive, we have something they describe as the “bank of active.” That in itself is limited to an extent: at present, indexing in about 45% of the overall market, and most people think the percentage can go higher, but clearly it can’t go to 100%. It would be interesting to see; we don’t know the answer, but we think it’s an essential question to ask.

For these reasons, we see a lot of opportunity in the areas that are excluded from indexation and ETFs or are just a small percentage of the assets in total. Small caps and micro caps are one such area, in our opinion. It’s interesting to note that, in the aggregate, small caps and micro caps represent more than 80% by number of companies, but small caps account for less than 10% of the total market capitalization, and microcaps – an area where we see a lot of opportunity – represent less than 1%. These numbers may seem surprising, but in a market capitalization-weighted world, you have companies such as Amazon, Google, Apple, and Facebook, which have individual market caps of anything from $500 billion to more than $800 billion, so any of these companies exceeds the totality of all micro caps put together. However, we think there’s an exceptional opportunity in these areas, and as the changes have gone on to the profitability of trading for Wall Street firms, there has been less and less liquidity and increasingly less coverage in the micro-cap area, which makes it an excellent time to look for value there.

Our choice of investment idea is US-traded BofI Holdings (ticker BOFI), BofI standing for Bank of Internet. In mid-June 2018, the stock was trading at about $42.40, giving the company a market cap of approximately $2.65 billion. Depending on who you ask, the cut-off for small cap is under either $2 billion or $3 billion, so some would define BofI as a small cap, and others would call it a micro cap. Our price target is for approximately 50% appreciation from here into the low $60s, which we think could occur within the next two to three years.

BofI is a bank, but while most banks have many branches and a fair amount of overhead, BofI started with the idea that technology and the Internet would allow a bank to have a national footprint without the traditional branch model. The bank operates from one or two buildings in San Diego, California.

We have followed this company for many years and like the advantage it has in terms of its low-cost, proven business model. We’ve also observed it has a history of effective capital allocation into various areas with good risk-adjusted returns. The bank has superior ROIs and ROEs relative to its competitors.

BofI was started in 2000 as a private company and IPO’d in 2005 at a split-adjusted price of $2.88 per share. If you had bought it in the IPO, you’d have CAGR of approximately 23% since then. But not only the price return has been excellent: since 2005, the company has compounded its book value at 17% per year and its EPS by 20% per year. It’s interesting because it’s one of the few publicly traded pure-play internet banks, without the brick-and-mortar branches that add a lot of cost.

We think highly of the company’s management. Greg Garranbrantz, who became CEO in 2007, has done a great job. He has a high-pedigree background as a former investment banker from Goldman Sachs and a management consultant before that at McKinsey & Co. He owns a significant stake in the bank: 1.2 million shares worth just over $50 million. The CFO, Andrew Micheletti, has also done a good job. He joined the bank six years prior to Greg and also owns a substantial stake in the business.

At Ridgewood, we focus on finding what we call compounding machines, and we have been doing this for a long time. BofI definitely qualifies, and we have had a position in it for many years. The company has been relatively consistent (at least on an annualized basis) in compounding earnings and book value, which is helping it compound the stock price as well. We believe this bank can keep doing this for many years to come.

Since this is a bank, we have to discuss loan origination. In a bank, you have assets and liabilities. Counterintuitively, the liabilities are the deposits and borrowings, which is the money customers give you. The loans are the amounts you give to others at higher interest rates than you give to your customers or your lenders, thereby generating a spread. In addition to that spread between the cost of money and the amount you can charge for it, you also have some fee income. One thing you see in a growth bank is its ability to generate assets, i.e., loans. One of the reasons this bank has performed so well on a profitability and earnings basis is its ability to grow its loan portfolio, which generates a lot of its income. Of course, it’s essential for a bank not only to generate a lot of loan growth but to generate good loans that will pay the money back with interest. BofI has done that. When you see a fast-growing bank, it is important to focus not only on the top line, revenue, and loan growth but also to make sure the loans the bank is making are of good credit quality and will pay back. In the 2008/2009 financial crisis, they made a lot of loans, but those were bad loans. It can happen sometimes and is something to be aware of. However, we think BofI understands that point and has done a wonderful job of growing its loan portfolio extremely carefully and intelligently.

This bank has some substantial cost advantages because of its branchless operations, among other things. This is apparent when you compare BofI’s core business margins to those of other banks. One of the major line items for most banks as a percentage of assets is their net interest income. There shouldn’t be a huge difference between the high-end banks as they compete against each other. If BofI was charging a lot more for its money or giving a lot less to depositors, it would show in that business line. As it is, its net interest margin is a little higher than that of the typical bank. The big difference is on the cost side. BofI has a cost advantage when it comes to its overheads for salary and benefits because it doesn’t have branches to staff with lots of people. Rather, it has two office buildings next to each other, and the entire bank and all the staff are run from that branch using technology.

Similarly, it doesn’t need to spend as much as competitors on premises and equipment because it doesn’t have much of a real estate footprint. Its non-interest expenses are also quite lower for the same reason. Cumulatively, this has led to BofI exiting 2017 with a core business margin of 2.37% versus 0.57% for regular banks. Since we’re talking about percent of assets, 2.37% is a big number for a bank getting close to around $10 billion of assets. One way to think about it is that its cost structure and its way of operating have allowed the bank to be far more profitable than the majority of its competitors of a similar size.

Sam Namiri: Let me start by noting that one of the advantages Geico has over other insurance companies is a business model structurally different from that of most other insurance companies. BofI also has this difference in business structural model that gives it the advantage of being a better-run bank than other competitors. This, in turn, allows it to do and try different things and to sustain its advantage over a long period of time.

When BofI started in 2000 as an online-only bank, people didn’t have smartphones. If you wanted to deposit a check, you had to mail it in. As other issues have come up over time, the bank has developed its entire business and has been able to solve any potential issues and address risks in its business. It has built a customer acquisition model through online marketing; it has distribution partners; and it is starting to get even more into using the data collected over a long period of time, which gives the bank yet another advantage. It has a massive amount of online data collected from existing and potential customers and hasn’t yet used much of it, but it is now starting to mine the data and do a much better job of using it to cross-sell.

The bank is also starting to use more automation, which would be difficult for a company with a bunch of branches all over the place. As BofI is a digital-only operation, it can do far more things, on the sale side as well. It has many of its own outbound call center staff, and its bankers are typically in a call center too. BofI was among the first to be able to accept online check deposits. If you have an account with the bank, you can call and either get your personal direct banker or deal with another banker at the call center. With its balance sheet, it securitizes some of the loans it writes and sells them off in addition to typically structured standard loans. That also helps the bank to maintain a strong balance sheet. Thanks to its core digital capabilities, BofI can use less staff than other banks would need to do the same thing.

In terms of the different segments it lends in, BofI has historically done an excellent job. Whenever it sees one lending area get competitive and believes the risk-adjusted returns are strong, it can allocate more capital and shift its focus to less competitive ones. That’s one way it’s been able to start new products as well. A structural advantage BofI has is that it tries not to do things a lot of the big banks do. An example is the single-family jumbo loans – many banks don’t like to give loans to people who don’t have a standard income, who don’t get paid through a job or get your typical pay stubs. What BofI does is give jumbo loans to people who maybe own their business and don’t get paid unless the business makes money. It’s hard to show a pay stub in such instances. BofI will go in and say, “Hey, you own your business and have a lot of assets; you’re able to pay for 40% of an expensive home in a nice big market like L.A., San Francisco, or New York.” And it will give the loan at a 60% loan-to-value (LTV) because it feels comfortable that the real estate prices aren’t going to drop too much and the borrower still has a good credit score despite not having the typical pay stub to show.

That’s one of the businesses the company seriously got into between 2012 and 2014, and it mentioned on a recent call that the business had gotten much more competitive. It has not written as many loans in that area as in the past. Instead, in the last couple of years, it has got into commercial and industrial (C&I) lending and equipment leasing, where it lends out at pretty high interest rates to businesses that don’t want to own the equipment and prefer to lease it. Other banks don’t want to do the work to truly realize whether the business is viable enough to be able to pay and cover that lease. I believe BofI has never had one bad loan in that equipment leasing business since it started.

Majmudar: I’d like to make an analogy with a specialty insurer. If you’re a bank and are able to look in the niches, there’s generally less competition and more opportunity if you’re willing to go into head-to-head competition on the commodity side of the business, as specialty insurers do. That’s part of the quality of this bank and the management team, who realize it and have a platform where they’ve developed this focus over time.

Namiri: Also, BofI is not afraid to admit that a certain segment is getting competitive and to back off during those times and lean up in that area while not fully getting out of that business because every loan is its own business in a way. You could still write loans and have staff there to keeps that structure in place, so once it gets less competitive, you can go back and pick up steam in that line of lending. BofI has historically done a good job of that.

The bank also does commercial real estate lending, most of it so far in the Southern California market. One of the reasons it went into that was because banks get certain benefits from writing loans within their community area. BofI went into small business lending through a good deal it signed with H&R Block. It also does consumer loans, which is a newer line of business for the company. It started doing prime auto lending, which has done well for it over the past couple of years, and this business started organically. And it started dabbling recently in unsecured lending and consumer lending, which is immaterial for its business currently but was a segment it thought could potentially work well.

Some of the numbers speak clearly to the strength of the business. For example, checking growth from 2013 to 2018, in terms of deposits, is 913%, while the savings growth is 268%. Originally, one of the knocks BofI took came from paying a lot of money for the deposits: in June 2013, when it had $2.1 billion in deposits, 50% of that base was time deposits, which are CDs and other higher interest rate deposit accounts and less in checking and savings. By March 2018, the deposit base had grown to $8 billion, and the company had managed to get 50% in checking and similar deposits and 30% in savings deposits, which are much lower rate interest than CDs, while the share of time deposits had shrunk to 17%.

Being an online-only bank has allowed BofI to achieve that. It doesn’t charge you anything at all to have a bank account, even at smaller minimums, and can also give you interest on your checking account. Depending on the checking account you have as a consumer, you can get up to 1.25% interest. This is the type of account where you can take the money out the same day or wire it out. Another benefit the bank can offer is no ATM fees. In other words, you can use it like a real bank and get a good amount of interest. I myself have a checking account with BofI because it makes sense to have one – why leave money on the table and have a checking account with Chase or Wells Fargo that pay either zero or little interest, especially with the low interest rates today? BofI has been able to do that, and it’s been a strength in its business.

Another good thing is that the deposit base is throughout the whole country, in all regions of the US. If one region has an issue economically, people may get worried and make a run on their deposits at a local branch, but BofI doesn’t have that risk.

With this company, the moat is the fact that it has been able to keep its costs low. There is also the fact that it is a great capital allocator. Evidence of that are the much higher returns BofI has been able to generate compared to most banks: its return on assets at the end of 2017 was 1.79% versus 0.85% for its peers, which puts it in the top 10% of all banks with assets of $1 billion or more. Even when you consider the largest banks in the country which have such great scale that they’re able to get the best returns, BofI ranks high up there. And it’s not just in return on assets and return on equity: it is in the top 20% in G&A and the top 6% in terms of the efficiency ratio, which is an essential ratio for banks.

One of the reasons BofI has been able to do this is because it is a disruptor and has been one for a long time. Legacy banks can’t copy its business model because they have so much infrastructure in place (bank branches and employees), and they can’t compete with themselves and launch their own online-only banking subsidiary or segment. If they do, they will be faced with the issue of whether to brand it separately, which would mean not using any of the brand advantage they’ve built over the years. If they decide not to associate the two, it could create different issues. In short, it’s hard to be a mix of two bank models if you’ve been doing it one way for a long time.

Majmudar: Allow me to add that the efficiency ratio represents non-interest operating expenses divided by the income of the bank., lower is better. People generally consider below 50% to be quite good. Peers are above 50%, and BofI is well below 50% (just under 33%) because of the structural difference in its business model.

Namiri: In terms of its competitive advantage, BofI has done an excellent job and continues to do it in finding new products and relationships it can build upon. For instance, it gets a lot of its mortgages (single family mortgages) through a relationship it has with Costco. Whenever a Costco customer wants to do a mortgage through Costco, the lead gets sent over to BofI, which underwrites the loan and its bankers deal with it. There is also the deal with H&R Block, which used to have a bank and was either forced to or decided to sell off that banking division. BofI runs four different products for H&R Block and gets paid a fee, so this has been a nice income generator for the bank since 2015.

One of the impressive things about BofI is that it has been able to grow its assets quickly but do so with good credit quality and while making sure it doesn’t have high loan losses. The bank focuses on that: when you go and talk to its underwriters, you’ll see that the first thing isn’t how many loans they can process in the long run but how to make sure they are getting enough information on the borrower to be comfortable that he or she will be able to pay back. If a situation arises where the borrower can’t repay, the underwriters make sure the asset value is so high and the LTV ratio so strong that if the bank has to foreclose on the asset, it will still get the money. The bank has a lot of checks and balances in place, not only culturally but also structurally. With the jumbo loans, it is strict in terms of the markets and only lends to dense markets. That’s because when it looks at the appraisal value, it doesn’t want it to be based off comps which aren’t relevant. In a dense market, there will usually be enough sales of a related property nearby to make the appraisal value more accurate. If you go to a small town, for instance, there may be certain issues with that one piece of land or piece of property that the appraisal value doesn’t capture.

The bank looks at new products in two ways. Sometimes, it looks at building them organically and testing them in small amounts. If it sees that the product is not competitive or it can get good risk-adjusted returns, it will go and hire a team that’s been doing it longer and has a strong track record of small loan losses and loan charge-offs. BofI did that with the C&I lending, acquiring the team that had been doing it for a long time in a bank which considered this an insignificant part of its business and not worth keeping it around. Total net charge-offs annualized are 0.07 for BofI against 0.26 for comparable banks, making this another area where BofI is best-in-class. Then, the amount of loans that are in non-accrual to total loans is 0.38 for BofI compared to 0.78 for peers. Even after the Great Recession, BofI’s net charge-off never went above 1%. Going into 2008, it was not writing many loans because it felt that lots of people were chasing loans and writing them at poor risk-adjusted returns. BofI chose to sit on the sidelines and have its money in a lot of Ginnies and Fannies. One of the reasons it was able to survive during that time was because it didn’t chase these poor loans. The peak in charge-offs was just under 0.8% in 2011, which was when the worst of the foreclosure crisis was going on in the U.S.

When speaking about strong capital allocation, it feels appropriate to bring up something CEO Greg Garrabrants told the San Diego Union Tribune in 2010: “As organization failed, we hired the best.” The article was about how BofI managed to hire the teams of two of the better performing lenders in two different industries. When it got into the jumbo home loan market in 2010, there was a company called Thornburg Mortgage (TM). It went bankrupt after the financial crisis not because it wrote poor loans but because the securitization market for home lending dried up during that time, so it wasn’t able to fund any new loans. TM had all these employees and all this overhead, and it was writing loans and then, all of a sudden, it couldn’t write any more loans because it didn’t have any more funding for them. The company went bankrupt, and BofI was able to purchase loans from TM. What’s more, it was able to cherry-pick the best ones because TM was in a funding crisis and needed to get as many forms of funding as it could for new loans, so it had to sell off only the best loans because nobody wanted any of the worst loans it had. BofI effectively continued the same strategy TM had employed – writing low LTV loans in prime housing markets – but because BofI uses deposits for its funding, it avoids the risk that pushed TM into bankruptcy. In 2010, BofI effectively had zero jumbo loan production, but it reported $324 million in jumbo loans in the March 2018 quarter. The company also revealed an average FICO score of 713 and LTV of 59.2%. The latter means that if a borrower doesn’t pay back a loan, BofI effectively has more than a 40% cushion on the value of the property that it can drop before the bank loses money.

Another example of hiring the best whenever it has the opportunity is Morgan Ferris, who came on board when BofI entered the multifamily loan market in 2010. Ferris was formerly with Commercial Capital Bancorp, which was acquired by Washington Mutual for $1 billion. BofI brought him in to oversee and develop that product. The bank had $141 million in multifamily loans in the March 2018 quarter. The stats here are also quite impressive: the LTV is 56.2%, and the debt service coverage ratio is 1.32. The total multifamily loan portfolio has grown to $1.75 billion from zero in 2010. This goes to show the bank is not only doing a good job of growing its loan book in those two segments, but it is also keen on keeping strong credit statistics on its loans.

Another example is the entry in the auto lending market. In the second quarter of 2016, the book was $20 million and had grown to just under $100 a year later. Today, the size of the auto lending book is just under $200 million.

Since 2011, BofI has grown its business through three categories: a new product, a new distribution channel, and M&A. It has been opportunistic in all three different areas. It was doing H&R Block franchising lending, and in 2017, it added refund advance for H&R Block. This gave it a new product to offer H&R Block customers who wanted to receive their tax refund in advance, and then BofI would effectively have the right to their tax refund once the customer received it. Upon that relationship, the bank was able to build a new distribution channel. One area of growth it sees going on in the future is cross-selling other products it has to H&R Block customers who have never heard of BofI before.

Majmudar: We see these developments as a sign of the quality of the culture and the management. The company leaders are smart and opportunistic about finding opportunities and incrementally growing in all these three different ways.

Namiri: BofI doesn’t give guidance but provides targets it internally looks for, typically net interest margin targets and return on equity. When we look at BofI and try to figure out what future value we place on the business, we typically look out at least two years. Assuming the lower end of its net interest margin targets (380 to 400 basis points) and assuming the company can grow its assets by 15% annually over the next two years (which it has been able to do and which we consider pretty conservative), we get a $3.10 EPS estimate in fiscal 2019. We think BofI can increase that to $3.50 EPS in fiscal 2020. The top 30 comparable banks (of approximately the same market cap, loan and asset size) are trading at an average of 18.45x next year’s PE and 17.76x the two-year forward PE. However, these other banks have a projected average ROE of 8.9% and ROA of 1.1%, while the respective figures for BofI are 17.5% and 1.8%.

Using that $3.50 EPS and giving it an 18x PE multiple – which seems quite reasonable because of the ROE and ROA BofI generates versus its competitors – we get a $63 per share price target in two years, which is a 45% gain over that time. BofI also expects to have $180 million in excess capital by the end of fiscal 2019. CEO Greg Garrabrants mentioned in a recent call he intends to deploy that via a buyback, dividend, or M&A, or a combination of the three depending on where he feels he’ll get the best risk-adjusted returns.

I think there’s even more upside opportunity. The bank has been working on the so-called Universal Digital Bank initiative and has spent a lot of money developing it. It’s close to being finished and will connect all the different lines of lending, the different deposits, and other consumer-facing accounts so the company can start cross-marketing and cross-selling. If, for example, you have a single family loan with BofI, it may find you would be a good candidate for an unsecured consumer loan and can start targeting you effectively. It makes sense on all ends and is one thing the bank didn’t have in the past. It may help to grow the business at an even faster pace.

I think it’s important to note that BofI has had short attacks on its business starting sometime in 2015. Some anonymous Twitter characters would have these impressive, lengthy Seeking Alpha write-ups that cherry-picked things, for example, some of the single-family jumbo loans BofI had given in the past. When you read them, and when you don’t know the bank or you don’t know banking well, it scares you and works on your emotions. People could say something like, ”Oh, wow, I don’t want to touch a business that has given a loan to somebody who has been in jail.” These writers did a good job and have done it with other businesses in the past. I think the main reason they are doing it is not necessarily to point out some issues the bank has but to make regulators go look at it and to do a deep dive where they may not normally do. The company has gone through three audits since then and these Seeking Alpha write-ups also triggered class action lawsuits against the company.

As an investor, such things leave you questioning whether it’s worth being invested in this business. Both Ken and I have known this company and its management for many years, and Ken in particular has invested in banks for a long time, so he’s able to take things apart and see what matters and what doesn’t. More recently, there was an article about BofI making a loan to Jared Kushner’s family company; it said no one else wanted to give a loan to this family, but BofI was willing to do it. The piece questioned the management, saying it was doing a poor job overseeing the loan book. In reality, when you look at that specific loan, you see the LTV was so low that the bank covered a lot of the risk in lending to that specific project. In addition, it was getting an extremely high interest rate, which again compensated for the risk it was taking to some degree.

The short attack articles are among the reasons we believe to be behind BofI’s currently favorable multiple given the quality of the business based on ROE and ROA and the growth the company has been showing and will continue to show, in our opinion. Before these articles appeared, BofI was getting multiples of 25x to 30x PE multiple versus today’s 18x. The risk here is that the short continue to attack – the short interest in the stock is still quite high, and that is a risk we’re aware of. We think it is unfounded, but it can work on human emotions and drag the stock down, at least in the short run.

Our model also assumes the historical credit performance of BofI stays at least flat and doesn’t uptick. If there’s an economic downturn, it may become an issue for the bank, as may a real estate crisis where the value of the real estate drops in excess of 40%-50%. Also, our model assumes BofI can grow assets by 15% a year, but it may not be able to do that. Additionally, it will have to grow the deposit base to some degree, which would be another risk if it can’t do it. It has shown itself capable of achieving both in the past, and we believe it will continue to do it in the future.

Besides, it will have around $180 million to $190 million in excess capital to deploy in about a year, and there’s a risk it may deploy it poorly. However, it has such a strong track record of not doing it – it waited patiently on the sidelines during the Great Recession for another opportunity to deploy capital. It makes sense to expect it will be patient again and act opportunistically.

Majmudar: Let me sum up by saying BofI is a position we’ve held for a long time, buying in at a time when this was a much smaller company. It’s the type of company we’re looking to put into our micro-cap fund. We also think it is absolutely not too late for other investors as this remains a compounding machine that has a long way to go, in our internal view.

John Mihaljevic: Guys, thank you so much for taking the time to share your thesis in such great detail. We truly appreciate it, and I think it will be quite valuable to our community. For those who would like to track this idea over time, what would be some data points on the fundamental side to either validate or challenge your thesis?

Majmudar: Fundamentally, you look at things like net interest margin and the efficiency ratio, as well as the credit loss statistics. Those, in my opinion, are the key ones for banks. Another one is the growth in assets and liabilities.

Those five statistics have been good at this bank, not only on growth but in the quality of that growth and efficiency. We think this is a far above average bank trading at a average multiple. It’s about a $2.5 billion company, so it can still keep doing what it’s doing and grow a lot larger as it maintains the culture and the quality and should be worth far more down the road.

Then we have things like technology and all the innovations, such as the concept of the digital universal bank. With such innovations coming in, it will only become a more fruitful area for a smaller bank to use technology to grow. There’s still a lot of potential in fintech, which is an area that has had all venture capitalists truly excited in recent years with things like cryptocurrencies, for example. Here you have a publicly traded bank that’s innovative and already profitable, so we think it should be trading at a higher multiple, and it will probably have higher EPS and book value two, three, or five years from now.

The following are excerpts of the Q&A session with Kaushal Majmudar and Sam Namiri:

Q: Are there public comparables you would say are similar in terms of their approach and technological advancement?

Namiri: I found some in the micro cap space that are effectively startups, but I’ve never found a bank that lends out its own money and writes its own loans. I found certain comps that have one part of the technology aspect, but not actual banks.

One of the things BofI has developed is an API allowing a fintech company to open a bank account pretty quickly using the API. BofI struck a partnership for a product called MaxMyInterest, which determines what checking accounts consumers should use to get the highest interest rate but also keep their money FDIC-secured.

But to go back to your question, I don’t think there are any comps like BofI – I haven’t found anything that is online-only and able to generate the quality of loans and the quality of deposit base BofI have.

Majmudar: Any bank of this size – $5 billion to $15 billion asset range – is the comps people look at. The difference is that virtually all of them have physical branches. In a sense, they’re all banks, but this one is quite different from the rest. Outside of BofI, you can look at other innovative financial companies (LendingClub comes to mind) that are doing pieces of this.

Depending on your view, on what you’re looking for in a comp, it could be the other banks of a similar size. But in terms of a bank doing things the way BofI is doing, it’s quite unique, which is part of what makes us quite excited about what this idea represents.

About the instructors:

Kaushal “Ken” Majmudar, CFA founded Ridgewood Investments in 2002 and serves as its Chief Investment Officer focusing on managing long-term Value Investing based strategies. Ken’s high level experience and work with clients has been recognized and cited on multiple occasions. He is a noted value investor who has written and spoken extensively on the subject of value investing and intelligent investing. Prior to founding Ridgewood Investments in late 2002, Ken worked for seven years on Wall Street as an investment banker at Merrill Lynch and Lehman Brothers where he has extensive experience working on initial public offerings, mergers and acquisitions transactions and other corporate finance advisory work for Fortune 1000 companies. He has been a member of the Value Investors Club – an online members-only group for skilled value investors founded by Joel Greenblatt – where he posted a buy recommendation on Nvidia in 2002 – possibly one of the best long-term investment ideas ever posted on VIC. He has also been a member of SumZero – an online community for professional investors, and written for SeekingAlpha – among others. Ken graduated with honors from the Harvard Law School in 1994 after being an honors graduate of Columbia University in 1991 with a bachelor’s degree in Computer Science. He is admitted to the Bar in NY and NJ, though retired from the practice of law, as well as a member of the CFA Institute and EO (Entrepreneurs Organization).

Sam Namiri recently joined Ridgewood to help build its Small and Microcap investments and will be co-managing the Ridgewood Select Value Fund with Ken. Prior to Ridgewood, Sam spent five years as an associate at Grand Slam Asset Management, a small cap value based Hedge Fund. Sam graduated with a bachelor’s in Industrial Engineering and Operations Research from UC Berkeley in 2005 and an MBA from Columbia Business School in 2012.

NOTA DEL EDITOR: Estas ideas de inversión presentadas por Marc Garrigasait, son obtenidas de una carta del fondo Japan Deep Value Fund.

* * *

“Cuanto más simple, más me gusta ese negocio para invertir. Cuando alguien dice: Cualquier idiota podría llevar este negocio, es un punto a favor para mí, pues probablemente tarde o temprano algún idiota terminará llevando el negocio.”

Peter Lynch, Un paso por delante de Wall Street

Peter Lynch, uno de los mejores gestores de fondos de inversión de la historia, con unos resultados excepcionales desde 1977 hasta su retiro en 1990 en el fondo Fidelity Magellan, nos regaló sus vivencias y consejos en varios libros rompedores y muy entretenidos. Los atributos que considera a la hora de señalar una empresa como una perfecta opción de inversión son muy transgresores con respecto al consenso. Alcanzar rendimientos superiores de forma sostenida sólo es posible haciendo las cosas de manera distinta. Muchos de estos atributos coinciden fielmente con los de nuestra cartera. Los enumeramos a continuación: Continue reading »

Thousands of years ago, before the use of horses, Native Americans utilized a hunting technique that preyed on animalistic instincts. This technique was called the buffalo jump. Hundreds of buffalo could be killed at a time without the use of weapons.

Thousands of years ago, before the use of horses, Native Americans utilized a hunting technique that preyed on animalistic instincts. This technique was called the buffalo jump. Hundreds of buffalo could be killed at a time without the use of weapons.