This article is authored by MOI Global instructor Phil Ordway, managing principal of Anabatic Investment Partners.

As regulatory frameworks, the yield curve, technology, and the competitive landscape are shifting, now is a good time to explore the banking industry for possible opportunities. Many investors relegate banks to the “too-hard” pile or label them all as “black boxes” that are unsuitable for conservative value investors. And there certainly are some banks that are too complex, too thinly capitalized or too poorly managed to offer favorable prospects to investors. But out of the thousands of banks in the U.S. and Europe there are often at least a handful that offer outstanding investment potential.

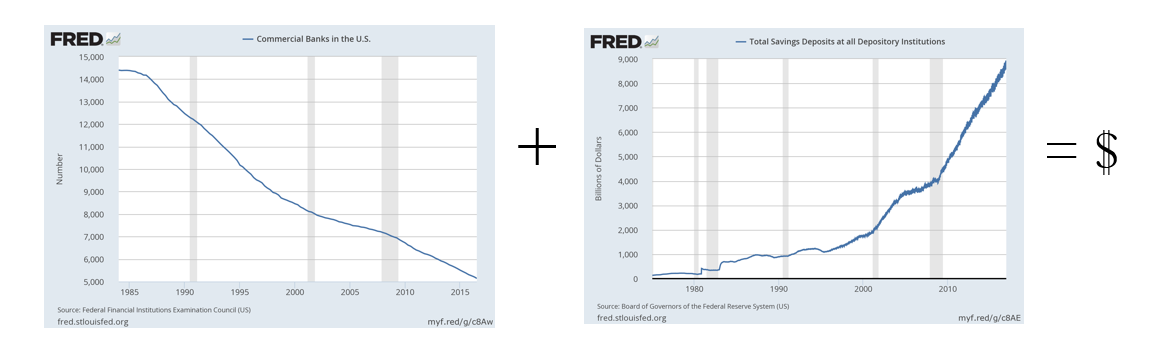

One key to understanding banks is the nature of their deposit base. The amount, cost and quality of these liabilities determine a bank’s safety and soundness as well as its ultimate profitability. Deposits are the “raw material” for banks, and a good deposit-gathering franchise can make for a very valuable business. And while all banks are levered, many capital structures are actually quite stable. Total deposits in the U.S. have exhibited remarkable consistency, growing almost every year since the Great Depression and often outpacing GDP growth. At the same time, U.S. banks have purged their problem assets and retained much more equity capital. My presentation at Best Ideas 2017 will argue that the quality of the U.S. banking sector’s aggregate capital and liquidity make the industry as safe as it has been in decades.

Another focus areas for investors is the quality of a bank’s assets. If deposits provide the “raw material” for a bank, it is up to management to then make intelligent capital-allocation decisions. The credit culture of a bank is crucial, and it must be judged both quantitatively and qualitatively. A few phone calls or meetings to find out which bank in a given market is stretching on terms or price will go a long way in avoiding future problems. In banking, an ounce of prevention really is worth a ton of cure.

A third factor driving returns for investors is consolidation. The total number of commercial banks in the U.S. has declined almost linearly from more than 14,000 in 1985 to approximately 5,000 today. Across the broader industry, M&A has – with very few interruptions – continued every year for decades. In a typical year, 2-4% of the banks in America are acquired by other banks, and essentially zero new banks have entered the industry in the past decade.

Some particularly interesting opportunities are often found in the small “community” banks that comprise the vast majority of the 5,000 U.S. banks in existence today. Some of them are attractive businesses, some may have quantitatively cheap stock prices, and some might be candidates for acquisition; the combination of those factors can make for a sound and profitable investment.

As with other investments, it is often helpful to look at the problem upside down. By developing a framework to eliminate certain banks as candidates for investment, the potential universe shrinks dramatically and the potential for good risk-adjusted returns improves. Investors should often avoid banks with thin capitalizations, aggressive managers, high-cost “non-core” deposits, a concentration in out-of-market loans, a lot of opaque assets, or a bloated cost structure. My presentation will walk through some benchmarks and resources in each of those areas.

My presentation will also explore the banking industry’s history, business model, accounting, capital allocation decisions, and competitive landscape, along with some unique situations such as “demutualizations.” At the end of my presentation will be two case studies. One features a century-old community bank that has recently completed several acquisitions and may be a merger candidate itself, and the other features a well-known large-cap bank.

About The Author: Philip Ordway

Philip Ordway is Principal and Portfolio Manager of Anabatic Fund, L.P. Previously, Philip was a partner at Chicago Fundamental Investment Partners (CFIP). At CFIP, which he joined in 2007, Philip was responsible for investments across the capital structure in various industries. Prior to joining Chicago Fundamental Investment Partners, Philip was an analyst in structured corporate finance with Citigroup Global Markets, Inc. from 2002 to 2005, where he was part of a team responsible for identifying financing solutions for companies initially in the global power and utilities group and ultimately in the global autos and industrials group. Philip earned his M.B.A. from the Kellogg School of Management at Northwestern University in 2007 and his B.S. in Education & Social Policy and Economics from Northwestern University in 2002.

More posts by Philip Ordway