This article is authored by MOI Global instructor Keith Rosenbloom, founder and managing member of Cruiser Capital, based in New York City. Keith is an instructor at Best Ideas 2018, the fully online conference featuring more than one hundred expert instructors from the MOI Global membership community.

Listen to Keith’s session at Best Ideas 2018.

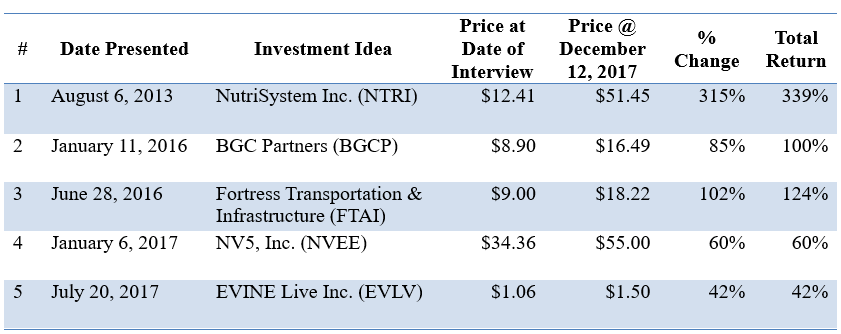

At Cruiser Capital we pride ourselves on being differentiated value investors. We have presented five times at online conferences hosted by MOI Global in the last four-and-a-half years, and our coming presentation on January 8th will be our sixth. Our previous discussions have related to investments we were making in attractive businesses with sound protective moats. The investments discussed with the dates of the presentations and the share prices at the time of presentation and at December 12, 2017 are shown in the chart below:

Recently we closed out of one of the investments, we intend to close out of another one and have reiterated our enthusiasm and positioning on the others. We will address each of those in our discussion on January 8th prior to discussing another investment and our thinking on various market opportunities.

What Compels Us To Invest:

Four key characteristics ultimately drive our willingness to invest in a given company.

1. Management Credibility

2. Clearly Defined, Easily Understood Growth Plan

3. Well Utilized Balance Sheet

4. Organic Exit Strategies

Management Credibility

At the core of every investment is the capability of the people who are going to execute the plan. We believe great managers make average situations great and poor managers make great situations poor. We’re quite aware that the definition of “great” can be backward looking and hard to evaluate prior to a manager doing “great things.” This is why we think it’s critical to research the backgrounds of the management teams you are investing with. We are consistently surprised (and often amused) when we see investor presentations and research reports that fail to discuss the qualifications of the management team.

One objective item we find useful in our evaluations of determining the caliber of management is whether their compensation is aligned with shareholder success. We like investing with teams who win when the shareholders win. A case in point is when Sealed Air Corporation (SEE) hired Jerome Peribere to become CEO 4 ½ years ago. When Jerome became the CEO of SEE the company’s stock price was under $15 per share. He took the vast majority of his compensation in 3 and 4 year RSUs exercisable only if the stock was $30, $35 and $40. When he retires on December 31, 2017 the stock will be close to $50.

We are motivated to invest with management teams who are motivated with an owner operator mentality.

Clearly Defined, Easily Understood Growth Plan

We find it’s important to remember basics: an aphoristic rule is that it’s hard to make money when you don’t know what you’re trying to do. We like to evaluate business plans that require straightforward blocking and tackling. And ultimately we like to invest when the “degree of difficulty” is low.

Frankly, one of the benefits of investing in turnaround situations is you get the opportunity to invest with great, new managers who are articulating a clear path to improved profitability. The bonus is that in turnarounds you are often getting those opportunities at value prices.

Well-Utilized Balance Sheet

At Cruiser we believe that balance sheet’s drive income statements, not vice-versa. We know that is an “old school mentality” – particularly in today’s environment of “easy money” – but today’s access to capital only underscores the point. With money cheap, you want to invest with managers who can generate a tangible Return On Invested Capital.

For those of us in the US who question how easy money is, we point to the European capital markets. For example, on November 23rd the French company Veolia Environnment SA issued three year zero coupon debt with a re-offer price above par. Per Grant’s, “…three year bonds priced to yield negative 0.026%%. Even better: Investor demand for the Veolia issue was such that the offering was oversubscribed by more than 4:1. Said another way, three out of four investors who wished to lose money on a yield-to-maturity basis were left disappointed.” The reality is when there’s $11 trillion in sub-zero/negative yield debt in the world, and the average dividend yield on the S&P 500 is below 2%, it’s easy to conclude we are still in a low rate environment. It’s our view that we will continue to be for some time.

Organic Exit Strategies

We invest with companies that often compete with larger players either directly or in adjacent markets. It’s clear often, particularly given the ultra-low cost of capital, that these companies should be a part of those larger players.

We like to clearly understand the competitive field so that when a company gets to a certain size, or achieves a particular milestone, it becomes evident that multiple paths to continued success exist. Sometimes that is becoming a part of a larger entity, often it is by buying a division or operating unit from someone else. And sometimes it means entering an adjacent market with an inherent competitive advantage.

How Today’s Capital Markets Impact Our Thinking

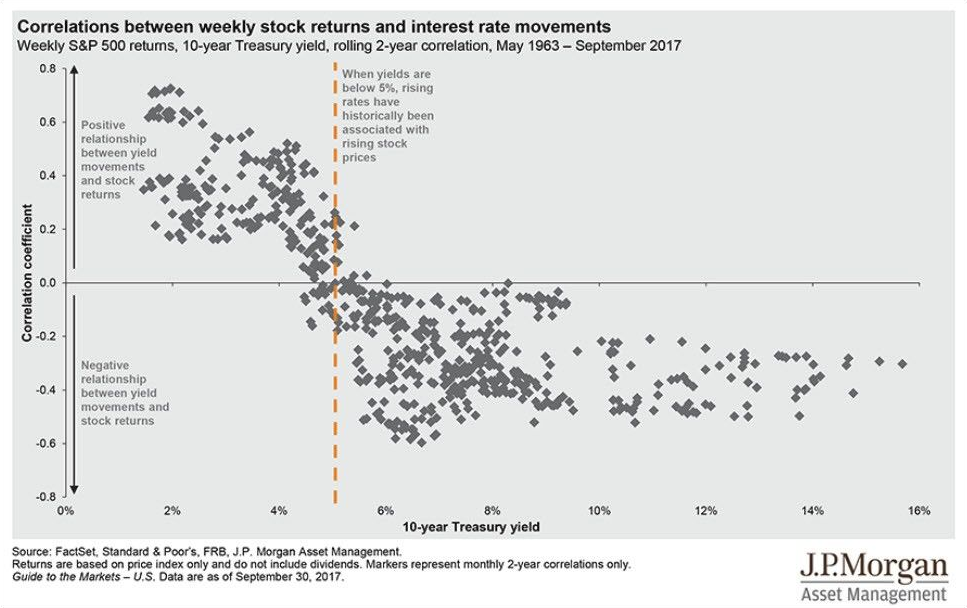

Literally every day for the past 8 years there is an article or talking head speaking about the risk to markets from impending rising interest rates. And yet, the data from May 1963 until today supports that measured increases in interest rates from low bases, specifically below 5% have historically been associated with rising stock prices.

An intriguing potential outcome in the current economic and political environment is the real possibility that for the first time in many years the US economy will have fiscal spending to accompany its easy monetary policy. With the backdrop of Hurricane’s Harvey and Irma, the devastation in Puerto Rico, bi-partisan discussion on intermodal infrastructure spending, etc., should fiscal spending occur, the earnings outlook for many of the companies we follow and like will dramatically improve.

An integral part of our mission at Cruiser is to determine the difference between value opportunities and “value traps.” When we find value opportunities we want to own them, and when we find value traps we usually short them.

But “value opportunities” are much more than companies simply trading at “cheap multiples.” They have inherent characteristics which computer driven algorithms cannot screen for; specifically we believe that quality people executing on well determined business plans can create enormous value.

We actually think it is advantageous to Cruiser that the majority of public companies with market caps under $10 billion have 30% or more of their shares held by rule based index funds who – by their mandates — don’t meet with management teams or model out businesses. We think this provides a target rich universe of potential investment opportunities for Cruiser.

Please note that per the Cooperation Agreement Cruiser Capital executed with A. Schulman (SHLM) in September 2017, we ask you to please appreciate that nothing contained herein is intended to be derogatory, or critical of, or negative toward Schulman or any of its past or present officers or directors. All information provided herein is for informational purposes only and shall constitute an offer to sell any securities or constitute a solicitation of an offer to purchase any securities. Any such offer to sell or solicitation of an offer to purchase shall be made only by formal offering documents, which include, among others, a confidential offering memorandum, limited partnership agreement, subscription agreement and related subscription documents. Such formal offering documents contain additional information not set forth herein, which such additional information is material to any decision to invest in Cruiser Capital, LLC (the “Fund”). The confidential offering memorandum contains additional information, including information regarding certain risks of investing which are material to any decision to invest in the Fund. Performance data and risks are historical and are not indicative of future returns and is no guarantee of future results. The performance reflected herein and the performance for any given investor may differ due to various factors including, without limitation, the timing of subscriptions and redemptions, applicable management fees and incentive allocations, and the investor’s ability to participate in new issues. Much of the performance results reflected herein is unaudited, is based on incomplete information and is subject to change. Actual results, when available, may differ. There is no guarantee that the Manager will be successful in achieving its investment objectives. All investments involve risk including the loss of principal. Past performance is not necessarily indicative of future results. This transmission is confidential and may not be redistributed without the express written consent of Cruiser Capital Advisors LLC. The Standard & Poor’s 500 Index (the “S&P 500”), the Russell 2000 Index and the HFRX are referred to only because they represents indices typically used to gauge the general performance of the U.S. securities markets. The use of these or any other index is not meant to be indicative of the asset composition, volatility or strategy of the portfolio of securities held by the Fund. The Fund’s portfolio may or may not include securities which comprise the S&P 500, will hold considerably fewer than the number of different securities which comprise the S&P 500 and engages or may engage in strategies not employed by the S&P 500 including, without limitation, short selling and utilizing leverage. As such, an investment in the Fund should be considered riskier than an investment in the S&P 500. Furthermore, indexes are unmanaged, do not incur management fees, costs, and expenses, and cannot be invested in directly.

About The Author: Keith Rosenbloom

Keith Rosenbloom has over 25 years of direct investing experience, with a focus on applying traditional private equity value oriented perspectives to both special situations and structured investments. Keith co-founded and managed the CARE Capital Group of Hedge Funds from 2002 to 2010. Since then he has managed discretionary capital and invests opportunistically in public and private entities. Previously he served as the Portfolio manager of the CAR Fund and co-managed Comvest Venture Partners. He served as the Director of Merchant Banking for Commonwealth Associates from 1996 to 2001 where he specialized in making primary investments in public and private companies (approximately 80 transactions representing approximately $800mm). Keith became a Partner at Commonwealth Associates in 1994. Previously Keith worked with Prudential Capital and Merrill Lynch Venture Partners. He has invested in or managed investments in over 100 hedge funds and private equity funds. Keith currently sits on the board of PAWSAFE, LLC, a private pet health insurance distribution company. In addition, he serves on several charitable boards including UJA -Federation of New York, Hillel International (Board of Governors), Hatzalah (Israel's private EMT service) and serves on the investment committee for Hillel International. He also serves on the investment committees of two family offices. He graduated cum laude from Yale University.

More posts by Keith Rosenbloom