This post has been excerpted from a letter by Michael Winer, Jason Wolf, and Ryan Dobratz, Lead Portfolio Managers of the Third Avenue Real Estate Value Fund.

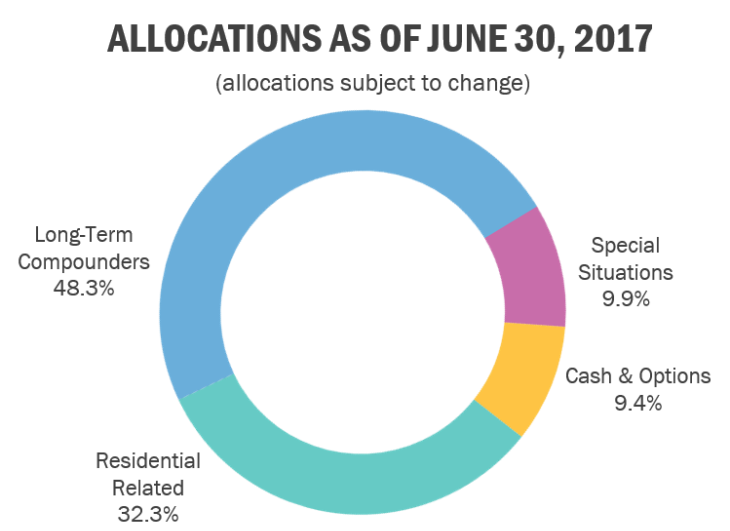

At the end of the quarter, the Fund had approximately 48% of its capital invested in property companies that are involved in long-term wealth creation. These holdings primarily include: Cheung Kong Property, Land Securities, Forest City Realty Trust, Westfield Corp, Brookfield Asset Management, Vornado Realty Trust, Wheelock & Co., and Henderson Land. Each of these enterprises is incredibly well-capitalized, trades at a discount to NAV, and seems capable of increasing NAV by 10% or more per year (including dividends) through further appreciation in the value of the underlying assets, as well as by undertaking additional development and redevelopment activities and by making opportunistic acquisitions.

The Fund also has 32% of its capital invested in real estate related businesses that have strong ties to the US residential markets, such as timberlands (Weyerhaeuser & Rayonier), land development (Five Point and Tejon Ranch), homebuilding (Lennar Corp), title insurance (FNF Group) and home improvement (Lowe’s). All of these businesses seem poised to benefit from a further recovery in housing fundamentals particularly from an increase in the construction of single-family homes and higher levels of residential purchase activity in the US.

An additional 10% of the Fund’s capital is invested in special situations such as Millennium & Copthorne in the UK, Trinity Place Holdings and the Bank Debt of Neiman Marcus in the US. Colonial was previously part of the special situations allocation.

The remaining 9% of the Fund’s capital is in cash & equivalents (e.g.., short-term US Treasuries). The Fund continues to maintain its hedges on the Euro and Hong Kong Dollar exposure, and implemented a hedge on the Singapore Dollar related to its position in Global Logistic during the period.

As we begin the third quarter of 2017, the Fund’s cash balances are gradually increasing. Factoring in the expected “cash-out” transactions at GLP and Parkway, the Fund’s cash balances would be approximately 16%. This is the highest amount of “dry-powder” the Fund has had since August 2015. In our view, this puts the Fund in a more defensive position and provides the resources to capitalize if there is a broader market dislocation. In the meantime, Fund Management continues to sift through two areas of the global real estate universe which have experienced significant pressure over the past year: UK-centric property companies and retail-related real estate businesses in the US.

In the UK, the Fund put substantial capital to work in a select set of UK REIT’s following the unexpected results of the referendum held in June 2016 In the days after “Brexit” became a reality, most UK property companies declined by 20% or more (in US Dollar terms). The Fund took advantage of the panic and increased its exposure to the UK to nearly 13% of Net Assets (largely by adding to Land Securities, Segro, and Hammerson). It was our view at the time that all three UK REITs were very well-capitalized and trading at substantial discounts to NAV, despite owning irreplaceable portfolios in and around London, one of the best property markets for long-term investors. Since that time, conditions have stabilized and certain positions have been trimmed back given their strong performance (e.g., Segro).

Fund Management was more cautious on UK companies that have (i) large-scale speculative development pipelines underway where rental rates were likely to be cut to entice tenants, (ii) residential-led redevelopment projects where prices were already declining from highs reached in 2015 and unlikely to be as profitable as previously budgeted, and (iii) portfolios that were appraised at very low cap rates (i.e., initial yields) because of substantial rental rate growth assumptions which were likely to moderate significantly.

More than a year out from the initial “Brexit” shock, we have seen weakness in some of the businesses within these areas, particularly those with assets appraised at low initial yields that are now increasing to offset reduced rental rate growth assumptions and a higher 10-year yield in the UK (thus declining property values). As a result, Fund Management is spending more time analyzing the securities of some of these issuers. A number of these businesses control hard to replicate portfolios, especially in the West-End sub-market of London that can be spectacular investments over the long-term if purchased at suitable prices.

In addition to the UK, Fund Management continues to spend considerable resources analyzing securities related to retail real estate in the US. The Fund has gradually increased its investments in companies that control market-dominant malls, such as Westfield and Macerich, which we believe are well positioned given (i) the accelerated demise of tertiary properties and (ii) the increasingly critical nature that these large destination centers play in retailers’ “omni-channel” business models.

During the quarter, the weakness in retail spread further as Amazon announced its intentions to purchase Whole Foods and expand its grocery offering. After the news, there was a significant sell-off in all related businesses including US shopping center REITs that own grocery-anchored strip centers and power centers.

At quarter end, the Fund did not have any investments in companies that focused exclusively on these necessity-based centers. However, just as we witnessed in the late 1990’s and early 2000’s with Wal-Mart’s aggressive expansion, strong retailers adapt to a more competitive environment and well-located shopping centers continue to act as an essential point for the distribution of goods (which seems to have been confirmed further with Amazon’s desire to add 400 urban locations in its Whole Foods purchase). With that as the backdrop, we expect to unearth some shopping-center related opportunities amidst the most recent selloff.

IMPORTANT INFORMATION

This publication does not constitute an offer or solicitation of any transaction in any securities. Any recommendation contained herein may not be suitable for all investors. Information contained in this publication has been obtained from sources we believe to be reliable, but cannot be guaranteed.

The information in this portfolio manager letter represents the opinions of the portfolio manager(s) and is not intended to be a forecast of future events, a guarantee of future results or investment advice. Views expressed are those of the portfolio manager(s) and may differ from those of other portfolio managers or of the firm as a whole. Also, please note that any discussion of the Fund’s holdings, the Fund’s performance, and the portfolio manager(s) views are as of June 30, 2017 (except as otherwise stated), and are subject to change without notice. Certain information contained in this letter constitutes “forward-looking statements,” which can be identified by the use of forward-looking terminology such as “may,” “will,” “should,” “expect,” “anticipate,” “project,” “estimate,” “intend,” “continue” or “believe,” or the negatives thereof (such as “may not,” “should not,” “are not expected to,” etc.) or other variations thereon or comparable terminology. Due to various risks and uncertainties, actual events or results or the actual performance of any fund may differ materially from those reflected or contemplated in any such forward-looking statement.Current performance results may be lower or higher than performance numbers quoted in certain letters to shareholders.

Date of first use of portfolio manager commentary: July 26, 2017.

Past performance is no guarantee of future results; returns include reinvestment of all distributions. The above represents past performance and current performance may be lower or higher than performance quoted above. Investment return and principal value fluctuate so that an investor’s shares, when redeemed, may be worth more or less than the original cost. For the most recent month-end performance, please visit the Fund’s website at www.thirdave.com. The gross expense ratio for the fund’s institutional and investor share classes is 1.40% and 1.65%, respectively, as of March 1, 2017. Please be aware that foreign securities from a particular country may be subject to currency fluctuations and controls, or adverse political, social, economic or other developments that are unique to that particular country or region. Therefore, the prices of foreign securities in particular countries or regions may, at times, move in a different direction than those of U.S. securities. Prospectuses contain more complete information on management fees, distribution charges, and other expenses.

Third Avenue Funds are offered by prospectus only. The prospectus contains important information, including investment objectives, risks, advisory fees and expenses. Please read the prospectus carefully before investing in the Funds. Investment return and principal value fluctuate so that an investor’s shares, when redeemed, may be worth more or less than the original cost. For updated information or a copy of our prospectus, please call 1-800-443-1021 or go to our web site at www.thirdave.com. Distributor of Third Avenue Funds: Foreside Fund Services, LLC.

Current performance results may be lower or higher than performance numbers quoted in certain letters to shareholders.

About The Author: Michael Winer

Mr. Winer has managed the Third Avenue Real Estate Value Fund since its inception in 1998. He is also the co-portfolio manager of the Third Avenue Real Estate Opportunities Fund LP.

As a real estate securities analyst for Third Avenue in the mid-1990s, Mr. Winer convinced his colleagues that real estate should be (and in fact always had been) an essential part of the firm’s value investing arsenal. This led to Third Avenue establishing its first sector fund — a new concept for a firm whose generalist approach runs deep. Since then, Mr. Winer has played crucial roles in several unique, landmark Third Avenue investments, including the firm’s participation in reorganizing Kmart (which was in Chapter 11 bankruptcy), where Mr. Winer determined that Kmart’s real estate assets provided a substantial margin of safety for Kmart’s stakeholders.

Prior to joining Third Avenue in 1994, Mr. Winer was Vice President of the Asset Sales Group for Cantor Fitzgerald, L.P. where he was responsible for evaluating and underwriting portfolios of distressed real estate loans. He had previously been First Vice President of Society for Savings, a Connecticut savings bank, and Director of Asset Management for Pioneer Mortgage, a financial institution, where he directed the workout, collection and liquidation of distressed real estate loan and asset portfolios.

Earlier in his career, Mr. Winer was the Co-Founder and Chief Financial Officer of Winer-Greenwald Development, Inc., a California-based real estate development firm that specialized in the development, construction, ownership and management of commercial properties. Mr. Winer previously held executive positions at Pacific Scene, Inc., and The Hahn Company, both California-based real estate development firms. Mr. Winer began his career in public accounting with Deloitte & Touche (formerly Touche Ross & Co.) where he specialized in real estate development companies.

Mr. Winer holds a B.S. in Accounting from San Diego State University. He is a member of the Board of Directors of Tejon Ranch Co., a public company that owns the largest continuous expanse of private land in California and Five Point Holdings LLC, a public company with three large master-planned communities in coastal California. Mr. Winer serves on the Board of Trustees of the Future Citizens Foundation (dba The First Tee of Monterey County) and the Pacific Legal Foundation (a public-benefit law firm).

More posts by Michael Winer