This article is authored by MOI Global instructor Ankit Agarwal, Senior Vice President and Fund Manager at Centrum Capital, based in Mumbai, India.

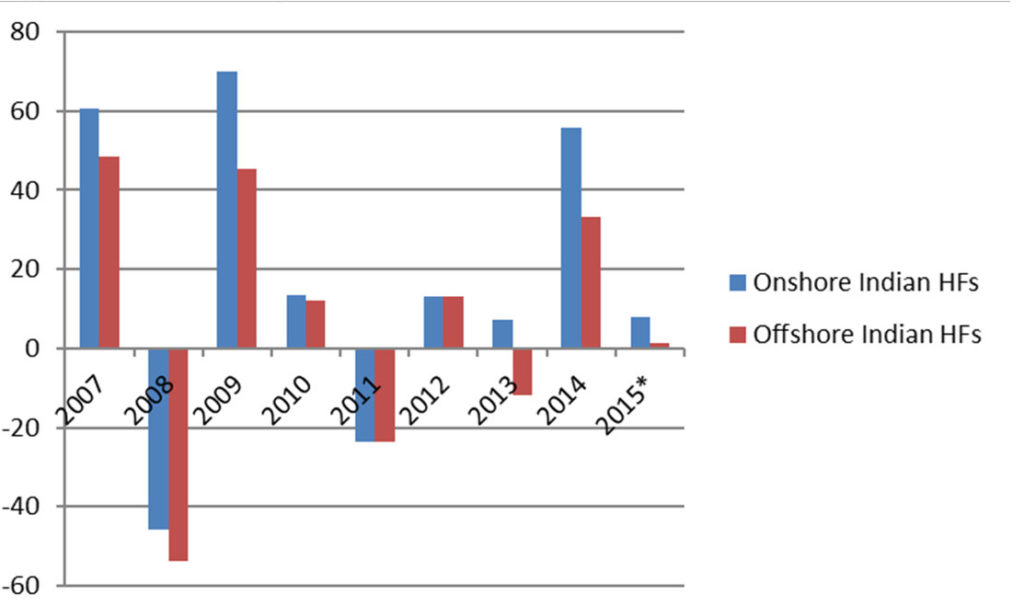

If one were to look at the performance of onshore funds versus offshore funds – the former tend to outperform the latter. Why would that be, do they have access to less information? Is the sell-side support to foreign institutional investors less than that to domestic funds?

Well, the only thing that probably differentiates an offshore fund from an onshore fund is access to information on the ground and the ability to do regular channel checks.

Figure 1: Comparison of onshore and offshore funds

Source: https://cafemutual.com/news/aif-corner/6693-onshore-hedge-fund-managers-outperform-offshore-india-hedge-funds

Source: https://cafemutual.com/news/aif-corner/6693-onshore-hedge-fund-managers-outperform-offshore-india-hedge-funds

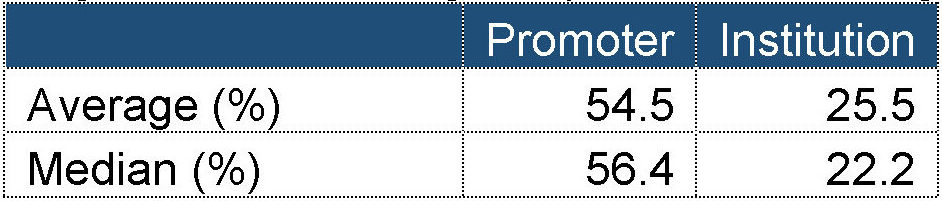

If one were to look at the structure of Indian firms – most of them are family-owned businesses where the owner, the so-called “promoter”, is the majority holder in the company. As a result, the fate of the business is linked to how savvy the promoter is, what his long-term thinking about the business is and, most importantly, how he fares on integrity.

Recent occurrences in the Indian stock market linked to some companies seeing governance issues makes the Indian equity market a minefield of possible mishaps. As a result, while the fundamentals of the company are a great starting point for investing in India, an assessment of the promoter and his integrity, is an essential component of analyzing any business.

In this article, I give a brief overview of the steps one can take to reduce the probability of some of these mishaps occurring in their portfolio.

Figure 2: Promoter holdings in BSE 500 index companies

Source: Capitaline

Source: Capitaline

First and foremost, the ability of the promoter is reflected in the way he/she manages the balance sheet and cash flows. The first cracks in the balance sheet appear when the EBITDA does not convert to cash fast enough, the leverage increases, or the company decides to make a significant acquisition in an unrelated business. There are a variety of accounting checks one can make to understand if there is any manipulation in the earnings, for example looking at the EBITDA to (pre-tax) CFO ratios (should be more than 80-90%) and depreciation rates (should have low variability).

Furthermore, high contingent liabilities, low provisioning of doubtful debts that could lead to overstatement of earnings, high capital work-in-progress, low cash taxes payouts, and low dividend payout ratios, are all red flags for the earnings. These can give an idea about the robustness of the reported numbers and also about how minority shareholder friendly the promoter is.

After we have done a thorough analysis of the capital allocation and the balance sheet of the company, one needs to look at the softer aspects. Since most of the companies are promoter-led, succession planning is an important aspect to consider. Who is going to drive the business, are the sons/daughters of the promoter involved in the business, and if so, what are their backgrounds. Many times a change of management from an old patriarch to a new energetic son could make a drastic change in the way the company is run. Companies that are heavily dependent on the promoter or have a weak bench strength have to be looked at skeptically, especially if the promoter is old.

Moreover, one needs to assess the promoter’s ambition to grow in a highly competitive market. Promoters who are overly aggressive might take shortcuts to achieve their goals and can lead to earnings manipulation. On the other side overly conservative promoter would not grow enough and may continue to remain a value play for the foreseeable future. Promoter assessment thus becomes an important metric of how companies are evaluated.

Many promoter-driven companies, as they become big, they realize that they have many stakeholders in the firm, many of whom are the sons, daughters, uncles, etc of the original leadership team, and as a result, the company starts entering multiple lines of business as per each family member’s whims and likes. A lot of these new businesses are privately held but would need capital at regular intervals to support and grow them, especially if they are in the infrastructure and real estate businesses.

It happens often that cash from the existing business is diverted into the new companies, or shares of the listed entity are given as pledge to NBFCs (Non-Banking Financial Companies – India’s shadow banking ecosystem) to raise debt to fund those new businesses. In times of stress, the lender might invoke this pledge and can cause severe damage to the minority shareholders of the listed entity.

Moreover, there are times when a part of the business is conducted under the unlisted entity, but a considerably higher cost is accounted for there, leading to an under-accounting of the costs under the listed entity, which in turn leads to an increase in the reported profitability of the company. And so one needs to assess companies with a parallel interest in other business with a fine tooth comb.

One even needs to monitor relationships with some of the companies that have related party transactions with the listed entity. Companies that have a large number of related party transactions can raise some issues concerning the arm’s length transactions that they are doing. A lot of times there could be promoter who could be lending to entities at a significantly higher lending rate (higher than the bank rate) or there could be a high royalty payment to the promoter or even the rentals that might be paid to the promoter owned building where the company resides might be prohibitively high. Related party transactions are again something that needs to examined in close detail while assessing the business.

The composition of the board and incentives of the promoters in the form of compensation, a percentage of profits or royalty payment is an essential indicator of governance. One needs to see if the board is occupied by all “friends and family” or if there are external professionals on it. If the promoter is taking out significant money from the company in the form of salary or royalty payments, then one needs to question whether is it in line with the industry and if the promoter is adding significantly to the brand value of the business such that a royalty payment is warranted. Annual General Meetings are an excellent way to know how independent the board is, who participates in its discussions, and if the others get an opportunity to interact with the shareholders.

However, at the end of the day, there is no better way to become aware of promoter intent than to talk to as many people as possible. Talk with the suppliers of the company, with the dealer distributor network as to how payments are made to them, speak with the consultants who have worked in the industry, the peers who have had the opportunity to see how they view management practices, the market participants who would have dealt with some of these companies in the past, to name a few avenues. And only once you have interacted with these or more people on the street you would understand what are the practices that are followed by the company and if they are going to create long term value for its shareholders.

In summary, promoter assessment is an essential tenet of investing in Indian markets. One should be extremely cautious when investing, especially when using a value approach, because if the promoter integrity is under question then such companies would be value traps and may not see re-rating in the future. Moreover, extremely high-growth companies are also something to be cautious about.

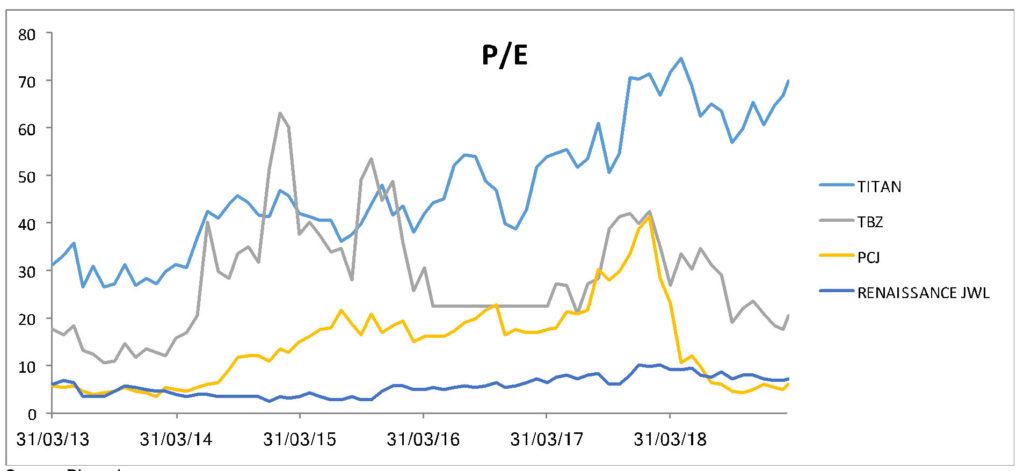

Figure 3: P/E chart for various jewelry firms

Source: Bloomberg

Source: Bloomberg

Some companies like Titan command a significant premium over their listed counterparts, and that premium has been maintained over cycles.

The gap between a well-managed asset financing company like M&M Financial and one that has a sketchy track record of performance continues to exist.

Members, log in below to access the restricted content.

Not a member?

Thank you for your interest. Please note that MOI Global is closed to new members at this time. If you would like to join the waiting list, complete the following form:

About The Author: Ankit Agarwal

Ankit Agarwal has a strong academic pedigree with MBA from IIM Bangalore and Btech in computer science from NIT Trichy. He currently works as a Fund Manager for a reputed listed financial services firm. He brings in experience in the investment management industry encompassing fund management, research, covering the equity asset class. Further, he has had diverse set of experiences in the financial services industry encompassing Wealth Management firms (Centrum, Barclays Wealth), hedge fund (D. E. Shaw & Co.), a french investment bank (BNP Paribas) operating in Hong Kong and Wall Street firm (Lehman Brothers) in London. He is very passionate about working in the industry and brings in expertise primarily in equities and derivatives. He often comes on various print and television media to give views on the markets.

More posts by Ankit Agarwal