An old gem I came across in my files: The Contango Story – A classic 4-pager on a 100-bagger in oil and gas. Should be mandatory reading for anybody in that business.https://t.co/zaa0ThMPUr

— Chris Mayer (@chriswmayer) May 11, 2019

This article is authored by Todd Wenning, senior investment analyst at Ensemble Capital Management, based in Burlingame, California. Visit Ensemble’s Intrinsic Investing website for additional insights.

“Do not go gentle into that good night. Rage, rage against the dying of the light.” –Dylan Thomas

“What do we say to the god of death? Not today.” –Game of Thrones

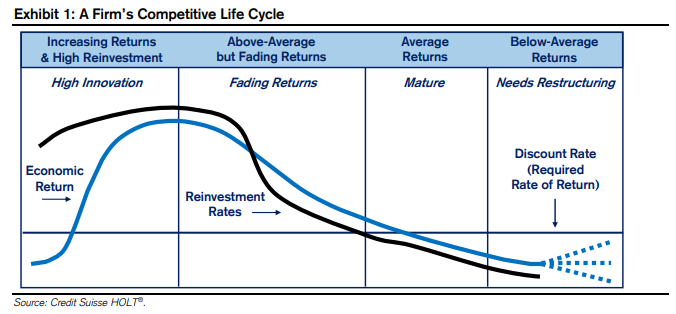

Financial theory tells us that eventually a company’s returns on invested capital (ROIC) will decay toward its weighted average cost of capital (WACC), or discount rate:

Of course, “eventually” can be tomorrow or in 30-plus years.

The difference between days and decades in a company’s competitive advantage period is massive, yet is often overlooked, as Michael Mauboussin and Dan Callahan note:

Despite the unquestionable significance of the longevity dimension (of sustainable value creation), researchers and investors give it insufficient attention.

Why does longevity get ignored? According to New York University Professor Aswath Damodaran, almost 85% of equity research reports are based on some relative valuation metric. In other words, most investors are laser-focused on what might happen over the next few quarters or years. What happens to a company in year five and beyond is of little concern to renters of stocks.

But even if you take a long-term ownership perspective like we do, it’s easy to be dismissive of competitive advantage longevity.

Let’s say you’re building a five-year discounted cash flow model to estimate a company’s fair value, your terminal value (i.e. which assumes the company operates in a defined state in perpetuity) accounts for between 70-75% of your fair value estimate. A huge swing factor.

It’s rational to assume that the good times won’t last forever. As such, prudent analysts will assume some amount of ROIC decay in their terminal assumptions. But, again, the billion-dollar question is, “How long will it take for ROIC to decay to WACC?”

Assume the decay is too rapid and you’re undervaluing the business; assume it’s too slow and you’re overvaluing the business.

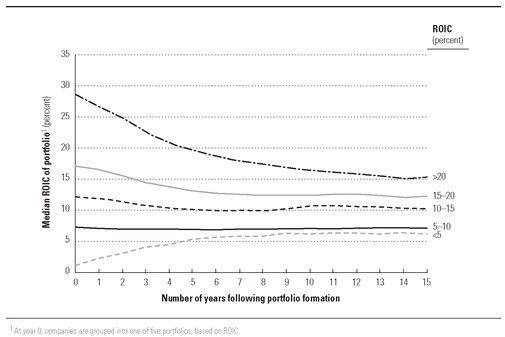

One thing we’ve noticed is that, while companies with top-quintile ROICs tend to fade toward WACC like any other cohort, they often stabilize at a rate still above WACC. Put another way, while it’s unlikely for a 50% ROIC company to sustain that level for decades, there’s a good chance it will still produce ROICs above WACC (say, in the 20% range) for an extended period. Assuming, of course, the company’s moat remains intact.

Source: McKinsey

As investors, our job is to compare our outlook with what is already baked into the market price. For example, if you think a company can generate 20% ROICs for two decades, but we conclude the market price already assumes these results, there’s no opportunity for alpha.

But because so many investors are ignoring ROIC longevity, we believe that, on average, market prices expect fade to happen relatively abruptly. To be fair, the market is right to be skeptical of extended competitive advantage periods. It’s the exception rather than the rule for companies to build moats in the first place, let alone successfully defend them for decades.

Those companies that can defend their moats, however, extend their competitive advantage period and require the market to continuously revise estimates higher. Somehow, these ROIC machines cheat natural decay and increase the company’s intrinsic value year after year.

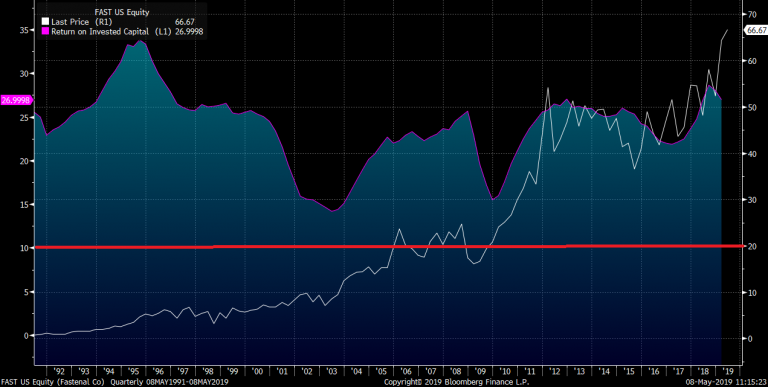

Consider this chart for Fastenal, which stretches back to 1991 and compares its ROIC (shaded) with its stock price (white line). I’ve inserted a red line at 10% to approximate WACC over this period.

Source: Bloomberg as of May 5, 2019

Source: Bloomberg as of May 5, 2019

An investor in 1991 might have prudently forecasted 10 years of cash flows and ROICs, with a terminal ROIC approximating WACC. Eventually, someone will compete away Fastenal’s advantages. Right?

Yet, as we see in the above chart, Fastenal’s ROIC held above 15% since 2001. In fact, it’s approaching all-time records set in the mid-1990s.

So, while the market kept expecting Fastenal’s ROIC to fade toward WACC, it never happened. Consequently, the market had to frequently revise expectations higher, which is reflected in the steadily rising share price (white line).

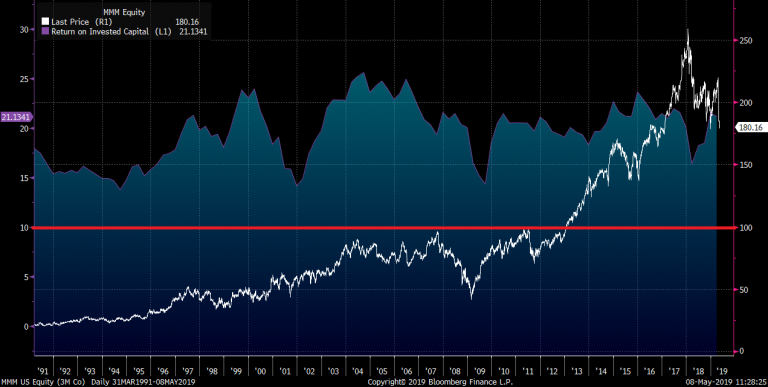

For some additional examples, here’s 3M:

Source: Bloomberg as of May 5, 2019

Source: Bloomberg as of May 5, 2019

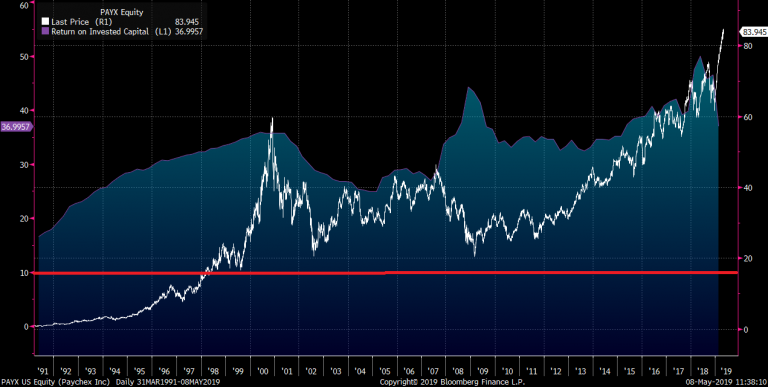

Paychex:

Source: Bloomberg as of May 5, 2019

Source: Bloomberg as of May 5, 2019

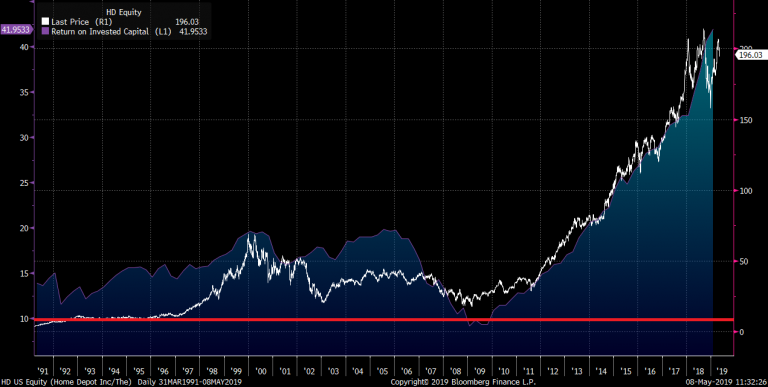

And here’s Home Depot, which despite sharp ROIC decay during the housing crisis, is now producing ROICs well in excess of pre-crisis highs. About as many people expected that outcome as expected Lazarus to rise from the dead. Consequently, the stock price has concurrently and justifiably soared.

Source: Bloomberg as of May 5, 2019

Source: Bloomberg as of May 5, 2019

Of course, it’s easy to identify ROIC machines with hindsight. Over the past 30 years, each of these companies has faced controversy, fierce competition, and macroeconomic headwinds. At many points along the way, investors could have talked themselves out of their position – and perhaps quite reasonably.

So, how might we identify a future ROIC machine and have the confidence to hold tight in periods of uncertainty?

First and foremost, we need to find companies with economic moats that can be defended and ideally widened over the next decade. This is no small task, of course. Once we’ve invested, we regularly evaluate the moat to see if it’s widening or narrowing.

Second, we want companies run by engaged management who understand the firm’s advantages and reinvest to strengthen those advantages. Incentives matter, for sure. But beyond that, we want to see thoughtful capital allocation and an intelligent use of debt. Owner-operators are particularly appealing.

Third, we seek companies we consider intrinsically understandable and forecastable. If we can’t fully appreciate the company’s opportunities and risks or we aren’t comfortable forecasting its financials, there’s no way we’ll hold on when times get tough.

Fourth, we seek companies with vibrant corporate cultures that are flexible and like a good challenge, for they will certainly come if the company’s successful. Costco’s ability to survive and thrive in a changing retail landscape is testament to its corporate culture.

Finally, we prefer companies who are value accretive to all stakeholders – not just shareholders. By this, we mean they also positively impact suppliers, customers, employees, and the communities in which they reside. As Professor Vicki TenHaken writes in her book lessons from century club companies: managing for long-term success: “Close-knit, mutually-supportive relationships heighten the company’s ability to weather challenges as well as to learn and adapt over time.” In other words, improve longevity.

Here’s Fastenal CEO Dan Florness on this topic: “There’s customers, there’s employees, there’s suppliers, and there’s shareholders. It has to work for all four for our business to be successful short-term and long-term.”

It’s a tall order, but if we can accurately check off these five criteria and pay a good price, we think we stand a good chance at finding and benefiting from the next ROIC machine.

As of the date of the post, clients invested in Ensemble Capital Management’s core equity strategy own shares of Ferrari (RACE) and First Republic (FRC). These companies represent only a percentage of the full strategy. As a result of client-specific circumstances, individual clients may hold positions that are not part of Ensemble Capital’s core equity strategy. Ensemble is a fully discretionary advisor and may exit a portfolio position at any time without notice, in its own discretion.

The information contained in this post represents Ensemble Capital Management’s general opinions and should not be construed as personalized or individualized investment, financial, tax, legal, or other advice. No advisor/client relationship is created by your access of this site. Past performance is no guarantee of future results. All investments in securities carry risks, including the risk of losing one’s entire investment. If a security discussed in this blog entry is owned by clients invested in Ensemble Capital’s core equity strategy you will find a disclosure regarding the security held above. If reviewing this blog entry after its original post date, please refer to our current 13F filing or contact us for a current or past copy of such filing. Each quarter we file a 13F report of holdings, which discloses all of our reportable client holdings. Ensemble Capital is a discretionary investment manager and does not make “recommendations” of securities. Nothing contained within this post (including any content we link to or other 3rd party content) constitutes a solicitation, recommendation, endorsement, or offer to buy or sell any securities or other financial instrument. Ensemble Capital employees and related persons may hold positions or other interests in the securities mentioned herein. Employees and related persons trade for their own accounts on the basis of their personal investment goals and financial circumstances.

A simple strategy that will save you so many headaches: don't care about winning trivial arguments.

Someone says something you don't agree with? Smile, nod, and move on to more important things.

Life is short. Not caring about having the last word will save you so much time.

— James Clear (@JamesClear) May 10, 2019

NOTA DEL EDITOR: Esta idea de inversión es obtenida de una carta de Trea European Equities.

* * *

Precio: 152,05 SEK (31 enero 2019)

Capitalización Bursátil = 41.200 Mill SEK

Deuda Neta ajustada = 12.250 Mill SEK

PER ajustado = 9,3x

Los que tenemos unas cuantas primaveras en nuestras espaldas recordaremos la exitosa serie MacGyver. En ella, el protagonista empleaba diversos artilugios cotidianos (chicles, clips, neumáticos…) para fabricar múltiples elementos capaces de ayudarle a escapar de cualquier situación complicada y solventar la misión que tenía asignada. Manteniendo las distancias, algo parecido hace la empresa sueca Trelleborg [STO: TREL-B], líder mundial en soluciones poliméricas especiales de ingeniería.

Continue reading »

Benjamin Graham Jr. recently told me this story about his father, which he heard from Warren Buffett. (Warren confirmed to me that it is accurate.) pic.twitter.com/k8PbSyb4jG

— Jason Zweig (@jasonzweigwsj) May 9, 2019

Classic on Richard Rainwater, "Lord of the Lowball" by Shad Rowe…https://t.co/lMAwxLMxxP

— Chris Mayer (@chriswmayer) May 9, 2019

What a great simple slide showing how value investing is about paying less than what something is worth even if that might mean paying a higher multiple than you could pay for an alternative investment. https://t.co/rLu8wFuTbV

— Ensemble Capital (@IntrinsicInv) May 9, 2019

This article is excerpted from a letter by MOI Global instructor Jim Roumell, portfolio manager of Roumell Asset Management, based in Chevy Chase, Maryland.

On March 26th, RAM filed a Form 13D with the SEC encouraging the company to take actions that we believe are necessary and prudent to realize the value we believe is embedded in ENZ’s shares. We have analyzed and discussed our ENZ investment rationale in our two past quarterly letters, thus we will not restate the case here. RAM now owns 4% of the company. Below are a few highlights from our letter to ENZ’s Board of Directors:

If the Board acts responsibly, shareholders should be richly rewarded from the current depressed market price. We believe our investment rationale is sound, predicated on the multiple avenues the company possesses to unlock significant shareholder value. Our investment thesis rests on the simple observation that the company has “multiple shots on goal”, a cash-rich balance sheet, and a market price significantly below any reason- able sum of the company’s discrete assets.

The Board should take a careful and discerning look at the amount of capital and time required to execute its growth strategy, as well as assessing the probability of success as a stand-alone enterprise. We believe it’s likely that the company’s enviable product and IP portfolio would be better suited in a larger company’s hands, where Enzo’s promising AmpiProbe platform can go to market more efficiently and quickly. In reviewing the company’s long history, one cannot avoid noting that the company’s leading-edge IP assets did not translate into shareholder returns. Why will this time be different? The Board should consider the advice of Warren Buffett when he said, “Aesop Was Right…a bird in the hand is worth two in the bush.”

Members, log in below to access the restricted content.

Not a member?

Thank you for your interest. Please note that MOI Global is closed to new members at this time. If you would like to join the waiting list, complete the following form:

The specific securities identified and described do not represent all of the securities purchased, sold, or recommended for advisory clients, and the reader should not assume that investments in the securities identified and discussed were or will be profitable. The top three securities purchased in the quarter are based on the largest absolute dollar purchases made in the quarter.

Chuck Akre’s 2 book recommendations from our roundtable discussion in Omaha.. ‘Dear Chairman’ by @jeff_gramm (I’m really enjoying it!!) and William Phelps ‘100 to 1 in the Stock Market’ pic.twitter.com/0ErfEcMh2y

— MastersInvest.com (@mastersinvest) May 7, 2019

I've also got basically everything he's ever written in a PDF:https://t.co/D8WfCGPkJ0

— Austin Value Capital (@AustinValue) May 6, 2019