This article by MOI Global instructor Robert Leitz is excerpted from a letter of Iolite Partners, based in Switzerland.

“If a problem has no solution, it may not be a problem, but a fact – not to be solved, but to be coped with over time.” –Shimon Peres

Earlier this year, Germany announced it would exit coal power generation by the year 2038. Prior to this, Norway (a country whose wealth is almost entirely based on fossil fuels) and the Rockefeller family charity started to divest their stakes in businesses related to fossil fuels. Accomplished investor Jeremy Grantham has publicly stated “thermal coal is dead meat”.

These attention-grabbing headlines make you believe humanity has made great strides and is winning the fight against global warming. In my opinion, a quick look at the facts reveals the material disconnect between this feeling and reality. It seems the (Western) mainstream is driven by wishful thinking and emotion, not rational thought.

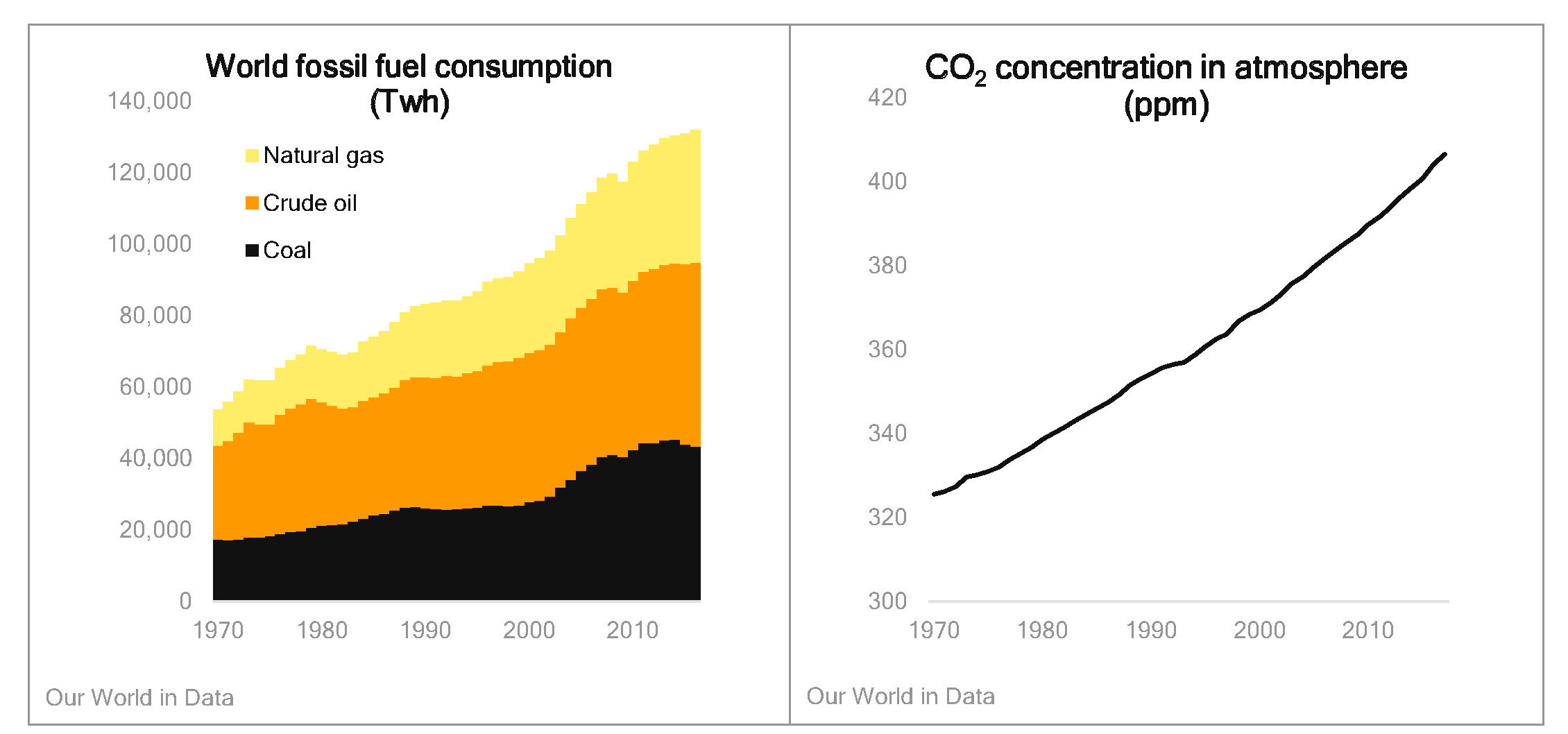

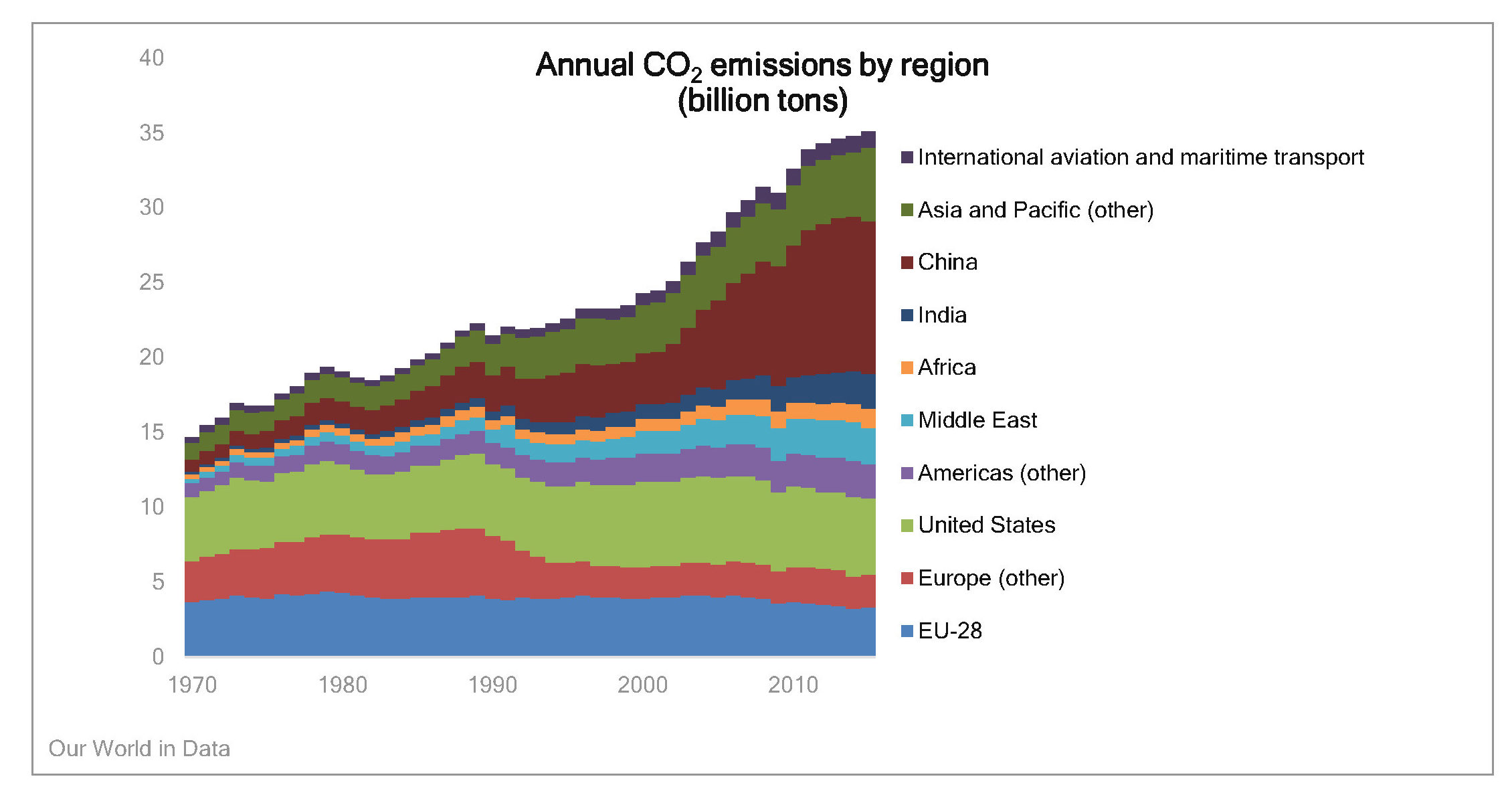

Economic prosperity is closely linked with the availability and consumption of electricity. From 2000-2017, global energy consumption increased by about 44%, at an annual growth rate of about 2.2%, while the world’s population increased by 23%. Fossil fuels account for about 85% of the global energy mix, and that share hasn’t changed much since the 1970s. This means the world keeps consuming more coal, gas, and oil.

Over the next two decades, in the absence of a major catastrophic event, the world’s population is likely to grow by more than one billion people and some two billion people are expected to join the “developed” world. Consequentially, the world’s hunger for energy will increase.

The U.N. Intergovernmental Panel on Climate Change found that global emissions would have to be cut nearly in half by 2030 to preserve a chance of capping the planet’s warming to 1.5 degrees Celsius (or 2.7 degrees Fahrenheit).

This goal seems utterly unachievable, given the growing demand for energy and how the world is generating its electricity. As of today, no impactful progress has made to reduce the world’s dependency on fossil fuels and thereby lower CO2 emissions. Any industrialized nation requires reliable baseload (the permanent minimum load that a power supply system is required to deliver). Unfortunately, wind and solar are unreliable sources of energy and we currently also lack the ability to store electricity on a large scale. Hence, nuclear power and fossil fuels are essential pillars of any energy mix.

Let’s spotlight a few issues.

Coal

Coal is one of the worst climate offenders. However, coal is also a cheap, reliable and simple way to generate electricity, and therefore the preferred energy source in many developing countries. It makes up about 40% of global electricity generation. Global demand and supply are growing as lower consumption in “Western” nations is offset with growth in “developing” regions such as China, India, Pakistan, and Southeast Asia. In 2018, coal emissions were at the highest level, ever. Developing nations will look to roll out cheap energy first and we can’t deny people the right to live a modern life.

Renewables

Germany is widely considered a role model in the fight against climate change. It is estimated that the country has invested something like US$ 500+ billion into wind and solar over the last two decades. All coal power supply is to go offline by 2038, and all nuclear power reactors are supposed to go offline by 2022.

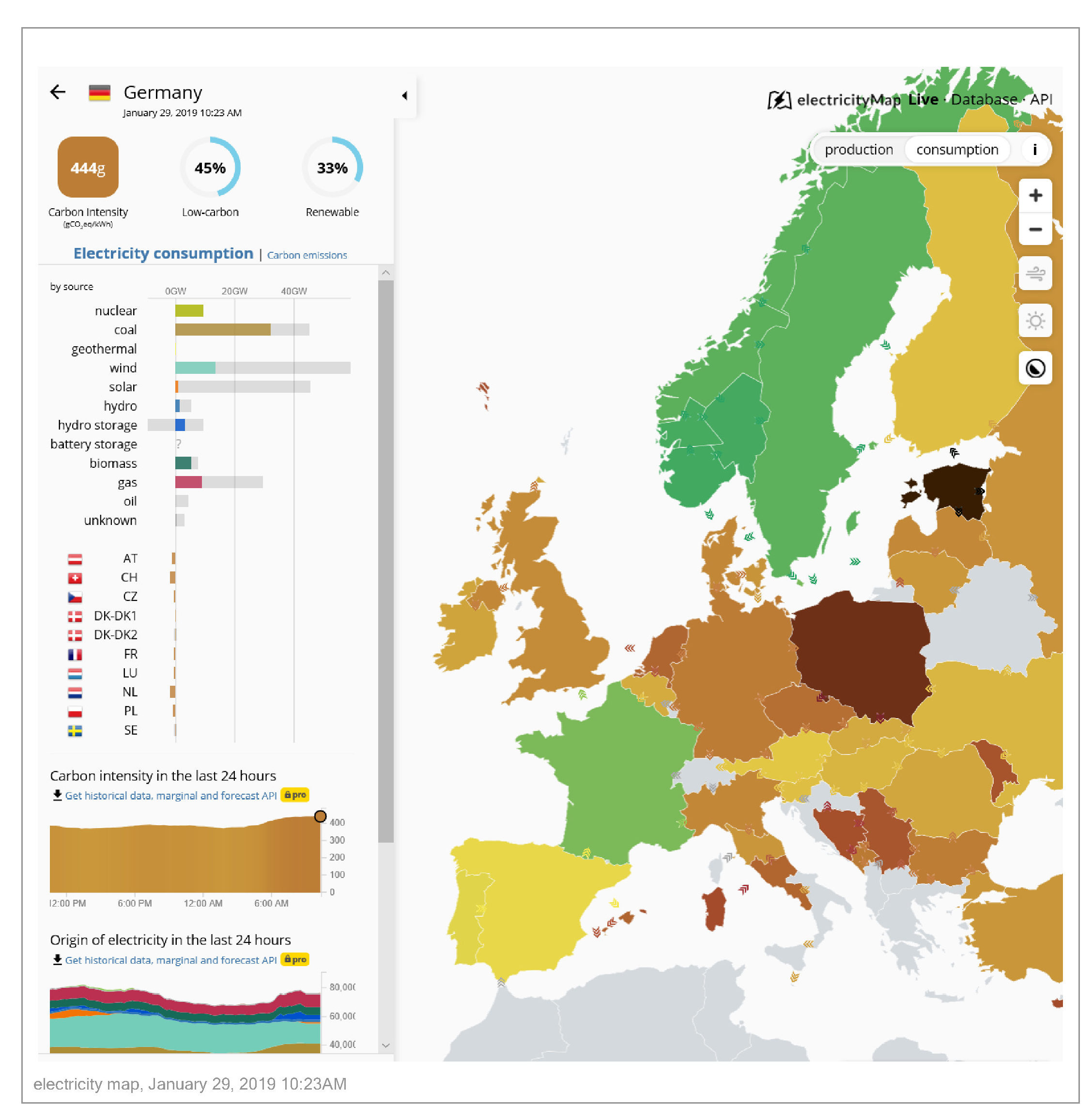

Despite the green headlines, Germany is one of Europe’s worst CO2 offenders with an average output of 450g/kWh. Fifty percent of Germany’s energy supply still comes from coal and nuclear (and up to 70% at night and when the wind is not blowing).

Germany’s recent announcement to shut down 50% of its power supply was made without a viable domestic alternative to rely on. In the absence of a major technological breakthrough regarding battery technology, Germany will have to import more energy from its neighbors in times of peak demand (i.e. nuclear from France or coal from Eastern Europe) and increasingly rely on gas sourced from Russia and the Middle East. Does this sound like a good plan?

Nuclear

A look at the electricity map also reveals that Europe’s cleanest energy producers are France (c. 75g/kWh, nuclear), Sweden (c. 50g/KWh, nuclear), and Norway (c. 50g/kWh, hydro). Hydro is restricted to geography (in Europe mainly to Norway, Switzerland, and Austria). Regarding nuclear: it took France and Sweden about 15 years each to roll out their nuclear programs and almost go emission-free. China is in process to materially increase its nuclear electricity generation, and this development could have a very positive impact on the country’s carbon footprint.

People with a rational mindset and not driven by fear and popular opinion are aware of the positive impact modern nuclear power can have on a country’s ability to produce clean energy. One of them is Bill Gates, who is supporting various projects in the field, for example Terrapower, a company working on a next generation reactor that uses nuclear waste to generate safe energy. Unfortunately, attempts to build a prototype reactor in China were halted given the current trade tensions between the U.S. and China.

Concluding thoughts

Despite many conferences on climate change, billions of dollars spent on research, glossy corporate brochures and enough public awareness, we haven’t made notable progress reducing CO2 emissions from fossil fuels on a global basis. Given the circumstances, a meaningful reduction of fossil fuels (in the absence of a huge nuclear rollout, material investment into carbon capture technologies, or a breakthrough in battery technology) in the next two decades is unlikely.

Members, log in below to access the restricted content.

Not a member?

Thank you for your interest. Please note that MOI Global is closed to new members at this time. If you would like to join the waiting list, complete the following form:

This information is not intended as financial advice and provided for general information only. It is not a solicitation to buy or sell shares. The historical performance is not indicative of the future. This report or any portion hereof may not be reprinted, sold or redistributed without our prior written consent.