Matthew Peterson of Peterson Capital Management presented his in-depth investment thesis on The Daily Journal Corporation (US: DJCO) at Best Ideas 2019.

Thesis summary:

The Daily Journal Corporation is an American publishing and technology company with hidden assets and off-balance sheet value. With no analysts or investor relations department, few understand the transformation that has occurred.

While historically a legal newspaper publishing company, today DJCO operates a SaaS business model providing case management software to courts and government agencies around the U.S. and the world. Licensed software for many ten-year contracts is currently in the multi-year implementation stage. Implementation is expensed as provided, while the long-term recurring high-margin revenue is not yet included on the income statement.

The board includes high-profile names such as Rick Guerin, Peter Kaufman, and Charlie Munger.

Matthew Peterson is the Managing Partner of Peterson Capital Management, LLC. Matthew has over a decade of experience with global financial services firms including Goldman Sachs, Morgan Stanley, Merrill Lynch, American Express, and Ameriprise Financial. Prior to forming Peterson Capital Management, LLC and launching Peterson Investment Fund I, LP, Matthew split time between Wall Street and London as Capital Markets Manager in the Financial Services Vertical at Diamond Management and Technology Consultants. Matthew worked as a member of both the U.S. and U.K. offices, with expertise spanning from risk management to derivative processing. During his tenure with Diamond, Matthew worked with top-tier investment banks, global payments firms, and international insurance companies to deliver high impact solutions to his clients’ most challenging business problems.

Stanley Lim of Value Invest Asia presented his theses on Facebook (US: FB) and Xiaomi Corporation (Hong Kong: 1810) at Best Ideas 2019.

Thesis summaries:

Facebook is the largest social networking company in the world. It owns four of the six social platforms in the world with more than one billion monthly active users. The company is well-placed in the growing digital advertising industry. Facebook has faced a series of negative press regarding security and privacy issues. These issues seem overblown and Facebook continues to have a strong moat that is growing due to control of users’ digital real estate.

Xiaomi Corporation is a smartphone manufacturer, Internet-of-Things device distributor, and a software company. It is one of the top smartphone brands in markets like China, India, Europe, and Indonesia. Xiaomi is one of the fastest-growing global technology companies, with the IoT segment more than doubling year on year. Xiaomi is a misunderstood company, with investors focusing too much on the low-margin smartphone business. Stanley believes that Xiaomi could be the next major electronics brand, rivaling Samsung and Sony.

The full session is available exclusively to members of MOI Global.

Members, log in below to access the full session.

Not a member?

Thank you for your interest. Please note that MOI Global is closed to new members at this time. If you would like to join the waiting list, complete the following form:

About the instructor:

Stanley Lim has spent the last decade in the investment industry. Over the course of his career, he has kick-started a few businesses, worked in the family office and most recently in the investment advisory industry. He has been a writer and analyst for The Motley Fool Singapore from 2013 to 2017. During his time at the Motley Fool, he was one of the pioneer staffs in building up the business and has successfully launched three products with the company. Personally, Stanley believes that financial literacy is a key component of the solution to ending global poverty. Stanley is currently the chief editor of Value Invest Asia.

Gaurav Aggarwal of Metis Capital Management presented his in-depth investment thesis on Time Technoplast (India: TIMETECHNO) at Best Ideas 2019.

Thesis summary:

Time Technoplast is the leading large-size plastic industrial drum manufacturer (market size of ~$1.5-2 billion) and has a dominant position in Indian plastic industrial packaging, used chiefly by the chemical, petrochemical, and food & beverage industries.

The management team is passionate, innovative, and transparent. Insiders own 51% of the equity. From 2010-2014, the company expanded aggressively and has become a market leader in Southeast Asia and the Middle East.

An increased percentage of global sales of industrial packaging comes from Asia (up from 20% to 35% over the last decade due to multiple industries shifting to a lower cost base). India is the leader in Asia for usage of plastic drums/containers with about 55% plastic, 45% metal. In Asia, the mix is closer to 15/85, so a runway of growth exists as the company converts customers to safer, longer shelf life, and lower lifetime cost products.

In light of an ongoing focus on value-added products and 70+% capacity utilization in the overseas industrial packaging business (~30% of revenue), Gaurav expects ROCE to continue to increase toward 20+% for the next few years.

Due to weak small-cap market sentiment and extrapolation of FQ2 numbers, the valuation is compelling. In FQ2, EBITDA margins were affected by unusually volatile material costs, which will be passed on with lag in FQ3 and FQ4. Gaurav estimates 50+% upside based on DCF analysis and 70+% upside based comparable company multiples.

The full session is available exclusively to members of MOI Global.

Members, log in below to access the full session.

Not a member?

Thank you for your interest. Please note that MOI Global is closed to new members at this time. If you would like to join the waiting list, complete the following form:

About the instructor:

Gaurav Aggarwal, CFA, CIPM is the co-founder and co-portfolio manager of Metis India Opportunity Fund (MIOF). Prior to starting Metis in 2011, he was a senior analyst with portfolio management duties over $50 million in fund of fund assets at a leading regional investment bank (Global Investment House) in the Middle East. Prior to this, he was with Bay Harbour Management, a $1.2 billion distressed debt and equity hedge fund in New York City. He has also served as an analyst with Polen Capital Management, a $8 billion+ long-only firm with a very successful long-term track record. He received an M.S. in Accounting (specializing in Finance) and B.S. in Business Administration from the University of North Carolina at Chapel Hill. He looks forward to continue building a charity corpus equaling 25% of his net earnings from fund management which he will deploy in future charity/cause of his choice.

Scott Phillips of Templeton & Phillips Capital Management presented his in-depth investment thesis on ZTO Express (US: ZTO) at Best Ideas 2019.

The full session is available exclusively to members of MOI Global.

Members, log in below to access the full session.

Not a member?

Thank you for your interest. Please note that MOI Global is closed to new members at this time. If you would like to join the waiting list, complete the following form:

About the instructor:

Scott Phillips is a principal and portfolio manager at Templeton and Phillips Capital Management, LLC. Prior to working with Templeton and Phillips Capital Management, LLC, Scott Phillips founded Cumberland Capital Corp, located in Chattanooga, TN. Founded in June 2004, Cumberland Capital provided equity research services to Green Cay Asset Management, a hedge fund management company located in Nassau, Bahamas. In this capacity with Cumberland Capital, Scott was the lead research analyst on the Siebels Hard Asset Fund a long/short equity fund managed by Green Cay Asset Management. In addition to consulting on this fund Scott also provided equity recommendations for the Green Cay Emerging Markets Fund. Prior to consulting Green Cay’s funds Scott was employed as a research analyst with Green Cay beginning in January of 2004. Before joining Green Cay, Scott was an equity research associate analyst with SunTrust Robinson Humphrey (including its predecessor companies) in Atlanta GA from January of 1999 to December of 2003. Scott co-authored with Lauren Templeton of the book “Investing the Templeton Way” released in 2008 by McGraw Hill. Scott is also the author of “Buying at the Point of Maximum Pessimism” a book on forward looking investment themes published by the FT Press in 2010. In addition to these books, Scott co-authored a revision of William Proctor’s 1983 biography of Sir John Templeton titled “The Templeton Touch” released in December 2012. Scott is a member of the John Templeton Foundation where he serves on the Finance Committee and Scott serves as chairman for the board trustees of the Templeton Foundation Inc, and as a member of the Audit Committee. Scott received his B.A. The University of the South.

Joe Magyer of Lakehouse Capital presented his in-depth investment thesis on Facebook (US: FB) at Best Ideas 2019.

Thesis summary:

Facebook may seem to be on the ropes given the bad press it has received. However, the user base and revenue are growing at very healthy rates. The business also owns three other fast-growing platforms — Instagram, WhatsApp, and Messenger — that each have more than one billion monthly active users and are at earlier stages of monetization.

The business is highly cash generative and has more than 9% of its market capitalization in net cash, affording downside protection and strategic optionality, and the shares are deeply our of favor at around 37% below recent highs.

The full session is available exclusively to members of MOI Global.

Members, log in below to access the full session.

Not a member?

Thank you for your interest. Please note that MOI Global is closed to new members at this time. If you would like to join the waiting list, complete the following form:

About the instructor:

Joe Magyer is the Chief Investment Officer of Lakehouse Capital. He’s also the Portfolio Manager of the Lakehouse Small Companies Fund, and the Lakehouse Global Growth Fund. He previously served as Director of Research at The Motley Fool Australia as well as the Portfolio Manager of Australia’s Motley Fool Pro. Before making the leap to Australia, Joe served as the Lead Advisor of Motley Fool Inside Value, which was recognised by The Wall Street Journal and Hulbert Financial Digest for outstanding performance. Joe is also known for his columns for the Australian Financial Review and regular appearances on the likes of CNBC and Sky News Business. Joe holds a Bachelor of Business Administration from the University of Georgia and a Master of Science in Finance from Georgia State University. He is a CFA charterholder.

Jean Pierre Verster of Fairtree Capital presented his in-depth investment thesis on Salmar (Norway: SALM) at Best Ideas 2019.

Thesis summary:

Salmar is one of the largest and most efficient producers of farmed salmon, with an equity market quotation of $6+ billion. The company is integrated across the salmon value chain, from broodstock, roe and smolt production to value added product processing and sales. The salmon fishing industry has attractive structural supply/demand characteristics.

As a low-cost producer with scale, Salmar is well-positioned to continue generating EBITDA margins of 30+%, maintain net profit margins of 20+%, and to deliver sustainable ROE of 30+%. Salmar shares have doubled over the past year and are up 55% annually over the past five years, raising the question whether the recent price includes a margin of safety.

Jean Pierre believes Salmar shares could be worth 50% more within four years, with additional upside from new offshore fish farming initiatives. Salmar is an example of the principle that the most expensive mistake in investing may be selling too soon, or thinking it is too late to buy a great company compounding intrinsic value at an above-average rate.

Jean Pierre Verster is a Portfolio Manager at Fairtree Capital in South Africa, where he manages the ‘Protea’ range of Equity Long/Short hedge funds. Mr. Verster joined the firm in 2016. Prior to this, he was an Analyst at 36ONE Asset Management for 6 years, as part of a team which managed the largest single hedge fund in the country. Previously, Mr. Verster had been a Portfolio Manager and Analyst at Melville Douglas Investment Management and fulfilled various roles at the Standard Bank Group, including as a credit research analyst in its Global Markets Research division, a financial manager in the insurance services division and an internal auditor in the retail banking division. Since 2015, Mr. Verster is also an Independent Non-Executive Director and Chairman of the Audit Committee of Capitec Bank, the second largest retail bank in South Africa by number of primary clients. He is a Chartered Accountant and holds the CFA and CAIA designations.

John Barr of Needham Funds presented his in-depth investment thesis on PDF Solutions (US: PDFS) at Best Ideas 2019.

Thesis summary:

PDF Solutions is a semiconductor data analytics company emerging from a period of investment in new products. It supplies software and other services to improve manufacturing yield for semiconductor manufacturing companies. PDFS has a market cap of $275 million, about $100 million of cash, and annual revenue of nearly $100 million. The company’s SaaS offering for big data analytics, Exensio, has ~$40 million of annual revenue and is growing 30% annually. Its solution for next-generation chip inspection and control, Design-for-Inspection, is in use at a leading semiconductor manufacturing company. At $200 million of revenue, the business could earn $1.50-2.00 per share. Risk exists with regard to new products and their effect on revenue and earnings.

PDF has cash of $3 per share and $50-60 million of royalties expected over the next few years, which could be worth another $1.50-1.80 per share. Exensio could be valued at 3-5x revenue, or $3.50-6.00 per share. These elements total $8-11 per share. Should the company’s lead Design-for-Inspection customer not come to terms on a next order, this part of the business might not have much value in the short term. VIEX Capital Advisors recently disclosed a 6% equity stake. Should the company fail to execute, VIEX might push for structural changes or a sale.

The full session is available exclusively to members of MOI Global.

Members, log in below to access the full session.

Not a member?

Thank you for your interest. Please note that MOI Global is closed to new members at this time. If you would like to join the waiting list, complete the following form:

About the instructor:

John Barr is a Co-Manager of the Needham Growth Fund (NEEGX). He has been its Co-Manager since January 2010. He also manages the Needham Aggressive Growth Fund (NEAGX). John started on Wall Street in 1995 with Needham as a sell-side analyst following technical software companies, including electronic design automation (EDA) companies. John rejoined Needham in 2009 because of the culture, which lives and breathes growth companies and long-term investing.

From 2000 – 2002, John was a managing director and senior analyst at Robertson Stephens, following semiconductor technology companies. He was an Institutional Investor All-Star and was ranked by Reuters as leader of one of the top software teams. In 2002 John moved to the buy-side and joined Buckingham Capital Management where he served as a portfolio manager and analyst for their diversified industry long/short domestic equity hedge fund.

John’s first career was outside of Wall Street, where he spent 14 years in sales, marketing and management, primarily in the EDA industry. Working in these small companies makes him think like an owner and to look for that trait in his investments. John loves the challenge of identifying businesses with compounding characteristics and getting to know the companies over the course of years. From his industry experience, he looks to invest in companies that he would have liked to have been part of.

Mike Kruger of MPK Partners presented his in-depth investment thesis on Boustead Projects (Singapore: AVM) at Best Ideas 2019.

Thesis summary:

Boustead Projects does the design and project management of Class A industrial real estate in Southeast Asia for multinational corporations in high-value industries; actual construction work is outsourced. Since 2010, Boustead has used its balance sheet to build certain properties, which are then leased to the client. Despite this, net cash is one-fourth of the recent market cap.

The shares recently traded at less than one-third of NAV. Boustead is not a typical family-owned Asian real estate stock that languishes at a discount with no catalyst in sight. Founder FF Wong has delivered a compounded total return to shareholders of 18+% since 2000.

Two catalysts are in place: First, backlog has soared 150+% to all-time highs recently, which should benefit earnings by the June 2019 quarter. Second, Boustead will likely put its owned properties into a REIT (comps at 1.0x NAV of higher) over the next couple of years.

The full session is available exclusively to members of MOI Global.

Members, log in below to access the full session.

Not a member?

Thank you for your interest. Please note that MOI Global is closed to new members at this time. If you would like to join the waiting list, complete the following form:

About the instructor:

Mike Kruger’s first investment experience was watching his shares of Berkshire Hathaway get cut in half during the tech-mania of the late 1990’s. But he didn’t panic, and today manages a global focused value portfolio of equities and distressed debt in New York City. He previously worked as a former equity and credit analyst at Promethean Asset Management LLC in NYC, and prior to that as a high-yield credit analyst at Liberty Mutual in Boston. He holds a Bachelor’s degree from the College of Arts and Sciences at Cornell University.

Brian Pitkin of URI Capital Management presented his in-depth investment thesis on AIG (US: AIG) at Best Ideas 2019.

Thesis summary:

AIG is another in a long line of global financial institutions that have fallen far out of favor with investors. AIG is a well-known global property and casualty insurer, paired with a US-dominated life and retirement business.

The company has derisked the balance sheet after taking painful reserve charges and implementing an “adverse development cover” with Berkshire Hathaway. Improving returns on equity, driven by P&C underwriting profitability, should lead to a higher, more normalized valuation for AIG.

The company fits the pattern of good — sometimes great — businesses operating profitably — sometimes very profitably — with global scale, but, for differing reasons, have been far out of favor with investors, allowing Brian to invest at valuations well below book value.

AIG recently traded at 8.5x 2019E earnings of $5.11 per share, i.e., a market price of $43 per share, well below adjusted book value of $56 per share and stated book value of $66 per share.

The full session is available exclusively to members of MOI Global.

Members, log in below to access the full session.

Not a member?

Thank you for your interest. Please note that MOI Global is closed to new members at this time. If you would like to join the waiting list, complete the following form:

About the instructor:

Brian E. Pitkin founded URI Capital Management to follow his long time passion for deep business analysis and long term value investing. Brian began his career in Investment Banking at Merrill Lynch in Chicago, and then joined The Edgewater Funds, a Chicago private equity firm. Brian ultimately returned to family-owned Ulrich Chemical, a Midwest chemical distributor where he helped accelerate both top and bottom line growth, including a near tripling of the company’s bottom line. He then helped negotiate and execute the sale of Ulrich to Brenntag, a global chemical distributor, before leaving to start his own ventures, now dominated by managing the fund URI Capital Partners. His background in both investing and managing businesses has contributed to his understanding of what makes for a successful business and thus a successful long term investment, while faith and family provide a strong foundation for the entirety of his life. URI Capital Partners is a long only investment fund focused on a highly concentrated portfolio of publicly traded companies. While our concentrated, long only strategy may present more volatility in the short term, we are not willing to sacrifice higher potential longer term returns for a more comfortable journey. Investing in enduring businesses at good valuations, avoiding leverage requiring margins of safety serves to solidify our foundation and protect investor dollars.

Adam Zuercher of Hixon Zuercher Capital Management presented his in-depth investment thesis on Walt Disney (US: DIS) at Best Ideas 2019.

Thesis summary:

Walt Disney is the world leader at the box office, their parks have no equals, and they are building an empire through mergers and acquisitions. The business is doing well and experiencing strong growth, while being fundamentally sound. Adam believes the best is yet to come.

Disney’s new family-oriented streaming service, Disney+, along with ESPN+ and the company’s majority stake in Hulu should provide growth for many years. The addition and growth of this new segment of the business should justify higher multiples for stock, which in combination with growth in other segments, makes Disney Adam’s best idea for 2019 and beyond.

The following transcript has been edited for space and clarity.

It’s an honor to participate with so many other great investors. I have participated in these events before and enjoyed learning from others; now I’m excited to reciprocate with a good idea of my own. First I want to share a little of information about me and our firm.

I started my career with a CPA firm in 1999 after graduating from the University of Toledo. That firm launched an investment advisory business where I worked for three years. In 2002, I co-founded Hixon Zuercher with Tony Hixon. It is a registered investment advisory firm specializing in investment management in the large capitalization U.S. equity space. Located in Findlay, Ohio, our assets under management total $135 million with over $60 million allocated to U.S. large capitalization equity in two portfolios, “Focused Equity” and “Focused Equity Income.” We apply a discipline of investing in high quality, durable, and growing companies trading at value prices. Each portfolio holds roughly 30 stocks, a number enabling us to concentrate our best ideas. A team of four manages our strategies; I lead the team with Tony Hixon, Josh Robb, and our research analyst, Austin Wilson.

Today I will present one of my best ideas for 2019, an idea we use in both of our portfolios. I chose this idea for today particularly because of a catalyst that could fuel growth in the company. If you have children, if you like to watch movies, or if you’re a sports fan, you have been touched by Walt Disney Company (DIS). Disney was founded in 1923, lists on the New York Stock Exchange, and recently traded at about $112 a share with a $167 billion market capitalization. The company headquarters in Burbank, California and employs over 200,000 people worldwide.

We started investing in Disney in August 2015. Including dividends, the return exceeds 3%; performance has fallen short of expectations. However, Disney’s catalyst will come at the end of 2019, so we remain optimistic.

Disney Business Segments and Markets

Disney’s business can be grouped under four world regions and four business segments. Percentages indicate percent of total revenue attributable to each region or segment:

World Regions

United States and Canada, 76%

Europe, 12%

Asia/Pacific, 9%

Latin America and Other, 3%

We expect Disney’s presence in China to create the largest theme park region in the future. Consequently, the percentage of revenue attributable to other regions will probably decline.

Business Segments

Media networks, 41%

Parks and Resorts, 34%

Studio Entertainment, 17%

Consumer Products and Interactive Media, 8%

The media networks segment includes Disney’s wholly owned subsidiary, American Broadcasting Company (ABC). With the Hearst Corporation, Disney shares ownership of ESPN and A + E Networks (A&E). Lifetime and the History Channel are A&E subsidiaries.

Disney’s largest domestic parks and resorts are located in Florida and California, and it owns smaller properties in other parts of the U.S. including Disney Cruise Line. Its foreign properties include Disneyland Paris, 47% ownership of a Hong Kong park, 45% of a Shanghai park, and royalties from licensing at a Tokyo park.

The studio entertainment segment includes Marvel Studios, Pixar Animation Studios, and Walt Disney Animation Studios. These studios’ movie pipelines for 2019 include “Star Wars Episode 9,” Frozen 2,” “Toy Story 4,” and “Avengers: Endgame.” Also, Disney recently announced its planned purchase of 21st Century Fox, the mass media corporation.

When you think of Disney’s Consumer Products and Interactive Media segment, think toys. Any toy Disney makes or licenses generates royalties from the toy manufacturers. This smallest business segment combines with other segments to create a well-diversified, competitive corporation.

The Disney Catalyst

Disney’s big catalyst will be new streaming services poised to compete with Netflix starting in the fourth quarter of 2019. It will be known as “Disney+.” A monthly subscription will deliver all Disney content, and Disney announced its Disney+ subscription will cost less than Netflix. The service will not, as far as we know, include ESPN+, the sports network’s streaming service.

Hulu, which streams television and other video content, presents an interesting Disney story. Disney first purchased part of Hulu in 2009; now it owns 30%. Likewise, 21st Century Fox owns 30% of Hulu, so Disney will own 60% of Hulu after the 21st Century Fox purchase. Bob Iger, Disney’s CEO, has expressed interest in purchasing the remaining 40%. Currently, Comcast (CMCSA) owns 30% and Time Warner owns 10% of Hulu. In our opinion, Disney will enjoy a competitive advantage with Netflix by capitalizing on its ESPN+, Hulu, and Disney+ properties.

Disney Acquisitions

Over the last 25 years, Disney’s inorganic growth complemented its organic growth. Some of the key purchases and their costs (where available) included:

BAMTech, a 2017 acquisition now charged with developing the Disney+ platform, $2.58 billion;

Lucasfilm, a 2012 acquisition, best known for its Star Wars and Indiana Jones franchises, $4.06 billion;

Hulu, 2009;

Marvel, 2009, $4 billion;

Pixar, 2006, $7.4 billion;

ABC and ESPN, 1995, $1 9 billion.

During this period, Disney spent over $100 billion on acquisitions. The 21st Century Fox acquisition will total an additional $71 billion funded equally from cash and stock. A new issue of 343 million Disney common shares will help underwrite the expansion expected to close in early 2019.

Economic Tailwinds

Certain economic trends should provide a tailwind for Disney, the most important of which is video streaming revenue growth. Projections set global video streaming growth from $30.9 billion in 2015 to $123.2 billion by 2024. That’s a compound annual growth rate of 17%. The following factors contribute to this trend:

Content makers and media companies, recognizing the opportunities, have committed more resources to create higher quality content. These developments lead to the impression of a media world trending toward a subscription-based economy. The trend resembles the same course the software industry followed when it started with licenses and evolved into subscriptions.

Growth in theme parks provides another economic tailwind. In 2017, attendance equaled 475.8 million people for the top 10 theme park companies worldwide. This represents an increase of 8.6% over 2016 attendance. Theme park attendance growth in China and Disney’s participation in that market present exciting possibilities: Year-over-year attendance grew by nearly 20% in 2017. Chinese theme park attendance explains about 25% of major operators’ worldwide attendance. Almost one-half billion people visit Chinese theme parks annually, more than double the attendance of all major sports leagues worldwide.

Disney Competitiveness

A company’s competitive situation explains a key factor in our decisions to invest. We think of this approach as an evaluation of economic moat creation:

Real and perceived product differentiation: There’s only one Mickey Mouse. When people think about sports news, they often think of ESPN. Disney enjoys trusted brands and a strong reputation.

Price: We expect Disney+ to enter the market with a lower price than competitors, particularly Netflix. Arguably, Netflix offers a broader content spectrum, partly because of Disney+’s focused devotion to family-based content. Based on the number of U.S. households with at least one child, the number of potential customers should grant Disney+ a strong base.

Barriers to entry: Disney’s 1,709 patents, 1,080 outstanding patent applications, and 5,997 trademarks help differentiate and protect its products. Disney’s brand recognition and consumer trust started to grow in 1923 when Walt and Roy Disney sketched and executed their vision; new competitors face a high hurdle.

Disney Competitors

Strong competitors do business in all four of Disney’s segments and in the planned Disney+ streaming services segment:

Media network competitors

CBS and CBS Sports Network

Fox and Fox Sports

NBC and NBC Sports

Parks and Resorts

Carnival Cruise Line

Cedar Fair

Six Flags

Universal

Studio Entertainment

Paramount

Sony Pictures

Time Warner

Universal

Consumer Products and Interactive Media

Hasbro

Mattel

Minecraft

Nintendo

Streaming Services

Apple

Amazon

AT&T

Netflix

Youtube

Disney’s park attendance exceeds competitors’ attendance, though large competitors enjoy strong market share. As for streaming services, Netflix presents the greatest competition, followed by Amazon. However, in our opinion, no single competitor does everything Disney does and as well as Disney does it.

Consider Disney’s theme park dominance in 2017:

North American attendance grew 2.3% year-over-year with over 150 million visitors.

Walt Disney World’s Magic Kingdom drew more visitors than any park in the world with 20 million visitors.

China’s parks experienced the most growth worldwide, and forecasters project China will have the largest theme park market in the world by 2020.

We expect Disney’s presence in China to amplify its theme park growth.

Disney Financials

Disney’s competitive success is important, and so are its financials. A quick summary of annual results for the ten years through the fiscal year ending in September 2018 (FY18) follows:

The compounded annual revenue growth rate (CAGR) equals 5%.

Operating income equals 7% CAGR with recent operating margin at 25% and trending upward for the last ten years. Operating income growth exceeds revenue growth, suggesting effective cost management.

Earnings per share equals 12% CAGR with a jump in FY18. Federal tax cuts aided the earnings jump, which should benefit future earnings. Cost control and stock buybacks have also aided the trend.

Another noteworthy observation is Disney’s historical profitability during recessions.

Net margin equals 5% CAGR, and FY18 net margin equals 19%.

For FY18, the cash balance equaled $4.15 billion and CAGR equals 3%.

Long-term debt equals 5% CAGR and the FY18 balance equals $26.87 billion. That represents a debt-to-equity ratio equal to about 39%.

Capital expenditure CAGR equals 11% and FY18’s balance equals $4.47 billion. Disney reliably increases investment in its business.

Free cash flow CAGR equals 10% and the FY18 balance equals $9.83 billion. Free cash flow drives shareholder and corporate economic value.

Diluted shares outstanding equals -3% CAGR, another favorable trend for shareholder value. The FY18 outstanding diluted balance equals 1.507 billion shares. Of course, the 343-million share issue to help fund the 21st Century Fox acquisition works against shareholder value. However, Disney should be able to retire or buy back those shares over the next five or six years.

The dividend-per-share CAGR equals 17%. We favor dividend-paying companies, and we favor annual dividend growth of at least 10% because it yields 100% growth after about seven years.

Return on equity (ROE) CAGR equals 6%, and the FY18 ROE equaled 28%.

Return on assets (ROA) CAGR equals 6%, and the FY18 ROA equaled 13%.

Return on invested capital (ROIC) CAGR equals 6%, and the FY18 ROIC equaled 18%.

Weighted average cost of capital (WACC) ranged between 8% and 10%. We favor companies capable of improving economic value added (EVA), which equals ROIC minus WACC. A positive EVA indicates the company generates higher returns on capital than the cost to acquire it. The EVA CAGR equals 53%, and FY18 EVA equals 9%.

Free cash flow to sales recently equaled 17%.

Disney Management

Bob Iger, 66, has worked as CEO since 2005 and Chairman since 2012. He started his career with ABC in 1974. After Disney’s 1995 acquisition of ABC, he became President and Chief Operating Officer, and in 2000 he became a Director. Mr. Iger owns over $100 million in Disney stock, about 0.1% of outstanding shares, which gives evidence to the alignment of his personal goals and those of shareholders. He also serves on the boards of Apple, the September 11th Foundation, and the Bloomberg Family Foundation.

The Board of Directors is completely independent with the exception of Bob Iger. We favor Disney’s requirement that directors must own Disney stock valued at five times their retainer; this encourages alignment of director and shareholder interests.

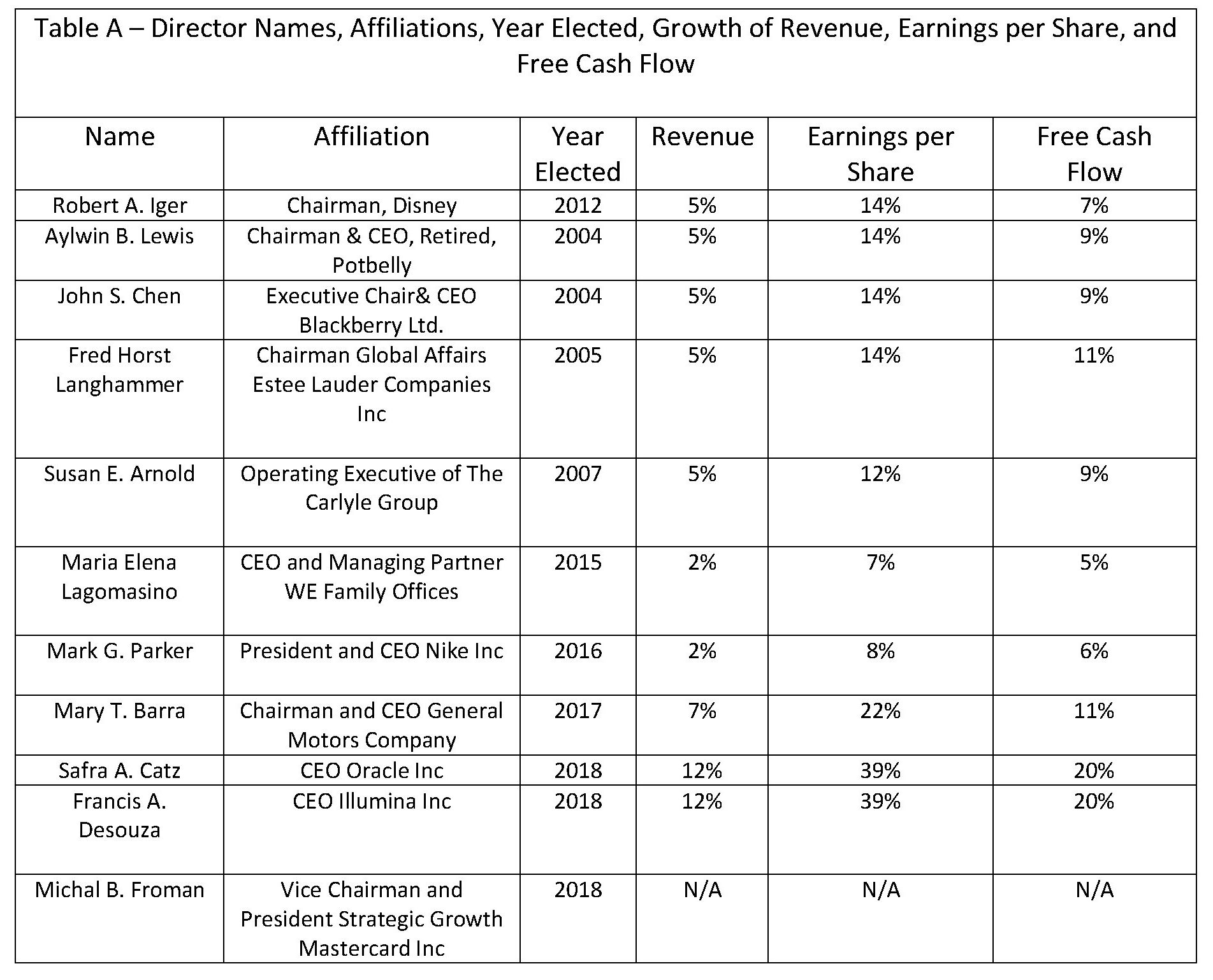

Table A lists directors, affiliations, the year shareholders elected each director to the board, and corporate performance during their tenure in terms of CAGR in revenue, earnings per share, and free cash flow.

Performance values indicate directors have produced exceptional positive growth, which proves to us their value to the company. Also, we conclude directors effectively regulate key executive compensation. The compensation rate equals about 0.1% based on revenue of $50 billion over the last five years and $68 million in compensation over the same period.

Disney Valuation

Disney offers great products, great services, a catalyst for the future in Disney+, and an effective management team. However, the story does not end until after we address valuation. From a traditional historical price-to-earnings perspective, the FY18 multiplier equals 15.6; the five-year average equals 17.2. Therefore, this year Disney trades at a 10% discount compared to its history. Compared to its competitors, Disney trades in FY18 at a 26% premium and at a 25% premium for the last five years.

Next we present our own valuation of Disney. Using certain business assumptions listed in Appendix A, we modeled future discounted free cash flows to solve for their present value. The model uses 10 forecast years, 3.00% terminal growth rate, years for historical multiple calculation equal five, and shares outstanding equal 1,489 billion. Please note the assumed revenue growth rate equals 5% and it ignores the forecast effect of the Disney+ catalyst; we address Disney+ later.

Discounted free cash flows sum to a present value equal to about $53.50 per share. The process yields a terminal price-to-earnings ratio of 18.78 and price-per-share equal to about $103.40. These results yield an intrinsic value equal to $156.90 per share. Assuming a recent $112 share price, we conclude the stock trades at a 39.69% discount.

In the next valuation step we incorporate assumptions about Disney+. Here I present base assumptions along with some of the worst-case and best-case assumptions:

Initial subscribers total 15 million, which we consider conservative because U.S. households with at least one child total 50 million, many households without children will consider Disney+ a viable entertainment option, and many non-U.S. households will subscribe.

In comparison, Netflix started with about 23 million subscribers. Our worst-case scenario projects five million subscribers and our best-case projects 20 million.

Annual subscriber growth totals 15%, at least 10%, and 20% at best.

Monthly pricing equals $8 per subscriber. Our worst to best scenarios price from $6 to $10.

The base case applies a price-to-earnings ratio equal to 35.0. We derive this value from a blend of our Disney valuation, reported above, and Netflix; Netflix trades above 55. A higher growing business probably justifies a higher price-to-earnings ratio. Price-to-earnings ranges from 20 to 50.

Our base case scenario assigns Disney+ $16.26 per share, ranging from $1.90 in the worst case and $52.08 in the best case. We add the Disney+ valuation to our original $156.89 Disney valuation and arrive at an intrinsic value equal to $173.15 for the base case. The worst case yields $158.79 and the best case yields $208.97. This result indicates Disney’s recent $112 price trades at a 54% discount for the base case, 41% for the worst case, and 86% for the best case.

Conclusion

Disney’s stock price was relatively stable during the fourth quarter of 2018 when the market was so volatile. Its price traded below the 50-day moving average but above the 200-day moving average. Disney’s diverse business consists of segments that have stood the test of time. Its history of acquisitions has helped accelerate growth and should propel it into the future as long as economic tailwinds persist. Though its competitors impose a strong market presence, Disney entrenches itself as a global entertainment leader and enjoys a wide economic moat. Fundamentally, the company is growing by nearly every metric, and we expect the 21st Century Fox acquisition and completion of the Disney+ platform to hasten its growth. Leadership, including Bob Iger and the Board of Directors, combine to form an effective team. By our measures, the company is drastically undervalued when we include Disney+’s contribution to growth potential. These facts and conclusions make Disney our best idea for 2019 and beyond.

The following are excerpts of the Q&A session with Adam Zuercher:

Q: Thank you, Adam, for such a comprehensive presentation. A component of Disney’s value, ESPN, seems to have fallen off. Does Disney still own a significant piece of that?

A: Yes, Disney still owns 80% of ESPN. Consumers traditionally access ESPN through cable platforms and providers, and diminution of the cable market presents concerns over ESPN valuation. ESPN+’s launch reflects the sports network’s aim to preserve its subscriber base even if they cut their cable. Also, subscribers can view ESPN on Hulu Plus, YouTube TV, and Sling. ESPN still offers significant value.

Q: It seems theme parks have pushed pricing quite hard, exercising their pricing power. From this perspective, has Disney extracted all it can from theme parks? What’s your take on how much prices have gone up over the last decade?

A: Yes, Disney has exercised its pricing power because it can. It’ll continue to increase prices. Rising prices are not limited to theme parks; we see it in the entire entertainment space. Disney will continue to exercise its theme park pricing power because Disney parks offer an experience unavailable anywhere else. As long as visitor growth continues, Disney prices will continue rising.

Disney’s theme park performance during recessions reveals Disney’s power: Attendance is strong, and Disney remains profitable because of its other business segments. Disney offers a strong brand and a sticky culture.

Q: Let’s talk more about the Disney+ streaming service. Can you elaborate on the nature of its content?

A: Disney has not revealed detailed information about content, pricing, or what the platform will look like. However, we know Disney+ will include Pixar, Marvel, Disney, and National Geographic content. We also know it will not include ESPN+, though some analysts speculate about bundling with ESPN+ or theme park tickets. I can imagine a VIP package in Disney+ wrapped with theme parks, or a package wrapping Disney+ and ESPN+. We expect more Disney+ content information as the rollout approaches, and I hope for more detail in next quarter’s earnings call. Perhaps while information is limited but promising – during this downturn in Disney’s stock price and the broader market – a buying opportunity presents itself for long-term investors.

Q: What revenue might go away as a result of Disney+? Will Disney reduce or eliminate its content on Netflix or iTunes? In other words, will Disney endure an offset to its projected incremental revenue?

Q: Yes, that’s a fantastic, insightful question. Disney will lose revenue. For example, today you might purchase a DVD to watch a Disney movie. However, Disney+ will diminish demand for DVD’s. It’s the way the world has evolved. Even though revenue declines in one product line, another replaces it.

You asked about Netflix. The answer is yes, Disney will phase out its Netflix content as agreements expire. It is possible Disney will negotiate new agreements with Netflix, but we anticipate they would be expensive for Netflix. Also, Marvel content will eventually disappear from Netflix, and Disney can reboot it to Disney+ after two inactive years. Disney might endure growing pains and some transitionary time, but we believe the result will serve Disney and its shareholders well.

Appendix A – Valuation Assumptions

Revenue growth of 5% Y-O-Y

Gross margin equal to 2018 actual gross margin

Effective tax rate of 21%

Capital expenditures equal to 2018 percent of revenue

Dividends increase 5% per share per year

Share repurchases equal rolling five-year average

Five-year historical price-to-earnings ratio

Price calculated at actual shares outstanding (to be conservative)

i The data source is Bloomberg, which lists Disney competitors as 21st Century Fox, CBS Corp, Discovery Inc., and Viacom.

About the instructor:

Adam Zuercher is co-founder, Chief Executive Officer, and Chief Investment Officer of Hixon Zuercher Capital Management. As Chief Investment Officer, he oversees investment research and the development and implementation of the firm’s investment strategies. Adam serves as a co-Portfolio Manager and as chairman of the firm’s Investment Committee. Adam is also a member of NAPFA. Adam has experience providing investment management and financial advisory services since 1999. Prior to co-founding Hixon Zuercher Capital Management in 2002, Adam worked at a CPA firm for three years specializing in financial planning and investment advisory services for high net worth individuals.

Performance values indicate directors have produced exceptional positive growth, which proves to us their value to the company. Also, we conclude directors effectively regulate key executive compensation. The compensation rate equals about 0.1% based on revenue of $50 billion over the last five years and $68 million in compensation over the same period.

Performance values indicate directors have produced exceptional positive growth, which proves to us their value to the company. Also, we conclude directors effectively regulate key executive compensation. The compensation rate equals about 0.1% based on revenue of $50 billion over the last five years and $68 million in compensation over the same period.