Adam Zuercher of Hixon Zuercher Capital Management presented his in-depth investment thesis on Walt Disney (US: DIS) at Best Ideas 2019.

Thesis summary:

Walt Disney is the world leader at the box office, their parks have no equals, and they are building an empire through mergers and acquisitions. The business is doing well and experiencing strong growth, while being fundamentally sound. Adam believes the best is yet to come.

Disney’s new family-oriented streaming service, Disney+, along with ESPN+ and the company’s majority stake in Hulu should provide growth for many years. The addition and growth of this new segment of the business should justify higher multiples for stock, which in combination with growth in other segments, makes Disney Adam’s best idea for 2019 and beyond.

The following transcript has been edited for space and clarity.

It’s an honor to participate with so many other great investors. I have participated in these events before and enjoyed learning from others; now I’m excited to reciprocate with a good idea of my own. First I want to share a little of information about me and our firm.

I started my career with a CPA firm in 1999 after graduating from the University of Toledo. That firm launched an investment advisory business where I worked for three years. In 2002, I co-founded Hixon Zuercher with Tony Hixon. It is a registered investment advisory firm specializing in investment management in the large capitalization U.S. equity space. Located in Findlay, Ohio, our assets under management total $135 million with over $60 million allocated to U.S. large capitalization equity in two portfolios, “Focused Equity” and “Focused Equity Income.” We apply a discipline of investing in high quality, durable, and growing companies trading at value prices. Each portfolio holds roughly 30 stocks, a number enabling us to concentrate our best ideas. A team of four manages our strategies; I lead the team with Tony Hixon, Josh Robb, and our research analyst, Austin Wilson.

Today I will present one of my best ideas for 2019, an idea we use in both of our portfolios. I chose this idea for today particularly because of a catalyst that could fuel growth in the company. If you have children, if you like to watch movies, or if you’re a sports fan, you have been touched by Walt Disney Company (DIS). Disney was founded in 1923, lists on the New York Stock Exchange, and recently traded at about $112 a share with a $167 billion market capitalization. The company headquarters in Burbank, California and employs over 200,000 people worldwide.

We started investing in Disney in August 2015. Including dividends, the return exceeds 3%; performance has fallen short of expectations. However, Disney’s catalyst will come at the end of 2019, so we remain optimistic.

Disney Business Segments and Markets

Disney’s business can be grouped under four world regions and four business segments. Percentages indicate percent of total revenue attributable to each region or segment:

- World Regions

- United States and Canada, 76%

- Europe, 12%

- Asia/Pacific, 9%

- Latin America and Other, 3%

We expect Disney’s presence in China to create the largest theme park region in the future. Consequently, the percentage of revenue attributable to other regions will probably decline.

- Business Segments

- Media networks, 41%

- Parks and Resorts, 34%

- Studio Entertainment, 17%

- Consumer Products and Interactive Media, 8%

The media networks segment includes Disney’s wholly owned subsidiary, American Broadcasting Company (ABC). With the Hearst Corporation, Disney shares ownership of ESPN and A + E Networks (A&E). Lifetime and the History Channel are A&E subsidiaries.

Disney’s largest domestic parks and resorts are located in Florida and California, and it owns smaller properties in other parts of the U.S. including Disney Cruise Line. Its foreign properties include Disneyland Paris, 47% ownership of a Hong Kong park, 45% of a Shanghai park, and royalties from licensing at a Tokyo park.

The studio entertainment segment includes Marvel Studios, Pixar Animation Studios, and Walt Disney Animation Studios. These studios’ movie pipelines for 2019 include “Star Wars Episode 9,” Frozen 2,” “Toy Story 4,” and “Avengers: Endgame.” Also, Disney recently announced its planned purchase of 21st Century Fox, the mass media corporation.

When you think of Disney’s Consumer Products and Interactive Media segment, think toys. Any toy Disney makes or licenses generates royalties from the toy manufacturers. This smallest business segment combines with other segments to create a well-diversified, competitive corporation.

The Disney Catalyst

Disney’s big catalyst will be new streaming services poised to compete with Netflix starting in the fourth quarter of 2019. It will be known as “Disney+.” A monthly subscription will deliver all Disney content, and Disney announced its Disney+ subscription will cost less than Netflix. The service will not, as far as we know, include ESPN+, the sports network’s streaming service.

Hulu, which streams television and other video content, presents an interesting Disney story. Disney first purchased part of Hulu in 2009; now it owns 30%. Likewise, 21st Century Fox owns 30% of Hulu, so Disney will own 60% of Hulu after the 21st Century Fox purchase. Bob Iger, Disney’s CEO, has expressed interest in purchasing the remaining 40%. Currently, Comcast (CMCSA) owns 30% and Time Warner owns 10% of Hulu. In our opinion, Disney will enjoy a competitive advantage with Netflix by capitalizing on its ESPN+, Hulu, and Disney+ properties.

Disney Acquisitions

Over the last 25 years, Disney’s inorganic growth complemented its organic growth. Some of the key purchases and their costs (where available) included:

- BAMTech, a 2017 acquisition now charged with developing the Disney+ platform, $2.58 billion;

- Lucasfilm, a 2012 acquisition, best known for its Star Wars and Indiana Jones franchises, $4.06 billion;

- Hulu, 2009;

- Marvel, 2009, $4 billion;

- Pixar, 2006, $7.4 billion;

- ABC and ESPN, 1995, $1 9 billion.

During this period, Disney spent over $100 billion on acquisitions. The 21st Century Fox acquisition will total an additional $71 billion funded equally from cash and stock. A new issue of 343 million Disney common shares will help underwrite the expansion expected to close in early 2019.

Economic Tailwinds

Certain economic trends should provide a tailwind for Disney, the most important of which is video streaming revenue growth. Projections set global video streaming growth from $30.9 billion in 2015 to $123.2 billion by 2024. That’s a compound annual growth rate of 17%. The following factors contribute to this trend:

- rising number of online users worldwide;

- technological developments render higher streaming quality;

- multiple devices can accommodate streaming;

- declining streaming costs.

Content makers and media companies, recognizing the opportunities, have committed more resources to create higher quality content. These developments lead to the impression of a media world trending toward a subscription-based economy. The trend resembles the same course the software industry followed when it started with licenses and evolved into subscriptions.

Growth in theme parks provides another economic tailwind. In 2017, attendance equaled 475.8 million people for the top 10 theme park companies worldwide. This represents an increase of 8.6% over 2016 attendance. Theme park attendance growth in China and Disney’s participation in that market present exciting possibilities: Year-over-year attendance grew by nearly 20% in 2017. Chinese theme park attendance explains about 25% of major operators’ worldwide attendance. Almost one-half billion people visit Chinese theme parks annually, more than double the attendance of all major sports leagues worldwide.

Disney Competitiveness

A company’s competitive situation explains a key factor in our decisions to invest. We think of this approach as an evaluation of economic moat creation:

- Real and perceived product differentiation: There’s only one Mickey Mouse. When people think about sports news, they often think of ESPN. Disney enjoys trusted brands and a strong reputation.

- Price: We expect Disney+ to enter the market with a lower price than competitors, particularly Netflix. Arguably, Netflix offers a broader content spectrum, partly because of Disney+’s focused devotion to family-based content. Based on the number of U.S. households with at least one child, the number of potential customers should grant Disney+ a strong base.

- Barriers to entry: Disney’s 1,709 patents, 1,080 outstanding patent applications, and 5,997 trademarks help differentiate and protect its products. Disney’s brand recognition and consumer trust started to grow in 1923 when Walt and Roy Disney sketched and executed their vision; new competitors face a high hurdle.

Disney Competitors

Strong competitors do business in all four of Disney’s segments and in the planned Disney+ streaming services segment:

- Media network competitors

- CBS and CBS Sports Network

- Fox and Fox Sports

- NBC and NBC Sports

- Parks and Resorts

- Carnival Cruise Line

- Cedar Fair

- Six Flags

- Universal

- Studio Entertainment

- Paramount

- Sony Pictures

- Time Warner

- Universal

- Consumer Products and Interactive Media

- Hasbro

- Mattel

- Minecraft

- Nintendo

- Streaming Services

- Apple

- Amazon

- AT&T

- Netflix

- Youtube

Disney’s park attendance exceeds competitors’ attendance, though large competitors enjoy strong market share. As for streaming services, Netflix presents the greatest competition, followed by Amazon. However, in our opinion, no single competitor does everything Disney does and as well as Disney does it.

Consider Disney’s theme park dominance in 2017:

- North American attendance grew 2.3% year-over-year with over 150 million visitors.

- Walt Disney World’s Magic Kingdom drew more visitors than any park in the world with 20 million visitors.

- China’s parks experienced the most growth worldwide, and forecasters project China will have the largest theme park market in the world by 2020.

We expect Disney’s presence in China to amplify its theme park growth.

Disney Financials

Disney’s competitive success is important, and so are its financials. A quick summary of annual results for the ten years through the fiscal year ending in September 2018 (FY18) follows:

- The compounded annual revenue growth rate (CAGR) equals 5%.

- Operating income equals 7% CAGR with recent operating margin at 25% and trending upward for the last ten years. Operating income growth exceeds revenue growth, suggesting effective cost management.

- Earnings per share equals 12% CAGR with a jump in FY18. Federal tax cuts aided the earnings jump, which should benefit future earnings. Cost control and stock buybacks have also aided the trend.

- Another noteworthy observation is Disney’s historical profitability during recessions.

- Net margin equals 5% CAGR, and FY18 net margin equals 19%.

- For FY18, the cash balance equaled $4.15 billion and CAGR equals 3%.

- Long-term debt equals 5% CAGR and the FY18 balance equals $26.87 billion. That represents a debt-to-equity ratio equal to about 39%.

- Capital expenditure CAGR equals 11% and FY18’s balance equals $4.47 billion. Disney reliably increases investment in its business.

- Free cash flow CAGR equals 10% and the FY18 balance equals $9.83 billion. Free cash flow drives shareholder and corporate economic value.

- Diluted shares outstanding equals -3% CAGR, another favorable trend for shareholder value. The FY18 outstanding diluted balance equals 1.507 billion shares. Of course, the 343-million share issue to help fund the 21st Century Fox acquisition works against shareholder value. However, Disney should be able to retire or buy back those shares over the next five or six years.

- The dividend-per-share CAGR equals 17%. We favor dividend-paying companies, and we favor annual dividend growth of at least 10% because it yields 100% growth after about seven years.

- Return on equity (ROE) CAGR equals 6%, and the FY18 ROE equaled 28%.

- Return on assets (ROA) CAGR equals 6%, and the FY18 ROA equaled 13%.

- Return on invested capital (ROIC) CAGR equals 6%, and the FY18 ROIC equaled 18%.

- Weighted average cost of capital (WACC) ranged between 8% and 10%. We favor companies capable of improving economic value added (EVA), which equals ROIC minus WACC. A positive EVA indicates the company generates higher returns on capital than the cost to acquire it. The EVA CAGR equals 53%, and FY18 EVA equals 9%.

- Free cash flow to sales recently equaled 17%.

Disney Management

Bob Iger, 66, has worked as CEO since 2005 and Chairman since 2012. He started his career with ABC in 1974. After Disney’s 1995 acquisition of ABC, he became President and Chief Operating Officer, and in 2000 he became a Director. Mr. Iger owns over $100 million in Disney stock, about 0.1% of outstanding shares, which gives evidence to the alignment of his personal goals and those of shareholders. He also serves on the boards of Apple, the September 11th Foundation, and the Bloomberg Family Foundation.

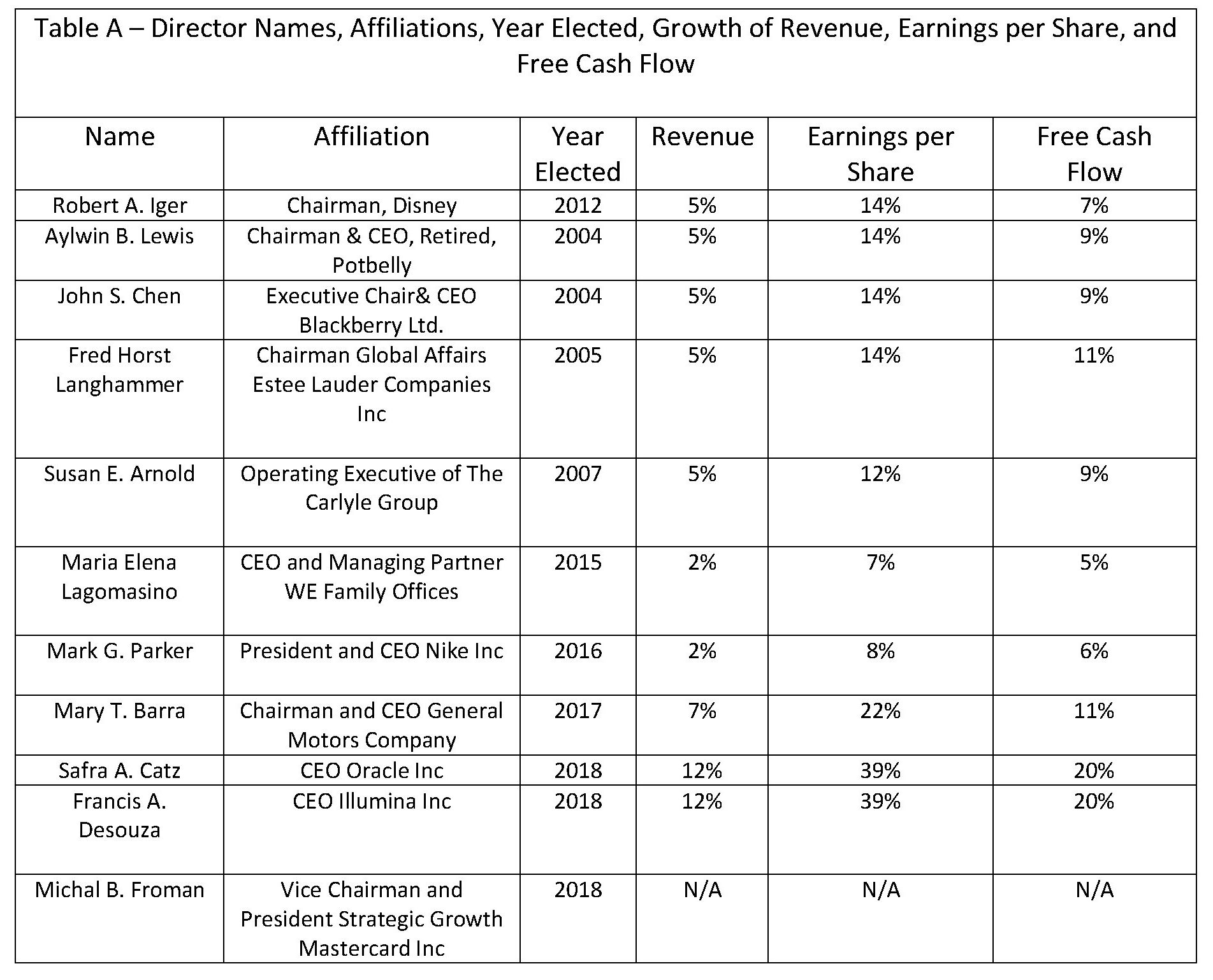

The Board of Directors is completely independent with the exception of Bob Iger. We favor Disney’s requirement that directors must own Disney stock valued at five times their retainer; this encourages alignment of director and shareholder interests.

Table A lists directors, affiliations, the year shareholders elected each director to the board, and corporate performance during their tenure in terms of CAGR in revenue, earnings per share, and free cash flow.

Performance values indicate directors have produced exceptional positive growth, which proves to us their value to the company. Also, we conclude directors effectively regulate key executive compensation. The compensation rate equals about 0.1% based on revenue of $50 billion over the last five years and $68 million in compensation over the same period.

Performance values indicate directors have produced exceptional positive growth, which proves to us their value to the company. Also, we conclude directors effectively regulate key executive compensation. The compensation rate equals about 0.1% based on revenue of $50 billion over the last five years and $68 million in compensation over the same period.

Disney Valuation

Disney offers great products, great services, a catalyst for the future in Disney+, and an effective management team. However, the story does not end until after we address valuation. From a traditional historical price-to-earnings perspective, the FY18 multiplier equals 15.6; the five-year average equals 17.2. Therefore, this year Disney trades at a 10% discount compared to its history. Compared to its competitors, Disney trades in FY18 at a 26% premium and at a 25% premium for the last five years.

Next we present our own valuation of Disney. Using certain business assumptions listed in Appendix A, we modeled future discounted free cash flows to solve for their present value. The model uses 10 forecast years, 3.00% terminal growth rate, years for historical multiple calculation equal five, and shares outstanding equal 1,489 billion. Please note the assumed revenue growth rate equals 5% and it ignores the forecast effect of the Disney+ catalyst; we address Disney+ later.

Discounted free cash flows sum to a present value equal to about $53.50 per share. The process yields a terminal price-to-earnings ratio of 18.78 and price-per-share equal to about $103.40. These results yield an intrinsic value equal to $156.90 per share. Assuming a recent $112 share price, we conclude the stock trades at a 39.69% discount.

In the next valuation step we incorporate assumptions about Disney+. Here I present base assumptions along with some of the worst-case and best-case assumptions:

- Initial subscribers total 15 million, which we consider conservative because U.S. households with at least one child total 50 million, many households without children will consider Disney+ a viable entertainment option, and many non-U.S. households will subscribe.

- In comparison, Netflix started with about 23 million subscribers. Our worst-case scenario projects five million subscribers and our best-case projects 20 million.

- Annual subscriber growth totals 15%, at least 10%, and 20% at best.

Monthly pricing equals $8 per subscriber. Our worst to best scenarios price from $6 to $10. - The base case applies a price-to-earnings ratio equal to 35.0. We derive this value from a blend of our Disney valuation, reported above, and Netflix; Netflix trades above 55. A higher growing business probably justifies a higher price-to-earnings ratio. Price-to-earnings ranges from 20 to 50.

Our base case scenario assigns Disney+ $16.26 per share, ranging from $1.90 in the worst case and $52.08 in the best case. We add the Disney+ valuation to our original $156.89 Disney valuation and arrive at an intrinsic value equal to $173.15 for the base case. The worst case yields $158.79 and the best case yields $208.97. This result indicates Disney’s recent $112 price trades at a 54% discount for the base case, 41% for the worst case, and 86% for the best case.

Conclusion

Disney’s stock price was relatively stable during the fourth quarter of 2018 when the market was so volatile. Its price traded below the 50-day moving average but above the 200-day moving average. Disney’s diverse business consists of segments that have stood the test of time. Its history of acquisitions has helped accelerate growth and should propel it into the future as long as economic tailwinds persist. Though its competitors impose a strong market presence, Disney entrenches itself as a global entertainment leader and enjoys a wide economic moat. Fundamentally, the company is growing by nearly every metric, and we expect the 21st Century Fox acquisition and completion of the Disney+ platform to hasten its growth. Leadership, including Bob Iger and the Board of Directors, combine to form an effective team. By our measures, the company is drastically undervalued when we include Disney+’s contribution to growth potential. These facts and conclusions make Disney our best idea for 2019 and beyond.

The following are excerpts of the Q&A session with Adam Zuercher:

Q: Thank you, Adam, for such a comprehensive presentation. A component of Disney’s value, ESPN, seems to have fallen off. Does Disney still own a significant piece of that?

A: Yes, Disney still owns 80% of ESPN. Consumers traditionally access ESPN through cable platforms and providers, and diminution of the cable market presents concerns over ESPN valuation. ESPN+’s launch reflects the sports network’s aim to preserve its subscriber base even if they cut their cable. Also, subscribers can view ESPN on Hulu Plus, YouTube TV, and Sling. ESPN still offers significant value.

Q: It seems theme parks have pushed pricing quite hard, exercising their pricing power. From this perspective, has Disney extracted all it can from theme parks? What’s your take on how much prices have gone up over the last decade?

A: Yes, Disney has exercised its pricing power because it can. It’ll continue to increase prices. Rising prices are not limited to theme parks; we see it in the entire entertainment space. Disney will continue to exercise its theme park pricing power because Disney parks offer an experience unavailable anywhere else. As long as visitor growth continues, Disney prices will continue rising.

Disney’s theme park performance during recessions reveals Disney’s power: Attendance is strong, and Disney remains profitable because of its other business segments. Disney offers a strong brand and a sticky culture.

Q: Let’s talk more about the Disney+ streaming service. Can you elaborate on the nature of its content?

A: Disney has not revealed detailed information about content, pricing, or what the platform will look like. However, we know Disney+ will include Pixar, Marvel, Disney, and National Geographic content. We also know it will not include ESPN+, though some analysts speculate about bundling with ESPN+ or theme park tickets. I can imagine a VIP package in Disney+ wrapped with theme parks, or a package wrapping Disney+ and ESPN+. We expect more Disney+ content information as the rollout approaches, and I hope for more detail in next quarter’s earnings call. Perhaps while information is limited but promising – during this downturn in Disney’s stock price and the broader market – a buying opportunity presents itself for long-term investors.

Q: What revenue might go away as a result of Disney+? Will Disney reduce or eliminate its content on Netflix or iTunes? In other words, will Disney endure an offset to its projected incremental revenue?

Q: Yes, that’s a fantastic, insightful question. Disney will lose revenue. For example, today you might purchase a DVD to watch a Disney movie. However, Disney+ will diminish demand for DVD’s. It’s the way the world has evolved. Even though revenue declines in one product line, another replaces it.

You asked about Netflix. The answer is yes, Disney will phase out its Netflix content as agreements expire. It is possible Disney will negotiate new agreements with Netflix, but we anticipate they would be expensive for Netflix. Also, Marvel content will eventually disappear from Netflix, and Disney can reboot it to Disney+ after two inactive years. Disney might endure growing pains and some transitionary time, but we believe the result will serve Disney and its shareholders well.

Appendix A – Valuation Assumptions

Revenue growth of 5% Y-O-Y

Gross margin equal to 2018 actual gross margin

Effective tax rate of 21%

Capital expenditures equal to 2018 percent of revenue

Dividends increase 5% per share per year

Share repurchases equal rolling five-year average

Five-year historical price-to-earnings ratio

Price calculated at actual shares outstanding (to be conservative)

i The data source is Bloomberg, which lists Disney competitors as 21st Century Fox, CBS Corp, Discovery Inc., and Viacom.

About the instructor:

Adam Zuercher is co-founder, Chief Executive Officer, and Chief Investment Officer of Hixon Zuercher Capital Management. As Chief Investment Officer, he oversees investment research and the development and implementation of the firm’s investment strategies. Adam serves as a co-Portfolio Manager and as chairman of the firm’s Investment Committee. Adam is also a member of NAPFA. Adam has experience providing investment management and financial advisory services since 1999. Prior to co-founding Hixon Zuercher Capital Management in 2002, Adam worked at a CPA firm for three years specializing in financial planning and investment advisory services for high net worth individuals.

About The Author: MOI Global Editorial Team

The MOI Global Editorial Team, led by John Mihaljevic, CFA, includes community builders, event organizers, writers, editors, research associates, security analysts, and fanatical member support advocates. Our sole purpose is to serve the members of MOI Global as well as we possibly can in order to help them learn, invest intelligently, and build lifelong friendships with like-minded people.

Who is MOI Global? In recent years, The Manual of Ideas has expanded to become more than simply “the very best investing newsletter on the planet” (Mohnish Pabrai). We are now a thriving global community of intelligent investors, connected through great ideas, thought-provoking interviews, online conferences, live member events, and much more.

Members of MOI Global enjoy complimentary access to a growing array of resources and content related to the art of intelligent investing. Members also enjoy preferential access to selected offline events as well as exclusive access to other events hosted by MOI Global, including the Zurich Project Summit, the Latticework Conference, and Ideaweek.

More posts by MOI Global Editorial Team