This article is excerpted from an Ossia Partners Fund letter by MOI Global instructor Curtis Jensen, portfolio manager at Robotti & Company Advisors, based in New York.

“Facts do not cease to exist because they are ignored.”

–Aldous Huxley

Portfolio Update

Viewed simply through the lens of your capital account, the Fund’s performance might feel like it has taken a torpedo amidships, despite strong gains made in the June quarter. However, performance at the companies underlying the Fund’s shareholdings has not deteriorated nearly as much as that of our metaphorical ship’s performance, as a review of the Fund’s top three holdings highlights.[1] Moreover, temporary market declines have opened the door to new investment opportunities, sketches of which are found later in this letter.

Tidewater Midstream (TSX: TWM)

The Fund’s largest holding, has seen its share price decline by more than 30% this year. Operationally, while management has lowered its forecasted 2020 results by 10% to 15%, gas processing volumes have held up reasonably well on the back of resilient natural gas prices in western Canada as have the volumes and spreads at its British Columbia refinery. Customers appear to be fully honoring or are close to their contracted terms. “Green hydrogen” continues to attract capital and capture headlines and the Prince George refinery’s prodigious hydrogen production not only helps to earn carbon credits, but also has attracted increasing interest from green technology companies.

Most significantly on June 18th Tidewater signed a definitive agreement to sell one of its pipelines for cash at a multiple that is nearly double that of the company’s public market multiple, relinquishing only a modest amount of the company’s cash flow. The sale proceeds, along with internally generated cash flow, will significantly de-lever the balance sheet and may amount to as much as 40% to 50% of the current market cap; much of that value ought to accrue directly to equity holders. While the public market shuns Tidewater’s shares, the company’s largest shareholder, Toronto-based, private equity firm Birch Hill, recently increased its ownership to 24% and now has two representatives on the board. A search process for another independent board candidate is underway. Assuming currently depressed conditions persist and the pipeline sale closes, my analysis suggests 50% to 70% upside in the value of the equity within 12 months.

Cpl Resources (ISE: DQ5)

Ireland’s leading workforce solutions group, updated the markets on July 9th noting that fiscal year results (i.e., pre-tax profits for the period ending June 30) were expected to show growth over last year (all organic), despite the disruptive impact of the global pandemic in the last four months of this fiscal year. Cpl’s permanent placement segment, a less predictable but higher margin business, has seen a drop in activity this year. But Cpl’s results have been buoyed by its flexible talent business (~ 70% of net fee income), where multi-year contracts underpin operations, and in verticals such as pharmaceuticals, life sciences and technology.

Cpl’s cash generative, high return business is supported by a fortress balance sheet and appears to be answering a growing demand for flexible workforce solutions and helping employers with contingency recruitment and skill-set shortages. Management, which owns more than 30% of the company, has implemented cost initiatives in response to Covid-19, but continues to make key investments in technology, further entrenching itself with its corporate partners. The company expects to expand beyond its current presence in nine countries. An attractive valuation (7x – 8x FY ‘20 cash earnings) along with cash on the balance sheet (equating to 25% of the market capitalization) ought to afford a high degree of downside protection. Cpl shares are down more than 10% YTD.

Exor N.V. (BIT: EXO)

The Agnelli family holding company, with interests in the auto, industrial and reinsurance sectors, is the Fund’s third largest holding. Despite a 24% drop in Exor’s share price this year, management’s “internal activism” – a mindset that characterizes many of OPF’s owner-operator led businesses – has been on full display. For example, management agreed to sell its reinsurance business, Partner Re, in response to an unsolicited $9 billion cash bid from French insurer Covéa. Covéa, which announced its bid after the WHO recognized Covid-19 as a pandemic, subsequently reneged on its offer and tried to renegotiate the terms of the deal. Exor declined, announcing that it was content to hold what it views as an attractive and growing asset.

Management has other capital allocation initiatives underway: it continues to support the merger of Fiat-Chrysler (28% Exor ownership) and Peugeot, a deal whose financial and industrial logic appears sound, but whose success has been given long odds in the marketplace. Knitting together two large auto companies presents a variety of challenges, but Fiat-Chrysler (“FCA”) has a successful roadmap and the need for industry consolidation has never been higher given the burgeoning transition to electric vehicles and, longer-term, autonomous driving.

Capital equipment company CNH Industrial (27% Exor ownership) has announced its intent to split its “Off-Highway” assets (agricultural and construction equipment) from its “On-Highway” assets (trucks, buses and powertrains). In time, such a transformation ought to improve management focus, expedite operational efficiencies and, ultimately, lead to better returns and growth.

The Covid pandemic has proved especially challenging for manufacturers such as FCA and CNH, as customer demand wanes and operations get disrupted, but the timing of these initiatives – coinciding with a more unforgiving environment – may prove auspicious longer-term.

Exor management stayed on the offensive even in March, making a $200 million investment in ride-share company Via Transportation – signaling its interest in further diversifying its portfolio – and has been similarly busy supporting financings on behalf of investees such as FCA.

These examples evidence management’s disciplined and dispassionate approach to capital allocation, suggesting their ability to continue compounding value at attractive rates remains intact. Assuming some recovery in currently depressed industrial and auto markets, Exor shares trade at a steep discount to underlying Net Asset Value.

The Search for Value – Corporate Transition

While severe market dislocations can introduce unsettling performance setbacks, they can also create attractive buying opportunities. I initiated a handful of new investments, the two largest of which are summarized below.

Larger corporate transitions often heighten investor uncertainty and disappoint short-term oriented capital, but can be fertile hunting grounds for those with longer-term investment time horizons and a cautious sense of probabilities. Two such investments have made their way into the Fund’s top ten holdings this year.

Voya Financial (NYSE: VOYA)

Voya has been steadily reshaping its business since its IPO in 2013[2], most recently exiting its variable annuity business (2018) and announcing the sale of its individual life business (December 2019, sale pending). Going forward, Voya will have a greatly simplified organization, one with lower capital intensity, fewer legacy liabilities and regulatory elements, and strong franchises in retirement services, investment management and employee benefits.

Voya’s retirement segment, which accounts for about 60% of the company’s pre-tax earnings, offers tax-deferred, employer-sponsored retirement savings plan and administrative services (e.g., record keeping and plan administration) to corporations of all sizes and to a wide variety of tax-exempt organizations. Within its defined-contribution market, Voya serves more than 50,000 plan sponsors and 5.6 million plan participants. The retirement segment’s offerings are complemented by a retail wealth management business focused on building long-term relationships with plan participants. Investment management offers a wide range of actively managed fixed income, equity, multi-asset and alternative products, managing nearly $140 billion on behalf of institutions and individuals. The employee benefits business provides group insurance products such as stop loss, group life and disability to mid-size and large corporate employers.

Individually each of these segments has reasonable organic growth prospects – defined as mid to high single digit percentages – and management seems to have cogent plans for cost cutting (especially those stranded costs likely to emerge after the sale of the life business (likely in Q3 2020). Combined, these internal dynamics ought to markedly improve profitability and returns from current levels. Beyond its operational levers, management is committed to an aggressive capital allocation strategy that includes both significant share repurchases and debt reduction. For perspective, management has repurchased nearly 50% of the company’s shares, or $6 billion, since the IPO while maintaining an investment grade balance sheet, and will enjoy further surplus capital once the sale of the life business is completed.

While I view the next six to 12 months as a transition (therefore neglect from Wall Street), I expect a truer picture of the company’s growth and returns to emerge by mid to late next year. With $5 to $6 of cash earnings power (starting Q3/Q4 2021), Voya’s shares may be worth $65-$70, 35% to 40% above current levels.

Management’s vision seems to recognize not only a voracious appetite among private equity firms for life insurance assets, but also an inexorable drive within the financial services industry toward consolidation and scale. Longer-term, Voya itself might find some benefit in partnering with one of its larger peers, peers who would likely pay a control premium to the going-concern values noted above.

Morgan Stanley (NYSE: MS)

Morgan Stanley continues to transform its business as well. In February the firm announced its intent to acquire brokerage firm E*Trade Financial, further diversifying away from its historic dependence on cyclical and capital intensive investment banking activities. E*Trade brings a nearly 40-year heritage of disrupting the digital brokerage industry[3] and the combination will not only broaden Morgan Stanley’s valuable wealth management franchise, but ought to fortify a digital banking capability deemed more essential by individual investors. The two firms also have attractive corporate stock plan businesses that, once combined, will serve 4.6 million plan participants across more than 4,700 corporate plans.

The stock for stock deal disappointed some investors and analysts who simplistically viewed the use of relatively cheap shares to pay a premium for E*Trade as dilutive to both book value and earnings. In tandem with a darkening stock market outlook and plunging interest rates, Morgan Stanley shares fell nearly 45% from late February into the market’s March nadir, a reaction that all but ignored a valuation approaching decade lows, an overcapitalized balance sheet and the longer-term benefits of E*Trade’s higher margins, its iconic brand and an attractive deposit base. Managed well, the deal might unearth longer-term benefits: for example, where Morgan Stanley’s wealth advisers have a 50% “share of wallet,” E*Trade garners only about 10% of its “Next Gen” clients’ wallet share.

Apart from the E*Trade deal, Morgan Stanley’s investment banking business reported surprisingly solid first half results. Corporations raised a record amount of equity in the June quarter and through May, U.S. investment-grade companies had issued more than $1 trillion in debt — nearly as much as in all of 2019. The firm’s Q2 results, including earnings of $1.96 per share, reflected significant operating leverage (higher revenues with expense control), translating to an impressive 17% return on tangible equity. Given an uncertain economic outlook and a benign capital markets environment, it seems likely that corporations will continue to raise capital opportunistically and seek advice on growth and restructuring, a backdrop that should favor investment banking firms.

I am cognizant that large corporate M&A deals often fail to create economic value, and investors with a sense of history who remember Morgan Stanley’s 1997 merger with Dean Witter Discover might have reason to be skeptical of the E*Trade deal.[4] Even Morgan Stanley’s deal to buy Smith Barney from Citigroup during the depths of the Financial Crisis – a deal later viewed as a master stroke – was clouded by doubts and encountered trouble at its incipience. Smith Barney brokers complained about poor technology, for example, and margins in the business were troublingly low. But management, led by current CEO James Gorman, made the right investments, raising margins in the wealth management business to the low 20’s from the single digits. This history, along with a near-death experience during the Financial Crisis has, I believe, aptly chastened management, better preparing it for a smoother transition with E*Trade. E*Trade shareholders have approved the merger, which awaits regulatory approval and is expected to close in Q4.

Morgan Stanley shares currently trade at an undemanding 1.2x tangible book value (1.0x GAAP book value), approximating 10x this year’s earnings, levels that would appear to limit downside in the investment. Management has not “bet the ranch” on E*Trade and would seem to have reasonable prospects of growing book value (a rough proxy for economic value) at attractive rates. On the other hand, should management capitalize on E*Trade’s full potential, shares could re-rate at considerably higher multiples, as the market begins to appreciate the shift to a mix of businesses distinguished by a greater measure of durability.

U-Turns and Exits

I sold a few holdings, including two new positions initiated this year (“U-Turns”) and one of the Fund’s early investments (“Exit”). A small position in Berkshire Hathaway was added in late March and subsequently sold when it became clear that Berkshire was unable or unwilling to deploy its substantial cash hoard – greatly diminishing the odds of an encore to its ’08-’09 performance. In February I initiated a position in Essent Group, a highly profitable mortgage insurance business, notably founded after the Global Financial Crisis and unburdened by that era’s legacy liabilities. Purchased at a single digit PE multiple and a modest premium to GAAP book value, Essent’s stock, like those of its peers, fell precipitously as the nation’s employment picture and mortgage market deteriorated. After some recovery, shares were sold at a loss as the potential outcomes for its business simply became too wide. I also sold the Fund’s longer-term, core holding in Diamond Hill Capital. Impressive gains made in its credit strategies are unlikely to offset the more profitable revenues lost in recent periods by its equity funds. The firm is well-managed, enjoys a highly liquid balance sheet and the shares remain stubbornly cheap, but asset flows are the life-blood of the business and the bulk of those appear to be ebbing. The Fund’s realized loss was partially offset by years of large, special dividends. Cheap is a necessary but not sufficient condition to hold an investment.

The Road Ahead – Notes of Caution

The Stock Market is not Main Street.

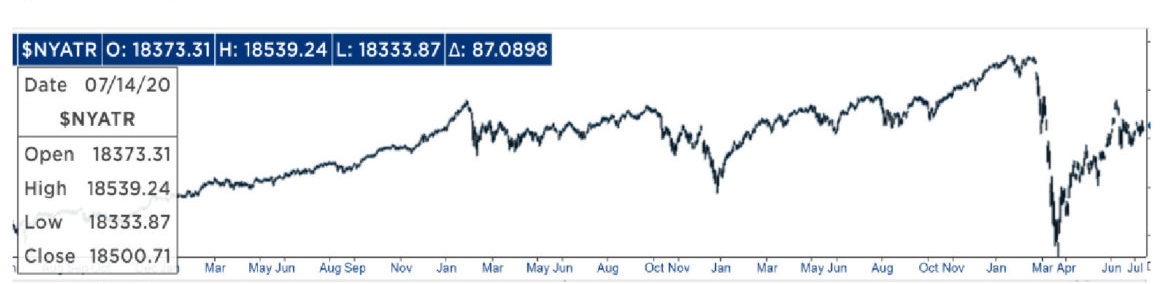

Select parts of the stock market, mostly a narrow group of technology and bio-tech/healthcare companies, have made eye-watering rebounds from their March lows, encouraged by an unprecedented tsunami of monetary and fiscal stimulus. But broader measures of the “stock market” suggest the accumulated damage of Trump’s multi-front trade war, OPEC’s oil price war and now the global battle with Covid-19 has put a halt to the inexorable rise across many risk assets. For example, total returns on the NYSE Composite Index, a much broader index than the S&P 500, one which includes roughly 1,500 U.S. stocks and 400 foreign stocks, have gone almost nowhere in the past three years.

Source: NYSE.

Market pundits and speculators rely on market aphorisms such “Low rates justify high multiples” and “Don’t fight the Fed.” Mathematically, low rates may justify higher stock valuations until one considers that these same low rates reflect an increasingly over-indebted and stagnant global economy. Low rates and rich valuations are two sides of the same coin. Paraphrasing strategist David Rosenberg, “At some point, P/E multiples will realize why interest rates are pressed to the floor.” While fiscal and monetary stimulus hearten a select group of stock investor/speculators, the impact of that stimulus on Main Street businesses and employment – the guts of the U.S. economy – are much less clear and the longer-term consequences of such massive debt accumulation remain an intricate riddle.

Will a vaccine help?

The bio-tech and pharmaceutical industries seem to be making astonishing progress in developing a Covid vaccine, yet it is not clear how effective such a vaccine might be and how quickly it can be distributed.[5] Nor is it clear how many households will get it, even if it’s free. Even less certain is America’s willingness to oblige government directives, such as mask wearing and social distancing, steps that appear to be indispensable keys to mitigating the virus’ impact. America’s rugged individualism and federalist system have, for the moment, stymied attempts at corralling an unprecedented public health crisis. Americans are often quick to assert their rights, but say little about their responsibilities – the Covid crisis illuminating one stark example.

Two-Pronged Political Risk.

Geopolitical risks and our presidential election may be reasons for a final note of caution. I am fairly convinced the U.S. is in a long-term Cold War with China, one that has been brewing for decades, but plainly exposed in recent years by Trump’s policies. Unfortunately for us, China’s Communist Party politics allow it to “play the long game,” defined as decades or more, while our asymmetric engagement is hamstrung by a four-year election cycle. At a minimum China’s subversive Cold War tactics and industrial might seem likely to pose a chronic threat to a number of U.S. industries. Will the outcome of the presidential election meaningfully change our country’s current trajectory — politically, economically and socially? I don’t know – and I hope that my concerns are unfounded – but I recognize that the policy menu in the years ahead likely requires higher taxes and cuts to social services, developments that won’t naturally engender improvements on Main Street or Wall Street.

Our “Don’t Ask, Don’t Tell” stock markets, driven more and more by value-ignorant participants,[6] seem blithely unaware of such questions. For the moment, a number of OPF holdings remain neglected or shunned by public markets, but our portfolio is, happily, distanced from those ignoring fundamental tenets, embracing instead companies whose shares are demonstrably cheap and enjoy tangible downside protection. OPF’s portfolio companies have strong balance sheets affording staying power and financial flexibility and are capably managed by “owner-operator” executives. The longer-term portfolio outcomes, I believe, will be driven by the idiosyncrasies of each company and the “internal levers” available to management (e.g., operational and capital allocation) and should be less reliant on broad market trends that continue to skate on the thin ice of high expectations and speculative fervor.

[1] At June 30th, OPF’s top three holdings accounted for ~ 29% of the Fund’s assets (at market value).

[2] Prior to its initial public offering in May 2013, Voya was a wholly-owned subsidiary of ING Groep N.V., a global financial institution based in the Netherlands. ING Group completely divested its ownership of Voya Financial common stock between 2013 and 2015 and its warrants in 2018.

[3] E*Trade’s predecessor, TradePlus, was founded in Palo Alto, CA in 1982. It began offering trading services via America Online and Compuserve in the early 1990’s. The firm IPO’ed in 1996.

[4] Despite early economic success, the Dean Witter merger ultimately led to an internal power struggle between “Mack the Knife” and Philip Purcell as well as a governance crisis.

[5] The four leading vaccine candidates are well reviewed here:

https://arstechnica.com/science/2020/07/meet-the-4-frontrunners-in-the-covid-19-vaccine-race/

[6] Among “value-ignorant” equity market participants I would include Index Funds/ETFs, Central Banks and most corporate share repurchase plans, the biggest buyer of stocks in recent years. Stocks of Apple, Amazon and Microsoft, which comprise about 1/3 of the Nasdaq 100, are valued at $5 trillion, larger than the German economy and roughly the size of Japan’s economy.

The above letter, dated July 2020, is the update letter of Robotti & Company Advisors, LLC (“Robotti Advisors”) with Ossia Partners Fund, LLC (“OPF”) and was sent to members of OPF. This letter should be read in conjunction with the following disclosure information:

This information is for illustration and discussion purposes only and is not intended to be a recommendation, or an offer to sell, or a solicitation of any offer to open a separate account managed by Robotti & Company Advisors, LLC, nor should it be construed or used as investment, tax, ERISA or legal advice. Any such offer or solicitation will be made only by means of delivery of a presentation, prospectus, account agreement, or other information relating to such investment and only to suitable investors in those jurisdictions where permitted by law. Investors in the Fund must be, at minimum, “accredited investors” within the meaning of Rule 501 of Regulation D under the Securities Act of 1933, as well as, in some cases depending on the specific fund, “qualified purchasers” as defined under the Investment Company Act of 1940.

Further, the contents of this letter should not be relied upon in substitution of the exercise of independent judgment. The information is furnished as of the date shown, and is subject to change and to updating without notice; no representation is made with respect to its accuracy, completeness or timeliness and may not be relied upon for the purposes of entering into any transaction. The information herein is not intended to be a complete performance presentation or analysis and is subject to change. None of Robotti Advisors, as investment advisor to the accounts or products referred to herein, or any affiliate, manager, member, officer, employee or agent or representative thereof makes any representation or warranty with respect to the information provided herein.

The information contained herein has not been provided in a fiduciary capacity, is not to be considered fiduciary investment advice under the Internal Revenue Code or ERISA or a recommendation, and is not intended to be, and should not be considered, as impartial investment advice.

In addition, certain information has been obtained from third party sources and, although believed to be reliable, the information has not been independently verified and its accuracy or completeness cannot be guaranteed. Any investment is subject to risks that include, among others, the risk of adverse or unanticipated market developments, issuer default, and risk of illiquidity. Past performance is not indicative of future results. If interested, please contact us for additional information about our performance related data.

The attached material was provided to investors in a specific Robotti Advisors vehicle at a specific past point of time, advice that may no longer be current or timely. References to past specific holdings of that specific vehicle and matters of related historic fact must be seen in context (as would have been apparent to investors in that vehicle) and are not intended to refer directly or indirectly to specific past recommendations of Robotti Advisors (other than as an indication of language sometimes found in the newsletters). Any reference to a past specific holding or outcome is not intended as representative. None the less, for individuals actively interested in investing in such vehicle, a list of recommendations made by Robotti Advisors with regard to the vehicle in question will be made available on request.

Note: certain statements on the attached material, including but not limited” to (a) statements of things that “are well known” to be the case, (b) statements with the phrase “every single time”, and (c) certain similar statements, are not intended to represent absolute literal fact, but rather represent certain colloquialisms/mannerisms expressed by select market participants (but not necessarily individuals associated with Robotti Advisors).

Opinions contained in this letter reflect the judgment as of the day and time of the publication and are subject to change without notice and may no longer represent its current opinion or advice due to market fluctuations. Robotti Advisors provides investment advisory services to clients other than OPF, and results between clients may differ materially. Robotti Advisors believes that such differences are attributable to different investment objectives and strategies between clients.

The information provided herein is confidential and proprietary and is, and will remain at all times, the property of Robotti & Company Advisors, LLC, as investment manager, and/or its affiliates. The information is being provided for informational purposes only. A copy of Robotti & Company Advisors, LLC’s Form ADV, Part 2 is available upon request. Additional information about the Advisor is also available on the SEC’s website at www.adviserinfo.sec.gov

About The Author: Curtis Jensen

Curtis Jensen is the portfolio manager of the Ossia Partners Fund. Ossia Partners employs a fundamentals-based strategy, grounded in primary research, to identify securities whose public market prices diverge significantly from a conservative estimate of intrinsic or economic value. Prior to joining Robotti & Company Advisors in 2016, Curtis was employed by Third Avenue Management in various roles from 1995 to 2014. Curtis oversaw that firm’s Small-Cap strategy and, from 2003 until 2009, he also served as Co-Chief Investment Officer, along with the firm’s founder, Martin Whitman, until being named sole CIO in January of 2010. Curtis was a member of the firm’s management and risk committees and oversaw the recruiting and mentoring of the firm’s research team. During his tenure at Third Avenue Curtis was a member of the nominating committee of the Board of Directors at Investor AB, Sweden’s leading industrial holding company. Curtis holds a BA in Economics from Williams College and an MBA from Yale University School of Management.

More posts by Curtis Jensen