This article by MOI Global instructor John Lewis is excerpted from a letter of Osmium Partners, based in Greenbrae, California.

Rosetta Stone Inc.[1], together with its subsidiaries, provides technology-based learning products in the United States and internationally. It operates through three segments, Enterprise & Education, Literacy and Consumer. The company develops, markets, and supports a suite of language-learning, literacy, and brain fitness solutions consisting of software products, Web-based software subscriptions, online and professional services, audio practice tools, and mobile applications. Rosetta Stone’s current market capitalization is approximately $361 million. The company generated $192 million in sales for the LTM ending September 30th, 2017. (RST is a holding across all funds.)

Please see below for the transcript of the most recent earnings call where I spoke with CEO John Hass:

We believe RST is growing intrinsic value in Lexia at about $4.00 per share per year, and Lexia alone is worth $12-13 per share in 2018. Our low-end, sum of the parts, distressed valuation now is $24 (using 1x sales for Consumer, Enterprise, and K-12 Language, which is a -75-80% discount to M&A multiples). Using this valuation is not reasonable as Rosetta Stone Consumer brand is known by 80% of Americans (250 million people), Duolingo is doing rounds at 20x revenue or a $800 million valuation with $40 million in sales, Rosetta Stone grew subscribers 11% quarter over quarter to 417,000. Enterprise signed the largest deal in company history for 10,000 seats and $1 million a year from a global Fortune 500 company.

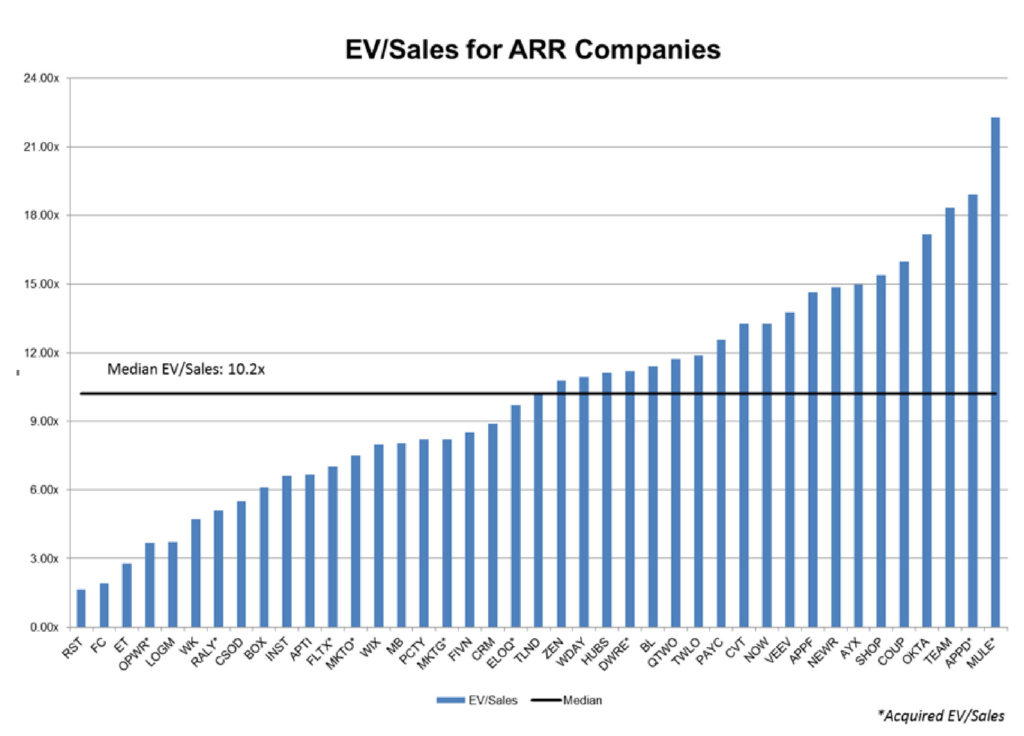

Shown below are Annual Recurring Revenue business models (typically software) with usually 80%+ gross margins, 90%+ annual renewal rates, and typically substantial growth. At first glance, the valuations seem quite high, but given these are very sticky, high margin, high growth businesses we believe these valuations are not unreasonable.

We added FC as the company’s All Access Pass has 85% gross margins and 90%+ annual renewal rates, with substantial growth. RST and FC are the two lowest valued businesses on our chart below.

Rosetta Stone continues to hire strong talent with the most recent hires from Amazon, Microsoft, Gartner group, and iTutorGroup. Jerry Huang was formerly the Global COO of iTutorGroup with a $1 billion+ valuation, and recently joined Rosetta Stone to expand internationally. iTutorGroup had 25,000 tutors in 80 countries. Both the online tutoring and international expertise should really help RST. [link]

Rosetta’s Seattle Office made some key hires and is growing very nicely[2]:

• Christine Chambers, VP of Finance, joined Rosetta Stone from RealNetworks and also worked previously for the Bill & Melinda Gates Foundation.

• Roya Salehi, VP of literacy customer success has been an executive at education companies Achieve3000 and Kaplan;

• Greg Spils, VP of product for the language division, worked at Microsoft, Amazon, Rhapsody and Shazam before joining Rosetta Stone in March;

• Dan Holmes, senior VP of global sales and marketing, spent 14 years at research and consulting powerhouse Gartner.

______

[1] Market price as of the date of dissemination of the letter

[2] https://www.geekwire.com/2018/beyond-yellow-box-rosetta-stone-reinventing-help-growing-seattle-office/

Certain factual and statistical (both historical and projected) industry and market data and other information contained herein was obtained by Osmium Partners from independent, third-party sources that it deems to be reliable. However, Osmium Partners has not independently verified any of such data or other information, or the reasonableness of the assumptions upon which such data and other information was based, and there can be no assurance as to the accuracy of such data and other information. Further, many of the statements and assertions contained herein reflect the belief of Osmium Partners, which belief may be based in whole or in part on such data and other information. The information contained herein is provided for informational purposes only. This is not an offer to sell, or a solicitation to buy, limited partnership interests in Osmium. An investment in Osmium is not suitable for all investors. Graphs/charts are provided for illustrative purposes only and should not be relied on to form an investment decision. Stocks mentioned in the newsletter do not constitute a recommendation to buy or sell the individual securities.

About The Author: John Lewis

Mr. John Hartnett Lewis co-founded Osmium Partners, LLC in 2002 and serves as its Chief Investment Officer and Managing Partner. Mr. Lewis served as a Director of Research at Retzer Capital. He was an Equity Research Analyst at Heartland Advisors, Inc. from March 1999 to January 2001. He served as the President of the University of San Francisco MBA Investment Group, where he managed a small portion of the school's endowment fund. Mr. Lewis served as a Director of Spark Networks, Inc. since July 2, 2014 until November 2, 2017. He served as a Director of Intersections Inc. since October 2015 until August 8, 2017. Mr. Lewis is a Guest Columnist for TheStreet.com. He received an M.B.A. from the University of San Francisco in 1999 and a B.A. from the University of Maryland in 1996.

More posts by John Lewis