Amey Kulkarni of Candor Investing presented his in-depth investment thesis on Ashiana Housing (NSE: ASHIANA) at Asian Investing Summit 2018.

Thesis summary:

Ashiana Housing is a real estate developer with a long growth runway in a country with 1.3 billion people, including 275 million families. Ashiana is a conservatively financed, well-run real estate operation in a country that is rapidly urbanizing, with a housing shortage in urban areas estimated at 18 million units.

Ashiana is run on a business model similar to that used by Mohammed Yunus to build the Grameen Bank in Bangladesh: “First check what the industry peers do and then go and do the exact opposite.”

Given that construction is financed by advances from customers, the company requires little external capital, except during a severe cyclical downturn. Ashiana, with average pretax ROIC of 25+%, is available at an earnings yield (five-year average pretax cash from operations to enterprise value) just below the ten-year government bond yield.

The following transcript has been edited for space and clarity.

Ashiana Housing is an India-based real estate developer with a differentiated business model. Let us first consider how the company has fared relative to the industry and its peers. Over the last almost 11 years, since before the global financial crisis, Ashiana Housing has outperformed all its peers by a ratio of 10:1. This is truly amazing, a phenomenal company performance in the stock returns!

The real estate business is a simple one in terms of how it works. What typically happens in India is you buy land or form a joint venture with the landowner, launch the project, then finish it, and start sales to customers. The customer usually pays 20% of the total agreement value upfront, then the builder goes and gets the building plans approved by the local authorities, after which construction starts. The customer makes payments for every single milestone achieved during construction, so before completion of the project, 95% of the money is typically already paid. The last leg of the project completion and handover is the 5% payment milestone.

To summarize: buy land, collect advance from customers, pay for the construction, and keep the balance as profit (except for buying additional land). A well-run real estate operation needs negative capital employed.

In India, the balance of power is typically with the developer as most customers have already paid upfront a huge amount of their net worth to buy their first or second house before the actual delivery of the project. What then is the perverse incentive for any developer?

As we all know, real estate is a cyclical business. When the going is good, land and property prices appreciate fast, and apartments and houses sell like hotcake.

The typical developer uses the advance from the customers and buys more land before starting construction on the project. Another project is launched in the second parcel of land bought, the developer takes the 20% upfront payment received, buys a third parcel and keeps rotating. The perverse incentive existing for the developers is to grow faster than what their own resources allow them to.

What does this usually mean? What is the reputation of a typical real estate developer in India? WE can find some anecdotal evidence in what some people are saying on websites like Quora. In reply to somebody asking “In what different ways can real estate builders and brokers cheat customers?” Sandeep Pandey answered in March 2015 it could be by “confusing the buyer between carpet area and salable area.” Buyer don’t know what exactly they are getting – how much area, what carpet area, how big the apartment will actually be, when it gets constructed. Developers could also hide additional charges like value added tax and maintenance services, or hype the prospects of the society or the locality. In the second case, they could advertise an upcoming highway, a new commercial IT Park planned very close and coming up in the next few months, and other things along those lines.

In another reply, a Quora member says the first rule is to have a good lawyer beside you when buying a property; observe carefully for clues from frauds and never trust words; and use your contacts to do a background check – fraudsters won’t be first-timers, and they would have left enough clues for you. For due diligence, using a lawyer is a different case, but for deciding whether you like and want to buy a property, first take the lawyer.

Other ways in which developers or brokers cheat people is by collection of booking amount for the same property from multiple people. This is the kind of reputation real estate in general has.

Let’s look at what makes Ashiana Housing’s business model different from what the industry does. We should first consider what the industry thinks about land banks. To construct homes, you need land. Here is an excerpt from the annual report of a reputed peer and one of India’s largest developers, Sobha Developers. It says, “Land portfolio is a distinguishing asset for a real estate company. The ability to acquire appropriate land parcels at strategic places and competitive prices or enter into joint developments for future launches helps maximize profits for the company.” Overall, the industry treats a land bank as a strategic asset. The cheaper and the more you acquire, the better it is.

However, Ashiana Housing says, “We as a company don’t believe in the land banking model.” At any given point of time, land inventory of five to seven times the execution capability is sufficient to achieve the targeted growth in sales and construction, according to the company.

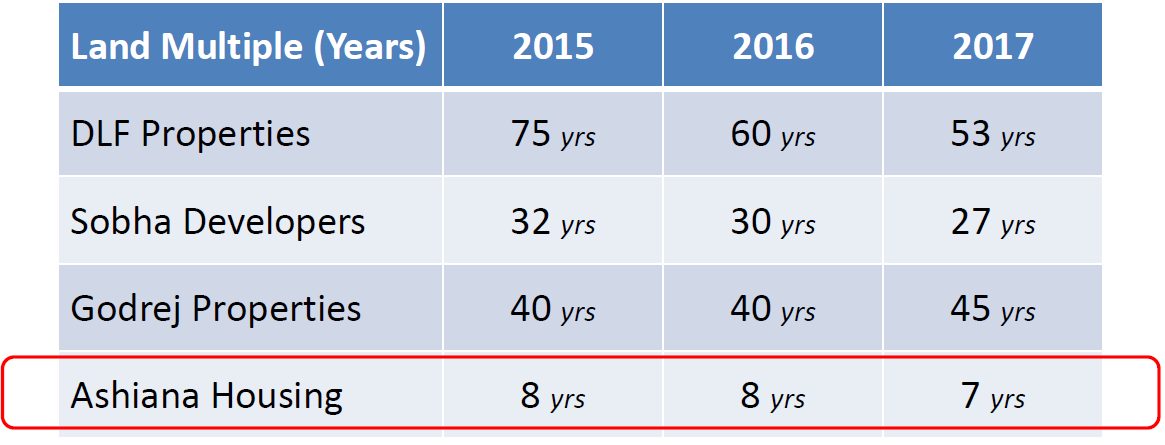

Ashiana Housing vs. Selected Comparables — Land Banks

Source: Amey Kulkarni at Asian Investing Summit 2018.

To measure its progress internally, it uses a metric called a land multiple, which is a total developable land area over equivalent area constructed in the corresponding period. If, for example, Ashiana Housing has the ability to construct, say, one million sq. ft. every year across its multiple projects, it would typically want to have between five to seven million of land inventory so it has enough to grow in the near future but not too much land.

If the pace of construction is similar to what it was in the last trailing year, given the land inventory, how many years will it take a company to construct homes on its entire land? Here’s what the land multiple looks for other industry players. DLF Properties, which is the biggest developer in India, has something like 60 to 70 years of land inventory, while Sobha Developers has around 30 years. Godrej Properties, another reputed builder, has about 40 to 45 years. With Ashiana Housing, it’s 7 to 8 years.

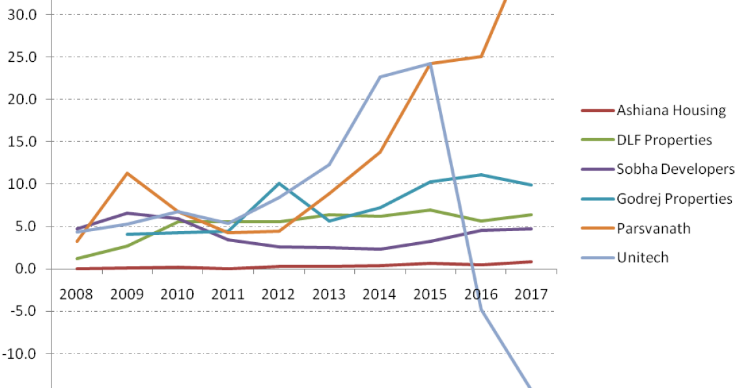

Ashiana does not have capital tied up in land banks, and this has a direct impact on financial leverage and operational flexibility. In studying the debt levels of different companies, I have taken as metric total debt upon EBITDA. For Ashiana Housing, over a 10-year period the total debt upon the EBITDA the company makes every year is a minuscule figure – about 0.1. For most other developers, it is much higher at three to four times, indicating that most of the industry takes a lot of debt to buy and hoard land.

Ashiana Housing vs. Selected Comparables — Debt to EBITDA

Source: Amey Kulkarni at Asian Investing Summit 2018.

What has happened because of this? After the global financial crisis, price appreciation in property stopped and sales velocity tapered off. We can use Unitech as an illustration – it had so much on its plate it started making losses, so EBITDA by total debt turned negative. At companies like Parsvanath, over the last 10 years, total debt by EBITDA has just gone through the roof. This shows excess debt can spiral a company into bankruptcy, which is what happened with Unitech – one of the biggest developers in India before 2008.

Let us now look at who the real estate industry sells to. Buyers can be segmented into two types. One is the end users who will stay in that apartment with their families, and the other are investors with extra money. As in stock markets, investors want to buy into real estate so that six months, one year or five years later, they can sell that property or apartment and make a decent return on their investment.

These two types of buyers prioritize different things. End users would seek amenities for comfortable living, convenience shopping, and hospitals. They would also look for schools nearby because they want their kids to get a good education. End users want a community living; they want to mingle with neighbors and have a good time. Typically, India has joint families, so parents live with their grown-up children and grandparents live with the young kids. People wishing to buy real estate for consumption wants to see whether their parents, who are now in their old age, will be comfortable living there, as well as whether the location of the apartment is convenient for an office commute or the construction is of good quality.

On the other hand, investors would consider things like whether this is a fast-developing locality and if some new highway or a road is being constructed, which will result in appreciation of the property. They would also want a property with exclusive amenities, something no other housing project has in, say, a 5 km or 10 km radius. Investors would look for some new upcoming office complex, which would suddenly increase the value of this property and demand for rental consumption. This type of buyer wants simple, easy payment options, like pay 10% now and 90% on possession.

These are the main differences in what investors and consumers look at. Ashiana Housing chooses not to pitch to the investors. Why? Let’s look at what happens to sales in an up-cycle. When real estate prices are increasing, these cycles last for four to five years, so sales to investors happen very fast in a real estate up-cycle. However, end-user demand tends to be more consistent.

Every sale to a happy customer who stays in an Ashiana property increases word-of-mouth publicity and the brand credibility of the company. This brand reputation continues to positively impact sales and business performance 5, 10, or 15 years down the line. In its brand and marketing communications, Ashiana Housing always targets the end-consumers, telling them they will have a good time living in its project, in its apartment complex. This demand is more consistent and comes from word-of-mouth.

Let’s look at how Ashiana Housing sells to its customers and what the industry does. Typically, the industry uses the help of real estate brokers. That’s because real estate is a project-driven industry, and you want to suddenly ramp up your sales efforts during the launch of some special campaigns or when the real estate project is getting over and you’re not ready for handover.

However, there is a moral hazard associated with using real estate brokers because they are paid commissions and want to sell as fast as possible. Typically, they will promise the customer something that is not available in the project, for example, a certain view or a garden which is probably not going to come up in that project, or the fact that maybe there is no adjacent building that will come up and block the view to the lake, which is, say, one kilometer away from the project.

Instead of a broker-driven model, Ashiana has an in-house sales and marketing team. This ensures greater ownership of customers and helps in selling projects to them in the future. The result is a high proportion of customer referral sales to overall sales due to established brand and high customer satisfaction levels.

Vishal Gupta, one of the promoters of Ashiana Housing, says the following: “Customer touch-point is most crucial. Everything else can be outsourced, but not sales or customer service because every interaction with a customer is an opportunity to further enhance our brand.” He says construction can be outsourced, account keeping can be outsourced, a lot of other things can be outsourced, but any and every interaction with the customer is an opportunity to enhance your brand, so you will never outsource it.

In terms of total sales, what are the referral sales? Referral sales are those which have been done based on word-of-mouth from existing customers. According to the 2013 annual report, over 50% of total sales were through referrals. This illustrates the level of customer satisfaction for Ashiana Housing.

The typical way to incentivize sales is by giving higher commissions when your salespeople achieve higher sales. However, Ashiana Housing’s sales process is different and not incentive-driven. As the company’s MD says, “We have built the sales force in a way that there is no sales incentive in making more sales.”

This is the exact opposite of the common perception of any sales function, where you incentivize for more sales. What Ashiana says is a) we don’t have brokers, so we won’t have third-party people selling our product, and b) we won’t even incentivize our own salespeople to sell more, because, as the MD explains, “If my sales people are missing targets they could misinform or misrepresent to customers, which will hit the very foundation of the trust customers have in the Ashiana brand.”

It also has to look at this from a reputational point of view – how builders cheat, what the reputation of real estate is in India, and how the balance of power is tilted towards the real estate developer because the customer is paying a huge amount upfront to buy the property. In that context, Ashiana Housing wants to maintain the trust the customer has in the brand.

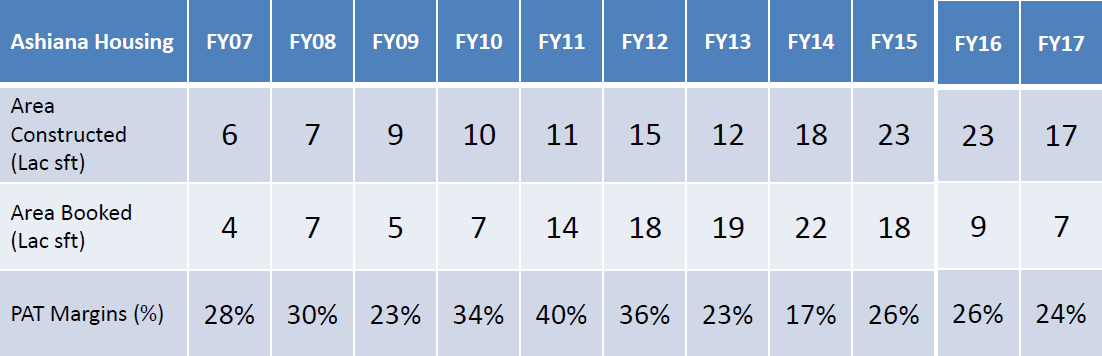

Ashiana Housing — Selected Metrics

Source: Amey Kulkarni at Asian Investing Summit 2018.

We also need to look at how accounting drives management behavior. The revenue recognition policy the entire real estate industry follows is the percentage of completion method. If a real estate project takes about four years from start to finish and we assume – for simplicity – that every year, 25% gets constructed, then the total revenue potential of that project will be spread equally over those four years.

If a company has 15 different projects at different stages of completion, then for the overall financial results declared to the public, it becomes quite difficult to track the performance of the company vis-a-vis each project.

With the percentage completion method, what the company also wants to do is try and increase the profits every year, which is what every company aims for. What does it lead to? Here is a quote from the annual report of one of India’s leading real estate developers: “In accordance with the aforesaid Scheme of Amalgamation, an amount of 137 crores on account of Goodwill on amalgamation has been adjusted from General Reserve and Surplus in the Statement of Profit and Loss instead of amortizing the same in the Statement of Profit and Loss over a period of five years.”

Had the amount been charged to this P&L, the profit for the year would have been lower by 28 crores. The cost and expenses incurred in implementing the scheme have been directly adjusted from the surplus in the P&L account, i.e., the company did an acquisition and suffered a loss. This loss was directly taken to the balance sheet rather than passed through the P&L, so for the next five years, the profits of the company will be shown as higher than what they have been. The loss of 137 crores is directly adjusted from reserves and surplus of the company.

What it is telling the minority shareholders is, we are making great profits and then in the 300-page annual report, in one paragraph on page 179, it is hiding a loss of 137 crores the company suffered when it acquired some other company.

Ashiana recognizes revenue on a project completion basis, i.e., it will toil for four years to construct the project and only when the project is handed over to the customer will it recognize the revenue. The revenue and the profits will be lumpy, and the celebration is only when the project is completed.

Let’s see how this affects management behavior. The MD of Ashiana Housing says in the first paragraph of his annual shareholder letter in 2016, “We had taken Happy Handover as a central theme for last year. The idea was to make the possession process memorable for the customer. So, we are pleased to share that we have achieved a Net Promoter Score of 68% versus our target of 60%.” This KHUSHIMETER, or the Net Promoter Score, is a customer satisfaction number the company achieved.

It’s nothing exceptional; everybody does customer satisfaction surveys. What is typical of Ashiana Housing is that in the shareholders’ letter, right in the first or the second paragraph, the MD wants to share the company is happy handing over so many completed projects to pleased customers.

When we look at the stock, we see it has gone up more than a thousand times in the last 17 years. Ashiana Housing does exactly the opposite of what the industry does. The industry sells through real estate brokers, but not Ashiana Housing. The industry wants to have a large land bank and treats land as a strategic asset. Ashiana Housing says it doesn’t want land above five to seven times its construction execution capability. But the question remains if it is still an investable company? Should we still buy the stock today?

In terms of some financial parameters for Ashiana Housing, we have looked at the area constructed for the last 10 years and the area booked, which is the sales that have happened in the last several years. Every single year from 2007 to 2015, both sales and the area constructed have increased. The PAT margins are between 20% and 30%, i.e., the company is making additional profit from every single square feet of flat or property it has been able to sell.

Over the last three years, sales have tapered off. The real estate industry is in a cyclical downturn and there was, so to say, a deep black swan event – the demonetization of the high currency notes in India, which was done in November 2016. The buyers started expecting real estate prices to fall, and the trade velocity slowed drastically.

This can be seen in the area booked numbers for Ashiana Housing and also for the other developers in the industry. The company keeps making profit for every additional square foot of flat it constructs.

With regard to changes in the industry, the Real Estate (Regulation & Development) Act was approved in 2016, making the industry in India regulated for the first time. One of the main provisions of this act says no sales can be made without getting all the required approvals. It is no longer possible to proceed as before, that is, launch the project, collect the money from the customers, then go for approvals, and move on to construction. Now you first invest in land, obtain the approvals, get the project in place, and only then you can launch it.

The other main provision of this act says 70% of cash flows from the project have to be kept in an escrow account. The money has to be utilized for that particular project. Real estate companies can no longer play the typical game of trying to buy more land from the advances customers have paid.

Another provision says there can be no change in development plan without the consent of customers who have bought the apartments in the real estate project. This used to happen a lot for large township projects where the builder probably has some 100 or 200 acres of land and keeps developing that parcel over, say, 10 years in three to four phases. For phases 1, 2, and 3, the developer will keep saying there is a large cricket stadium, then there is a huge golf course to be constructed, or some 20 acres of green parcel will be there. By the time 7 or 8 years have passed by, the local laws change, urbanization happens, the floor space index changes. The developer can construct more buildings over the same land, and then the development plan itself gets changed. The original buyer who wanted a green lush space suddenly has a concrete jungle.

The likely impact of this real estate bill will include consolidation. Financial muscle power will become more important because now, cash flows from a project will be used only in that particular project. Land and approvals will have to be bought upfront before sales to the customer start. Brand reputation, which already impacts sales velocity, will be even more relevant going into the future. The trade slowdown after the demonetization of 2016 will wipe out many, and that has already happened in the last two years. Typically, land owners or local developers will do a joint venture with a bigger developer that has better repute and a better ability to sell through brand reputation.

What is happening at the company level? Let me quickly read out from the conference call transcript of the third quarter of 2018. One of the investors asked promoter Varun Gupta about the deal with IFC. “Is it to get cheaper debt funding or cheaper equity funding to scale up faster? That is something which I was keen to understand.”

The promoter replied the strategic idea of the deal with International Finance Corporation (IFC) rests on the belief now is a good time to purchase land and get more projects going. “So, whether we’d like to do joint development or to acquire ourselves, the IFC platform gives us the flexibility of doing both the joint development and outright acquisitions. We were not doing outright acquisitions a lot just because they took a lot of capital. Here, the return on capital to IFC is variable dependent on the project performance, with no defined timeline of repayment obligations or defined interest obligations as such. Therefore, what happens is the biggest issue in real estate as such, in terms of capital, is providing capital to purchase land. So, there is an asset liability mismatch that happens because the cash flows from the project are inherently volatile and difficult to estimate as to when they will come or how they will come. What we need is capital that is willing to be sort of patient with the project cash flows. So, if sales happen faster, cash inflow is faster.” What the promoter is saying is the company has tied up with IFC because it is patient capital tolerant to the inherent variability of project cash flows. Given this background of real estate cyclical downturn and the change in regulation, Ashiana Housing is partnering with the right kind of people to get the right nature of capital.

To conclude, let’s look at the valuation of the company. If we take the 5-year average EBITDA, it comes to around 95 crores. The enterprise value (based on market closing prices on 9th March) is about 1,409 crores. The earnings multiple, which is enterprise value over 5-year average EBITDA, comes to about 15.

We have to also remember Ashiana Housing is almost a debt-free company. Currently, it has debt of about 80 crores on its books and the total debt by EBITDA numbers are extremely low.

In summary, this is a high-quality real estate company with a superior business model and debt-to-equity of around 0.1 across business cycles. It operates in a rapidly urbanizing country with 275 million families and favorable structural changes in the industry. In addition, it is focused on cash flow rather than accounting profits and is available at an earnings multiple of 15 at a time when the real estate industry is probably near its cyclical bottom.

The following are excerpts of the Q&A session with Amey Kulkarni:

Q: Is there anything you would prioritize differently in terms of capital allocation or are you satisfied with management’s priorities?

A: This is a family-run business. Three brothers – Vishal, Varun, and Ankur – are now part of the management. Their father started the business. They have always prioritized conservative financial management, taking very low debt and only as much land as they think is necessary to execute in the near future. I don’t see them doing anything differently from what they have done in terms of capital allocation. Their capital allocation skill is one of the key reasons I would want to invest in this company.

Q: Could you tell us what data points you are tracking or someone wanting to invest could track in order to either validate or challenge the thesis?

A: Absolutely. The biggest thing is what sales it does on a yearly basis. We may not track this on a quarterly-quarterly basis but how much sales it can do versus how much construction.

One major risk to a real estate operation is sales not happening. You launch projects, invest in land and then you’re not able to sell. That’s a big problem because cash flow doesn’t come, so one has to track sales.

The second risk is that real estate is a highly localized business. Will the company be able to go to new geographies over a period of three, four, five years? Looking at the history of Ashiana Housing, you can see it entered Bhiwadi – a town 100 km from the Indian capital – in 1991. It has expanded from there, starting initially in Patna, then expanding to Jamshedpur and came to Bhiwadi. In the last 10 years, it has gone to Jodhpur, Jaipur, Pune, Kolkata, and Chennai, which is right across the country. Very few real estate developers are able to do well in multiple cities across the country, and everybody has been trying to be present everywhere. One has to be sensitive to whether the company is able to execute projects and sell in new geographies.

About the instructor:

Amey Kulkarni is an investor in Indian public markets, following a bottom-up investment philosophy. Amey has worked closely with top managements of multi-national corporations in India, including L&T, Jindal Steel, and Siemens for almost a decade in roles in business development, business planning, and project management. At Candor Investing, Amey invests in companies that have the potential to grow five-fold in five years or ten-fold in ten years. Amey invests in companies deriving competitive advantage from unique or innovative business models.

About The Author: MOI Global Editorial Team

The MOI Global Editorial Team, led by John Mihaljevic, CFA, includes community builders, event organizers, writers, editors, research associates, security analysts, and fanatical member support advocates. Our sole purpose is to serve the members of MOI Global as well as we possibly can in order to help them learn, invest intelligently, and build lifelong friendships with like-minded people.

Who is MOI Global? In recent years, The Manual of Ideas has expanded to become more than simply “the very best investing newsletter on the planet” (Mohnish Pabrai). We are now a thriving global community of intelligent investors, connected through great ideas, thought-provoking interviews, online conferences, live member events, and much more.

Members of MOI Global enjoy complimentary access to a growing array of resources and content related to the art of intelligent investing. Members also enjoy preferential access to selected offline events as well as exclusive access to other events hosted by MOI Global, including the Zurich Project Summit, the Latticework Conference, and Ideaweek.

More posts by MOI Global Editorial Team