Shared with permission: Eight terrific companion videos from the new edition of Bruce Greenwald and Judd Kahn's "Value Investing" — featuring Glenn Greenberg, Seth Klarman, Michael Price, Tom Russo, Andrew Weiss, et al. https://t.co/zXZqAfcHdZ

— MOI Global (@manualofideas) November 7, 2020

Ep. 16: Equity Incentives | Reverse DCF as an Analytical Tool

November 7, 2020 in Audio, Diary, Equities, Interviews, Podcast, This Week in Intelligent InvestingWe are delighted to share with you Season 1 Episode 16 of This Week in Intelligent Investing, featuring Phil Ordway of Anabatic Investment Partners, based in Chicago, Illinois; and Elliot Turner of RGA Investment Advisors, based in Stamford, Connecticut. Chris Bloomstran returns in the next episode.

Your host is John Mihaljevic, chairman of MOI Global.

Enjoy the conversation!

In this episode, John Mihaljevic hosts a discussion of:

How equity incentives affect long-term returns: Phil Ordway takes a look at some of the more excessive equity-based compensation practices at public companies, particularly in the tech sector, and how they may dilute long-term investors’ returns. We discuss Twitter and selected other case studies.

Reverse DCF analysis as an analytical tool: Elliot Turner explains how he uses so-called “reverse” discounted cash flow (DCF) models in order to isolate the key variables that drive a company’s valuation. One of Elliot’s preferred analytical tools, reverse DCFs enable him to assess market-implied expectations and to develop a high-conviction variant thesis.

Chris Bloomstran rejoins us in the next episode.

Follow Up

Would you like to get in touch?

Follow This Week in Intelligent Investing on Twitter.

Engage on Twitter with Chris, Elliot, Phil, or John.

Connect on LinkedIn with Chris, Elliot, Phil, or John.

This Week in Intelligent Investing is available on Amazon Podcasts, Apple Podcasts, Google Podcasts, Podbean, Spotify, Stitcher, TuneIn, and YouTube.

If you missed any past episodes, you can listen to them here.

About the Podcast Co-Hosts

Christopher P. Bloomstran, CFA , is the President and Chief Investment Officer of Semper Augustus Investments Group LLC. Chris has more than 25 years of investment experience with a value-driven approach to fundamental equity and industry research. At Semper Augustus, Chris directs all aspects of the firm’s research and portfolio management effort. Prior to forming Semper Augustus in 1998 – in the midst of the stock market and technology bubble – Chris was a Vice President and Portfolio Manager at UMB Investment Advisors. While at UMB Investment Advisors, Chris managed the Trust Investment offices in St. Louis and Denver. Among his investment duties at the firm, he managed the Scout Balanced Fund from the fund’s inception in 1995 until 1998, when he left to start Semper Augustus. Chris received his Bachelor of Science in Business Administration with an emphasis in Finance from the University of Colorado at Boulder, where he also played football. He earned his Chartered Financial Analyst (CFA) designation in 1994. Chris is a member of the CFA Society of St. Louis and of the CFA Institute. He has served on the Board of Directors of the CFA Society of St. Louis since 2002, where he was elected to sequential terms as Vice President from 2005 to 2006, President from 2006 to 2007 and Immediate Past President from 2007 to 2009. Chris has judged the Global Finals and the Americas Finals several times for CFA Institute’s University Global Investment Challenge. Chris served for a number of years as a member of the Bretton Woods Committee in Washington DC, an institution championing and raising awareness of the International Monetary Fund, the World Bank and the World Trade Organization. He has also served on various not-for profit boards in St. Louis. His resides in St. Louis with his wife and two children.

Philip Ordway is Managing Principal and Portfolio Manager of Anabatic Fund, L.P. Previously, Philip was a partner at Chicago Fundamental Investment Partners (CFIP). At CFIP, which he joined in 2007, Philip was responsible for investments across the capital structure in various industries. Prior to joining CFIP, Philip was an analyst in structured corporate finance with Citigroup Global Markets, Inc. from 2002 to 2005. Philip earned his B.S. in Education & Social Policy and Economics from Northwestern University in 2002 and his M.B.A. from the Kellogg School of Management at Northwestern University in 2007, where he now serves as an Adjunct Professor in the Finance Department.

Elliot Turner is a co-founder and Managing Partner, CIO at RGA Investment Advisors, LLC. RGA Investment Advisors runs a long-term, low turnover, growth at a reasonable price investment strategy seeking out global opportunities. Elliot focuses on discovering and analyzing long-term, high quality investment opportunities and strategic portfolio management. Prior to joining RGA, Elliot managed portfolios at at AustinWeston Asset Management LLC, Chimera Securities and T3 Capital. Elliot holds the Chartered Financial Analyst (CFA) designation as well as a Juris Doctor from Brooklyn Law School.. He also holds a Bachelor of Arts degree from Emory University where he double majored in Political Science and Philosophy.

The content of this podcast is not an offer to sell or the solicitation of an offer to buy any security in any jurisdiction. The content is distributed for informational purposes only and should not be construed as investment advice or a recommendation to sell or buy any security or other investment, or undertake any investment strategy. There are no warranties, expressed or implied, as to the accuracy, completeness, or results obtained from any information set forth on this podcast. The podcast participants and their affiliates may have positions in and may, from time to time, make purchases or sales of the securities or other investments discussed or evaluated on this podcast. [dkpdf-remove][/dkpdf-remove]

I think it's mainly a function of value's long underperformance. Even when companies do the right thing, the share price doesn't always (often?) respond. Also, much worse outside of US.

— Riley English (@cardinalcap12) November 6, 2020

Polyus: Low-Cost Russian Gold Miner, with Growing Production

November 6, 2020 in Audio, Equities, Europe, European Investing Summit 2020, European Investing Summit 2020 Featured, Ideas, Large Cap, Materials, TranscriptsMarta Escribano of Salmon Mundi Capital presented her in-depth investment thesis on Polyus (Russia/UK: PLZL) at European Investing Summit 2020.

Thesis summary:

Polyus is the largest Russian gold miner and the fourth-largest globally. It has an outstanding portfolio of six operating mines and one project that could become one of the best gold mines in the world.

Polyus has the third-largest reserve and resource base globally, with 21 years of reserve life, which doubles the average of top ten global peers. The grade of the reserves of 1.8 g/T is much higher than the sector average of 1.3 g/T. Polyus is the lowest-cost producer among the majors in the industry at an all-in sustaining cost (AISC) of $574 pr ounce. Low costs allow Polyus to have one of the best EBITDA margins in the sector (67% in 2019 vs. sector average of 42%). Polyus is increasing production in an industry in which growth is difficult to achieve. It brought into operation Natalka at the end of 2018 and could commence production at Sukhoil Log in 2026. The latter is the third-largest greenfield asset in the world, with 63 million ounces in resources, a forty-year mine life, and a grade of 2.1 g/T.

Polyus has been free cash flow positive throughout the cycle.

The full session is available exclusively to members of MOI Global.

Members, log in below to access the full session.

Not a member?

Thank you for your interest. Please note that MOI Global is closed to new members at this time. If you would like to join the waiting list, complete the following form:

About the instructor:

Marta Escribano has been working in financial markets for more than a decade. She became principal analyst in 2013. Formerly she worked for three years in the Treasury Department of Banco Popular at the FX and fixed income desk. Before that, she had joined the Treasury of Inversis Bank and the international equity desk of Interdin as equity sales trader advising mostly Swiss and Italian clients. Since the beginning of her professional career she has been passionate about financial markets because they are global, changing and are related to human psychology. Her interest in the Austrian School of Economics began after reading “Money, Bank Credit and Economic Cycles” by Huerta de Soto. She holds a Bachelor´s Degree in Law from the Universidad Pontificia Comillas (ICADE; E-1) and a Master’s Degree in Financial Markets and Alternative Investments (MFIA). Her main hobbies are travelling around the world, reading philosophy books, officiating at triathlon events and running. She speaks Spanish, English, Italian and German.

The content of this website is not an offer to sell or the solicitation of an offer to buy any security. The content is distributed for informational purposes only and should not be construed as investment advice or a recommendation to sell or buy any security or other investment, or undertake any investment strategy. There are no warranties, expressed or implied, as to the accuracy, completeness, or results obtained from any information set forth on this website. BeyondProxy’s officers, directors, employees, and/or contributing authors may have positions in and may, from time to time, make purchases or sales of the securities or other investments discussed or evaluated herein.

Swatch: Leading Swiss Watch Maker, with Overcapitalized Balance Sheet

November 5, 2020 in Audio, Consumer Discretionary, Equities, Europe, European Investing Summit 2020, European Investing Summit 2020 Featured, Ideas, Large Cap, TranscriptsSamuel S. Weber of SW Kapitalpartner GmbH presented his investment thesis on Swatch Group (Switzerland: UHR) at European Investing Summit 2020.

The full session is available exclusively to members of MOI Global.

Members, log in below to access the full session.

Not a member?

Thank you for your interest. Please note that MOI Global is closed to new members at this time. If you would like to join the waiting list, complete the following form:

About the instructor:

Samuel S. Weber is an independent wealth manager based in Zug, Switzerland. He is a passionate value investor, who is focused on generating long-term, market beating returns by investing in high-quality opportunities in the stock market and providing patient capital to SMEs with the overall aim of fostering productive investments in Switzerland and Europe. To achieve the latter, he founded the SW Kapitalpartner GmbH (www.swkapitalpartner.com). Samuel holds a master’s degree in strategy and international management from the University of St. Gallen.

The content of this website is not an offer to sell or the solicitation of an offer to buy any security. The content is distributed for informational purposes only and should not be construed as investment advice or a recommendation to sell or buy any security or other investment, or undertake any investment strategy. There are no warranties, expressed or implied, as to the accuracy, completeness, or results obtained from any information set forth on this website. BeyondProxy’s officers, directors, employees, and/or contributing authors may have positions in and may, from time to time, make purchases or sales of the securities or other investments discussed or evaluated herein.

Ep. 15: Dividend Policy | Forecasting Surprises and Disasters

November 3, 2020 in Audio, Diary, Equities, Interviews, Podcast, This Week in Intelligent InvestingWe are delighted to share with you Season 1 Episode 15 of This Week in Intelligent Investing, featuring Chris Bloomstran of Semper Augustus Investments Group, based in St. Louis, Missouri; and Phil Ordway of Anabatic Investment Partners, based in Chicago, Illinois. Elliot Turner returns in the next episode.

Your host is John Mihaljevic, chairman of MOI Global.

Enjoy the conversation!

In this episode, John Mihaljevic hosts a discussion of:

Dividend payout policy as part of overall capital allocation: Chris Bloomstran casts a critical eye toward the tax (in)efficiency of dividends and the decision-making process behind corporate boards’ dividend policies. We discuss the utility of dividends within a capital allocation framework.

Forecasting surprises (and disasters) based on a Phil Tetlock article: Phil Ordway shares insights from a recent Phil Tetlock article and takes a look at the conditions under which forecasting can add value. We discuss the role of forecasting in equity valuation and investment decision-making processes.

Elliot Turner rejoins us in the next episode.

Related Links

Chris Bloomstran segment:

- Letter to Disney, by Semper Augustus

Phil Ordway segment:

- A Better Crystal Ball, by Peter Scoblic and Phil Tetlock

- Superforecasting, by Phil Tetlock

- Expert Political Judgment, by Phil Tetlock

Follow Up

Would you like to get in touch?

Follow This Week in Intelligent Investing on Twitter.

Engage on Twitter with Chris, Elliot, Phil, or John.

Connect on LinkedIn with Chris, Elliot, Phil, or John.

This Week in Intelligent Investing is available on Amazon Podcasts, Apple Podcasts, Google Podcasts, Podbean, Spotify, Stitcher, TuneIn, and YouTube.

If you missed any past episodes, you can listen to them here.

About the Podcast Co-Hosts

Christopher P. Bloomstran, CFA , is the President and Chief Investment Officer of Semper Augustus Investments Group LLC. Chris has more than 25 years of investment experience with a value-driven approach to fundamental equity and industry research. At Semper Augustus, Chris directs all aspects of the firm’s research and portfolio management effort. Prior to forming Semper Augustus in 1998 – in the midst of the stock market and technology bubble – Chris was a Vice President and Portfolio Manager at UMB Investment Advisors. While at UMB Investment Advisors, Chris managed the Trust Investment offices in St. Louis and Denver. Among his investment duties at the firm, he managed the Scout Balanced Fund from the fund’s inception in 1995 until 1998, when he left to start Semper Augustus. Chris received his Bachelor of Science in Business Administration with an emphasis in Finance from the University of Colorado at Boulder, where he also played football. He earned his Chartered Financial Analyst (CFA) designation in 1994. Chris is a member of the CFA Society of St. Louis and of the CFA Institute. He has served on the Board of Directors of the CFA Society of St. Louis since 2002, where he was elected to sequential terms as Vice President from 2005 to 2006, President from 2006 to 2007 and Immediate Past President from 2007 to 2009. Chris has judged the Global Finals and the Americas Finals several times for CFA Institute’s University Global Investment Challenge. Chris served for a number of years as a member of the Bretton Woods Committee in Washington DC, an institution championing and raising awareness of the International Monetary Fund, the World Bank and the World Trade Organization. He has also served on various not-for profit boards in St. Louis. His resides in St. Louis with his wife and two children.

Philip Ordway is Managing Principal and Portfolio Manager of Anabatic Fund, L.P. Previously, Philip was a partner at Chicago Fundamental Investment Partners (CFIP). At CFIP, which he joined in 2007, Philip was responsible for investments across the capital structure in various industries. Prior to joining CFIP, Philip was an analyst in structured corporate finance with Citigroup Global Markets, Inc. from 2002 to 2005. Philip earned his B.S. in Education & Social Policy and Economics from Northwestern University in 2002 and his M.B.A. from the Kellogg School of Management at Northwestern University in 2007, where he now serves as an Adjunct Professor in the Finance Department.

Elliot Turner is a co-founder and Managing Partner, CIO at RGA Investment Advisors, LLC. RGA Investment Advisors runs a long-term, low turnover, growth at a reasonable price investment strategy seeking out global opportunities. Elliot focuses on discovering and analyzing long-term, high quality investment opportunities and strategic portfolio management. Prior to joining RGA, Elliot managed portfolios at at AustinWeston Asset Management LLC, Chimera Securities and T3 Capital. Elliot holds the Chartered Financial Analyst (CFA) designation as well as a Juris Doctor from Brooklyn Law School.. He also holds a Bachelor of Arts degree from Emory University where he double majored in Political Science and Philosophy.

The content of this podcast is not an offer to sell or the solicitation of an offer to buy any security in any jurisdiction. The content is distributed for informational purposes only and should not be construed as investment advice or a recommendation to sell or buy any security or other investment, or undertake any investment strategy. There are no warranties, expressed or implied, as to the accuracy, completeness, or results obtained from any information set forth on this podcast. The podcast participants and their affiliates may have positions in and may, from time to time, make purchases or sales of the securities or other investments discussed or evaluated on this podcast. [dkpdf-remove]

[/dkpdf-remove]

Christian Billinger: In Defence of Cognitive Biases

October 29, 2020 in Commentary, Equities, Portfolio Management, Risk Management, SkillsThis article is authored by Christian Billinger, Investor at Billinger Förvaltning, a Sweden-based, family-held investment company with no external capital.

Background

Behavioural finance, as applied in the world of investing, often focuses on perceived irrationalities in decision making. It has become increasingly popular for investors to attempt to ‘correct’ for some of these perceived irrationalities by making changes to their investment process etc.

We are certainly not disputing the results of the controlled experiments that form the basis for much of this research, or the validity of many of the concepts developed by people like Kahneman etc. We would also point out that while behavioural finance texts often refer to ‘errors of judgment’ etc in our way of thinking, some leading researchers in the field also emphasise that their message is simply that traditional economic models are poor at describing human behaviour (rather than pointing out that we as humans are poor at making decisions under uncertainty).

What we are questioning is the approach of taking these insights and directly applying them to a ‘real world’ environment where we are dealing with unknown (and unknowable) payoffs and probabilities. We find that what is considered a ‘bias’ is in fact often a rational and pragmatic rule for dealing with an uncertain and complex environment, especially by those who have spent considerable time developing expertise in the field. The ambition with this article is to provide a few examples of when what is described as irrational in behavioural finance research makes perfect sense when applied to the ‘real world’.

Another aspect to consider is that the claims of behavioural finance theorists are often based on individual behaviour as opposed to large aggregates like financial markets, which reflect the behaviour of very large numbers of actors. This makes the relevance of these ideas in practice even less clear.

What the research suggests is that most of the time, intuitive thinking works relatively well. This intuition is often also the result of long practice in a specific field. However, intuitive thinking is less likely to work well under time pressure and other kinds of stresses which is one reason why Guy Spier’s contributions around creating the ‘right’ environment are so important; in his excellent book, The Education of a Value Investor, he shows us how he created a better environment for himself as an investor and we can all learn from him in trying to create our best possible investment environment.

Behavioural finance and research into cognitive ‘biases’ is today a very large field and as a result we will necessarily need to focus on a few aspects that we feel are key for long-term equity investors; we have there picked four topics/’biases’ that we think are highly relevant to equity investors. Much of our thinking on this topic has been formed by thinking on heuristics and biases (especially Kahneman), decision making under uncertainty (especially Taleb and Kelly) as well as the practical insights of Warren Buffett and Charlie Munger, Tom Gayner, Guy Spier, Mohnish Pabrai, Nick Train, Terry Smith etc.

Ultimately we are trying to follow Charlie Munger’s advice when he says, ‘Figure out what works and do it’. That really is the essence of what we are trying to describe. We have also tried to include some examples of possible applications of each ‘bias’ in equity investing. The text is not a technical investigation of these issues but rather a look at things that have worked for us (and others) in the past and where we believe there is reason to believe they will do so in future.

Our ‘solution’ to dealing with these supposed ‘biases’ is therefore the following:

1) Create a peaceful environment for reading, reflection and discussion (in order to reduce the impact of emotions on decision-making; this is when expertise and heuristics etc are less likely to work well).

2) Apply your expertise, if you are operating within a field where it is relevant (this is the ‘circle of competence’; if you are not within this circle you shouldn’t be trying to answer the question to begin with).

3) Apply heuristics if there is no explicit experience to draw on, but only after having gone through steps 1) and 2) above.

The examples below also fit well with our philosophy of being long-term investors in a small number of great businesses.

A look at some cognitive ‘biases’ as relates to long-term equity investing

1) Loss aversion

Simply put, loss aversion is the idea that the negative feelings associated with a loss of a certain size are much more significant than the positive feelings associated with a gain of the same size.

In real life, loss aversion often makes sense; we are dealing with time series of returns where we must do everything we can to eliminate the ‘zeros’ (i.e. going out of business/losing all our capital). Expected values are relevant in a controlled environment of repeated bets etc but not in the ‘real world’ where blowing up means we are no longer participating in the game (although in institutional money management it is of course common to set up new vehicles following failure).

One example of an application of this idea in equity investing would be the price targets established by sell-side analysts. Often, these incorporate some form of ‘scenario analysis’ whereby the analyst details a bullish scenario, a base case and a bearish scenario with different payoffs and probabilities assigned to each. This then aggregates into a target price and the idea would be to buy if shares are trading below this ‘intrinsic value’ and vice versa.

The issue with this is that depending on your temperament, level of diversification, any financial leverage etc your ability to withstand a loss on an investment will differ. This can mean that e.g. even if there seems to be significant upside based on where shares are trading currently, you may be unwilling to invest because you find the downside (even if considered unlikely to materialise) too large.

Our solution to this problem is 1) don’t look at price targets, 2) always consider the potential downside of an investment first and 3) consider the investment as part of your overall portfolio.

More generally, we try to avoid permanent loss of capital in a number of ways e.g. by buying great businesses, by some diversification, by not using any financial leverage etc.

2) Mental accounting

Mental accounting is a process whereby we categorise different financial outcomes and entities.

Sometimes we think this makes sense, sometimes not; let us provide two examples.

In the case of ‘playing with house money’, it is well established (by John Kelly and others) that increasing your bets as a result of winning makes perfect sense, just as reducing your bets as a result of losing makes sense. One obvious advantage of this policy is that (in principle), we eliminate the possibility of going bust. Another advantage is that we participate in the upside through compounding of our capital.

In practical terms, we believe one of the easiest ways to achieve this to some extent is by employing a buy-and-hold philosophy with some cash holdings. This way, our exposure to the market and to specific securities increases as they increase in value and vice versa with the cash component eliminating risk of ruin.

In other cases, we think mental accounting makes less sense and this is e.g. when it comes to total returns and their composition. It is quite common to invest a portion of a portfolio into securities with high dividend yields, in order to satisfy cash flow needs. We would argue that it makes more sense to invest based on the outlook for total returns and to make partial disposals to the extent one needs liquidity. These disposals can replace dividends and we can then focus on generating the ‘optimal’ total return (which is not necessarily, or even probably, the highest possible expected return). We focus on total returns and expect dividend payout ratios etc to be a reflection of capital allocation decisions and reinvestment opportunities in the businesses of which we are shareholders (although, of course, many high quality durable businesses also tend to be reliable dividend stocks).

This just goes to show that instead of simply accepting labels like ‘mental accounting’, we as investors need to think independently about these issues and their application.

3) Commitment bias

For those who have read Robert Cialdini’s book on influencing other people, the idea of commitment and consistency is familiar. In investing, most of us have heard the advice ‘Never fall in love with a stock…’ (as expressed by Peter Lynch and others).

For us as long-term investors, we feel that this is not always very useful advice. While we constantly monitor our portfolio companies and spend much of our time thinking about what we might have missed, it is essential to have a deep commitment to our holdings. A reluctance to sell anything is an almost inevitable aspect of true long-term investing; while ideally we would like to hold on to our winners and get rid of the losers, it is very difficult to know in advance which of our holdings belong to which category! We prefer to hold on to our investments until there is clear evidence things are ‘going wrong’ (unfortunately, this is not usually clear until very late in the game).

In the words of Nick Train: ‘There’s a piece of stock market wisdom that we strongly disagree with, and that’s the piece of stock market wisdom that says you should never fall in love with your investments. We profoundly disagree with that. We think it’s absolutely critical to fall in love with, or have deep, deep commitment, both intellectual commitment and, if you like, emotional commitment to the ideas that you build into an investment portfolio. How else are you going to stick through thick and thin…in order to capture the full potential of an investment?’

Other harmful side effects of lack of commitment can be high portfolio turnover and lack of direction in our portfolio management activities.

One excellent way to actually create some commitment is to talk about ideas in a forum like MOI Global, where we also have an opportunity to get challenged by some very intelligent and skilled investors (of course, many investors find it is better not to speak publicly about their holdings in order not to develop excessive commitment). However, please note that it is absolutely essential to be willing to listen to the other side of the argument; one of the things we do before making an investment is to ask ourselves ‘what could cause this to be a terrible investment?’ and we repeat this exercise constantly for all of our holdings. The point is not to change course simply because the market value of our portfolio fluctuates or for other arbitrary reasons.

4) Endowment effect

The endowment effect is the idea that we often value an item more when already possessing it.

As long-term investors, it makes perfect sense to us that we are more committed to an idea about which we know something, than one about which we know nothing. We often hear the following; ‘if you would not buy the shares today, you should not be holding them’. We disagree.

Apart from taxes and transaction costs, there are a few reasons we think that the endowment effect makes sense in many cases. One is that over time, we learn more and more about the businesses in which we are invested and this is usually a form of learning that would not take place on the same level would we not have skin in the game. For an example of this, look at Tom Gayner and his practice of buying very small stakes in a large number of businesses that he then follows more closely than he would have otherwise. Thus, already being invested in a business makes it qualitatively different to us.

Another reason why the endowment effect makes a lot of sense to us is the concept of ‘margin of safety’. According to economic theory, the highest price at which we are willing to buy a product or service and the lowest price at which we are willing to sell the same product or service should be almost identical. In reality, we are often unwilling to sell a great business at valuations that are much higher than those at which we would be prepared to buy the same business. This is a reflection of ‘margin of safety’ and recognition of how little we know. There is very little precision involved in valuing equities for a long-term investor and we don’t want to make the mistake of working towards ‘false precision’.

In addition, we can think of several other reasons why this effect might make sense like reinvestment risk, scarcity of high quality assets etc.

Conclusion

We take a pragmatic approach to investing. As part of this, we think there are certain behaviours that make sense simply because they have stood the test of time and because they suit our temperament and structure e.g. worrying about the downside, taking a long-term view, investing in what we know etc.

Behavioural finance research has challenged a number of these approaches. While it is always valuable to consider alternative theories in order to challenge one’s own beliefs, we try to remember to think independently. For the last few years, the money management industry has been enamoured with thinking around cognitive ‘biases’ and how to correct for these despite the fact that these ‘biases’ often make sense in real life situations. What often seems to happen is that parts of the industry either misunderstands the true meaning of an idea, like in the case of ‘Black Swan’ events, or that it takes a sensible idea too far.

Ultimately, the golden rule remains; ‘figure out what works and do it’. It is as simple, and as hard, as that.

download printable version

Special Edition: The Logistics of Food Delivery, with Isaac Schwartz

October 28, 2020 in Audio, Diary, Equities, Interviews, Podcast, This Week in Intelligent InvestingWe are delighted to share with you a special edition of This Week in Intelligent Investing, featuring Isaac Schwartz of Robotti & Company in a conversation with Elliot Turner of RGA Investment Advisors. The two investors discuss Isaac’s long arc with the logistics behind food delivery.

How Isaac’s interest in food delivery logistics was born: A history of Isaac’s involvement with Net-a-Porter and studying opportunities to introduce disruptive logistics, based on ground-up, dedicated architecture, to established supply chains.

A deep dive on Ocado: What makes Ocado such a unique opportunity and how the business has evolved from a supermarket with great technology to a technology platform.

Experience leads to HKTV: How Isaac’s global perspective and long history with food delivery logistics put this opportunity on his plate.

Enjoy the conversation!

Follow Up

Would you like to get in touch?

Follow This Week in Intelligent Investing on Twitter.

Engage on Twitter with Chris, Elliot, Phil, or John.

Connect on LinkedIn with Chris, Elliot, Phil, or John.

This Week in Intelligent Investing is available on Amazon Podcasts, Apple Podcasts, Google Podcasts, Podbean, Spotify, Stitcher, TuneIn, and YouTube.

If you missed any past episodes, you can listen to them here.

About the Podcast Co-Hosts

Christopher P. Bloomstran, CFA , is the President and Chief Investment Officer of Semper Augustus Investments Group LLC. Chris has more than 25 years of investment experience with a value-driven approach to fundamental equity and industry research. At Semper Augustus, Chris directs all aspects of the firm’s research and portfolio management effort. Prior to forming Semper Augustus in 1998 – in the midst of the stock market and technology bubble – Chris was a Vice President and Portfolio Manager at UMB Investment Advisors. While at UMB Investment Advisors, Chris managed the Trust Investment offices in St. Louis and Denver. Among his investment duties at the firm, he managed the Scout Balanced Fund from the fund’s inception in 1995 until 1998, when he left to start Semper Augustus. Chris received his Bachelor of Science in Business Administration with an emphasis in Finance from the University of Colorado at Boulder, where he also played football. He earned his Chartered Financial Analyst (CFA) designation in 1994. Chris is a member of the CFA Society of St. Louis and of the CFA Institute. He has served on the Board of Directors of the CFA Society of St. Louis since 2002, where he was elected to sequential terms as Vice President from 2005 to 2006, President from 2006 to 2007 and Immediate Past President from 2007 to 2009. Chris has judged the Global Finals and the Americas Finals several times for CFA Institute’s University Global Investment Challenge. Chris served for a number of years as a member of the Bretton Woods Committee in Washington DC, an institution championing and raising awareness of the International Monetary Fund, the World Bank and the World Trade Organization. He has also served on various not-for profit boards in St. Louis. His resides in St. Louis with his wife and two children.

Philip Ordway is Managing Principal and Portfolio Manager of Anabatic Fund, L.P. Previously, Philip was a partner at Chicago Fundamental Investment Partners (CFIP). At CFIP, which he joined in 2007, Philip was responsible for investments across the capital structure in various industries. Prior to joining CFIP, Philip was an analyst in structured corporate finance with Citigroup Global Markets, Inc. from 2002 to 2005. Philip earned his B.S. in Education & Social Policy and Economics from Northwestern University in 2002 and his M.B.A. from the Kellogg School of Management at Northwestern University in 2007, where he now serves as an Adjunct Professor in the Finance Department.

Elliot Turner is a co-founder and Managing Partner, CIO at RGA Investment Advisors, LLC. RGA Investment Advisors runs a long-term, low turnover, growth at a reasonable price investment strategy seeking out global opportunities. Elliot focuses on discovering and analyzing long-term, high quality investment opportunities and strategic portfolio management. Prior to joining RGA, Elliot managed portfolios at at AustinWeston Asset Management LLC, Chimera Securities and T3 Capital. Elliot holds the Chartered Financial Analyst (CFA) designation as well as a Juris Doctor from Brooklyn Law School.. He also holds a Bachelor of Arts degree from Emory University where he double majored in Political Science and Philosophy.

The content of this podcast is not an offer to sell or the solicitation of an offer to buy any security in any jurisdiction. The content is distributed for informational purposes only and should not be construed as investment advice or a recommendation to sell or buy any security or other investment, or undertake any investment strategy. There are no warranties, expressed or implied, as to the accuracy, completeness, or results obtained from any information set forth on this podcast. The podcast participants and their affiliates may have positions in and may, from time to time, make purchases or sales of the securities or other investments discussed or evaluated on this podcast. [dkpdf-remove]

[/dkpdf-remove]

Ep. 14: Unstoppable Automation | Value Traps and IBM | Index Data

October 28, 2020 in Audio, Diary, Equities, Interviews, Podcast, This Week in Intelligent InvestingWe are delighted to share with you Season 1 Episode 14 of This Week in Intelligent Investing, featuring Chris Bloomstran of Semper Augustus Investments Group, based in St. Louis, Missouri; Phil Ordway of Anabatic Investment Partners, based in Chicago, Illinois; and Elliot Turner of RGA Investment Advisors, based in Stamford, Connecticut.

Your host is John Mihaljevic, chairman of MOI Global.

Enjoy the conversation!

In this episode, John hosts a discussion of:

The implications of automation: Elliot Turner examines the megatrend of automation from both a societal and investment perspective. We discuss how automation is accelerating in new areas today. We explore the key investment implications and highlight several public companies.

The concept of value traps: Phil Ordway shares his perspective on the widely used term “value trap” and explains why investors may want to focus more on cash flow and less on stated earnings. We discuss what differentiates an undervalued business from a value trap and examine IBM as a case study.

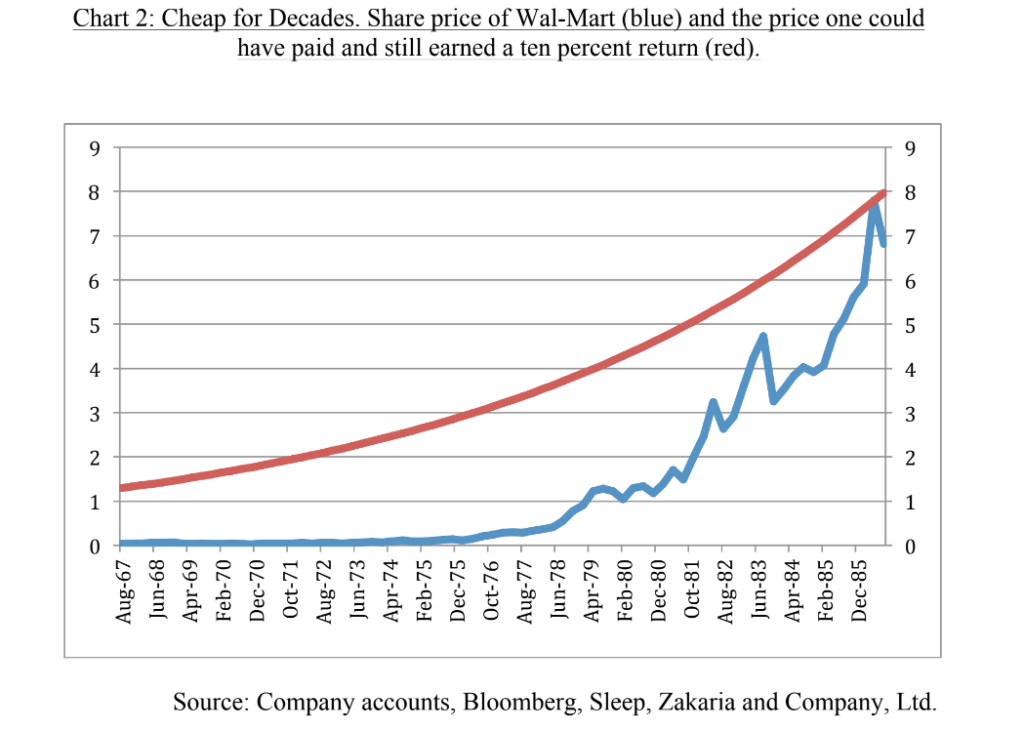

Recap of stock market index data: Chris Bloomstran looks at the major U.S. stock market indices and their composition at the end of Q3, noting that the top five constituents of the S&P 500 Index have risen 38% YTD, on average, while the bottom 495 stocks have declined 5%, on average. We discuss the nuances of the unprecedented concentration of market cap in the largest companies.

Related Links

Value traps segment:

- The Rise and Fall of American Growth, by Robert J. Gordon

- The future of work and innovation, a debate

- “Techno-optimist” Erik Brynjolfsson Takes on Robert Gordon, by WSJ

- Boom or Gloom, by Thomas B. Edsall in The New York Times

Automation segment:

- More Than You Know, by Michael Mauboussin

- The Structures of Everyday Life, by Fernand Braudel

- Nick Sleep’s chart of what to pay for Walmart for a 10% return:

Follow Up

Would you like to get in touch?

Follow This Week in Intelligent Investing on Twitter.

Engage on Twitter with Chris, Elliot, Phil, or John.

Connect on LinkedIn with Chris, Elliot, Phil, or John.

This Week in Intelligent Investing is available on Amazon Podcasts, Apple Podcasts, Google Podcasts, Podbean, Spotify, Stitcher, TuneIn, and YouTube.

If you missed any past episodes, you can listen to them here.

About the Podcast Co-Hosts

Christopher P. Bloomstran, CFA , is the President and Chief Investment Officer of Semper Augustus Investments Group LLC. Chris has more than 25 years of investment experience with a value-driven approach to fundamental equity and industry research. At Semper Augustus, Chris directs all aspects of the firm’s research and portfolio management effort. Prior to forming Semper Augustus in 1998 – in the midst of the stock market and technology bubble – Chris was a Vice President and Portfolio Manager at UMB Investment Advisors. While at UMB Investment Advisors, Chris managed the Trust Investment offices in St. Louis and Denver. Among his investment duties at the firm, he managed the Scout Balanced Fund from the fund’s inception in 1995 until 1998, when he left to start Semper Augustus. Chris received his Bachelor of Science in Business Administration with an emphasis in Finance from the University of Colorado at Boulder, where he also played football. He earned his Chartered Financial Analyst (CFA) designation in 1994. Chris is a member of the CFA Society of St. Louis and of the CFA Institute. He has served on the Board of Directors of the CFA Society of St. Louis since 2002, where he was elected to sequential terms as Vice President from 2005 to 2006, President from 2006 to 2007 and Immediate Past President from 2007 to 2009. Chris has judged the Global Finals and the Americas Finals several times for CFA Institute’s University Global Investment Challenge. Chris served for a number of years as a member of the Bretton Woods Committee in Washington DC, an institution championing and raising awareness of the International Monetary Fund, the World Bank and the World Trade Organization. He has also served on various not-for profit boards in St. Louis. His resides in St. Louis with his wife and two children.

Philip Ordway is Managing Principal and Portfolio Manager of Anabatic Fund, L.P. Previously, Philip was a partner at Chicago Fundamental Investment Partners (CFIP). At CFIP, which he joined in 2007, Philip was responsible for investments across the capital structure in various industries. Prior to joining CFIP, Philip was an analyst in structured corporate finance with Citigroup Global Markets, Inc. from 2002 to 2005. Philip earned his B.S. in Education & Social Policy and Economics from Northwestern University in 2002 and his M.B.A. from the Kellogg School of Management at Northwestern University in 2007, where he now serves as an Adjunct Professor in the Finance Department.

Elliot Turner is a co-founder and Managing Partner, CIO at RGA Investment Advisors, LLC. RGA Investment Advisors runs a long-term, low turnover, growth at a reasonable price investment strategy seeking out global opportunities. Elliot focuses on discovering and analyzing long-term, high quality investment opportunities and strategic portfolio management. Prior to joining RGA, Elliot managed portfolios at at AustinWeston Asset Management LLC, Chimera Securities and T3 Capital. Elliot holds the Chartered Financial Analyst (CFA) designation as well as a Juris Doctor from Brooklyn Law School.. He also holds a Bachelor of Arts degree from Emory University where he double majored in Political Science and Philosophy.

The content of this podcast is not an offer to sell or the solicitation of an offer to buy any security in any jurisdiction. The content is distributed for informational purposes only and should not be construed as investment advice or a recommendation to sell or buy any security or other investment, or undertake any investment strategy. There are no warranties, expressed or implied, as to the accuracy, completeness, or results obtained from any information set forth on this podcast. The podcast participants and their affiliates may have positions in and may, from time to time, make purchases or sales of the securities or other investments discussed or evaluated on this podcast. [dkpdf-remove]

[/dkpdf-remove]

On the topic of investment firms accentuating differences rather than trying to be well rounded: quite a few of the stockpicking firms I know who have produced the best returns…

— Joel Cohen (@joelmcohen) October 26, 2020