This article is authored by MOI Global instructor Stuart Mitchell, investment manager at S. W. Mitchell Capital, based in London.

Let us start with a short quiz, a Challenge, if you will. I am going to list the financial characteristics of five banks – for the moment I will call them BlueBank, GreenBank, YellowBank, RedBank and GreyBank. I will then ask you to match them with their market valuation metrics.

So, here we go.

Financial characteristics

Valuation metrics

Source: Exane, company annual reports.

You may well have guessed that GreenBank goes with A: GreenBank generates a paltry 1.6% on equity and trades at just 0.2x book. It also has a very high 93.1% cost income ratio. Not too difficult.

Now it gets a bit trickier. GreyBank looks like it could go with valuation D. The highest RoE (16.4%) is, as you might expect, rewarded by the highest price to book value (1.1x). But then again, maybe this valuation is YellowBank’s. YellowBank dominates its local market, derives almost half of all revenues from fee income, is well-capitalised, has the second highest RoE and the second lowest CIR.

Wrong. YellowBank in fact carries valuation E; those top-notch characteristics trade on a measly 0.6x book value, and YellowBank throws off a dividend yield of no less than 9.5%. But enough suspense. Time to drop the colour-coding and reveal all: YellowBank is Intesa Sanpaolo.[1]

Intesa Sanpaolo is by far the largest bank in Italy with an 18% market share in loans and deposits (as shown in the table above). Just as importantly – perhaps more so – the bank has over 20% market shares in the lucrative asset management, pension funds and factoring markets.

The business is highly diverse, with 48% of revenues coming from wealth management and insurance.

And since 2013-14, when net income was under peak pressure, the recovery has been strong, and it has been consistent:

With financial and commercial characteristics of the business as impressive as this, how can it be that the market accords Intesa such a lowly valuation?

There are three main reasons in our view.

1/ Cost cutting under-appreciated.

That the Italian backdrop is subdued is no secret. But this is causing the market to fail to appreciate the opportunity for the bank to increase returns significantly by cutting costs. The bank has put in place a highly ambitious cost-cutting programme which includes branch closures, redundancies, Information Communication Technology integration, the centralisation of procurement and – above all – digitalisation. Assuming no more than a modest 2.8% per annum net interest income growth and 5.5% annual growth in net fee income, the bank should be able to generate the following returns before 2022:

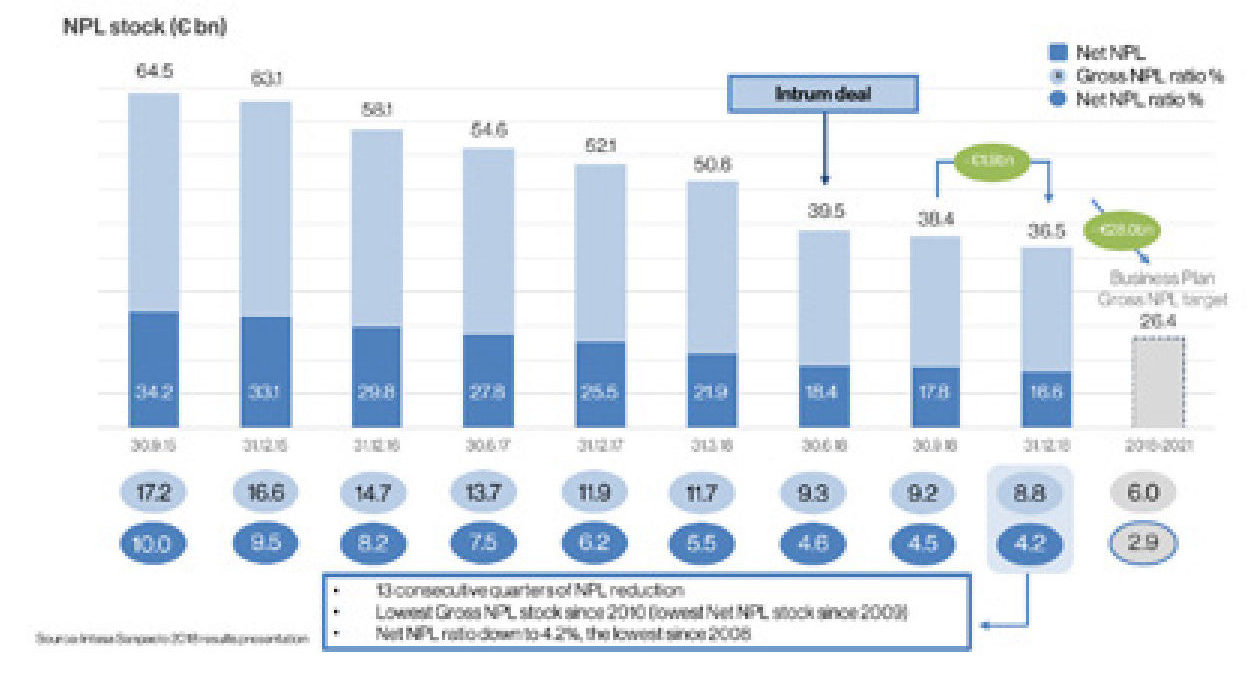

2/ Non-performing loan risk exaggerated.

The market has also in our view exaggerated the risks associated with non-performing loans (NPLs) in the balance sheet. Whilst the net NPL ratio as a proportion of the existing loan book is still optically higher than it would ideally be (4.2% of assets), the exposure has fallen steadily over a good number of years, and new NPL creation is now running at the lowest level ever.

Investors, furthermore, have in our view not understood the complexities of the Italian legal system where it can take anything up to ten years for a bank to take control of collateral in the event of a defaulting loan. This makes for a startling contrast with, say, with the UK, where a bank can normally seize a defaulter’s assets within months. The collateral is there. It just takes a long time for it to arrive. In the meantime the accounts can look (unrealistically) poor.

3/ Italian sovereign risk too high.

Lastly, we believe that the market has exaggerated the risks that the bank suffers for being Italian. Directly the bank owns €30bn of Italian government bonds, equivalent to 27% of tier 1 equity. Even a 20% default in Italian bonds would wipe out a manageable 14% of tier 1 equity. Run the numbers backwards, and you will find that the current share price implies an 11-12% plus cost of equity, a figure which is wholly fanciful. Or, as we see it, wrong.

You might be surprised to see that Italy has a similar country risk premium to Hungary, Morocco, South Africa and Russia. India is, indeed, viewed as being lower risk than Italy.

Source: Country default spreads and risk premiums, January 2019, NYU Stern School of Business.

Source: Country default spreads and risk premiums, January 2019, NYU Stern School of Business.

What could justify such levels? Perhaps only fear of Italy crashing out of the European Union. We think this unlikely as long as support for such a break is at modest levels:

Source: Kantar, in-out Europe poll, April 2019.

Source: Kantar, in-out Europe poll, April 2019.

And finally, we think that investors underappreciate the wealth of the private sphere: Italians are seen as being in distress. Not so. According to Allianz, where mighty Germany has just over €52,000 of net financial assets per capita, and the Celtic Tiger Ireland €47,000, Italy notches up assets per capita of nearly €59,000. The distress is perhaps not acute….

But what about valuation?

Our calculation produces some startling results, depending on which of a range of more or less probable scenarios.

1. If we assume that the restructuring programme fails (we don’t of course assume this, by the way), that the RoE stays at 9.6% and that profits grow at 4.5% per annum, we come out with a share price of €2.60, or 37% higher than where the stock trades today.

2. If we then assume that the restructuring programme is successful, and that the group generates a somewhat higher sustainable RoE of 12%, then the share price should be €3.95, more than double where the shares trade today.

3. And finally if we were to reduce the Italian country risk and the cost of equity by 2%to 11% we get a share price target of €4.97, 2.6 times higher than today.

So you may well not have got your starter for ten. But markets are not like quiz games.

It isn’t Jeremy Paxman who holds the answers (or Bamber Gascoigne, if you can remember that far back). Future reality is rarely accurately reflected in current share prices. And it won’t be revealed before the jaunty closing theme music strikes up. It may take time and patience as well as insight.

That is the opportunity for stock pickers like us. The Challenge, so to speak…

________________

[1] Blue: BNP on valuation C / Green: Deutsche Bank (A) / Red: RBS (B) / Grey: Swedbank (D).

download printable version

Disclaimer: This thought piece is a confidential communication issued by S. W. Mitchell Capital LLP and is for information only. It was prepared by S. W. Mitchell Capital LLP only for, and is directed only at persons that qualify as Professional Clients or Eligible Counterparties under the FCA rules, including appropriate institutional investors and intermediaries. It is not intended for the use of and should not be relied on by any person who would qualify as a Retail Client. No person receiving a copy of this newsletter may copy it for transmission to another person. This document has been prepared from sources which are believed to be accurate, however in producing it S. W. Mitchell Capital LLP may have relied on information obtained from third parties and accepts no liability for the accuracy or completeness of such information. It is the responsibility of every person reading this document to satisfy himself as to the full observance of the laws of any relevant country, including obtaining any government or other consent which may be required or observing any other formality which needs to be observed in that country. Past performance should not be seen as an indication of future performance and will not necessarily be repeated. The value of investments and the income from them may fall as well as rise and is not guaranteed. The investor may not get back the original amount invested. Changes in rates or exchange may cause the value of investments to fluctuate. S. W. Mitchell Capital LLP is a Limited Liability Partnership registered in England No. OC312953. Registered address 38 Jermyn Street, London SW1Y 6DN. Regulated and authorised in the UK by the Financial Conduct Authority. The material provided herein has been provided by S. W. Mitchell Capital LLP and is for informational purposes only. S.W. Mitchell Capital LLP serves as investment sub-adviser to one or more mutual funds distributed through Northern Lights Distributors, LLC member FINRA/SIPC. Northern Lights Distributors, LLC and S.W. Mitchell Capital LLP are not affiliated entities.