This article is authored by MOI Global instructor John Barr, Portfolio Manager at Needham Funds, based in New York.

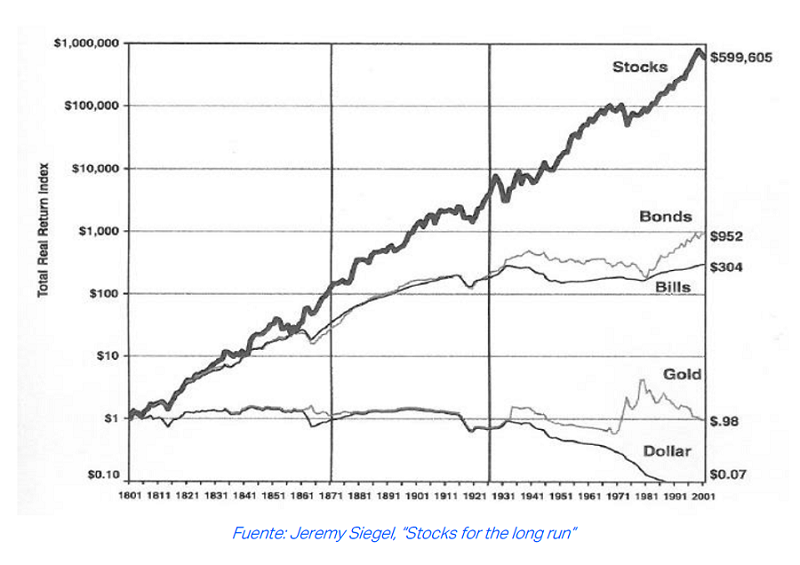

The Needham Funds’ mission is to create wealth for long-term investors. I believe that the market inefficiently values the prospects of some companies beyond a 1-2 year time frame. There is opportunity to generate alpha over a multi-year period by investing in small-cap equities that are going through investment periods. A new product or distribution strategy may have a significant impact on a small company and it may require patience for the desired results to show in a company’s financials. I look for companies that have continuing investment opportunities and may create wealth over the long-term.

The financial results of a small-cap company may not follow the orderly pattern that Wall Street prefers. Consequently, stock prices of these companies may suffer during periods of investment. Sometimes small-cap companies, like PDF Solutions, Inc. (PDFS) described below, can take several years to create value. In the end, if a company creates a product or service that major customers care about, it may also create value for shareholders. I believe that finding companies making promising investments and holding them in the portfolio as long as they continue to have investment and growth opportunities is a path to long-term wealth creation.

Needham Funds’ portfolios offer the opportunity to be a financial partner with great entrepreneurs. Our investments represent partial ownership of businesses that provide value to customers, invest in new products, employ people, and may generate cash for their shareholders.

Investment Criteria

I look to make investments in companies with great management teams, which to me generally includes founders, family, or long-tenured managers. I also look for high return on capital, or the potential for a high return, and the opportunity for the company to grow 5-10 times larger.

I look for companies available at an attractive valuation that may be in an investment stage, operating near break-even, and below potential operating margin. The company’s investments may be in operating expenses or capital equipment to open a new office, expand capacity or bring a new product to market. The level of investment can be measured by looking at a company’s potential operating margin and its current level, or by comparing capex spending with the historical level of depreciation and amortization. Patience is required for companies still in investment mode that have yet to show financial results.

When I purchase a new investment, I believe that financial results could come as soon as 6-12 months. However, investment periods may last longer than expected while the companies are making progress behind the scenes.

PDF Solutions, Inc.

The company supplies Software-as-a-Service and other products and services to help improve manufacturing yield for semiconductor manufacturing companies. New semiconductor manufacturing processes enable lower power semiconductors, which make for longer battery life on devices such as iPhones. As of December 14, 2018, PDFS has a stock price near $9 per share , a market cap of near $300 million, about $100 million of cash and annual revenue of near $100 million. It went public in 2001.

The Upside Opportunity

PDF has been investing in its Design For Inspection (DFI) and Exensio Big Data Analytics offerings for the last five years. Exensio has grown to an annual run-rate of about $40 million of revenue and is growing at about 30% per year. Exensio is used by approximately 200 design, manufacturing and test companies throughout the semiconductor ecosystem. It brings PDF a diversified customer base. Design For Inspection has been in use at an initial customer, which I believe to be a leading edge semiconductor manufacturing company.

These two offerings have the potential to substantially increase the size of the company. At $200 million of revenue, PDF could earn $1.50 to $2.00 per share after tax, which could result in a $20 to $30 stock price. Of course, there is risk in these newer products and revenue, earnings and stock price appreciation may not happen.

The Downside Risk

Cash, Gain Share and Exensio could be worth $8-10 per share and provide downside protection for investors.

PDF has cash of $3 per share. Additionally, the company has $50-60 million of “Gain Share yield ramp royalties” expected over the next few years, which could be worth another $1.50 to $1.80 per share. As a SaaS business with recurring revenues, Exensio could be valued at 3-5x revenues or about $3.50 to $6 per share. These elements total $8-10 per share. The next step in the commercialization of Design For Inspection has taken over a year longer than expected. Should PDF’s lead customer not come to terms on a next order, this part of the business might not have much value in the short-term.

Additionally there is an activist investor involved with PDF. VIEX Capital Advisors recently disclosed a 6% stake in PDF. Should PDF fail to execute on its business plan, we believe VIEX might push for sale of the company or structural changes to realize value.

When Might the Value in PDF Be Recognized?

I believe that PDF could announce a Design For Inspection order in the next quarter or two. Such an announcement might be a short-term catalyst for the stock. However, the longer-term question and the path to a $20-30 stock price might then become, “How large is the market for DFI?”

PDF Solutions’ Design-for Inspection offering

Design-for-Inspection (DFI) is sold to semiconductor design and manufacturing companies to determine whether leading edge semiconductors can be manufactured and operated at a new level of reliability. As semiconductors become the brains of autonomous vehicles, chip failures become unacceptable. During its July 27, 2018 conference call, PDF mentioned that John Chen of NVIDIA Corporation (NVDA) was the keynote speaker at PDF’s User Meeting. This is the first confirmation that NVIDIA, a leader in autonomous vehicle processors, computer graphics and artificial intelligence, is interested in DFI.

Today, semiconductor manufacturing companies use light-based inspection systems to find problem areas on semiconductors. Today’s most advanced semiconductors have feature sizes that are about 20 atoms, and these features are very difficult to see with light. DFI software inserts billions of tiny test instruments on a semiconductor wafer. The wafer can then be analyzed electrically by a PDF-designed electron-beam microscope, called an eProbe. DFI may perform 10 billion electrical measurements on a single wafer, which produces a great deal of data. PDF’s Exensio Big Data Analytics software is then used for analysis. DFI allows a manufacturing engineer to inspect a wafer to “detect the undetectable.”

PDF does not sell the eProbe as a machine. Rather, PDF’s business model is to provide the eProbe, the Exensio platform and Software -as-a-Service, which might result in recurring revenue for PDF.

In May 2016, PDF announced that it had received orders for several DFI systems. These orders were received earlier than expected and led the market to anticipate commercial progress in 2017 and 2018. However, the progress in 2017 and 2018 was behind the scenes. PDF made progress with some advanced technical capabilities, including the Gen-2 eProbe 250 DFI tool, which could allow DFI to be used on a production line, rather than in a development or test lab. TheGen-2 eProbe 250 provides an order of magnitude faster performance than the Gen-1 eProbe 150. The eProbe 150 was designed to be used in research applications, but the first customers found it so valuable that they placed those orders in May 2016.

Can PDF be a much larger company?

DFI’s available market can be estimated by looking at the optical and e-beam inspection markets which total $1.4 billion and some portion of the process control market which is $5 billion. With less than $100 million of revenue, success with DFI has potential to be a significant contributor to PDF.

Profitability and Return on Capital

In 2017, PDF reported a GAAP loss of $1.3 million on revenue of $102 million. PDF has been hurt by its reliance on its Integrated Yield Ramp services and the related GainShare royalties. This revenue stream has been in decline since 2016. In 2014, Global Foundries, Samsung and IBM were 79% of revenue. In 2018, Global Foundries should be the only 10% customer and I don’t expect additional IYR contract revenue from Global Foundries in 2019, although some could happen. From 2012 to 2015, PDF had cumulative operating margins of 25%. I believe this margin is possible in the future.

Management – Founders Motivated to Create Long-Term Value

PDF Solutions was founded in 1991. Dr. John Kibarian, CEO and Co-founder, has served as CEO since 2000 and a Director since 1992. Dr. Kimon Michaels, Vice President and Co-Founder has served as a Director since 1995. I believe they are out to solve significant problems for their customers and to build a business for the long-term. Dr. Kibarian owns approximately 8% and Dr. Michaels 5% of the company.

I got to know the company when it was private and I was a sell-side analyst at Robertson Stephens. Co-founders John Kibarian, CEO, and Kimon Michaels, VP Products, already had a decade of researching and commercializing technology to analyze semiconductor designs for manufacturability. Robertson Stephens led PDF Solutions’ IPO in July 2001 and I was one of the analysts to follow the company.

Dr. Kibarian’s view of stock options and bonuses shows a manager looking to build a business, not maximize his short-term compensation. “In part due to his request, which is based on a desire to conserve cash for other purposes, including funding the business and compensating other employees, Dr. Kibarian did not receive an increase to his base salary or annual bonus for many years … As a significant stockholder, Dr. Kibarian’s interests are already strongly aligned with the interests of our other stockholders.” (May 29, 2018 Proxy)

Members, log in below to access the restricted content.

Not a member?

Thank you for your interest. Please note that MOI Global is closed to new members at this time. If you would like to join the waiting list, complete the following form: