We make mistakes. We all do and experience failure. But why is it so important to embrace those failures?

Some great piece of actionable advice by Arnold Van Den Berg in less than 5 mns. Watch the interview. Loved it. https://t.co/fbDlIGVRQ6 Many thanks to @manualofideas pic.twitter.com/8C7ejPp1HE

— Value Investor Journal (@VJ_Rabindranath) April 16, 2018

This article by John Lewis is excerpted from a letter of Osmium Partners.

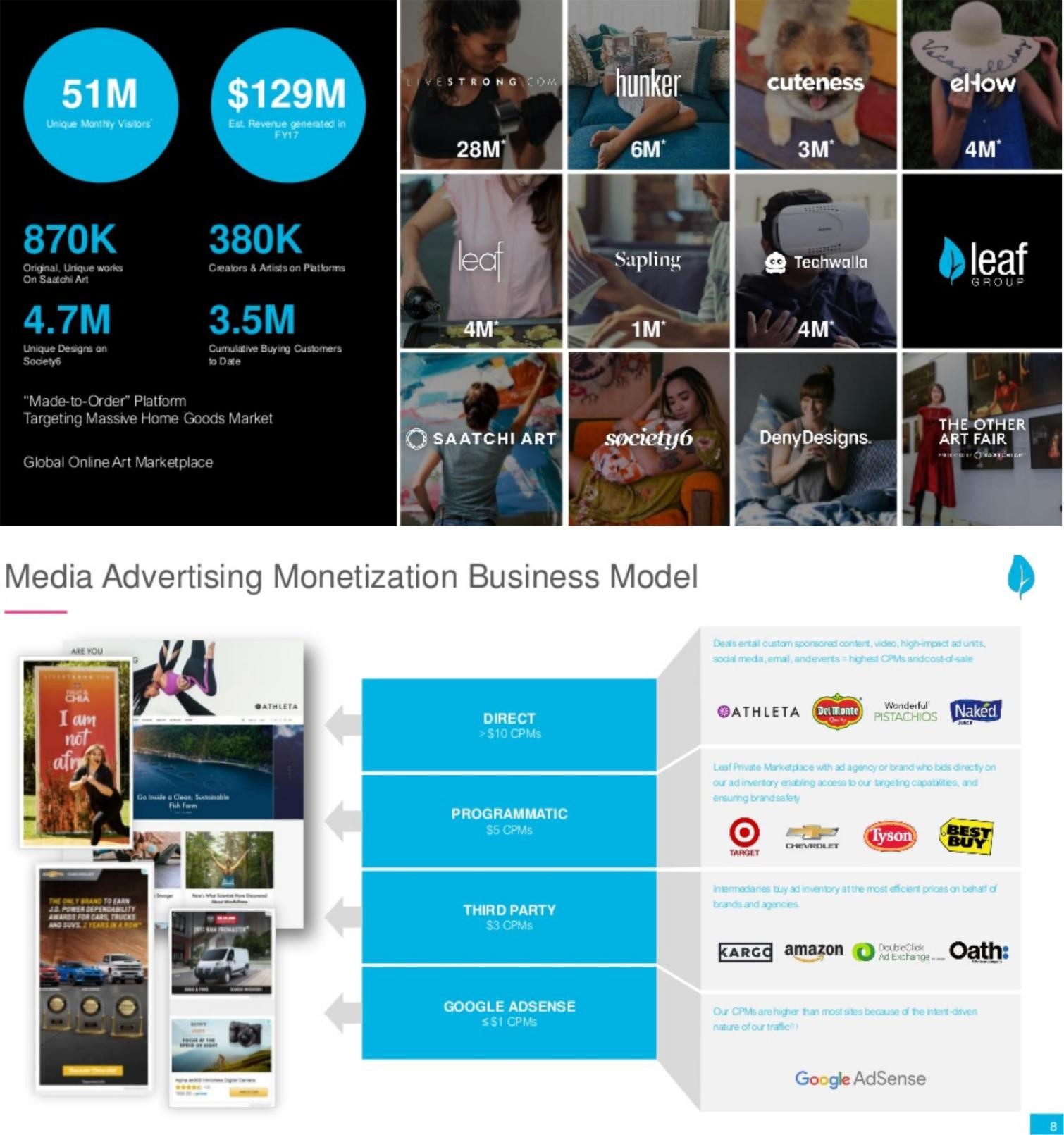

Leaf Group Ltd. (LFGR; $7.00)1, is an online digital media company composed of two service offerings: Content & Media (C&M) and Marketplaces. C&M publishes and distributes content, accumulating a library of articles, videos, and blogs across their properties such as eHow.com and Livestrong.com. They also operate two leading artist marketplaces, Society6 and Saatchi Art, which provides the global community of artist with an online commerce platform. Leaf Group’s current market capitalization is approximately $165 million. (LFGR is a holding across all funds.)

Net cash per share is $2.30

Leaf Marketplaces: Society6 we think is worth $4-5 a share, Deny Designs is probably worth $.50 a share and Saatchi Art we think is worth $1-$1.50 per share (Saatchi has 600,000 works or art on the platform worth $2.5 billion and takes 35% of sales as a commission)

We conservatively value Media at $5-6.50 a share, or approximately 6.6-8.2x 2017 segment operating contribution margin

NOL’s $10 per share

Guidance to be profitable by end of 2018 on steady state basis

Marketplaces grew 24% in 4Q17 and organically mid-teens

LFGR Sell Side analyst forecasts revenue should approach $145 million in 2018 (organic growth 14% top line growth) and has a $12 price target which is about 70% over the current share price.

LFGR Media business generated $18.2 million or .75 a share in segment contribution margin for 2017 (media segment contribution was up 75% over 2016).

Our most conservative DCF model get us to $8.00 a share, while the only Sell Side analyst who covers LFGR rates the company a Buy and has $12 target, and our Sum of the Parts we get $13-15.80 (we have taken our Media valuation down slightly given industry dynamics). We think LFGR current valuation multiples will expand as the company gains further revenue scale as the business has significant incremental EBITDA margins.

Below is a thumbnail of LiveStrong, which has 28 million unique monthly users.

Below is one of Leaf Group’s Marketplace companies, Saatchi Art, the company takes 35% of transaction revenue:

Leaf should approach close to $150 million in revenue between Media and their e-commerce Marketplaces business segments and the business is valued at $110 million net of cash:

Source: Leaf Group Latest Investor Presentation.

There are tremendous benefits to scale in online media. The big catalyst is to move up the ad stack in terms of monetization. There is a 10x difference in monetization for the same ad depending if you use Google Adsense $1 (this is why Google is a $500 billion company) to direct, $10 in revenue per thousand impressions.

KKR acquired WebMD for $2.8 billion in July 2018 and Everyday (EVDY) was acquired for $440 million in the online healthy living industry. In Leaf’s Media segment, we think LiveStrong is a gem acquisition target as it is a top property in traffic with 28 million monthly visitors. We think conservatively, Media is worth $120-150 million with $50 million in net cash on 24 million shares or $7-8 per share and Marketplaces should be worth an additional $8 per share based on 2x sales with $85 million in marketplaces revenue (+24% growth with mid-teens organic growth rates). Public peer group for comparable businesses trade between 2-6x sales.

______

1Market price as of the date of dissemination of the letter.

Certain factual and statistical (both historical and projected) industry and market data and other information contained herein was obtained by Osmium Partners from independent, third-party sources that it deems to be reliable. However, Osmium Partners has not independently verified any of such data or other information, or the reasonableness of the assumptions upon which such data and other information was based, and there can be no assurance as to the accuracy of such data and other information. Further, many of the statements and assertions contained herein reflect the belief of Osmium Partners, which belief may be based in whole or in part on such data and other information. The analyses provided may include certain statements, assumptions, estimates and projections prepared with respect to, among other things, the historical and anticipated operating performance of the companies. Such statements, assumptions, estimates, and projections reflect various assumptions by Osmium Partners concerning anticipated results that are inherently subject to significant economic, competitive, and other uncertainties and contingencies and have included solely for illustrative purposes. No representations, express or implied, are made as to the accuracy or completeness of such statements, assumptions, estimates or projections or with respect to any materials herein. Actual results may vary materially from the estimates and projected results contained herein. Past Osmium performance is not indicative of future results. Osmium Partners disclaims any obligation to update this letter. A portion of the Partnership’s assets may from time to time be invested in securities that have limited liquidity. The Partnership’s investment strategy is to make concentrated investments in what it views as its best ideas. The Offering Memorandum and Limited Partnership Agreement offers a comprehensive overview of the risk factors involved in investing with Osmium Partners. The information contained herein is provided for informational purposes only. This is not an offer to sell, or a solicitation to buy, limited partnership interests in Osmium. An investment in Osmium is not suitable for all investors. Stocks mentioned in the newsletter do not constitute a recommendation to buy or sell the individual securities.

NOTA DEL EDITOR: Estas idea de inversión son obtenidas de una carta a los inversores de Valentum FI.

* * *

Flow Traders: Es un creador de mercado en ETFs (el que da contrapartida cuando alguien compra o vende un ETF), con más cuota de mercado en Europa. FLOW lleva en cartera desde hace casi un año, tiempo durante el que hemos estudiado el negocio y balance de la compañía, hemos viajado a Holanda y nos hemos reunido en dos ocasiones con los directivos. Hemos construido poco a poco la posición en un entorno de volúmenes y volatilidad flojos donde los beneficios han ido mermando. Aún así, dada su estructura de costes, tecnología potente y fuerte capitalización, pensábamos que era un gran valor a tener en cartera, y cuanto más lo estudiábamos, más nos gustaba. Sus resultados fluctúan, pero vemos complicado que pierda dinero. Además, su modelo de negocio nos debería proteger en momentos de volatilidad (ya que es cuando más suben los volúmenes y cuando FLOW más dinero gana). En febrero se han juntado dos noticias positivas: primero, que el regulador holandés anunció que considera que está lo suficientemente bien capitalizado (tras la petición de la European Banking Authority de que aclarase las normas de capitalización para creadores de mercado) y segundo, el incremento de la volatilidad. Tal ha sido el aumento del volumen que en los resultados del 4T17 anunciaron que hasta la primera semana de febrero habían tenido más ingresos que en su mejor mes de la historia (3T’15 donde hicieron €0,8 de BPA). El VIX de volatilidad del Eurostoxx 50 durante el mes de febrero no ha bajado de 17 marcando máximos de 34 (frente a niveles de 10-12 en los meses anterior) y pensamos que si sigue a estos niveles pueden hacer un 1T’18 superior a €1,5/acc. Ahora mismo cotiza en torno a €33/acc. Posiblemente por debajo de 10x PER’18. Otro de los puntos importantes es que pensamos que muchos gestores utilizarán en el futuro FlowTraders como compañía para cubrir el incremento de la volatilidad (sin que el paso del tiempo les penalice como en el caso de las opciones) lo que puede hacer que tenga un re- rating importante.

Bogumil Baranowski on Outsmarting the Crowd

April 15, 2018 in Podcast, The Zurich Project, The Zurich Project Podcast, TranscriptsIn an episode of The Zurich Project Podcast, presented by MOI Global, John Mihaljevic speaks with Bogumil Baranowski about his highly recommended book, Outsmarting the Crowd.

Bogumil Baranowski has a Master’s degree in Finance and Strategy from Institut d’Etudes Politiques de Paris (Sciences Po), and a Master’s in Finance and Banking from Warsaw School of Economics. He has over 12 years of investment experience. Before joining Sicart Associates, LLC, he worked at Tocqueville Asset Management L.P. as a portfolio manager and senior equity analyst. With a European background, his special focus is on consumer sectors, and the broadly defined New Economy. He is the author of Outsmarting the Crowd – A Value Investor’s Guide to Starting, Building and Keeping a Family Fortune (2015). His articles are frequently published on Seeking Alpha. He is an active member of Toastmasters International.

Bogumil is a participant in The Zurich Project.

The Zurich Project Podcast is on iTunes, Soundcloud, and Stitcher.

An edited transcript of the conversation is available to members of MOI Global.

Members, log in below to access the restricted content.

Not a member?

Thank you for your interest. Please note that MOI Global is closed to new members at this time. If you would like to join the waiting list, complete the following form:

In my experience, at least, overconfidence is followed mercifully often by shame and humiliation. Those are fairly effective cures. https://t.co/5RB5jlvXqY

— Jason Zweig (@jasonzweigwsj) April 14, 2018

MITIMCo’s Advice to Aspiring Superinvestors

April 14, 2018 in Building a Great Investment Firm, Featured, The Manual of IdeasWe interviewed the investment team of the MIT Investment Management Company, based in Cambridge, Massachusetts for The Manual of Ideas, the flagship publication of MOI Global, in 2014.

We had the privilege of getting a glimpse into the decision-making process at one of the world’s finest allocators of capital, the MITIMCo. In this exclusive Q&A, President Seth Alexander and global investment team members Joel Cohen and Nate Chesley share their process for identifying and partnering with exceptional investment managers. The team also provides invaluable lessons to emerging managers who aspire to become the superinvestors of tomorrow.

In their mission to deliver outstanding long-term investment returns for MIT, Seth, Joel, Nate and the rest of the MITIMCo team seek to cultivate an ecosystem of enduring partnerships with no investment manager being “too small, too young, or too ‘non-institutional’.”

The MITIMCo team’s perspective and advice are timeless and truly invaluable for emerging managers looking to build a great investment firm. Enjoy!

MOI Global: How did you get interested in investing?

“My early professional experience at an investment consultancy was influential in my desire to invest for the benefit of an extraordinary institution like MIT, where the capital we manage is reinvested in world class scholarship, research, and global problem-solving” —Nate Chesley

Nate Chesley: I didn’t grow up with a lot of exposure to the stock market but was always inclined to view the world through an economic lens. I studied finance and economics in college where I came to appreciate the role of the capital markets as a sort of circulatory system for the global economy. My early professional experience at an investment consultancy was influential in my desire to invest for the benefit of an extraordinary institution like MIT, where the capital we manage is reinvested in world-class scholarship, research, and global problem-solving.

Seth Alexander: I took a course on endowment management taught by David Swensen and later went to work for him. He is both a wonderful investor and a wonderful teacher so it was a very fortunate experience. I think I was initially drawn in by the quality of the people at the Yale office and later by the breadth of the business.

Joel Cohen: Similarly, my interest in MITIMCo came first and my passion for investing came after I started working here. In my job search during my senior year of college, no one else came close to what MITIMCo could offer in combining interesting and challenging work, a real commitment to investing in every member of its staff no matter how young, and an incredible mission.

Within a few months after I joined MIT as a 22 year old, I realized that investing was actually an even better fit for my interests and personality than I thought. I’ve always been intellectually curious and enjoyed reading widely – I was a philosophy major in college in addition to econ, after all. So when we read Hagstrom’s Investing: The Last Liberal Art, it clicked for me why I found it fascinating: investing is an ongoing quest to integrate mental models from a variety of disciplines into a framework for understanding the world and making decisions. I feel very lucky to have joined an organization that thinks about investing that way.

MOI: Which people and/or experiences have shaped your investment thinking?

Seth Alexander: It is honestly a little hard to pinpoint the exact source of what has influenced our thinking most. We gather thoughts and ideas from lots of different places and try to amalgamate them into what makes sense for us. Probably our best source of investment thinking comes from conversations with managers in our portfolio. There are lots of challenges they face – how to build an organization, how to size positions, how to structure a typical day, when to hold cash, and so on – that are analogous to challenges we face and so we have been influenced a lot through those discussions.

For example, we restructured the organization a few years ago to make everyone generalists based on what had worked well with some of our managers. We also read a great deal. We have an internal book club that covers science and history and other subjects to help us generate ideas from outside the investment world. We are very happy to borrow ideas so we do that liberally and work to fit them into our frameworks.

MOI: How have you gone about building the organization and team?

Seth Alexander: We have tried to find the best athletes with a passion for investing, not necessarily the most experienced investors. We also look for people who get excited about the ways MIT contributes to cancer research and alternative energy research and other efforts. We started early on with a vague organizational chart and eventually eliminated it altogether to make it clear we wanted people with all levels of experience to come in and contribute as investors and partners.

We do not try and hire someone every year or anything like that. Instead, we hire opportunistically. If two great people came along in the same week who would both be a great fit, we would hire them. We are always looking to hear from passionate investors about working here and really encourage people to reach out to us.

MOI: What is similar/different in the skillset required to successfully invest in securities versus investing in managers?

“Our approach to underwriting investment managers is quite similar to the way a stock-picker might analyze a company’s management…” —Nate Chesley

Nate Chesley: We avoid drawing too bright a line between our approach and direct investing because there are more similarities than differences. We have a culture and mindset of thinking like owners and focusing on the micro that is motivated by Graham’s sentiment that “investing is most intelligent when it is most businesslike.” That leads us to focus a lot of our time understanding how our capital is invested bottom-up in the specific companies, properties, and other securities we own through our managers.

One similarity between the two skillsets is the emphasis on evaluating people. Our approach to underwriting investment managers is quite similar to the way a stock-picker might analyze a company’s management: an intense focus on integrity, a track record of outstanding judgment, and a clear alignment of interests. Also, for every investment decision we make we evaluate the margin of safety, the range of potential outcomes, and the associated probabilities – just as one would do when investing directly in a security.

One difference might be our generalist approach. Each member of our investment team has the flexibility to cover the entire waterfront, whereas many investors are intensely focused on a very specific niche, such as biotechnology stocks or early stage consumer technology companies – or at least one particular asset class or geography.

The Process of Identifying and Partnering with an Investment Manager

MOI: You have stated that you “aim to establish investment management relationships that last decades.” What are the key implications of such a mindset on how you go about doing business and what managers you look for?

Joel Cohen: MIT, which hopefully will continue to be a leader in education and research hundreds of years from now, is one of few market participants for whom even decades are a comparatively short time period. We think this creates an enduring competitive advantage in a market where three years passes for long term. Thinking about partnering with managers for decades naturally leads us to ask a lot of questions to understand the trajectory they are on and what they are trying to accomplish. For example – how do you define success? How are you building an organization around that goal? Which investors do you hope to emulate? What are you doing to become an even better investor 10 years from now than you are today?

Another implication of this multi-decade mindset is we have a willingness to engage with managers earlier in their careers. These managers can have decades of compounding ahead of them. Will the 25 year old manager we just hired still be compounding our capital half a century from now? We are excited that it is even a possibility!

MOI: How do you categorize investment managers?

“The more we thought about it, the more we realized that perhaps exceptional investors by definition could not be easily classified.” —Seth Alexander

Seth Alexander: The biggest way we categorize managers is whether or not they fit into our comfort zone. For example, in looking at public markets investors we have defined our comfort zone as long-term oriented, fundamentals-based, value investors that pursue strategies we can understand and underwrite. This narrows the field quite a bit, as macro, quant, momentum/trading, and benchmark-driven strategies tend to fall out.

Beyond that, we actually try pretty hard not to categorize managers. We tried for a while but every time we came up with a classification scheme, we would come across an interesting manager that did not fit. The more we thought about it, the more we realized that perhaps exceptional investors by definition could not be easily classified. Once we got comfortable without having classifications and just focused on finding great investors, we were much happier.

MOI: What is your process for evaluating managers to find the ideal manager? Does that process differ depending on the type of manager, and if so, how?

Nate Chesley: Our process deemphasizes asset class distinctions in favor of a manager-centric approach, so our process is generally consistent across all types of strategies. However, we have accumulated a variety of mental models for different strategies that provides a framework through which we hone-in on the key risks and areas of potential exceptionality across investment strategies. This manifests in a sort of internal lexicon that allows the team to evaluate a wide range of opportunities with the same process, but more nuanced understanding. For example, we’ve developed an appreciation for equity strategies that are unusually long-term in nature. It occurs to us that there are huge inefficiencies when you to try understand what a business could look like five or ten years from now. This is not easy, but we’ve studied investors who have pursued this approach and have developed our own understanding of the attributes a manager might have to succeed with this style of investing. Jeff Bezos talks about this, saying that on a three-year time horizon, you’re competing against a whole lot of people. But if you’re willing to really lengthen your time frame, there is a fraction of the competition because so few people are willing to do that.

We focus on evaluating opportunities that are within our circle of competence, which is bounded by our core investment principles. The nature of our research really boils down to: developing conviction in the quality of an investor’s judgment; understanding the risks to which our capital is exposed; and ensuring that the right structure and alignments exist to serve as the foundation for a long-term partnership. On a practical level, we spend our time conducting in-person meetings; reading any relevant materials, such as letters, investment case studies, or company materials; conducting reference calls; and analyzing historical data.

MOI: You have stated on your website that “since exceptional judgment is crucial to virtually all investment strategies, a critical element of our due diligence process is to evaluate historical decision points.” What are some examples of such decision points and how do you go about evaluating them?

Joel Cohen: I’ll give an example from a manager we recently underwrote. In the mid-2000s, he stumbled across a small, sleepy community bank that had earned high ROAs and ROEs for decades. He thought to himself, how on earth do they do that? As he explored further, he discovered that there were quite a few others as well, and eventually it became clear that these were gems of businesses if they had certain characteristics. Of course, banks at the time were very overvalued because it was a boom time for the financial industry. Nonetheless, he knew the industry was prone to the occasional crisis so he did his work and identified a handful he would love to own – at one-third the valuation, of course. Four years later the financial crisis hit, and these great banks were babies thrown out with the bathwater, so he got the chance to participate in their high rates of internal compounding at discounts to book.

Now, what does this tell us about the manager’s judgment? First, he correctly identified these banks as quality assets. Second, he had the discipline and patience to wait four years before touching them. Third, he had the stomach to buy them in the midst of a financial and economic panic. These things are all as unusual as they are impressive.

MOI: How do you define a manager’s investment record and how important is it in your overall due diligence? What do you look for in a track record?

“Over time, we have learned that great investors tend to be more focused on process than on outcomes.” —Joel Cohen

Joel Cohen: Over time, we have learned that great investors tend to be more focused on process than on outcomes. So, we try to follow this principle as well. The idea goes that if the process is correct, results will take care of themselves over the long term. Of course, a track record, if presented over a long period of time, is an important check on whether what should work is working. But we have to be cautious about this, as even great managers have multi-year periods of meaningful underperformance – there is a great Eugene Shahan article from 1985 about how plenty of investors with great long-term track records looked mediocre in any given year and underperformed for three or more years in a row in many cases. If our own investment process works well we should be able to identify great investors even when their backward looking track records temporarily look mediocre – and I think developing conviction in their processes is the way to do that. A number of years ago, we hired a health care focused manager who had earned essentially market-like returns over the prior seven years, but we understood the reasons for their performance and had enormous conviction in their process and judgment. Subsequent returns have more than justified our decision.

MOI: How do you make decisions throughout the stages of the process? What are some instances that make decision-making especially difficult/easy?

Seth Alexander: For every new investment opportunity, we form underwriting teams of two to four people. They work together to establish a due diligence plan with appropriate checkpoints to keep the rest of the team informed. If we want to proceed forward on something, we put our thoughts on paper into an investment memo that describes the investment manager, our reason for investing, our concerns, our sizing calculus, our due diligence, and anything else that might be relevant. This is important because we want to have a very transparent process that provides plenty of opportunities for the rest of the team to give feedback, ask questions, and debate points of disagreement. Ultimately though, it is the underwriting team alone that makes the final decision to make sure we avoid group-think. I meet every manager, usually near the end of process, and technically can veto the underwriting team’s selections but that does not happen very often. The underwriting teams have imposed a pretty rigorous process on themselves to ensure that the things that make it through our process are compelling.

Honestly, we do not seem to have a lot of easy decisions. That may be because there are shades of grey in every decision for us to argue about. Even if we don’t argue about the soundness of the decision itself, we can still argue about the sizing of the decision or what red flags to watch out for or the appropriateness of the fee structure. The other thing that adds complexity is that we tend to focus on managers earlier in their careers so there is less evidence to examine and we are always going to have to make a judgment call on the future potential of the people involved. For example, of the last twelve managers we’ve hired, eight founded their firm in the last two years.

MOI: What are the attributes of exceptional managers/firms?

“If you define an exceptional firm as one which achieves outstanding returns over a very long period of time, one trait they all seem to have is that they view investing less as a job and more as a vocation or a form of self-expression.” —Joel Cohen

Joel Cohen: We try to be humble about thinking that we can crack the code of what makes a firm exceptional, even though we will spend our whole working lives trying to do it. We have developed our own, constantly evolving, always imperfect view of what constitutes an exceptional investor based on many years of working at it. If you define an exceptional firm as one which achieves outstanding returns over a very long period of time, one trait they all seem to have is that they view investing less as a job and more as a vocation or a form of self-expression. There are a lot of nice side effects that you often see from people who come to investing this way. First, they tend not to take a cookie cutter approach to investing or try to cater to what they think allocators want, but instead spend more time tailoring their methods to their own personality and what works for them. For example, with the manager I mentioned earlier who studied small community banks, he realized that the intellectual engagement of identifying great assets regardless of price, adding them to his list of things to follow, and then waiting for a crisis felt natural to him, and leveraged the skills he has that are most uncommon. Second, if investing is someone’s passion, they are going to be thinking about it in the shower, on the subway to work, etc.. Most importantly, their efforts are going to be sustainable. Time spent working is not a sacrifice, but an indulgence. Those who pursue investing for intrinsic reasons seem to keep performing at a high level for long after those who were in it for the money.

MOI: Seth Klarman is quoted as saying, “Value investing is simple to understand, but difficult to implement. The hard part is discipline, patience, and judgment.” How do you define these elusive traits—discipline, patience, and judgment—and how do you recognize them in a manager?

“Once invested, our primary objectives are continued learning, relationship building, and trying to help our managers achieve their goals.” —JOEL COHEN

Joel Cohen: These traits are hard to define, and if you asked different people on the team I’m sure you’d get different answers. To me, discipline means a willingness to keep one’s standards incredibly high across an organization – in hiring people, making investments, and making business decisions. Patience is a willingness to forgo activity today in order to end up with better results over the long term. Judgment is the ability to conquer the behavioral side of investing, think clearly in terms of probabilities, identify the key variables, and weigh difficult tradeoffs.

Given the amount of time we spent with managers analyzing their historical decisions and talking about companies, there is generally a good body of qualitative evidence to make a reasonable judgment along these lines. One thing to look for is whether the manager has worked to create an environment, structure, and set of routines that enable them to be patient, disciplined, and to exercise good judgment. The great investors seem to design their whole operation with these things in mind – from the people that they partner with, to the way they spend their time, to the things they focus on in their letters, to the way they set the organization’s culture and habits.

MOI: You have talked about the need to “identify and underwrite the competitive advantages that allow sustained outperformance” of a manager. What are some examples of such advantages?

“Larry Pidgeon of CBM Partners is an example of an investor we really admire whose competitive advantage came from a long string of small advantages.” —NATE CHESLEY

Nate Chesley: Bill Miller’s categorization of competitive advantage is a sound framework. He offers three with which you are most likely familiar: informational, analytical, and behavioral. I might add to that list “structural”, which serves to reinforce an investor’s ability to leverage their behavioral advantage. For example, access to stable capital is a huge tailwind to an investor’s ability to be patient and disciplined. I’d also note that competitive advantage may be derived from the accumulation of many small advantages thoughtfully linked together and executed well. This is in contrast to what you might find with an exceptional company that operates with one big competitive advantage – for example, a cable operator that benefits from a regional monopoly resulting from the local ownership of privileged physical assets. Larry Pidgeon of CBM Partners is an example of an investor we really admire whose competitive advantage came from a long string of small advantages. Before starting his partnership Larry worked with Lou Simpson at GEICO. He was someone whose many years of experience had given him a deep reservoir of accumulated knowledge and wisdom about businesses, which complemented his even temperament, thoughtful and methodical nature, and instinct to behave in a highly principal-oriented way, as if all the capital in the fund were his own. None of these may seem so unusual in isolation, but together they create a powerful advantage.

MOI: Do you prefer generalists or specialists among your managers?

Seth Alexander: It really depends. We try to think carefully about where the competitive advantage might be. Sometimes the generalist has the competitive advantages and sometimes the specialist has the advantage. If I think about the biotechnology sector, I am pretty sure I want to work with a specialist because the industry is complicated enough that focused expertise and analysis can be of real benefit. For a distressed debt manager, on the other hand, we would typically favor the generalist because this opportunity set is created by distress and fear that could arise in any industry anywhere in the world and there would be a benefit to being able to allocate across a very wide universe.

MOI: How do you approach your manager relationships?

Joel Cohen: Once invested, our primary objectives are continued learning, relationship building, and trying to help our managers achieve their goals. On the first point, while we aim to do most of our work upfront, we tend to find that great investors evolve in interesting ways and so we continue to learn a lot – both from them and about them – after we invest. A lot of this is work we can do on our own – for example, by learning about companies they own, or by reading the books the manager recommends to us. In terms of relationship building, we are working to build the kind of trust and open dialogue that can help the partnership withstand difficult times. The emphasis on helping our managers achieve their goals in any way we can is another implication of our multi-decade partnership mentality, because we believe that working really hard to be great partners can expand our managers’ moats and make a difference to their long-term performance in a modest but meaningful way. This can be anything from using the MIT network to help a manager solve a problem to structuring our interactions differently in order to minimize disruptions to their productivity or thought process. Usually of course the best way we can add value is if we just get out of the way and let a manager do their thing, and we’re happy to do that too.

MOI: How do you decide when to part ways with a manager?

“We tend to find that great investors evolve in interesting ways and so we continue to learn a lot – both from them and about them – after we invest.” —Joel Cohen

Nate Chesley: This is a very difficult part of our process, but an important one if we are to fulfill our duty of producing truly exceptional returns for MIT over the long run. Our ideal outcome is to partner with a manager for decades, but this isn’t always the case. First, we make mistakes. We have to be brutally intellectually honest with ourselves in recognizing our mistakes and seeking to learn from them. We have an internal culture of transparency and open debate in which the entire team has exposure to all managers across the portfolio and can identify where we may have weaknesses so we can have an open debate about them and take action if need be. Firms also can evolve. Our ongoing relationship and monitoring efforts evaluate an investment’s evolution relative to the expectations we established during our initial underwriting. Competitive advantages can erode, key people can depart, small stresses can develop into considerable issues, and incentives can change. We are mindful of these shifts and must create sufficient pressure on ourselves such that we are always raising the bar of exceptionality within the portfolio. In a recent example we parted ways with a manager because AUM had more than tripled since we invested, and we felt their competitive advantage depended on being small and nimble.

Advice to Emerging Managers

MOI: What is the best preparation a manager can have before starting to manage other people’s money?

Seth Alexander: One perhaps obvious thing that we have noticed is that it is helpful for people to have a good mentor. Good mentors are thoughtful people who are motivated by a desire to help you grow and succeed, and generally don’t have a vested interest beyond that. This makes them likely to give honest feedback and invest time in helping you.

Some people start naturally with a mentor because that is how they were introduced to the business but others have to proactively search them out. From our vantage point it seems like the people who have spent the time to find a good mentor have found the effort involved to be very worthwhile. In some cases, we have been able to provide introductions of experienced investors to younger managers to help create a relationship.

MOI: What are some common mistakes you see emerging managers make?

Nate Chesley: The most common mistake we see is when an investor makes small compromises in the early days of the partnership in ways that limit future success. These seemingly small compromises at the outset compound over time into considerable stresses, which are prone to fracturing at the least opportune times. People compromise on the quality of their LP base, unwilling to turn away the wrong investor. Start-up managers sometimes have the misguided view that they need to be all things to all potential sources of capital and compromise by adjusting their strategies to investor demands. We also see investors give away economics in their business in seed deals in order to scale-up as quickly as possible. We’ve observed that almost all the very successful and established firms we work with turn away large amounts of capital – they even did so when they were small, by the way – because they understand the need to apply the same high bar to their choice of partners as they do their choice of investments.

MOI: What is the biggest misconception emerging managers have in terms of attracting institutional capital, including from MITIMCo?

“The most common mistake we see is when an investor makes small compromises in the early days of the partnership in ways that limit future success.” —Nate Chesley

Nate Chesley: One thing that many people remark on when they meet us the first time is that we are very different from their conception of what a traditional institutional investor would be. They are surprised to hear we spend a lot of time meeting with managers in their 20s and 30s, that we are frequently the first or only institutional investor in a firm, that a meaningful number of our firms are one- and two-person shops, and that we are very content with unconventional firms and strategies. We have made a deliberate effort to invest in un-institutional firms because many investors with exceptional long-term track records have been unconventional and un-institutional. So I think there is an interesting misconception here that all institutional capital thinks the same way.

MOI: What advice do you have in terms of structuring the fund?

Nate Chesley: First, there is no one-size-fits-all solution. There are many aspects of a partnership’s terms and conditions that should be thoughtfully tailored to the strategy’s objectives. The foundation starts with a long-term vision of success that is shared by both the manager and the investors. We think a lot about alignment of interests over the life of the partnership and want terms that serve that purpose. Ultimately, we’re really aiming to create structures where managers are rewarded for producing exceptional results for their partners. Our intent is not fee minimization – we want to create incentives for the manager to attract and retain talent and to do extraordinarily well if they produce outstanding returns.

A while ago we came across a group of stockpickers with one of the best structures we’ve seen in terms of aligning the whole operation around the compounding of capital. First, the management fee was budget based rather than a percentage of assets, which removes the strong incentive to grow AUM. Second, the performance fee was tied directly to long-term performance (in this case, 5 years) over a 6% hard hurdle, and a significant portion of the performance fee was held in a reserve against future poor performance. This removes the temptation for the either the manager or their LPs to focus on annual results. So, the structure was very well aligned, which served the manager just as well as it did their investors – it helped them attract a group of very high quality partners, generate one of the best records we have seen out there, and create significant personal wealth too.

MOI: Managers who are just starting out often take the view that as long as they take care of the investment side (i.e. achieve a good 3 or 5-year track record), the business side of the firm will take care of itself (i.e. allocators will come knocking). What’s your view?

Joel Cohen: Broadly, I think we subscribe to the view that if you have a compelling value proposition, it is hard to imagine you will not attract attention over time. I would not agree though with the idea that the business side does not deserve attention in the early years. First, it can take a lot of work to figure out how to set up a fund with a cost structure that doesn’t force you to go out and raise a lot of early capital from the wrong partners. Second, just because you are not spending time on marketing does not mean you should not be investing in building your business, for example by creating a roadmap for building your firm and in creating the materials you can use to communicate to prospective investors later on. Even something as simple as an “owners’ manual”—like Buffett did for Berkshire Hathaway—can help clarify your thinking for yourself and share your thinking with prospective partners when they arrive.

MOI: What are some resources you would recommend to emerging managers?

Joel Cohen: There are a lot of great books out there whose insights can be helpful to the up and coming investment manager. Charles Ellis has a paper called “The Characteristics of Successful Investment Firms” that is great food for thought. There is also the Eugene Shahan article we mentioned earlier that is worth sharing with all of your partners to make it clear that short-term underperformance is not inconsistent with meeting your long-term goals. Built to Last is an enjoyable read with plenty of insights for anyone building an organization—consider pairing it with The Halo Effect for another point of view.

“We would recommend that a new manager write down on a piece of paper what their definition of success is and… make sure that everything is aligned to reaching that goal.” —Seth Alexander

In terms of generally good reads, I’d recommend The Art of Learning by Josh Waitzkin, Different by Youngme Moon and some well written business histories like Built from Scratch, Made in America, and Nuts! I imagine most people have read Daniel Kahneman’s Thinking Fast and Slow but I mention it because it is so good and because it is a great book to be reading as you are designing decision making processes.

MOI: If there is one thing an emerging manager should ask himself or do after reading this interview what should that be?

Seth Alexander: We would recommend that a new manager write down on a piece of paper what their definition of success is and then systematically go through everything they can control—their business structure, who they let in their fund, how they spend their time, what fees they charge, and so on—and make sure that everything is aligned to reaching that goal.

Of course, the other thing that an emerging manager should do after reading this is give us a call! We are always looking for good investors to partner with. If something resonated in this interview, we can be reached at www.mitimco.org [or via MOI Global].

MOI: Thank you very much for your insights.

Albert Einstein reminded us some time ago to “strive not to be a success, but rather to be of value.” In the world of money management, there are many successful people managing large pools of capital. However, few of them are of value to their investors. Warren Buffett and Charlie Munger are exceptions to the rule, not only because they have delivered superior investment returns to Berkshire Hathaway shareholders, but also because they have been of value to all of us as teachers on investing and life.

Below, we are pleased to share selected words of wisdom and advice to aspiring investors excerpted from our conversations with some of the more experienced value investing practitioners in our community. We hope these words will be of value to aspiring investors and, in the process, contribute to our shared global value investing community.

Jean-Marie Eveillard, Senior Adviser, First Eagle Funds

“When our younger daughter was six or seven years old somebody asked her at school, what does your father do? And Pauline didn’t have the answer. So that evening when I came home she said she was embarrassed, so she said, hey what do you do? And I didn’t feel like particularly at the end of the day, I didn’t feel like explaining to a six-year old money management, so I said Pauline, I will tell you how I spend my time.

And I said to Pauline, half of my time is spent reading, because I had read or heard that Warren Buffett was a voracious reader, which he is. So I said to myself I don’t have his skills but if I read voraciously maybe it will help me too, which it did I believe. And the other half of my time I spend talking with my in-house analysts. And Pauline said, reading, talking, that’s not work. So I said sorry, Pauline but that’s just what I do.”

Chuck Akre, CEO, Akre Capital Management

“I’ll tell you a quick anecdote. There is a financial writer who used the nom de plume of Adam Smith years ago, his name is Goodman I think. And back in the 1980s, he interviewed Warren Buffett and he said, well, what advice can you give somebody who wants to be a good investor? Warren said, well, just learn about all the public companies. So he said, oh, you couldn’t possibly mean that? There must 7,000 public companies. Warren says, well, just do what I do, start with the As.

Most of us are not blessed with the kind of mind and capability that he has, and so I would just say, it’s been hugely important to me to be curious and passionate about it. And if you go back and read…of things that Warren Buffett suggested that one had to have to become a successful investor. And among them were things like control greed and so on.

Be curious and read everything you can get your hands on and try to identify the people who’ve been winners and then try to identify why they have been winners. What it is about what they’re doing that causes them to be successful? I mean that’s all I’ve ever done, and try to create a system that works for the way I’m wired and allows me to get along in the market. That’s all there is to it, be curious, interested and uninhibited.”

Brian Bares, Founder, Bares Capital Management

“Conceptually, from an investment process and philosophy standpoint, obviously the Berkshire Hathaway annual reports going back and even his partnership letters are a great source for understanding the concept of viewing a stock as a business, fundamentally, and understanding that to be successful in the stock market, you need to be successful in owning businesses that compound high rates over time. I think that’s the fundamental tenant that I took away from the Buffet/Munger philosophy.

I think the more Munger influence of buying high-quality business over time that compound because of that convergence between stock price and intrinsic value is probably even more of a fundamental tenant of our process. I think anything by the two of them is great. All of the books that have been written about them I devoured in my early investing career.

I like business biographies. Business biographies tend to just show how passionate people who live and breathe their business have created something out of nothing, such as the Sam Walton biography. I recently read a biography of In and Out Burger on the west coast, which I thought was really great. So, anything that you can get your hands on, modern business biographies have been extremely beneficial in understanding the characteristics of management teams that are exceptional, especially because they all don’t look identical but there are some common personality characteristics.

I think the McKinsey book on valuation was very helpful in constructing our original DCF models. I think more than reading the entire finance section at Barnes and Noble, a better approach would probably be to start reading as many annual reports that you can get your hands on because that’s what’s really happening in American publically-traded small businesses. You start to get a feel for what exceptional looks like by doing that.

Everybody in our office, oddly enough, even though it’s kind of an individual investor tool, reads Value Line cover to cover every week, the paper edition. It’s just mental weight lifting for us to get a sense for what returns on capital, returns on sales, and common-size financial statements look like for particular industries over time, and you can sort of see that “Hey, the precision instrument industry has really delivered fantastic results for investors over time” and “Hey, look the airline space has really done the exact opposite,” and you can start figuring out what industries and sectors are doing really well and which ones aren’t, and that can help hone your investment process a little bit and focus your time and energy on the right places.”

Rupal Bhansali, Chief Investment Officer – International Equities, Ariel Investments

“For someone who’s starting out, they should try to absorb a lot of information because you do need to have an antenna. Insights are developed when you connect the information, when you process the information, when you interpret the information. So that will come with experience and acumen and know-how. But it does not obviate the need for collecting that information. So it’s not easy.

They should read and learn from someone who’s been in the profession as up close and personal as they can. So the first thing they should do is try to find a job with someone who actually has a great long term investment track record because you learn from others. That’s why it’s like osmosis. You see people, how they process information, how they interpret it and it sort of gets into your DNA and your consciousness. It’s almost subliminal.

And you will form your own rhythm, and you’ll apply that know-how and knowledge at your own way because this is a very creative exercise but at least you will have learned from someone so that will speed up your process of creativities, as I like to think about it, as opposed to constrain it.”

Charles de Vaulx, Chief Investment Officer, International Value Advisers

“Besides the classics, Ben Graham, of course, I think Berkshire Hathaway annual reports. One has to not only read them, but re-read them. I’m very fond of Vladimir Nabokov, the writer of Lolita. He said, “a good reader is a re-reader”. I think some of the books that are a must would be Peter Bernstein’s book about risk, Against the Gods: The Remarkable Story of Risk.

I believe that awareness of history, in particular, economic history, financial history, history of how technological improvements and technological breakthroughs have impacted the world, and history of geography — are important, so I think some history books are a must. Financial history, there’s a wonderful historian who passed away a year or two ago, Charles Kindleberger, who many people know. One of his most famous books is Manias, Panics and Crashes, but he also wrote more in-depth books. One is called, The Financial History of Western Europe, and there are other books that are a compilation of many of his essays, and I think these are very valuable. There is a great book by David Kynaston called City of London. It goes back 300 or 400 hundred years and basically walks through the financial history of the world through what happened in the city of London.

Some reading that delves into behavioral finance and psychology can be very interesting. Daniel Kahneman’s books should be read along with Poor Charlie’s Almanack, which has transcripts of many of the speeches that Charlie Munger has made over the years.

Otherwise, for anyone who begins as an investor, I would recommend books by John Train. Some 20 or 30 years ago he wrote, The Money Masters, where you have a chapter on Ben Graham, one on Philip Fisher, one on Warren Buffett and so forth ,and then ten years later John Train wrote, The New Money Masters, with Peter Lynch, Mario Gabelli, and so forth. The advantage of those books is that you have one chapter on one money manager, and that book helps the reader understand that there are many ways, many recipes to invest money, and each of these ways has its own internal logic and own set of rules. If someone who starts as an investor reads the book, he or she will appreciate that there are many ways to do it, many ways to cook, and he or she will probably be able to, based on his or her temperament, identify and find some affinity with one of those investment styles, whether it’s George Soros or Paul Tudor Jones or Ben Graham with the cigar butts, or Philip Fisher. I think The Money Masters and The New Money Masters are great books to read to begin in our business.”

Tom Gayner, Chief Investment Officer, Markel Corporation

“I read endlessly. John Wooden, the basketball coach at UCLA during their dynasty is a hero to me. General Grant is a hero. Warren Buffett is a hero. Pick some good heroes and read everything you can about them.

I also like reading about history, psychology, and human nature, technological progress and scientific thought. The world is a fascinating place and you will never run out of rich material if you want to keep understanding more and more.

I think I saw a recent interview with Seth Klarman where he said something like, “value investing is the marriage of a contrarian and a calculator.” Some books, like Twain’s, the histories and biographies help you with the human nature and contrarian side of that equation. Some books, like the ones about science and technological developments, along with the accounting homework I did a long time ago, help you with the calculator side. Both elements are essential. Each is severely limited without appropriate balance and understanding from the other side.”

Robert Hagstrom, Chairman, SAM Investment Management Committee

“As students of the Buffett methodology, we’re becoming well-versed in the mechanics of it, well-versed in the procedures if you will. But we need to be spending a little bit more time on the issue of rationality. Buffett not only has the process and the mechanics down perfectly, but he has the rationality, the temperament that allows him to apply it and not get thrown off course.

And the mistakes that people make as they adopt the Buffett methodology is they get thrown off course by the emotional aspects of it. The irrationality of it all. We need to spend more time talking about that.”

Paul Lountzis, President, Lountzis Asset Management

“Greg Alexander [at Ruane, Cunniff & Goldfarb] once said to me: ‘You really learn from your mistakes’ and he’s so right. And so I try to reflect on ideas over the years that I’ve done right and especially those that I’ve done wrong: What could I have done better? What could I have known? What could I have not known?, and I find that very, very helpful to assess your performance and assess the exercising of your judgment. And that’s how you learn.”

Atticus Lowe, Chief Investment Officer, West Coast Asset Management

“For somebody that wants to get into the business, especially a younger crowd, interning is great, multiple internships to get different senses of different types of experience. We have an active internship program here at West Coast. And reading is a great resource whether it’s reading books on investments or just reading 10-K’s, annual reports, proxies – things of that nature, the more the better. We all have a passion for that, learning about businesses.”

Howard Marks, Chairman, Oaktree Capital Management

“I keep going back to what Charlie Munger said to me, which is none of this is easy, and anybody who thinks it is easy is stupid. It is just not easy. There are many layers to this, and you just have to think well. I can’t tell you how to think well. Some people get it, some people don’t.”

“There is no secret method for any of this stuff. You just have to be aware of concepts, smart in their application, and it helps to be an old man, or an old woman, so that you have the experience that helps.”

David Nierenberg, Founder, The D3 Family Funds

“And so, what would you say to someone other than the fact that you want them to read and think extensively, and at the very same time that they do it broadly, to drill a “T.” So that in the vertical part of the “T” you also build substantive expertise in a far narrower domain where you can establish true competitive advantage relative to what other investors might know. If you do both of those things and you keep doing it and you keep learning, you’re going to be fine even if you don’t have a Yale degree.”

Lisa Rapuano, Portfolio Manager, Lane Five Capital Management

“You can practice this craft anywhere. I don’t think that if you’re young and you know you’re a value guy, but you’re stuck in a growth shop or you know you’re an Asia guy and you get stuck in the Europe shop or whatever, I think you can learn anywhere. Too many people spend too much time needing a defined path and this is a very fluid business. You have to just sort of go with the flow sometimes. It’s also really hard to get a job so sometimes you just have to take what you can get and do your best wherever you are.

But I don’t think your job defines your philosophy necessarily, unless you get to run your own shop. Then you get to define your philosophy. But everyone works for someone, I work for my clients, everyone works for someone and so you’re always going to be able to be differentiate between what you are expected to do for your job and what you want to do for yourself, and you have to sort of figure out how to balance those things.

Too many people hold out for the perfect thing, and too many people have very, very strident views when they’re too young to have strident views. You need to develop and you need to learn. You can learn from anyone, anyone who has been successful in his business has something to teach you. Even the technician, even the momentum guy, even an economist, there’s something to learn from all of these people.

So I think that it’d be great to end up with the perfect match, with the perfect place that’s perfect for you. But in fact, unless you’ve started it, it’s not going to be perfect. So go with the flow, learn what you can, figure it out. Be glad that you’re somewhere and try to find the best from whoever it is that you’re working with.”

Robert Robotti, President, Robotti & Company

“As I always say…I’m not smarter than the average guy, I’m not more connected than the average guy, I’m not any of those things. And if I can be successful at investing, that means you can be successful at investing.

Therefore, the capabilities are within most humans to be successful, if you have an idea of what are businesses, how do they run, what are the drivers in terms of future economics and can you identify businesses that the market isn’t looking at properly. And that’s easy enough to do in certain cases because the market does have a very short term focus. And so by having that longer term focus, it’s not so hard to identify a couple of companies that the market isn’t getting right.”

Tom Russo, Partner, Gardner Russo & Gardner

“Stretch out your time horizon. Think five years and not five minutes. When you are presented with ideas always ask critically about the prejudice that may be expressed by the source of an idea. That came to me from the study of history. And the quick answer there is to say whenever someone says “Truth,” say, “Who says?” Understand the bias of a person who tells you something. It’s very good for critical thinking.”

Larry Sarbit, Chief Investment Officer, Sarbit Advisory Services

“It comes down to one good place to start and that is read Benjamin Graham, read Warren Buffett’s annual reports to shareholders which are easily accessible on the web. They weren’t accessible on the web because there was no web when I started investing back in the 1980’s. Read those, and read them all, and then reread them because he presents the most rational, the most logical, and the most business-like approach to investing.

That’s where I learned to invest was reading Buffett, reading Graham, or many other people who have written in this fashion and understand the power of this investment philosophy. That’s the place to start. If you get off in the right foot in this business and once you grab that concept that Buffett’s talking about and Graham’s talking about, it’ll guide you for an investment lifetime.

But as Buffett says grabbing the concept of value and behaving in a rational business-like fashion is like an inoculation. It either takes you immediately or never takes you. It either grabs you or it will never grab you. It’s not something you learn gradually, it’s not something you pick up on a slow basis. You either get it or you don’t. So read that stuff and read it early. The earlier you read it the more likely it is to grab your mind, and it’s the right way to go in my estimation.”

Kenneth Shubin Stein, Portfolio Manager, Spencer Capital Management

“It’s very important to do something you’re passionate about. Life is highly unpredictable. We have no idea about our future health, our future wealth and a lot of things in life are just hard to predict. Therefore, it makes all the sense on the world to do things that we’re passionate about now and today.

Suffering for a long period of time in the hope of some future payoff is generally not a good idea. One needs to do that to some degree to follow trades or professions and we all have to get through the grunt work to learn our crafts whether it be doctors, lawyers or investors. But it’s really important to follow passion I believe. Oftentimes, there’s a way to learn how to follow passion profitably. That’s not always the case but it’s often the case.

With students, I always suggest that they go into fields they care about and they enjoy because it’s just much more fun if you enjoy the process. I love what we do, I love what I do. I really enjoy being part of my company, I love being part of Columbia and overall it’s all great. It’s a lot of work but I really enjoy it. If I did not enjoy it, it would just be torture because it is a lot of work.

My first advice would be enjoy what you do. In terms of becoming a professional investor, one, I would say most people don’t need to. You can learn to be a very good investor and invest very profitably over your whole life without doing this professionally. Everybody needs to handle their retirement accounts and their savings accounts. These are very useful skills for everybody including just knowing you don’t want to be an active investor, and a very smart decision is for a lot people to say I’m not going to try to pick individual stocks and bonds. I’m going to go into index funds and you’re guaranteed to outperform more than half the professional money managers in the world if you just do that.

Just understanding how this works is important. It’s very competitive. If you can do something else profitably and enjoy it, there are a lot less competitive areas to go into. And if you do still want to pursue being a professional investor, and try to outperform the market over a long period of time then it’s very important to be a lifelong learner, to have a passion for learning.

Learning comes in all sorts of places. There’s experiential learning. There’s didactic learning. There’s a host of ways to acquire wisdom. Something Munger has talked a lot that I appreciate the longer I do this is this is not a business of who’s the smartest. There are a lot of very smart people that don’t end up doing well in our business. Being smart always helps if one is as smart as Buffett and Munger, I’m sure that’s fantastic but most of us are not.

It is a business of acquiring some worldly wisdom and I believe all of us can acquire worldly wisdom over time by trying to get better at this and trying to think better. A book that greatly impacted me was Poor Charlie’s Almanack, along with the essays of Warren Buffett or his annual letters, and a lot of what Ben Franklin wrote. Poor Charlie’s Almanack pulls a lot of this together in one book. I’ve read and reread that book several times and each time I do, I seem to get something else useful out of it, some other nugget or pearl of wisdom. For me, that’s what’s been helpful.”

Michael van Biema, Managing Partner, Van Biema Value Partners

“Certain people have, for lack of a better term, I will call funny ways of thinking about the world. They naturally think in an off-colored or contrarian, or whatever you want to call it way. It’s both fun and fascinating to listen to these people and listen to how they perceive various situations and various companies. They perceive them in a different light, and where the rest of us may see a very standard manufacturing company they will see something that actually is quite different, intriguing and should be valued in a completely different way…

The way we think about the world is basically a manager has two skills. He has the skill of being a stock picker or a good stock analyst, company analyst, and that skill is reasonably easy to identify and reasonably easy to document over time. The much more difficult skill is can he, does he know how to run a good portfolio and will that portfolio generate good returns over the long term?

We have certainly had managers who are great stock analysts and lousy portfolio managers, and therefore generated poor to mediocre investment returns. It’s unfortunate because they have half the skillset there but they don’t have the entire skillset. You got a guy who has a lot of raw talent but not in the right places necessarily. He’d do better if he wasn’t quite as good an analyst than he was a better portfolio manager.”

Amit Wadhwaney, Portfolio Manager, Moerus Capital Management

“It is important that anybody who goes down this path be aware of a few things. Know yourself. There’s certain kinds of things that value investors do which are not fun. Fun in terms of patience, fun in terms of due diligence. This is grunt work, this is hard work, it’s very unglamorous.

I would tell you growth investors have a far more glamorous life. That’s the fun end of the business. Their companies are always growing, they always look good, they have high ROEs. It’s always wonderful. We’re at the other end of the spectrum. We do the unpleasant stuff, we deal with these terrible companies, terrible countries, companies facing difficulties, companies which may need recapitalized. There’s all sorts of stuff. So know what you want to do. Value investing may or may not be for you. That’s item number one.

But notwithstanding that, if you really think value investing is for you, there’s a lot of stuff that’s been written about value. Books that come to mind – again, this is in no particular order – obviously Marty [Whitman]’s first book, his original copy of The Aggressive Conservative Investor was, to me, a great book. As I said before and I will say without being bashful, the book’s a damn turgent read. It’s a deadly read but it’s a very bright book. It’s full of a lot of ideas. Then, of course, are the other books that he’s written, namely Value Investing, A Balanced Approach. Those will get you going. And then, of course, Seth Klarman’s book, The Margin of Safety which also came out, I believe it was in the early ‘80s, if I recall. Seth’s book was a fabulous book, a great book. It’s a much more user friendly book. So there is that.

Then, of course, if you enjoy special situation investing, there’s Joel Greenblatt’s book [You Can Be a Stock Market Genius: (Even if You’re Not Too Smart!)], it’s got a very odd title. It’s actually a very bright book. I think it’s a very clever book. Again, I’m not a fan of mechanical investment formula. If that’s what you do Joel has another book about that. Most recently there’s Howard Marks’ book. Howard Marks is a great writer. The book is a very nice, easy summary of what we do, what he does. There’s no question there’s lots of wisdom encapsulated in Howard Marks’ book, which is a really worthy read.

So if you’ve made it through all that stuff and you actually read Graham and Dodd’s book, you really want to pursue it, the only way to do it is by doing it. Doing it is, I believe, a process of some degree of apprenticeship with somebody who is going to actually teach you. You can learn generalities. There’s an art of recognizing these things. There’s an art of not being freaked out by these things and these auctions where they’re staring you in the face. There’s an art of recognizing things that are sometimes very subtle, things that could hurt you. That’s very important. You can only learn that by doing and you do it by ideally working with an experienced person. I mean, it’s obviously easier said than done, finding the right person who’s actually looking for somebody, or the right temperament to be a mentor. But that’s probably the way to do it.”

NOTA DEL EDITOR: Esta idea de inversión es obtenida de una carta a los inversores de Numantia Patrimonio Global.

* * *

Ryman Healthcare: Continuando con las buenas perspectivas a largo plazo como nuestro hilo conductor, una de las nuevas empresas que encontramos en cartera y de la que esperamos ser accionistas muchos años es Ryman Healthcare. La empresa diseña, construye y opera villas de alta calidad para la tercera edad en Nueva Zelanda y Australia.

Controlan toda la cadena de valor, desde la construcción de los edificios hasta la contratación de las enfermeras. Poseen 32 villas y tienen 14 más en distintas etapas de desarrollo. Proporcionan un hogar, una comunidad, compañía, seguridad y cuidados a personas que ya no pueden cuidarse por sí mismas. Una necesidad básica, natural y poco cambiante.

The Evolution of Value Investing Since Graham-Newman

April 12, 2018 in Commentary, Featured, Full Video, History of Value Investing, Interviews, TranscriptsWe had the great pleasure of sitting down with Brett Reiss, senior vice president of investments at Janney Montgomery Scott, to discuss the evolution of value investing since the time of Graham-Newman, the investment partnership founded by Benjamin Graham.

Brett Reiss on how value investing has changed, and what remains the same:

Members, log in below to access the restricted content.

Not a member?

Thank you for your interest. Please note that MOI Global is closed to new members at this time. If you would like to join the waiting list, complete the following form:

This article by John Lewis is excerpted from a letter of Osmium Partners.

Rosetta Stone Inc. (RST; $13.20)1, together with its subsidiaries, provides technology-based learning products in the United States and internationally. It operates through three segments, Enterprise & Education, Literacy and Consumer. The company develops, markets, and supports a suite of language-learning, literacy, and brain fitness solutions consisting of software products, Web-based software subscriptions, online and professional services, audio practice tools, and mobile applications. Rosetta Stone’s current market capitalization is approximately $297 million. The company generated $192 million in sales for the LTM ending September 30th, 2017. (RST is a holding across all funds.)

We were very impressed with Rosetta’s 4th Quarter 2017 results.

Members, log in below to access the restricted content.

Not a member?

Thank you for your interest. Please note that MOI Global is closed to new members at this time. If you would like to join the waiting list, complete the following form:

Certain factual and statistical (both historical and projected) industry and market data and other information contained herein was obtained by Osmium Partners from independent, third-party sources that it deems to be reliable. However, Osmium Partners has not independently verified any of such data or other information, or the reasonableness of the assumptions upon which such data and other information was based, and there can be no assurance as to the accuracy of such data and other information. Further, many of the statements and assertions contained herein reflect the belief of Osmium Partners, which belief may be based in whole or in part on such data and other information. The analyses provided may include certain statements, assumptions, estimates and projections prepared with respect to, among other things, the historical and anticipated operating performance of the companies. Such statements, assumptions, estimates, and projections reflect various assumptions by Osmium Partners concerning anticipated results that are inherently subject to significant economic, competitive, and other uncertainties and contingencies and have included solely for illustrative purposes. No representations, express or implied, are made as to the accuracy or completeness of such statements, assumptions, estimates or projections or with respect to any materials herein. Actual results may vary materially from the estimates and projected results contained herein. Past Osmium performance is not indicative of future results. Osmium Partners disclaims any obligation to update this letter. A portion of the Partnership’s assets may from time to time be invested in securities that have limited liquidity. The Partnership’s investment strategy is to make concentrated investments in what it views as its best ideas. The Offering Memorandum and Limited Partnership Agreement offers a comprehensive overview of the risk factors involved in investing with Osmium Partners. The information contained herein is provided for informational purposes only. This is not an offer to sell, or a solicitation to buy, limited partnership interests in Osmium. An investment in Osmium is not suitable for all investors. Stocks mentioned in the newsletter do not constitute a recommendation to buy or sell the individual securities.