This article is authored by MOI Global instructor J.Dennis Jean-Jacques, founder and chief investment officer of Ocean Park Investments LP, based in Stamford, Connecticut. Dennis is an instructor at European Investing Summit 2023.

An Omaha Encounter with Susie Buffett

I have an aunt on my wife’s side of the family who lives in Omaha, Nebraska. Over 20 years ago, in 2000, I attended my first Berkshire Hathaway meeting. Rather than stay with Aunt Lafae, I decided to stay in a hotel. That year, the hotels near the old Omaha Civic Auditorium, where the annual shareholder meeting was being held, were unusually low in capacity. Few people decided to make the pilgrimage to Omaha in 2000 because Warren Buffett, according to many publications at the time, was not as relevant in the modern era. This was the height of the dot-com bubble. Perhaps would-be attendees at the annual meeting convinced themselves that value investing was outdated. That value investing was dead. Again.

The low attendance gave those of us who attended, and me, the opportunity to fully experience the weekend activities, bond with colleagues and make new friendships. At the Berkshire meeting, sitting in a sparsely attended auditorium, I walked up to the microphone and posed a question to Warren and his partner, Charlie Munger. I thanked Buffett for continuously sharing his knowledge and asked him a specific question about business moats. Buffett gave me a detailed answer and ended with: “… And I thank you for coming.” A statement, which I suspect, had a bit more meaning to Warren given the low attendance at the annual meeting that year. My question to Buffett and his full response has since been posted at various places online including here.

Soon thereafter, an older woman approached me and asked if I would like to meet Warren. I did not know who she was at the time, but I agreed. She and I spoke briefly, and we walked to another room. Today, on my desk, sits a framed picture of me and Warren Buffett backstage after that meeting and the woman who introduced us, Warren’s wife, Susan T. Buffett smiling over my left shoulder in the background. I learned from our conversation that day, how much of a committed champion Susie was for women rights and equality for all.

I firmly believe if there had not been a brief Omaha dislocation in attendance at the Berkshire annual meeting from the those who normally attend, I would not have had the opportunity to publicly thank Warren and meet Susie Buffett. Susie became ill and passed away a few years later.

Investing During Market Dislocations

Dislocations are special, vintage periods presenting unique opportunities to participate in activities that one, otherwise under normal circumstances, would not have been afforded the opportunity to participate. In the public markets, it is often a vintage opportunity period that plants seeds for future outsized returns when there are forced sellers and fewer buyers.

For many investors to maximize opportunities during dislocated markets, the challenge is to 1) employ the right temperament that is consistent with a patient and opportunistic investment process; 2) actively prepare and be informed when such dislocated opportunities are occurring, and 3) have your capital for investment structured in a way that you are liquid enough to take advantage of opportunities. The objective is to capture asymmetry where the downside is lower, and the upside is higher. However, you are not going to capture asymmetry consistently without having the right mindset.

Having The Right Temperament

It is important to know how you are wired, your behavioral tendencies. The number one skill and most enduring in value investing is having the right temperament – the right patience, self-control, and judgement to decipher fact finding from storytelling. A temperament for emotional steadiness and delayed gratification. Value-based dislocations are grounded on an ascertainable, intrinsic worth of a company that has been severely disjointed from its public share price. For the appropriately tempered value investor, there is limited appetite for storytelling and speculation about key assessments such as business quality and management excellence. They want to see the facts; business track records. It is like buying the highest grossing farmland during a real estate correction or buying five-star travel-related assets during a shelter-in-place pandemic. You know an Omaha dislocation when you see one. Temperament is vital as an investor because you should be comfortable being in the minority in such dislocated situations to allow yourself to think independently.

One mistake I see investors make during dislocations is drifting into groupthink and speculations. In the public markets, reality is often processed through group perception, or storytelling. As Ben Graham discusses in the very first chapter of his 1949 classic book The Intelligent Investor, speculative investing is an exercise in persuasion. Shareowners make money if future buyers are persuaded to agree with a higher perception of value. The hope of the speculators is that future would-be owners will be persuaded by narratives and stories. Unsurprisingly, key star contributors of this game of speculation are the very best storytellers which might include certain Wall Steet pundits, fast money traders, and even management teams. Value investors speculate less and think independently more.

Humans have evolved and survived because we like to think and act the same while staying in groups. This is how we are wired. Resisting that urge for groupthink can be difficult for some. One way to neutralize this is to be an independent researcher with genuine curiosity about companies and how they generate value for shareowners. Indeed, value investing is more like being an investigative journalist or a critical historian than it is being an economist. You must be willing and eager to read everything there is to know about a particular company, its management team, and the industry. Dislocated opportunities do not come routinely. When they do, you must be prepared to jump on it.

Actively Preparing for Opportunities

Preparing to put capital to work during market dislocations is a bit different than in other environments. For one, it could be frustrating once you realize that after extensive research is done on a particular company, no one knows when such accumulated, detailed knowledge will be put to good use. Yet, much of your ability to assess situations will be based on how well you were prepared – assessing companies several weeks or even months before any expected dislocations or special opportunities would occur.

Having a research framework is critical. Keys to any research framework is evaluating the quality of the business and company moats; knowing why the market is offering you the company at such a price; understanding the company’s true worth as well as the catalysts needed to get the shares to fair value are important. But the assessment of your downside protection, your margin of safety is most important.

During dislocations if you are knowledgeable and assess the downside correctly, the rest will take care of themselves. While listed equities are consistently discounted during broad market swings, during market dislocations, the goal for value investors is to identify those companies who are truly impaired and should be discounted and those that are only temporarily disconnected from their true worth. Your job is to know the difference. Few things in this profession are as satisfying as buying shares of a great business during a dislocation when your downside is the least and your upside is the greatest.

If you missed the last dislocation, don’t worry, there will be another. Market dislocations happen more often than people would believe. Many recall the major dislocations such as the global financial crisis, the pandemic, or most recently, the summer of 2022. But since the GFC in 2009, including the great bull market run that followed, the S&P 500 was down at least ten percent every 18 to 24 months. Being down 10% for the broader market does not seem much of a dislocation, but if one looked deeper into the numbers, during those times, some very valuable companies were down over 40%. Certain investors missed these opportunities because if, for example, you were running a long only portfolio, you were likely nursing a performance drawdown as well with the market.

Having The Right Fund Structure in Place

Warren Buffett has seen significant market corrections and dislocations in his career. Yet, during those times, he leans forward often underwriting new positions. Indeed, the structure of Berkshire’s funding source is different and unique. It seems that each time during tough performance periods, Buffett is out in the markets planting seeds for future outsized returns. It is clear that Warren structures his life’s activities, and investable capital in such a way that when market dislocations appear he is prepared, knowledgeable and ready to act. Fund structure matters. A lot.

Some investors use high cash levels as part of their portfolio construct to protect capital in order to prepare for dislocated opportunities. At times, some funds hold as much as 20% to 30% of their portfolio’s capital in cash. With treasury bills rising to the mid-single digits lately, that seems quite attractive. However, I am not sure how consistently T-bill levels will remain at such levels or if fundholders are content paying active management fees on such high, inactive cash levels.

Another solution is to run a low net market exposure portfolio construct to generate adequate return as one actively prepares for market dislocations. Low net exposure often refers to portfolios with long and short positions with net exposure to the equity market of less than 20%. Indeed, some of the best low net strategies have less than 10% market exposure while adequately compounding and preserving capital, particularly during significant market dislocations. There are a number of well-known hedge fund platforms and long short managers who do this well. It is a skill that can be acquired, but many value investors tend to shun away from shorting stocks. This makes a lot of sense in one context. But given our objective, this is a mistake.

Warren Buffett and his mentor, Ben Graham, both shorted stocks heavily. As for Buffett, he shorted stocks consistently to help preserve capital until he was able to structure his investable capital and access permanent capital.

Running a low net portfolio construct is a way to compound and preserve capital, as well. In addition, there are other benefits to being a long-short manager, such as gaining a differentiated perspective. Troubled companies and those artificially held up in an overly euphoric market are often the first to be repriced. Second, shorting companies makes investors better analysts. For those investing with a long-short investing capability, up to half of what you do every day is look at companies that are likely to run into fundamental hardships. In such situations, you can still put that knowledge to work. This ability to act gives an investor more conviction when they come across a really good long idea. Indeed, long-only investors may not get the same benefit partly because everything they come across, subconsciously starts as a potential buying opportunity. It reminds me of the old adage: if you give a person a hammer, everything looks like a nail.

The third advantage, and perhaps most important, is investing during dislocations: Short positions allow one to hold on to long positions longer in a portfolio that is able to withstand steep market declines. Needless to say, if the market is being dislocated and your portfolio is relatively unaffected, you are more emboldened to add to your very best long ideas or seek new ones that are being thrown out by distressed owners. With the right long-short structure, preserving capital going into market dislocations is perhaps an underappreciated structural advantage.

A Final Word on Dislocations

There are significant inefficiencies during market dislocations. A value investor with the right temperament and fund structure is uniquely positioned to capitalize on those inefficiencies. Great ideas do not happen every day, every month, or even every year. When they do appear, however, it is best to have been actively preparing by compounding and preserving your investable capital.

One needs to participate in a number of dislocated markets over a time period to generate outsized returns for their fundholders. Once again, temperament and behavior are critical. It reminds me of Buffett’s “punch card” approach. Warren provides an analogy where an investor has a fixed number of slots in a punch card that represents all the investments that can be made in that investor’s lifetime. Once the investor punches through all the slots on that card, he or she cannot make any more investments. Buffett then makes an important point about good investment behavior. In that punch card scenario, the investor would really think long and hard about when to use each opportunity to invest and to load up when she does. Some value investors think those unique opportunities often come during market dislocations when there are motivated sellers and few buyers.

Back in Omaha, Nebraska, the Berkshire Hathaway annual meeting attendance “dislocation” that I experienced two decades ago has long been corrected. In fact, last year, the nearest hotel room I could find was across state lines in Council Bluffs, Iowa. Needless to say, Aunt Lafae has been getting early calls from me, at least once a year, to prepare her guest room.

Members, log in below to access the restricted content.

Not a member?

Thank you for your interest. Please note that MOI Global is closed to new members at this time. If you would like to join the waiting list, complete the following form:

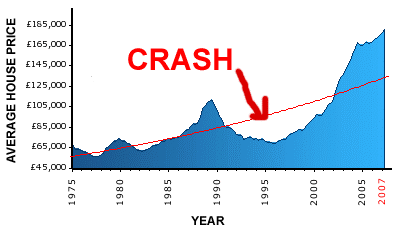

Source: Sky News.

Source: Sky News. Source: Landlord Blog.

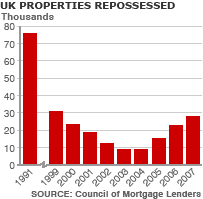

Source: Landlord Blog. Source: BBC.

Source: BBC.