This article is excerpted from a letter by MOI Global instructor Patrick Brennan, portfolio manager of Brennan Asset Management.

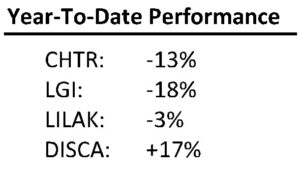

As detailed in several of our previous letters, we believe investor fear over a changing landscape has created several opportunities in the media/telecom sector. Our largest positions are in various cable systems around the world: Liberty Global (LGI), Charter (CHTR) via Liberty Broadband (LBRDA)/GCI Communications (GLIBA), Liberty Latin America (LILAK) and in one mispriced content asset (DISCA).

While investors may group all cable names together, we believe the cable industry structure, growth outlook and regulatory environment vary considerably for cable companies in the US versus Europe versus Latin America. DISCA, our sole content investment, is most exposed to the ever-changing (for the worse) US TV ecosystem. As we have noted in multiple letters, we believe cable’s broadband business is better protected from the various video cord-cutting pressures that are likely to continue or to accelerate. We think this basic thesis has not materially changed, but investors’ reactions to the various media assets have varied widely.

CHTR (which we own via Liberty Broadband and GCI Communications) declined nearly 12 percent in a single day this past April as investors fretted about the decline in video subscribers with a chunk of the decline related to so-called “non-pay disconnects.” Essentially, as CHTR moved from 13 to 2 billing systems, certain individuals were erroneously not required to pre-pay their subscription.

These customers never paid for their service and CHTR disconnected them. While CHTR’s integration of the Time Warner and Bright House acquisitions has generally gone well, this non-pay error was a clear glitch. There will be some carryover effect from this change in the second quarter, but the mistake will not impact the back half of this year. If this is CHTR’s worst integration issue, it will have done a phenomenal job. While the one-day decline was not fun, there does not appear to be any lasting harm.

That said, the “non-pay” issue did not account for the entire video subscriber decline and CHTR was negatively impacted by the video losses affecting the rest of the media industry. Over the past couple of years, CEO Tom Rutledge has publicly discussed growing the video subscriber base, but during the first quarter call, he essentially stated that the ultimate free cash flow will not materially move with “a couple of million video subs.” In our opinion, this sentiment is directionally accurate, but some investors interpret his statement as essentially moving the goal posts and thereby hurting his credibility. Additionally, CHTR’s stock drop likely reflected some concerns about the pending rollout of 5G wireless broadband services which we discussed in our Q1 letter.

We presented LBRDK/GLIBA at Wide-Moat Investing Summit, hosted by MOI Global, this past June where we discussed the above issues in far greater detail. […] We believe Rutledge’s basic thesis regarding video loss impact on free cash flow is directionally accurate. That said, we wish Rutledge would have acknowledged a range of possibilities relating to the US video market. Video subscribers are generally costlier to service (higher number of questions/complaints) and require large amounts of capex support (technicians and video boxes). For this reason, there are considerable offsets for cable if video losses continue to accelerate. We will not rehash the entire 5G conversation again, but we simply note that there are considerable uncertainties with regard to the underlying technology, timing, costs and addressable markets. Furthermore, even if the technology works perfectly, the most plausible rollout areas of deployment are in the largest metropolitan areas, and CHTR is underrepresented in these areas. We continue to believe that CHTR is undervalued and that owning the name through LBRDK/GLIBA allows a “double discount,” as we can own CHTR at levels 10-20% below the current stock price.

DISCA is perhaps more controversial than CHTR, and the number of issues that DISCA bulls and bears agree upon is probably similar in number to the shared political beliefs of Donald Trump and Elizabeth Warren (with conversations often as friendly). That said, we would suggest that going into the first quarter, both bulls and bears probably would have agreed that US video losses would continue, that there would be continued growth in DISCA’s international business, and that DISCA was likely to increase synergy targets from its recent Scripps acquisition. Unofficially, we also believe that ~90 percent of the bull/bear camp would also agree that CEO David Zaslav was likely to make a hyperbolic statement during the earnings call regardless of results. All of these expectations came to fruition (arguably the synergy bump was greater than anticipated) when DISCA reported first quarter results and yet the stock still rose.

What has changed? From a fundamental perspective, very little. In fact, DISCA’s stock price barely budged earlier in the year, despite a rash of upgrades from sell-side analysts who finally calculated pro-forma numbers and ran out of creative ways to show “neutral” ratings with 50%+ upside. But, a couple of external events (neither surprising) marginally changed sentiment on the name. First, AT&T’s acquisition of Time Warner was initially approved without condition[2]. At the same time, Comcast and Disney were practically tripping over each other to acquire Fox/Sky at nosebleed valuation levels (the ~13x valuation for Sky is insane relative to the implied value of LGI – more on this in a bit). Some investors began to realize that there are only a certain number of international content assets still available as the demand for global content continues to accelerate. At roughly the same time the deal was approved, Dr. Malone bought $30+ million worth of stock in the open market. We would argue that this news (while quite positive) was not completely unexpected as Dr. Malone publicly declared that he liked the Scripps merger and would consider additional purchases. Of course, an even larger Malone open market purchase of LILAK approximately one year ago has not inspired LILAK investors, as investors can now purchase shares nearly 20% below what Dr. Malone paid. But, we digress. We have no doubt that investors could punish DISCA shares if US subscriber losses materially increase. Furthermore, we do not argue that DISCA’s US business is not facing substantial headwinds and could very well be a declining business over time. Instead, we simply argue that DISCA’s international business is stronger than many realize and its increased US size, increased focus on female viewers and the possibility of further skinny bundle penetration are not reflected in its current valuation.

And then there is Liberty Global (LGI) – the “bad news bears” of the cable space. In several past investor letters, we described management missteps but argued that the private market value of its cable assets was far higher than current trading values. We also noted that a transaction with Vodafone was highly likely. So, after announcing a deal with Vodafone (VOD) that values its German and select Eastern European cable assets at ~11.5x trailing EBITDA, we were surprised to see the stock actually decline 6 percent on the day of the announcement. LGI has never been an easy asset for outsiders to value. It operates in multiple markets with varying ownership levels, is listed in the US but operates exclusively in Europe (F/X and Brexit 2.0 concerns), has content/tax assets and is currently embarking on an aggressive rollout (Project Lightning) that significantly inflates current capex levels. Unlike CHTR, LGI has not provided a clear breakout of the value of its content assets and significant tax assets and, this value is therefore often ignored by investors. Furthermore, Deutsche Telecom’s CEO has loudly complained about the VOD transaction. While the deal will be reviewed at the EU level (not at the local German level) and while past regulatory history would suggest approval is likely, there will be multiple ugly headlines before the deal closes.

Certainly, LGI’s Swiss market has weakened and the sell-side has become more concerned about UK organic growth levels. Investors have grown increasingly disillusioned with CEO Mike Fries, who many perceive as overpromising but under-delivering.

Clearly, LGI has been a frustrating name to own, especially as the broader market has gone straight up. The UK is a competitive market, but we continue to see price increases from competitors and we think low single-digit operating cash flow growth is likely. At current valuation levels, little else is needed to achieve meaningful upside. Assuming the deal goes through, the stock currently trades ~6.3x 2019E EBITDA, near recession trough valuation levels and far below private market value. If shares don’t budge and the VOD deal closes as expected, LGI could end up retiring nearly 50% of outstanding shares.

Again, the business dynamics of LGI/LILAK/CHTR are very different – Virgin’s UK performance has little to no correlation to CHTR’s mobile launch in the US or Chile’s continued fiber rollout. But, cable is quite unpopular and therefore multiple contractions at CHTR will impact those at LGI and LILAK. We cannot pinpoint a single moment when this will change, but we believe investors will ultimately reexamine whether double-digit free cash flow yields for oligopolistic businesses are really appropriate.

[2] As we were completing this letter, The Justice Department announced an appeal to AT&T’s merger with Time Warner, after the deal was completed in June.

Disclaimer: BAM’s investment decision making process involves a number of different factors, not just those discussed in this document. The views expressed in this material are subject to ongoing evaluation and could change at any time. Past performance is not indicative of future results, which may vary. The value of investments and the income derived from investments can go down as well as up. It shall not be assumed that recommendations made in the future will be profitable or will equal the performance of the securities mentioned here. While BAM seeks to design a portfolio which reflects appropriate risk and return features, portfolio characteristics may deviate from those of the benchmark. Although BAM follows the same investment strategy for each advisory client with similar investment objectives and financial condition, differences in client holdings are dictated by variations in clients’ investment guidelines and risk tolerances. BAM may continue to hold a certain security in one client account while selling it for another client account when client guidelines or risk tolerances mandate a sale for a particular client. In some cases, consistent with client objectives and risk, BAM may purchase a security for one client while selling it for another. Consistent with specific client objectives and risk tolerance, clients’ trades may be executed at different times and at different prices. Each of these factors influences the overall performance of the investment strategies followed by the Firm. Nothing herein should be construed as a solicitation or offer, or recommendation to buy or sell any security, or as an offer to provide advisory services in any jurisdiction in which such solicitation or offer would be unlawful under the securities laws of such jurisdiction. The material provided herein is for informational purposes only. Before engaging BAM, prospective clients are strongly urged to perform additional due diligence, to ask additional questions of BAM as they deem appropriate, and to discuss any prospective investment with their legal and tax advisers.

About The Author: Patrick Brennan

Patrick Brennan is the founder and portfolio manager of Brennan Asset Management, a Registered Investment Advisory firm based in Napa, CA, which utilizes a concentrated value investing strategy. Patrick has given presentations at multiple value investing conferences, including presentations to The New York Society of Security Analysts (NYSSA), The Nebraska Society of Securities Analysts and presentations on various names at the VALUEx Vail Conferences. Patrick coauthored an article on tracking stocks with Lawrence Cunningham for The Financial History Magazine and Patrick was featured in a write-up of Liberty LILAK in The Private Investment Brief. Prior to founding Brennan Asset Management, Patrick managed portfolios and led research efforts at two value investing firms in California: Hutchinson Capital Management and RBO & Co. Previously, Patrick worked at Mark Boyar & Company, where he led the firm’s research team and helped manage $800 million of assets across individual portfolios, institutional accounts and a mutual fund. Patrick also worked for six years in investment banking and equity research with Deutsche Bank, CIBC World Markets and William Blair & Company. Patrick graduated summa cum laude from the University of Notre Dame with a degree in economics and was inducted into Phi Beta Kappa. Patrick received the Chartered Financial Analyst (CFA) designation in 2002 and is a member of the CFA Institute (formerly AIMR). Patrick is originally from Omaha, Nebraska.

More posts by Patrick Brennan