MOI Global had the distinct pleasure of sitting down for a wide-ranging conversation with David Marcus, co-founder, chief executive officer and chief investment officer of Evermore Global Advisors, in mid-2017. Shai Dardashti visited David at Evermore’s headquarters in Summit, New Jersey.

David has more than two decades of experience in the investment management business. He began his career at Mutual Series Funds, mentored by renowned value investor Michael Price, and rose to manage the Mutual European Fund and co-manage the Mutual Shares and Mutual Discovery Funds. He also served as director of European Investments for Franklin Mutual Advisors. After leaving Franklin Mutual, David founded Marcstone Capital Management, a long-short Europe-focused equity manager, largely funded by Swedish financier Jan Stenbeck. When Mr. Stenbeck passed away in 2002, David closed Marcstone and then co-founded a family office for the Stenbeck family; as an advisor to the family, he advised on the restructuring of a number of the public and private companies the family controlled.

David has shared profound insights into catalyst-driven investing and owner-operated businesses, particularly in Europe, with the MOI Global community on multiple occasions over the years. We are fortunate to benefit from David’s wisdom. Enjoy!

The following transcript has been edited for space and clarity.

MOI Global: You spent fourteen years working with Michael Price, one of the great value investors. Share a bit about this background experience.

David Marcus: It was a phenomenal experience. I started working for Michael as an intern while at Northeastern in Boston, just before the crash of 1987, so it was quite some time ago. I began answering the phones as a customer service representative. I had always wanted to work in the environment of picking stocks and being around investing. That internship gave me my shot to do that, and being in the room while they were doing their thing was a transformative learning experience, and my first exposure to the trading floor. It stuck with me, so when they offered to hire me full time after graduation I accepted without considering any other opportunities. I came back after I graduated in 1988, and stayed all the way through to 2000. I went from answering the phones to being an assistant on the trading desk, getting screamed at all the time, and eventually getting my shot as a junior analyst. I learned pretty early that Michael respected one thing: “You’re here to make money for the clients, if you do that, you will do well here.” To Michael, everything else was noise. My focus became picking stocks that made money for the clients.

I worked on the desk, I became a junior analyst, I worked my way up by working on ideas for Michael and other senior analysts in the firm, learning from a variety of people, and eventually finding my own ideas and getting portfolio management responsibilities. In 1996 he sold the firm to Franklin Templeton – I stayed until 2000. When Michael left he anointed people into different roles; I became head of all European investments. I was given my own fund to run when I was named the sole manager of the Mutual European Fund. I was also named co-manager of the global fund, Mutual Discovery, and the flagship domestic fund, Mutual Shares. At the time that I left I was managing or co-managing more than half the firm’s assets – about $14 billion.

In the years that I was there I learned so much. Michael wasn’t there to be a teacher; you had to sort of absorb it. We all sat in one big room. He sat on the trading desk, he had an office – he was rarely in it, he was on the desk. If you did well, you didn’t hear much; if you made a mistake, you sure heard about it and so did everybody else, because you were all in one big room, there was no place to hide. You learned how to develop a thicker skin, and to get ahead you had to always pick yourself up after your knockdown, dust yourself off and come back the next day looking for another idea, or continuing to work on the idea that you thought was a good idea and just keep pushing forth, always learning. Michael brought out the best in those who were willing to work at it.

MOI Global: You said ‘absorb it’ – could you elaborate what you absorbed?

Marcus: Michael had a distinct style of investing, which wasn’t just focused on finding cheap stocks. He would simply ask, “Great, it’s cheap, what’s going to make it go up?” Which, to me, means what are the catalysts? I was always trying to figure out what is going to make this stock go up. Because there are so many stocks out there, especially back in those days, that were cheap. Some of them were perennially cheap stocks, and some were value traps. This focus on catalysts, what is going to make it go up, what is going to make the stock do well and become less cheap, first and foremost, was absorbed. But it was about digging through the footnotes, digging through the balance sheet and understanding hidden assets.

Even Seth Klarman in the foreword or the introduction to his book Margin of Safety writes about the two years that he worked with Michael Price and Max Heine. He wrote about the concept of digging deeper, and that is truly what Michael pushed us to do. What is in that “other” category on the balance sheet, what are those other assets, are they on the books at cost and they are real estate assets in midtown Manhattan? Is it a fantastic property that’s priced at the level of a hundred years ago; what is it? Or, is it a portfolio of securities? That has been an area where we’ve historically found a lot of gems, where companies bought something many years ago or two CEOs ago. Current management does not think about it. I have seen cases where management didn’t even realize they owned all the land around their building; crazy things happen. This concept of digging deeper, and then after you dig deeper – go even deeper, and find where the trail takes you. That tenacity is invaluable. We do that to this day. Even though that was decades ago, many of those lessons and methods are the foundation of everything that I do today here at Evermore.

MOI Global: Could we learn a bit more about your operating experience, private companies, public companies, company board seats?

Marcus: As I said, the foundation was what I learned working for Michael Price at Mutual Series. After I left the firm in 2000, I started my own business. I partnered with a Swedish industrialist, a man named Jan Stenbeck, who was the chairman of seven public companies in Europe, including telecom, media, and forestry businesses. I had gotten to know him when I was at Mutual Series, because I was fixated on getting to know who runs the businesses, meaning it’s not just meeting the CEO or the CFO or the Chairman, it was who’s the main shareholder? Ultimately, as I got further along in my process and I was investing outside the US, I realized there’s so many families that control businesses. I’d call on those families, anyone that would say ‘no’ to a meeting, I’d keep calling them. Of course, they would say ‘no’ the next time, but I wouldn’t take no for an answer. I’d call, call, call, and eventually get a meeting. Some of those meetings turned into relationships and I continue to this day to talk to them. Get together, talk about ideas, pick their brains, share thoughts on what we’re seeing here in the US.

One of those was Jan Stenbeck. He and I partnered in 2000. He seeded the business with one hundred million dollars, then I grew a fund around that. But, what he also did was, he invited me into his inner circle, with the CEOs of all his public and private businesses. Once I partnered with him I didn’t invest in any of his companies. Instead, I would sit in the kitchen at his farm in Luxembourg, where it could be two o’clock in the morning, and it’s me and Jan and the CEOs of all these other companies, and we’re talking about strategy, like how they’re going to attack telecom in Germany. I started to be on the inside, getting first-hand experience for how these guys were running their businesses in developed markets, in emerging markets. It was an eye-opener. Getting this exposure was invaluable. As a stock picker, you don’t usually get the insider’s perspective. I ended up going on boards; the board of a bank, the board of a media company.

Unfortunately, Jan died two years into our partnership. When he died I closed the fund, returned the capital, and helped his family build their family office. As part of that, I became the chairman of their US holding company, which was a private equity business and had wholly-owned operating units as well. I found myself getting immersed into helping fix companies: it was a turnaround situation, restructuring businesses. Then, I went on the board of their media conglomerate, which is a three billion market cap in Sweden, and became an advisor for their telecom business for emerging markets. I reported to the board, and I helped them restructure the balance sheet. Once again, going from the one side of the desk where you’re picking a stock, to the other side where you’re helping make decisions – should we keep this CEO, should we keep these board members, should we change out the old guard, put in more aggressive and progressive board members and managers? That experience has been invaluable — and then helping management review strategy, business lines, and push them to consider if we should keep a business unit or not, for example. In the long-run, it has helped me become a better investor because I have the insider’s perspective, not just the outsider’s perspective.

Having all these perspectives and viewpoints, from running a business, it makes us more cynical to challenge these managers when they talk about their restructuring or plans going forward.

MOI Global: What do you aim to do at Evermore Global that capitalizes on what you’ve learned throughout your career, to date?

Marcus: We started Evermore with the launch of our ’40 Act fund, the Evermore Global Value Fund, in 2010. To me Evermore is the culmination of everything that I’ve done prior to this. The foundation is the investment approach that I learned from Michael Price, cheap stocks with catalysts; it is engrained in my DNA, a successful transfer of knowledge. We add the operating experience. We’ve also developed an unbelievably extensive network of individuals, capitalists, families that control businesses, Chairmen and CEOs. We’re not looking for secrets when we talk to these people in the network, we’re looking for perspective and interesting ideas we hadn’t considered. Or, they’re helping us vet and triangulate investments or people that we’re looking at. There are also certain investment bankers around the world who understand the kinds of things that we are looking for. The network is invaluable to our research process.

At Evermore we’re focused on creating value for our investors. That’s all we’re here to do, make money for our clients. To do that, our approach is to look for cheap stocks, where there are catalysts, and we leverage everything that we’ve come to know over the years. It’s the hedge fund knowledge, it’s private equity knowledge, it’s operating experience, and bringing it all into a mutual fund, charge a mutual fund price, and deliver things that you don’t normally find in a mutual fund. We have a mutual fund as our flagship, and then, for certain institutional investors, we manage separate accounts that invest similarly. Not everybody can invest in a mutual fund.

Even though we’re in a world of 70,000 mutual funds, our view when we put the business together was, “Does the world need one more mutual fund?” The answer was yes, but only if you bring something differentiated to the table. You can’t go into an investor meeting and say, “Hey, here’s why I’m different.” That’s what everybody does. You’re no different if you start off by saying that. What makes you different should come out of you when you talk about how you invest. People should say, “That guy is different, and he makes money. We have seen the gamut of investors, and we try to associate with the best of breed that are able to pick up on these nuances.” My thought is, we are not here to serve everybody, we are here to serve those investors whose worldview and investment perspectives match our own. Opportunistic investors, investors who could care less about what the benchmark is doing, and, investors who don’t impose artificial handcuffs to an investment approach, will benefit the most from partnering with us.

MOI Global: I once heard you detail how the world of traditional value approaches has changed…

Marcus: [Content restricted to members of MOI Global]

Members, log in below to access the restricted content.

Not a member?

Thank you for your interest. Please note that MOI Global is closed to new members at this time. If you would like to join the waiting list, complete the following form:

Mutual fund investing involves risk. Principal loss is possible. The Fund invests in foreign securities which involve greater volatility and political, economic and currency risks and differences in accounting methods. These risks are greater for emerging markets. Investing in small and mid-sized companies involves additional risks such as limited liquidity and greater volatility. The Fund may make short sales of securities, which involves the risk that losses may exceed the original amount invested. Investments in debt securities typically decrease in value when interest rates rise. This risk is usually greater for longer-term debt securities. Investment in lower-rated, non-rated and distressed securities presents a greater risk of loss to principal and interest than higher-rated securities. Due to the focused portfolio, the fund may have more volatility and more risk than a fund that invests in a greater number of securities. Additional special risks relevant to our Fund involve derivatives and special situations. Please refer to the prospectus for further details.

Investors should carefully consider the investment objectives, risks, charges and expenses of the Fund before investing. This and other important information is contained in the Evermore Funds’ statutory and summary prospectuses, which may be obtained by contacting your financial advisor, by calling Evermore Global Advisors at 866-EVERMORE or (866-383-7667) or on our website at www.evermoreglobal.com. Please read it carefully before investing.

Evermore Global Advisors, LLC is the advisor to the Evermore Global Value Fund which is distributed by Quasar Distributors, LLC. Quasar Distributors, LLC is not affiliated with Franklin Templeton

The opinions expressed are those of the author and are subject to change, are not guaranteed and should not be considered investment advice.

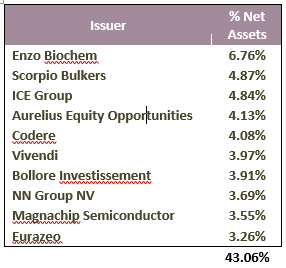

Evermore Global Value Fund – Top Ten Holdings as of June 30, 2017:

Fund holdings and/or sector allocations are subject to change at any time and are not recommendations to buy or sell any security.

FOR REGISTERED PROFESSIONAL USE ONLY – NOT FOR USE WITH THE GENERAL PUBLIC

About The Author: MOI Global Editorial Team

The MOI Global Editorial Team, led by John Mihaljevic, CFA, includes community builders, event organizers, writers, editors, research associates, security analysts, and fanatical member support advocates. Our sole purpose is to serve the members of MOI Global as well as we possibly can in order to help them learn, invest intelligently, and build lifelong friendships with like-minded people.

Who is MOI Global? In recent years, The Manual of Ideas has expanded to become more than simply “the very best investing newsletter on the planet” (Mohnish Pabrai). We are now a thriving global community of intelligent investors, connected through great ideas, thought-provoking interviews, online conferences, live member events, and much more.

Members of MOI Global enjoy complimentary access to a growing array of resources and content related to the art of intelligent investing. Members also enjoy preferential access to selected offline events as well as exclusive access to other events hosted by MOI Global, including the Zurich Project Summit, the Latticework Conference, and Ideaweek.

More posts by MOI Global Editorial Team