This article is authored by Adam Mead of Mead Capital Management.

Many investors restrict the cash flow from their equity investments to the periodic dividends they receive. They are content to let the company’s board of directors decide the payout ratio (how much of current earnings to pay out as a dividend), and trust the remainder to be reinvested back into the business. There is another way, and you might not be surprised to learn that Warren Buffett has weighed in on the topic. The answer: “manufacture” your own dividend, as you see fit, by selling shares. Though perfectly rational, this is easier said than done.

At the tail end of his 2012 annual letter to Berkshire Hathaway shareholders, Warren Buffett laid out his case for why Berkshire’s shareholders were better off with their company not paying a dividend. His rationale was simple: 1. More opportunities for wealth creation were available within Berkshire; 2. Not all shareholders wanted a dividend, and if they did, their preferences for the payout ratio quite likely spanned a wide range; 3. Shares could be sold at a premium to book value; and 4. Selling shares instead of paying a dividend would be more tax efficient for many shareholders.

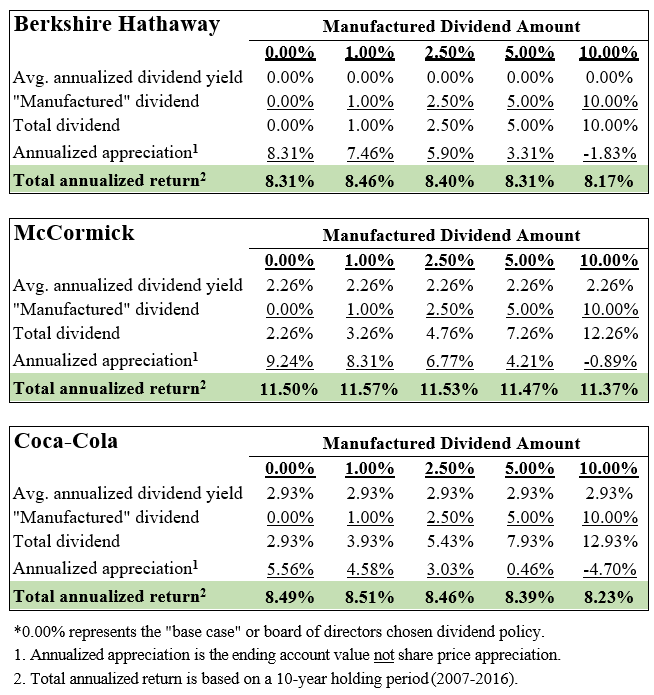

Not content to take Buffett’s word on the matter, I’ve tested his theory on real-world companies, including Berkshire. The result: (not surprisingly) Buffett was correct. You can find some more of the details in the appendix below (I’ve also published my workbook for anyone to examine). In looking at three companies, Berkshire Hathaway, McCormick and Coca-Cola (Berkshire of course paying no dividend and the latter two having traditional payout ratios), the returns from all three under varying payout ratios were strikingly similar. Although their absolute returns varied compared to one another, in looking at each company separately, varying the payout ratio did not meaningfully change the return an investor would have received over a 10-year period. Whether no “manufactured” dividend was chosen as a payout ratio, or 1%, 2.5%, 5%, 10%, or a payout equal to the prior years’ earnings, the pre-tax return to the investor at the end of the period was basically the same.

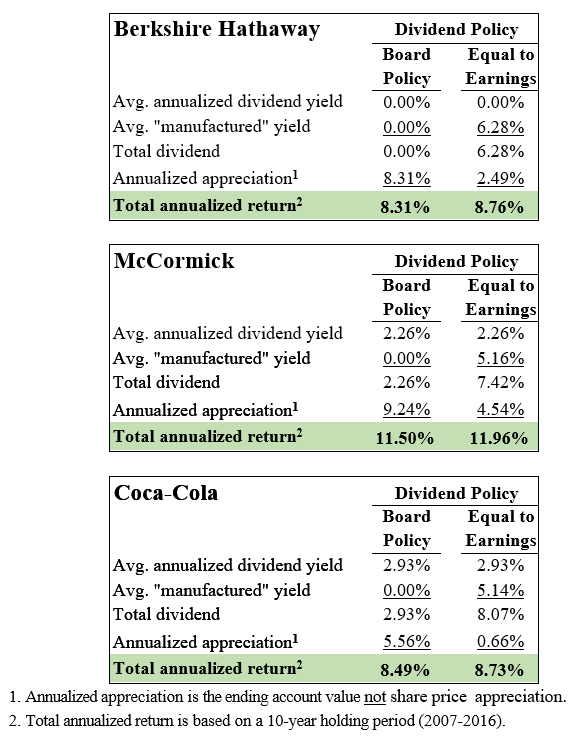

Take Berkshire for example: An investment at year end 2006 would have returned 8.31% for the ten years ended 2016. If instead an investor decided to “manufacture” or sell 2.5% of the prior year’s share price as a dividend the return would have actually increased to 8.40% (with our hypothetical investor benefitting marginally from favorable quirks of timing). How about a 5% manufactured dividend? The return would have coincidentally been the same 8.31% as the no payout ratio scenario. What if the investor chose to sell an amount equal to the prior year’s reported earnings (admittedly not the best figure but an okay proxy in this case)? The return would have been 8.76%. In the other cases I examined, McCormick and Coca-Cola, no matter what payout ratio was chosen the net return varied within 0.59% – almost trivial.*

The only difference in these scenarios, outside of the marginal differences due to timing, is the amount of cash received by the investor. He or she could have spent it or reinvested it into other enterprises. So why don’t more investors choose their own dividend? Probably a combination of psychology, ignorance and inertia.

Psychology – It’s hard to see the share count shrink. Even in the case of a modest 2.50% manufactured dividend for Berkshire an investor would have seen their share count shrink by 20% over ten years. For many this is hard to stomach. Another pitfall is the fact that (most) people aren’t machines. My examples were, for the first part backward-looking, but also formula-based. Most people would have a hard time following a sell-down program without trying to time the market in some way (‘Should I hold off selling in a down market, or try to wait to sell higher?’). But, just as the share price is irrelevant on its own – you need the number of shares outstanding to determine the market capitalization – share count in a portfolio is meaningless in isolation. What matters is the dollar value of the investment, which could go down, remain the same, or increase, all while share count is in a continual state of decline.

Ignorance – This is not questioning investors’ intelligence. Rather, I would venture to guess that most simply don’t know a dividend-on-demand strategy is an option. Yes, many investors sell part of their equity portfolios as part of a re-balancing strategy, or as they shift from stocks to bonds heading into retirement. This type of selling, however, is based on an allocation strategy and (I’d guess) not tied to monetizing the underlying earnings of their investments.

Inertia – Related to ignorance, the board-chosen dividend policy is probably what most investors follow as a default.

Add these up and you get what Charlie Munger calls a “lollapalooza” – a confluence of factors all working in the same direction. That is, against selling off shares to augment board-declared dividends. What is interesting, though certainly not surprising, is that investors regularly do the opposite.

Investors regularly choose to turn a dividend yielding stock into one that pays nothing. How? Through common DRIP, or dividend reinvestment plans. By taking their dividends and using that money to purchase shares, these investors are in effect saying they’d prefer the company retain the earnings for future growth. Yet since they cannot do this they must instead purchase shares from other owners (or newly issued shares from the company). Worse, because of tax implications this positive-yield-to-no-yield is negative! The company pays a dividend, the investor’s share count goes up, and he/she outlays cash to Uncle Sam for the tax bill. Yikes!

In terms of implementing this strategy it would be wise to remember taxes and opportunity cost. In two previous memos (March 2015 & June 2015) I explained the awesome power of deferred taxes. Selling shares to create a dividend goes against this strategy, though that is not to say it isn’t sometimes the best course. Opportunity cost is another major consideration. What will the funds be used for? If they are being ‘recycled’ into the portfolio, is that new opportunity better than the existing investment? Would it be better not to pay taxes on any gains and instead leave your share of earnings in the company to be redeployed by its managers?

Far from simply opining on theory, Buffett, by structuring his annual philanthropic donations as a percentage of his current shares, has demonstrated this sell-off approach works. From the same 2012 Chairman’s Letter:

“For the last seven years, I have annually given away about 4.25% of my Berkshire shares. Through this process, my original position of 712,497,000 B-equivalent shares (split-adjusted) has decreased to 528,525,623 shares. Clearly my ownership percentage of the company has significantly decreased. Yet my investment in the business has actually increased: The book value of my current interest in Berkshire considerably exceeds the book value attributable to my holdings of seven years ago. (The actual figures are $28.2 billion for 2005 and $40.2 billion for 2012.) In other words, I now have far more money working for me at Berkshire even though my ownership of the company has materially decreased. It’s also true that my share of both Berkshire’s intrinsic business value and the company’s normal earning power is far greater than it was in 2005.”

Update: As of the beginning of 2017 when Berkshire filed its proxy statement, Buffett’s B-equivalent share count had declined to 442,760,141 – representing a book value of $48.7 billion and with a market value of over $73 billion. The share count of Buffett’s Berkshire ownership stake declined by 37.9%, yet the value of his stake – despite selling hundreds of millions of shares – rose by about 75%.

All of this leads to an unsurprising conclusion, which is a recurring theme in these memos: An investor should treat public companies just like private businesses. If a larger dividend is desired from any stock in a portfolio, selling shares to “manufacture” a dividend is possible.

It is the mindset that an investor has a claim on the underlying earnings of a business, and therefore should only expect to receive as much in cash, over time, which is powerful. It focuses not only the selection of which companies to purchase, but expectations as well. Owners of private businesses only expect to earn what the underlying enterprise earns; why should owners of public companies expect any different? As Charlie Munger would say, “How could it be otherwise?”.

* For the more academically-minded readers, I admit that the average annualized dividend yield technically does not represent the yield to the investor, which is instead based on purchase price. I also conducted an internal rate of return (IRR) analysis to correct for this minor flaw. The range of returns based on the scenarios listed, including the “EPS dividend”, was -1.26% to +0.56%. While I stopped here, I would venture a guess that the differences were the result of the timing of sales (more favorable or less favorable price/earnings ratios). Given the upward trajectory in asset prices over this period it is not surprising that a higher sell rate would result in a lower IRR, as shares became more expensive on a P/E basis. Please refer to the workbook.

About The Author: Adam Mead

Adam Mead is a life-long student of business and capital allocation. He is the founder of Mead Capital Management, a New Hampshire-based Registered Investment Advisor started in 2014. In addition to managing assets for his clients at Mead Capital, he is also an officer of Pentucket Bank, a $650 million Haverhill, Massachusetts-based mutual bank. As a Commercial Loan Officer / Commercial Loan Portfolio Manager his duties include the origination and servicing of a commercial loan portfolio, and day-to-day credit analysis responsibilities. Adam has been in the banking business since 2008, and has been investing in public securities markets since 2004. Adam has also been the owner of two other small businesses (non-financial) in the past, and grew up in a family of small business owners. Adam holds a Master of Business Administration from Southern New Hampshire University, from which he graduated Summa Cum Laude in 2013. Previously he graduated Summa Cum Laude from Southern New Hampshire University in 2008 with an undergraduate degree in Business Studies and a Minor in Economics. A native of Derry, NH for his entire adult lifetime, he lives in Derry with his wife and infant daughter, and their cat and dog.

More posts by Adam Mead