This post has been excerpted from a letter by Chip Rewey, Lead Portfolio Manager of the Third Avenue Value Fund.

One of the questions we are frequently asked by our clients is how do we see our sector positioning in the markets. Our answer at Third Avenue has always been that we are fundamental bottom up investors and sector agnostic as to where our ideas originate. We look to invest in securities of companies that meet the Third Avenue philosophy of creditworthiness, compounding book value growth and significant price undervaluation. We don’t think the sector index weightings in the indices in any way represent either portfolio construction or risk control guidelines as to how we should invest our fund. The Third Avenue Value Fund has always been an opportunistic and eclectic collection of well-researched investments constructed with the aim of superior long term returns matched with a “balance sheet first” focus on risk control.

However, we do hold long term high conviction beliefs on some sub-sectors of the economy, and as a result, we have high concentration positioning in groups of companies that we believe will collectively outperform over the long term. But, just as we will not invest in companies or industries that we do not find attractive along the Third Avenue philosophy of creditworthiness, compounding book value growth and significant price undervaluation, we will hold concentrated weightings in sectors where we see favorable investment dynamics over the next three to five years.

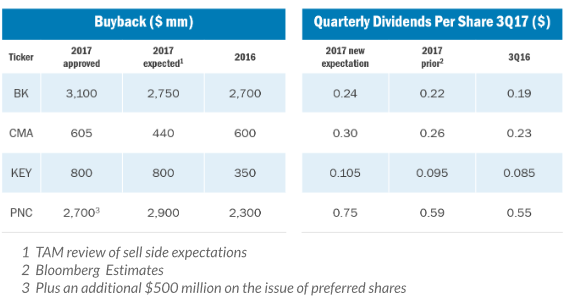

One of the areas of greatest concentration for the Fund over the past three years has been in banks, namely Comerica (CMA), PNC Bank (PNC), Keycorp (KEY) and the trust and processing company, Bank of New York Mellon (BK). Our collective weighting in these four positions on June 30th was approximately 18%. These four banks added 118 basis points of positive attribution to the Fund in the second quarter. Post the worst of the financial crisis and post the institution of programs by the US government to strengthen the financial sector (e.g., Troubled Asset Relief Program or TARP), market sentiment on the banks was very low despite the fact that banks’ balance sheets had been bolstered. They had charged off problem loans and addressed any balance sheet concerns (TARP and equity) — and thus the companies were set up to generate cost saves, build capital, generate loan growth and had asset sensitivity to interest rate hikes.

Under the new post crisis financial regulatory regime, these banks indeed built significant excess capital, far beyond their needs to reserve for tepid loan growth, which in our opinion left them dramatically ‘under-earning’ a normal economic recovery pace. While the profit acceleration of these banks took longer to develop than we initially foresaw, we believe their excess capital position protected our downside risk, effectively allowing us to ‘risk time and not capital’ over our holding period. In fact, we continued to add to our positions on stock market weakness. The late June 2017 results of the Federal Reserve’s capital plan reviews of all these banks allowed a significant step up in share buybacks and dividend increases year-over-year to a level that was higher than still skeptical market expectations.

Beyond the next twelve months’ accelerated share buyback schedule, we see loan growth maturing with the economic cycle, moving away from Commercial Real Estate and growing in areas like consumer mortgage and business lending. Rates paid for deposits remain stubbornly low from a depositor perspective, but are providing an increasing spread for these banks as the Federal Reserve has raised its benchmark lending rate 4 times for 100 basis points off ‘generational lows.’

While this overarching financial theme does apply to many banks, our specific investment thesis on the Fund’s portfolio positions are individually fundamental with strong self-help and potential resource conversion attributes. Comerica is engaged in a significant cost reduction effort termed GEAR-Up, that is targeted to drive down its efficiency ratio and increase earnings even in a flat interest rate environment. PNC Bank, too, is engaged in continuing cost reduction through technology implementation and branch consolidation, while it also has the ‘hidden asset’ of its 21.29% ownership of Blackrock Corp., where the market value of $14.3 billion of this stake is approximately $15.30 per share over the valuation represented in PNC’s March 31, 2017 Book Value of $86.14 and Tangible Book Value of $67.47. Likewise, CEO Beth Mooney of Keycorp in early June indicated the acquisition of First Niagara has been a tremendous success from a cost reduction and geographic expansion perspective, and that while Keycorp will remain vigilant on costs, it is now looking to resume both its organic and M&A driven growth strategies. Finally, Bank of New York Mellon is dramatically reducing costs, which include rapid adoption of “Block Chain” and “Artificial Intelligence” software modules, that should also improve customer service. While these have driven strong returns for the Value Fund, we believe all four companies remain well positioned to drive market leading book value growth over the next three to five years.

Another significant industry weight for the Fund is in the US housing sector, as we have high conviction that the housing market will continue to recover from over a decade of new home ‘starts’ below a sustainable trend line of roughly 1.2-1.4 million units annually. Our housing sector exposure is comprised of Lennar (LEN), Cavco (CVCO), Weyerhaeuser (WY), Masco (MAS), and Canfor (CFP). They represented a combined 15.13% weighting for the Fund on June 30th, 2017 and returned 101 basis points for the second quarter 2017. Our thesis again starts with the Balance Sheets of our owned positions, which are all strong and indeed improving as building activity continues to recover. Housing starts and building permits are continuing their long-term trend of improvement, which should continue as job and wage growth continues broadly as well. Lumber and building product prices have improved with stronger activity, favoring Weyerhaeuser and Canfor, while Cavco, Masco and Lennar have been very successful in passing along higher prices while still driving margin improvement. For the sector as a whole, and more importantly for our portfolio investments, we see these factors continuing and even strengthening over the next few years.

Of course, each of these investments has specific fundamental positives that are more important to our ownership criteria than homebuilding exposure. Lennar continues to de-lever its balance sheet through monetizing its long term land position, and in the second quarter the company completed an important step to show its sum-of-the parts undervaluation with the successful Initial Public Offering of its Five Point Holdings unit. Cavco maintains a strong net cash position of $15.19 per share, and in the quarter acquired Lexington Homes Inc., synergistically expanding its market presence to Mississippi, Louisiana and Alabama. Masco continues to drive strong revenue growth, even against the negative impact of walking away from low margin cabinet sales. Strong sales leverage and the dramatic impact from internal restructuring initiatives has helped Masco post improved margins and raise its long term earnings forecasts. Canfor and Weyerhauser both continue to benefit from higher lumber prices, as trade duties on Canadian Lumber by the U.S. have driven up prices, which greatly benefit the U.S. manufacturing units of both companies. Weyerhauser specifically has unique resource conversion opportunities to monetize its ‘higher and better use lands’, as well as potentially separating out its building products division into a separate company.

We have also written about our “Bull Pen” list of well researched and fundamentally attractive companies that we continue to monitor for a potential opportunity to invest if an appropriate discount to our price target materializes. The Healthcare sector is an area where we have added several new positions over the last two years, including Cerner (CERN), Amgen (AMGN), and Baxalta (which was subsequently acquired by Shire PLC). Along with these positions, we are monitoring several related companies on our “Bull Pen” list as we see the growth in Health Care, which now represents almost one-fifth of all U.S. GDP spending, continuing for the long term.

One new area that we are intrigued with is the rapid emergence of Artificial Intelligence into the economy and the truly revolutionary opportunities its application can have on lowered costs and improved customer service. From our perspective it is a diverse theme that will express itself across all industries, with wide ranging examples from autonomous driving, to improved healthcare diagnostics and patient specific treatments, to phone systems which will have the potential to respond to conversational requests providing an end to frustrating hold times for airlines, banking, cable TV, etc. In our view, this technology will become ubiquitous for all industries, like the internet itself, providing attractive opportunities that are overlooked and outside the large cap technology sector. As we mentioned earlier, Bank of New York has been an early adopter of this technology, i.e. in systems that can recognize simple trade errors like incomplete address or name information and fix them automatically, avoiding human intervention. Almost every company we own should to some extent be able to lower costs and improve service with this embryonic technology. We will continue to search for those that can be disproportionate winners and for which we can invest at attractive prices.

IMPORTANT INFORMATION

This publication does not constitute an offer or solicitation of any transaction in any securities. Any recommendation contained herein may not be suitable for all investors. Information contained in this publication has been obtained from sources we believe to be reliable, but cannot be guaranteed.

The information in this portfolio manager letter represents the opinions of the portfolio manager(s) and is not intended to be a forecast of future events, a guarantee of future results or investment advice. Views expressed are those of the portfolio manager(s) and may differ from those of other portfolio managers or of the firm as a whole. Also, please note that any discussion of the Fund’s holdings, the Fund’s performance, and the portfolio manager(s) views are as of June 30, 2017 (except as otherwise stated), and are subject to change without notice. Certain information contained in this letter constitutes “forward-looking statements,” which can be identified by the use of forward-looking terminology such as “may,” “will,” “should,” “expect,” “anticipate,” “project,” “estimate,” “intend,” “continue” or “believe,” or the negatives thereof (such as “may not,” “should not,” “are not expected to,” etc.) or other variations thereon or comparable terminology. Due to various risks and uncertainties, actual events or results or the actual performance of any fund may differ materially from those reflected or contemplated in any such forward-looking statement. Current performance results may be lower or higher than performance numbers quoted in certain letters to shareholders.

Date of first use of portfolio manager commentary: July 17, 2017

Past performance is no guarantee of future results; returns include reinvestment of all distributions. The above represents past performance and current performance may be lower or higher than performance quoted above. Investment return and principal value fluctuate so that an investor’s shares, when redeemed, may be worth more or less than the original cost. For the most recent month-end performance, please visit the Fund’s website at www.thirdave.com. The gross expense ratio for the fund’s institutional and investor share classes is 1.40% and 1.65%, respectively, as of March 1, 2017. Please be aware that foreign securities from a particular country may be subject to currency fluctuations and controls, or adverse political, social, economic or other developments that are unique to that particular country or region. Therefore, the prices of foreign securities in particular countries or regions may, at times, move in a different direction than those of U.S. securities. Prospectuses contain more complete information on management fees, distribution charges, and other expenses.

Third Avenue Funds are offered by prospectus only. The prospectus contains important information, including investment objectives, risks, advisory fees and expenses. Please read the prospectus carefully before investing in the Funds. Investment return and principal value fluctuate so that an investor’s shares, when redeemed, may be worth more or less than the original cost. For updated information or a copy of our prospectus, please call 1-800-443-1021 or go to our web site at www.thirdave.com. Distributor of Third Avenue Funds: Foreside Fund Services, LLC.

Current performance results may be lower or higher than performance numbers quoted in certain letters to shareholders.

About The Author: Chip Rewey

Mr. Rewey is the leader of Third Avenue’s Value and Small-Cap Teams, serving as the Lead Portfolio Manager for the Third Avenue Value and Small-Cap Funds. Mr. Rewey joined Third Avenue Management in 2014.

Before he joined Third Avenue, Mr. Rewey spent more than ten years at Cramer Rosenthal McGlynn, LLC as a Senior Vice President and Senior Portfolio Manager where he oversaw the firm’s smid, mid, large and all cap investment strategies. Prior to Cramer Rosenthal McGlynn, Mr. Rewey was a Senior Portfolio Manager at Sloate Weissman Murray & Company, where he worked directly with the Founder on research and portfolio construction. Mr. Rewey began his career as an Acquisitions Analyst for Associates Corporation of North America before moving on to roles at Oak Value Capital Management and Smith Barney, Inc.

Mr. Rewey earned an M.B.A. in Finance from Duke University Fuqua School of Business and holds a B.S. in Finance from Boston College, graduating Magna Cum Laude. He is a member of the New York Society of Security Analysts.

More posts by Chip Rewey