This article is authored by MOI Global instructor Jim Roumell, president of Roumell Asset Management, based in Chevy Chase.

Dundee’s DPM investment equals total enterprise value – free option on everything else

- The company has dramatically reduced corporate overhead, employees and its number of investments in the past two years

- Dundee’s primary asset – its 20% ownership interest in Dundee Precious Metals (DPM) – is trading at 7.5x our 2020 FCF estimate and is poised to initiate a dividend in 2020

- Jonathan Goodman is executing on the vision articulated two years ago – monetize, simplify, and pivot

Investment Thesis: Large margin of safety to a conservative case NAV in a SOTP analysis. Today, Dundee is a principally a passive investor in a slimmed down portfolio with interesting core assets, anchored by its 20% ownership in publicly-traded Dundee Precious Metals (DPM), the value of which now equals Dundee’s total enterprise value. The company has no real capital commitments going forward as a result of monetization and restructuring events, executed over the past few years. Moreover, Dundee is in front of more monetization events, and likely share buybacks given the company’s deep commitment to deliver value to shareholders after several years of destroying capital (under previous management regimes), in our opinion.

Dundee has no funded debt, and its leverage is solely through the use of perpetual preferred stock that has no maturity date, allowing it to control a significant number of assets with the benefit of a permanent capital structure. Dundee enjoys the benefits of leverage without the typical risks, i.e. refinancing.

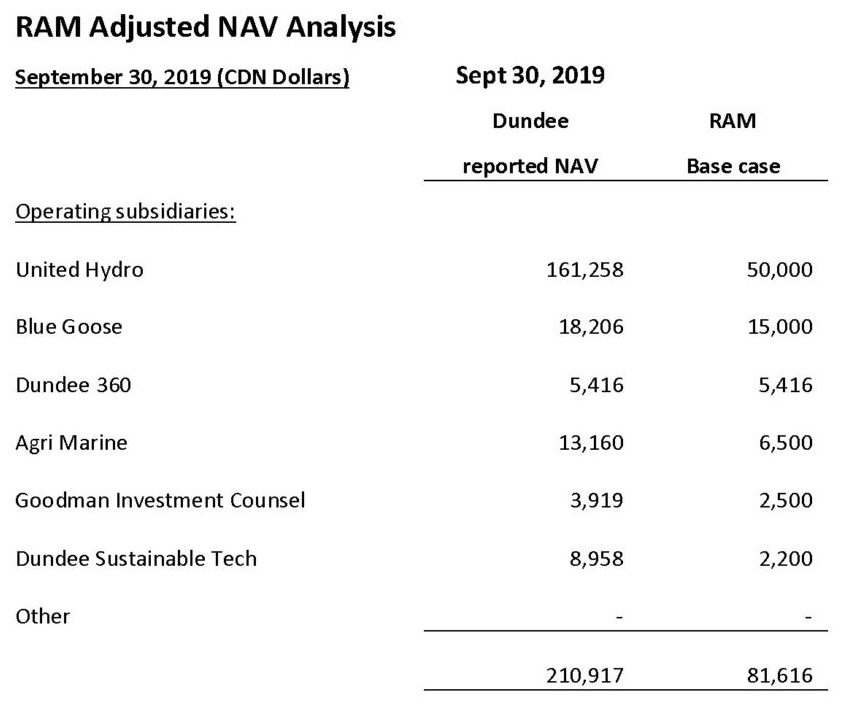

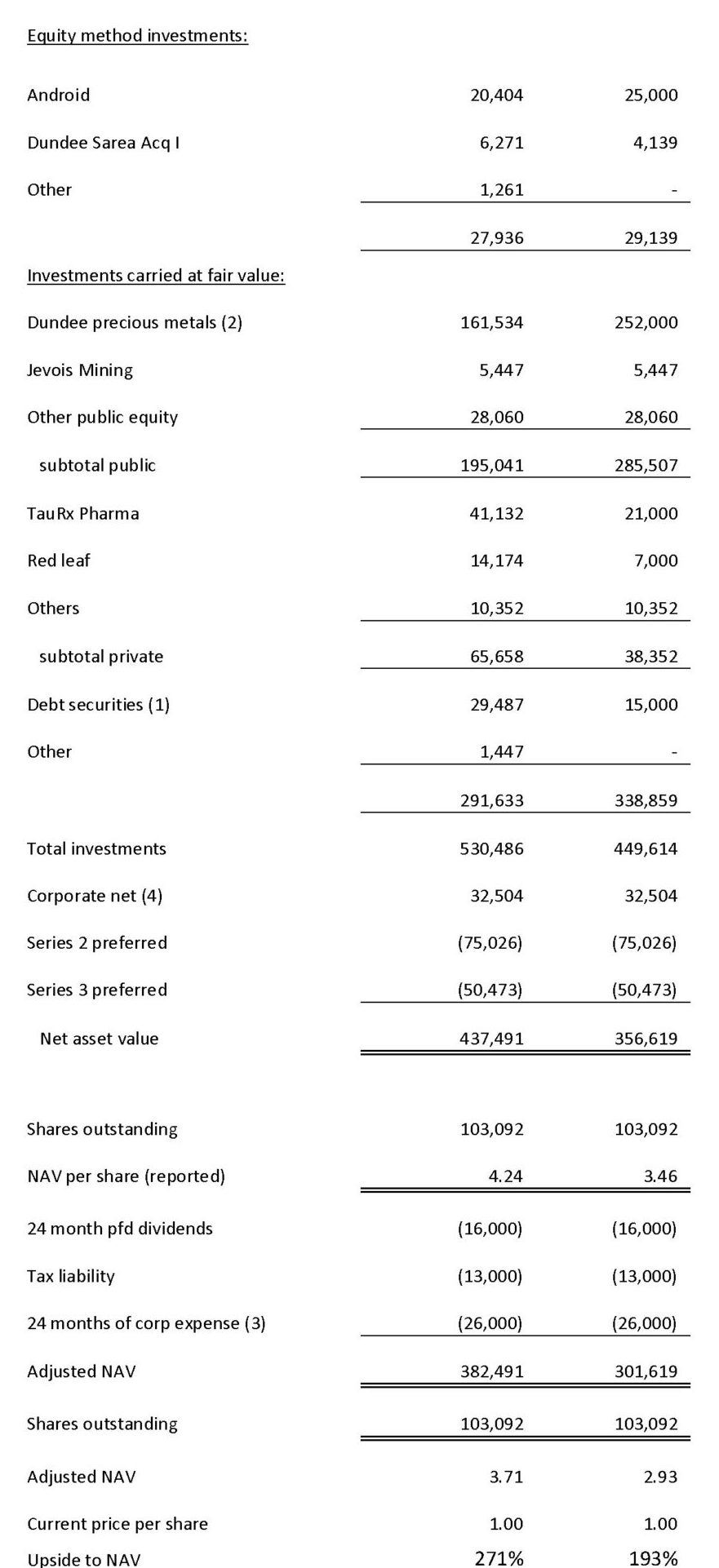

We wrote-up Dundee in April 2018 at $1.63/share (we were early). We have steadily accumulated shares over the past two years and now own roughly 5% of the company’s outstanding A shares. See end of write-up for summary analysis of NAV. All amounts in this report are in Canadian dollars, unless specifically stated otherwise.

| Company NAV | $4.24 |

| RAM Adjusted NAV | $2.93 |

| Price | $1.00 |

| Upside to RAM NAV | 193% |

BLUF (bottom line up front): Dundee Precious Metals (DPM) stake equals the company’s enterprise value providing a free option on everything else in the portfolio:

| Outstanding shares: | 103 million |

| Price: | $1.00 |

| Market Capitalization: | $103 million |

| Preferred Shares: | $125 million |

| Cash: | $19 million ($32 million less $13 million tax liability) |

| Enterprise Value: | $209 million |

Dundee Precious Metals (DPM) Shares owned by Dundee: 36 million

Value @ current price of $5.80: $209 million

DPM Value @ $7/share: $252 million

Conclusion: Our calculation of Dundee Precious Metals’ value exceeds the total enterprise value of Dundee Corporation by over $40 million, or $0.40 per share. Thus, in our opinion, Dundee shareholders have access to all of the company’s other assets for free.

Business Overview and Background

Dundee is a Canadian holding company that owns a portfolio of operating subsidiaries, public investment securities and investments in private enterprises. Ned Goodman, the founder, stepped down in 2014 and one of his sons, David Goodman, took the helm as CEO. In 2011, Ned took a view that there would be hyper-inflation, so he decided to invest heavily in commodity businesses. Many of those investments have since been written-off or significantly written-down, resulting in the destruction of significant shareholder value. The Goodmans own roughly 17% of Dundee Corp and have never sold shares. The Goodman family controls Dundee through a dual class voting share structure. There are 100 million Class A shares that each get one vote. There are 3.1 million Class B shares (Goodman shares) that each get 100 votes.

Jonathan Goodman, another son of Ned’s, was appointed Chairman and CEO in early 2018. Jonathan left the company four years prior, partially in protest to the capital allocation decisions being made at that time. He set out a clear vision upon returning to Dundee Corp.: dramatically reduce the number of investments the company holds by monetizing non-core assets, reduce headcount by two-thirds, settle the company’s Series 5 preferreds due in June of 2019, and position the company as a Canadian resource-focused investor. To wit, the company has reduced its investments from 90 two years ago to roughly 30 today, settled the Series 5 preferred stock by exercising the company’s right to settle it in common stock, and has taken headcount down from 70 to 30 people. The company’s annual G&A expenses were roughly $30 million at the time Jonathan took over as CEO and are now estimated to be at a go-forward run rate of about $12 million. In the first 9 months of 2019, G&A was down to $16.8 from $23.1 million during the same period of the prior year.

The company’s objective to create a portfolio of passive investments, requiring no on-going capital commitments from Dundee, has largely been accomplished. The company’s “strategic pivot” is toward becoming a Canadian resource investor by taking advantage of the bear market in Canadian junior minors in three different ways – through direct investments, as an asset manager, and as a banker in the sector. Dundee’s pivot is in line with Jonathan’s background as a mining investor who oversaw Dundee Precious Metals as its President and CEO from 1995 to 2013. Today, DPM is poised to reap the rewards of acquisitions made during Jonathan’s tenure. DPM’s market cap is roughly $1.05 billion and is effectively unlevered taking into account the company’s cash and its ownership in publicly traded Sabina Gold & Silver (“SBB-T”). DPM is expected to generate over $100 million in FCF in 2020 as a result of its second Bulgarian mine – Ada Tepe – going into production earlier this year.

Importantly, earlier this year Dundee put its employee stock purchase plan back in place after suspending it three years ago. Employees can now elect to receive up to 10% of their salary in stock. All senior management elected to participate at the full 10% level and well over half of all employees chose to participate. Dundee’s culture is one of long-standing employee relationships, so we don’t believe the company would have turned this program back on without a high degree of confidence in its future. Bob Sellars, CFO, elected to take 100% of his 2018 bonus in stock (at a price of $1.20), i.e., 20% above today’s price.

We believe the company has signaled that it expects 2020 to be the year that much of the past two years’ hard work starts to pay off.

Balance Sheet/Capital Structure

Dundee has a permanent capital base. Earlier this year, the company exercised its option to convert its Series 5 preferred to stock. The company now only has preferred Series 2 and 3 (totaling $125 million at roughly 6%), both of which are perpetual and trading at about $15/share vs. par of $25/share. The company has begun to opportunistically buyback preferred shares, which immediately increases NAV on a per share basis (eliminating a $25 liability for every $15 spent) and reduces interest expenses.

Buying back common stock would also be hugely accretive to NAV.

“As part of our ongoing strategy to optimize our capital structure, we initiated a normal course issuer bid for the Corporation’s Preference Shares, series 2 and series 3, during the third quarter,” said Jonathan Goodman, Chairman and CEO. “Additionally, we are considering the implementation of a normal course issuer bid for the Corporation’s Class A subordinate voting shares, subject to the approval of the Toronto Stock Exchange. We believe this could be a prudent use of capital and will provide us with additional strategic flexibility.”

The following table summarizes the net accretion to NAV per share under four buyback scenarios. The preferred stock buyback scenarios include three years of dividend savings on the repurchased preferred stock. The below analysis assumes the $15 million common stock buyback occurs at $1.05 (5% above the current market price) and the $30 million common stock buyback occurs at $1.20 (20% above the current market price).

| Accretion $15 mm common buyback | 12% |

| Accretion $30 mm common buyback | 22% |

| Accretion $15 mm Pfd buyback (w/3 yr. div save) | 3.0% |

| Accretion $30 mm Pfd buyback (w/3 yr. div save) | 6.0% |

The repurchase of common shares would create substantial value for common shareholders of Dundee Corporation and is far superior to purchasing preferred shares.

In summary:

- The $15 million and $30 million buyback scenarios of common stock repurchases create NAV accretion of 12% and 22%, respectively.

- Purchasing preferred shares of the same amounts only creates 3% and 6% accretion, respectively (after factoring in three years of dividend savings).

Primary Assets

1. Dundee Precious Metals, DPM. Dundee Corp owns 20% of publicly traded DPM, or 36 million shares. DPM is an unlevered mining company with two producing assets in Bulgaria (a NATO nation). DPM is supported by its own smelter in Tsumeb, Namibia (92% owned). DPM has invested $350 million into Tsumeb over the past ten years after acquiring it for $33 million in 2010. DPM considers Tsumeb to be non-core and has indicated its willingness to sell the asset under the right conditions, i.e., maintaining a long-term contract for processing its own ore.

DPM’s Ada Tepe mine in Bulgaria went into production in June 2019 and is expected to produce 103K ounces of gold annually in its first five years of production. The company’s Chelopech mine, also in Bulgaria, produces 200K ounces of gold annually. It has an estimated eight years of remaining mine life and will bring total annual production to roughly 300K ounces per year with an all-in-cost of roughly $750/oz. At current spot gold of about $1,450, that’s $700/oz multiplied by 300K ounces, or $210 million of gross income. There is an opportunity and focus on extending the Chelopech and Ada Tepe mines. There is 8 years of reserves and strong potential for approximately 4-5 years of additional reserves, according to the company. Note, Bulgaria is a European Union member, and a stable democracy.

DPM’s estimated annual FCF for 2020, extending out five years, is estimated to be between $125 to $150 million. Refer to the company’s current presentation at https://s21.q4cdn.com/589145389/files/doc_presentations/2019/Investor-Presentation.Denver_long_FINAL_website.pdf. Note, roughly $10 to $15 million of growth cap-ex needs to be subtracted from these numbers for a “true” FCF number. Thus, DPM stands in front of a dramatic FCF growth story, which is not being fully appreciated in the marketplace, in our opinion.

DPM has stated its intention to introduce a dividend and/or buyback in 2020. DPM currently trades at roughly $5.50/share; we value it at $7.00/share (See DPM analysis below). Canaccord Genuity issued a C$8.50 price target December 2nd, and stated the following:

“Substantial FCF on the horizon: With Ada Tepe now built and ramped up, DPM is expected to generate substantial FCF from 2020 onward given ~50% overall AISC margins. We forecast a 20% FCF yield for 2020 based on the current share price, with similar yields for 2021 and 2022, and we note that DPM offers the highest FCF yield in our mid-cap precious metals coverage universe. We discuss the company’s capital allocation criteria in the body of the report, but note here that we believe management is likely to initiate some form of shareholder return program in 2020 (or earlier).”

Paradigm Capital’s target price is C$6/share and M Partners’ target price is C$7.50; neither of these firms assign a separate value for DPM’s smelter. Given the company’s new production profile post-Ada Tepe, we believe DPM will undergo a significant rerating valuation by going from a junior miner to a mid-tier rated miner.

DPM Intrinsic Value:

1. Production Value: $1.150 billion. We put a conservative cap rate of 10% on estimated $115 million in 2020 FCF (this number is after growth cap-ex and FCF related to the Tsumeb smelter). Using an 8% cap rate would take production value to $1.440, and DPM’s intrinsic value to $8.75, from our more conservative calculation of $7/share, noted below.

2. Tsumeb Smelter: We value Tsumeb at roughly 33% of the estimated $400 million of sunk cost ($50 million purchase and $350 million in cap-ex), much of which was needed to meet regulations that went into effect after DPM purchased it. While the smelter currently only generates roughly $10 million in EBITDA, CFO Hume Kyle walked us through the effects of a modest capital expansion which would meaningfully increase EBITDA because 80% of smelter costs are fixed. For example, a $30 to $50 million investment would likely increase EBITDA by $20 to $30 million, according to Mr. Kyle. Tsumeb is a highly sophisticated smelter capable of processing highly arsenic grade ore. $400 million times 33% times 92% ownership = $121 million.

3. Cash/Investments: $56 million (DPM owns 10% of publicly-traded Sabina Gold & Silver)

4. Debt: $41 million

5. Sum: $1.286 billion

6. Per Share Value: $7.15

If DPM institutes a 2% dividend in 2020 (based on its current price), it would result in a $3.3 million annual dividend to Dundee Corp., or roughly 25% of Dundee’s stated on-going corporate overhead costs of $12/$13 million per year. Moreover, whatever combination of dividend and/or buyback DPM puts in place, it is likely to be well-received by the market, thus increasing Dundee’s stated NAV. Dundee Corp. Chairman and CEO Jonathan Goodman is the Chairman of the Board of DPM.

2. United Hydrocarbon International Corp. United Hydrocarbon International Corp. (UHIC) is a privately-held Canadian junior exploration company that is focused on seeking opportunities internationally, both directly and indirectly, for the exploration, development and production of oil and natural gas. At September 30, 2019, Dundee Corp.’s carrying value of its 83% interest in UHIC was $158.6 million. Dundee originally invested $357 million in this investment (despite the objection of current CEO Jonathan Goodman, who left the company shortly thereafter).

UHIC’s assets are in Chad. According to the U.S. Energy Information Agency, slightly over 25% of Chad’s GDP and over 60% of the government’s revenues come from oil production, making the country dependent on the oil industry. Exxon has a large presence in the country. There is also a significant Chinese presence (producing wells) on acreage adjacent to UHIC’s properties. In May 2017, Dundee converted its equity into a royalty (with no further capital commitments). UHIC’s production sharing contract (PSC), was renewed in 2017:

- US$20M upon UHCL achieving commercial production at Doba Basin

- US$30M upon UHCL achieving commercial production at Block H

- 10% royalty on specified cash flows to UHCL from Doba production

- 5% royalty on specified cash flows to UHCL from Block H production

“The royalties are payable when the average quarterly price of Brent crude oil is greater than US$45.00/bbl. Under the terms of the share purchase agreement, dated May 10, 2017, UHCL’s owner, Delonex Energy Limited (“Delonex”), committed to a US$65 million comprehensive exploration program for the assets in Chad and a further US$35 million investment in the Doba Basin should commerciality be achieved during the remaining life of the PSC.” http://dundeecorp.com/pdf/2017-05-10-UHIC-Delonex-Agr.pdf

In its 2019 earnings announcement, Dundee provided a positive update on its UHIC investment. Dundee noted that after having spent the required US$65 million on initial development work, Delonex decided to move forward in 2020 with Phase 2 – shooting 2D and 3D seismic to identify drilling prospects. It is anticipated that by year-end 2020, or shortly thereafter, a full resource analysis will be completed showing proven and probable resource data. At that time, Dundee has indicated it will entertain monetizing its royalty interest (Dundee has no capital commitment requirements) at an appropriate price to either Delonex (who has first right of refusal) or an outside third-party royalty buyer.

Dundee’s partner, Delonex Energy, is backed by Warburg Pincus, who invested $600 million into Delonex in 2013. https://www.livemint.com/Companies/xPKfrVC3LSg7Fvx92A5tpK/Delonex-Energy-raises-600-mln-led-by-Warburg-Pincus.html. Warburg’s investment was no doubt related to its faith in one of its own, CEO Rahul Dhir. Given the importance of this investment to our Dundee investment, it’s worth highlighting his background:

Rahul is the founder and Chief Executive Officer of Delonex Energy. He was previously Executive-In-Residence at Warburg Pincus LLC, a leading private equity firm focused on growth investing.

With nearly 30 years of experience in natural resources across technology, finance and business leadership, Rahul served as the Chief Executive Officer and Managing Director of Cairn India from August 2006 to August 2012. Under his leadership, the Company grew to a market value of nearly USD 13 billion, with operated production of over 200,000 barrels of oil per day and a world-class resource base, with interests in nine blocks in India and one in Sri Lanka.

Rahul is a Distinguished Member of the Society of Petroleum Engineers. He holds a B. Tech in Chemical Engineering from IIT Delhi, an MS in Petroleum Engineering from the University of Texas at Austin, and an MBA from Wharton Business School at the University of Pennsylvania.

In an effort to be conservative and account for energy development risks, RAM carries Dundee’s UHIC investment at $50 million, or roughly one-third of the company’s carrying value. As Delonex gets closer to going into production, Dundee will consider monetizing its royalty interest and has even had very preliminary discussions on the topic, according to our sources.

3. TauRx Pharmaceuticals Ltd. TauRx is a private neuroscience company focused on the discovery, development and commercialization of products for the diagnosis and treatment of Alzheimer’s disease (“AD”). The business was established in 2002 with the aim of discovering treatment and diagnosis of AD characterized by abnormal aggregation of the Tau protein within the brain. Dundee determined that the fair value of its investment in TauRx at March 31, 2018 was $40.1 million (which gives TauRx a total valuation of $1 billion). In determining the fair value, Dundee applied a value per share of US$30.60, the equivalent of a 50% discount to the volume-weighted average price of shares issued during 2015 and 2016.

We believe TauRx is in the process of raising capital at a price that may be above Dundee’s carrying value. Dundee owns roughly 4% of TauRx and is carried at $40.1 million by Dundee as noted above. Dundee has made clear that it views TauRx as a non-core asset and will look to a TauRx capital raise as an opportunity to monetize its 4% interest, if available on acceptable terms. Nonetheless, in an effort to be conservative and account for drug development risk, we discount TauRx by 50% and carry it at $20 million. In fact, our 50% discount is on top of Dundee’s 50% discount:

“At September 30, 2019, the Corporation held an approximate 4% interest in TauRx. The Corporation has determined that the fair value of its investment at September 30, 2019 was $41.1 million. In determining the fair value of its interest, the Corporation applied a value per share of US$30.60, the equivalent of a 50% discount to the volume-weighted average price of shares issued from treasury during 2015 and 2016.”

To be clear, we do not view TauRx as a binary investment. Because the tau protein appears to be a long-term “platform-type” molecule, if current trials fail, it’s likely that new trials will be designed and developed given the long-term prospects, and upside, to tau molecule research.

The tau protein offers a wholly new, and thus far, promising pathway to creating a drug to treat Alzheimer’s disease. Prior development efforts have focused exclusively on amyloid plague therapy. https://pubs.acs.org/doi/abs/10.1021/acsomega.9b00692

In June of 2019, TauRx was the recipient of Frost & Sullivan’s 2019 Asia Pacific Neurodegenerative Disease Management Technology Innovation Award https://taurx.com/uploads/press%20releases/FS%20Award%20Press%20Release.pdf

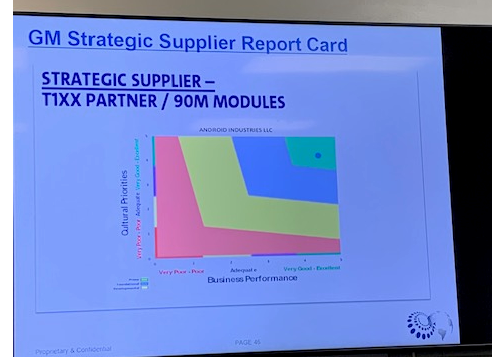

4. Android Industries (AI). Dundee owns 20%. Android is a privately owned, significant and growing Value-Added Assembler (VAA) manufacturing partner to General Motors (“GM”) and, to a lesser extent, Fiat and Ford. In 2020, GM is expected to account for roughly 70% of company revenue as a result of the major new TX11 contract; Fiat accounts for roughly 20% and Ford accounts for roughly 10% of revenue. The company has 25 plants (average plant size about 225K sq ft), and generated about $225 million in revenue in 2018. According to the company, the TX11 contract represents the largest VAA award in GM history. The TX11 truck platform will add roughly $100 million in additional annual revenue to Android. The contract is expected to be at a normalized run-rate by mid-2020.

We toured AI’s Flint, MI plant in late October and witnessed first-hand how the TX11 contract is a game-changer for Android. In the past 8 months, the company has hired 300 people at its Flint plant, bringing its workforce there to 450 people. Mary Barra, GM’s CEO, is using Android as an example of the type of high-quality partner it is looking to partner with going forward to drive down its own costs. AI is now a slide (see below) in GM CEO Mary Barra’s corporate presentation. The vertical axis shows “Cultural Priorities” and the horizontal one shows “Business Performance”. AI is the asterisk in the top right highlighting its high score on both measurements.

Android’s all-in cost per employee is roughly $30/hr vs GM’s $65/hr labor cost structure. The company’s GM contract is a very attractive fixed plus variable cost structure, which insures steady revenue from GM. In fact, AI was not hurt during GM’s recent strike as its fixed-cost retainer payment was received un-interrupted during the strike.

Dundee values its AI investment on an EBITDA multiple basis. The investment was marked down in 2019 vs 2018 because of some one-time issues associated with legal costs (it recently won a suit against Fiat and is expecting reimbursement of legal expenses in the 4th quarter) and a slowdown in Fiat Jeep sales. Despite the suit, Fiat and AI are now in negotiations. The company is confident it can structure an attractive fixed plus variable cost structure contract, similar to the GM one. Evidently, AI provides a unique mix of capabilities. For instance, according to the company, it has the widest suite of auto sub-assembly capabilities in the U.S. We witnessed the company’s machinery place tires onto wheels and assemble complete transmission packages that are delivered “just in time” to GM assembly plants, i.e., within two hours of final car assembly.

Dundee’s current AI valuation is $20 million, down from a $25 million valuation a year ago despite the game-changing TX11 contract win because of its strict adherence to an EBITDA multiple valuation methodology. We use a $25 million valuation (more likely higher, in our opinion, post-TX11) based on our confidence in EBITDA growth in 2020 and our belief that Android is well-positioned going forward.

Kathy Nichols, AI’s CEO, is the founder’s daughter and has articulated a clear vision that Android is a growth company. Earlier this year, GM awarded AI with its Supplier of the Year award for the second year in a row (20,000 suppliers, only 133 awardees). https://www.android-ind.com/android-recognized-gm-supplier-year/

5. Blue Goose. Blue Goose is a private Canadian company focused on the production, distribution and sale of organic, and conventional beef, chicken and fish. Blue Goose is currently carried at roughly $15 million and the company is in active discussions to sell this property to a rancher owning adjacent property. The discussion with this individual has been on-going for several months and there can be no assurance a deal will be struck. In its 3rd quarter release, Dundee marked Blue Goose down to $70 million (there’s $55 million of debt on the property) from $80 million given the nature (and price) of current negotiations. Interestingly, as a result of cost-cutting, Blue Goose showed positive EBITDA in the most recent quarter. We handicap the probability of a sale by the end of January 2020 at 70%.

Honorable Mentions:

1. Parq Hotel and Casino. This investment has been a real loser for Dundee and has taken up an inordinate amount of time in the past two years. In short, roughly $125 million was invested (primarily in preferred shares) and today the investment is given no value except for a $6 million note. However, Dundee now owns 23% of the equity in Parq, and provides investors a free call option on a very well-situated property now in the hands of a first-rate hotel operator. Dundee has no capital commitments for its Parq investment.

The property’s $550 million in debt was refinanced earlier this year with Westmont Hospitality Group now operating the property as the majority equity owner. The refinancing was done on relatively attractive terms: $300 million 1st lien note at 5%; $250 million 2nd lien note at 5% cash interest and 11% PIK interest. Westmont put up the 2nd lien capital. The property’s cost to build was $900 million. Westmont is a well-respected, privately owned, Vancouver-based large hotel operator with a long-term vision and commitment to the property. Westmont is the primary equity owner. https://www.whg.com/

We visited the Parq Hotel and Casino in the summer of 2018. It’s a fabulous property with two Marriott hotels (over 500 rooms): JW Marriott and DOUGLAS (An Autograph Collection Hotel). The property also boasts five separate restaurants, convention space, a spa and a large parking facility. The Parq Casino is the only casino in downtown Vancouver and sits right next to the Canucks arena. Mercer ranks Vancouver the third best city in the world for “quality of living”. We believe Parq has a bright future despite initial opening missteps and a British Columbia money laundering law that has hampered its casino operations (while being overly leveraged). Moreover, we believe Dundee’s 23% equity interest will grow into real value even though we subscribe no value to it today.

The expectation has always been that the Parq, once operating as a “mature” property, will generate $75 to $100 million in EBITDA. High-end downtown Vancouver hotels (without casinos), have traded at $1,000/key. If Parq is able to get to $100 million in EBITDA at the end of five years, capped at 10x, equals $1 billion. Less $650 million debt (inclusive of 5 years of PIK interest), that leaves $350 million in equity value, multiplied by 23%, equals a potential value of $80 million.

2. Red Leaf. Red Leaf is a privately held oil and gas technology company. Red Leaf’s patented technology, EcoShale, is a next generation oil and gas recovery technology focused on unlocking oil reserves in oil shale deposits. Dundee is a preferred share owner and is seeking to be taken out at par value. Another preferred shareholder sued Red Leaf demanding to be liquidated and the case is set to go to trial in December 2019. We are assigning a 50% probability to the suit going our way this December, and thus assign a value of $7 million to this asset.

3. Agrimarine. Agrimarine describes itself thus, “The world’s leading developer of Floating Container Systems for Sustainable Fish Rearing.” According to Dundee, after suffering steady losses for the past two years, Dundee’s $1 million investment earlier this year appears to have allowed Agrimarine to become cash flow positive by fourth quarter 2019 or first quarter 2020. Agrimarine purchased automated fish feeders that have dramatically reduced the company’s op-ex. We carry Agrimarine at 50% of the company’s carrying value of $13 million, i.e., $6.5 million. We experienced Agrimarine’s excellent salmon first hand at Toronto’s Cactus Club.

4. Jervois Mining Limited. In July 2019, eCobalt merged with Jervois (ticker: JRV-V/JRVMF). Dundee’s Jervois shares are valued at $5.5 million. eCobalt’s primary asset is the Idaho Cobalt Operations. The Company’s Idaho Cobalt Project (ICO), located in East Central Idaho in the historic Idaho Cobalt Belt, is the only near-term, environmentally permitted, primary cobalt project in the United States. This asset is viewed as particularly attractive given the rising interest in clean cobalt to meet the world’s increasing need for this mineral as a key component to batteries found in electric cars. Most of the world’s cobalt is mined in the Congo where working conditions have continued to attract worldwide condemnation.

Cobalt is listed as one of the 35 minerals that the U.S. Department of Interior considers critical to U.S. national security and its economy. https://www.doi.gov/pressreleases/interior-seeks-public-comment-draft-list-35-minerals-deemed-critical-us-national

The ICO is a high-grade cobalt-copper deposit and a partially completed mine site and mill located in Lemhi County outside the town of Salmon, Idaho. Significant pre-works have been undertaken at site, with approximately US$100 million invested thus far. Jervois’s entire market cap is now roughly US$83 million. Jervois is an Australian based company with three other projects in addition to ICO.

The Strategic Pivot

Jonathan is a graduate of the Colorado School of Mines and holds an MBA from the University of Toronto. From his company biography: “Jonathan Goodman has over 30 years mining investment and operating experience. He has worked as a geologist, senior analyst, portfolio manager and senior executive, operating a mining company, leading a mining-focused investment banking group, and building extensive knowledge and relationships in the global mining resource and finance sectors over a distinguished career. Jonathan held the role of Executive Chairman of Dundee Precious Metals (DPM-T) from April 2013 to September 2017, at which time he was appointed Chairman, and was its CEO from 1995 until 2013.”

The junior mining sector in Canada is in a bear market. Cannabis companies raised $4 billion in 2018 as compared to only $217 million by mining companies, according to data from the Canadian Securities Exchange. Kai Hoffmann, chief executive of Oreninc, noted that many companies may run out of cash soon. “We might see a cash crunch by the end of the year…Maybe some of these companies will disappear” said Hoffmann.

Canada’s cannabis industry has been sucking out capital leaving the junior mining industry without access to traditional capital sources. https://www.mining.com/cannabis-fad-mows-canadas-junior-mining-sector/. Dundee hopes to take advantage of this capital starved industry by buying in at what it believes are super-cheap prices. It’s a three-pronged approach to serve the industry: direct investments, asset management and banking. The aforementioned activities will all occur under the Dundee Goodman Merchant Partners division of Dundee.

Dundee’s largest outside shareholder, Polar Asset Management, has been steadily accumulating shares in Dundee over the past two years (as has RAM) and now owns 13% of the company. Polar is a highly-regarded hedge fund firm (Canada’s largest and oldest) and manages roughly $4 billion. We met with Polar earlier this year in its Toronto offices and were impressed by the depth of their team’s asset-specific knowledge of the current portfolio and their long-term commitment to Dundee’s vision.

Led by Jonathan Goodman, CEO, and Bob Sellars, CFO, Dundee Corp. has been executing on its plan articulated in March 2018 to monetize, monetize, monetize and focus on core competencies as a resource investor. We’ve come to know and trust Jonathan and Bob over the past 18 months and have visited with the company twice in Toronto during that period. They are all-in and accumulating shares alongside their employees. We have found both Jonathan and Bob to be transparent, non-promotional, hard-working and dogged in pursuing the company’s reinvention. We describe Dundee as a “reverse prodigal son” story because in this instance, the son returned to clean up many of the father’s messes.

While other investors have given up, we have welcomed the opportunity to buy into the company’s shares after suffering from extreme investor fatigue and outright capitulation. It’s the way we pursue value – out of favor, overlooked and misunderstood investment situations. No doubt, we were early to the story, as is often the case.

While Dundee’s stock has stayed moribund in the past twelve months, in reality, much has been accomplished and remains unappreciated. The investment set-up is very attractive, in our opinion. The next 12 months is when the story should really come into focus for investors as:

- DPM begins to generate significant FCF and institutes a dividend and/or buyback

- Dundee Corp.’s operating expense reductions come into full view

- Delonex’s drilling program clarifies United Hydrocarbon’s resource value

- Android is rerated as EBITDA rises from its TX11 contract with GM

- Blue Goose and/or TauRx is monetized allowing for meaningful Dundee share buybacks

Dundee Corp. has accomplished much since Jonathan Goodman became its CEO in early 2018. In our opinion, Dundee is super cheap, and possesses multiple shots on goal, making the upside/downside profile highly attractive, for patient long-term investors.

Roumell TipRanks rating: https://www.tipranks.com/bloggers/jim-roumell

(1) includes the Parq loan for $5.9 million and Eight Capital for $13.7 million.

(2) Dundee Corp own 36.382 million shares of DPM at Sept 30, 2019 ($4.44 per share)

(3) Corp expenses assume $13 million/year (company ’20 guidance is $12 million).

(4) Primarily corporate cash

About The Author: Jim Roumell

Jim Roumell entered the securities industry in 1986. Before founding the firm in 1998, he was a Registered Principal at Raymond James Financial Services, Inc. Mr. Roumell is a frequent contributor to Manual of Ideas Global and has been featured in such publications as Barron’s, Kiplinger’s, Value Investor Insight, Financial Planning Magazine, and The Washington Post. He is listed and quoted in “The Art of Value Investing: How the World’s Best Investors Beat the Market.” Mr. Roumell was selected to participate in, and won, two consecutive Wall Street Journal stock picking contests in 2001 and 2002. He is a Board Member and Chairman of the Investment Committee of Wayne State University Foundation. He is also a Board Member and serves on the Investment Committee of Amalgamated Casualty Insurance Company. Mr. Roumell is a graduate of Wayne State University in Detroit, Michigan.

More posts by Jim Roumell