This article is authored by MOI Global instructor Ben Beneche, co-founder and portfolio Manager at Tourbillon, based in London.

Ben is an instructor at Best Ideas 2023.

“Although competitive advantage period has unassailable importance in valuation, it is a subject that has not been explicitly addressed in finance textbooks in a way commensurate with its importance.” –Michael Mauboussin & Paul Johnson, Competitive Advantage Period: The Neglected Value Driver

“Look beneath the surface; let not the several quality of a thing nor its worth escape thee.” –Marcus Aurelius, Meditations

“Time isn’t the main thing. It’s the only thing.” –Miles Davis

Context

At the heart of the 24/7 news cycle and vast amounts of trading in public securities lies a simple, often forgotten fact: equities represent part-ownership of a business over its lifespan. While we understand the temptation to equate shrinking holding periods with investor short-termism, we view asset prices as discounting future fundamental expectations over the long-term. Even short-term price moves can be framed through the lens of implied probabilities of future outcomes 10+ years into the future.

A simple thought exercise illustrates this. It is not at all unusual to find companies trading at a 5% cash flow yield (20x P/FCF multiple) growing at 4%. If one were to buy the company outright (in a ‘take private’ transaction) and hold it ‘forever’, it would take about 15 years to simply break-even on the investment from the cash generated and distributed to owners. And this doesn’t even embed the opportunity cost of equity capital! It is axiomatic that it is the long-term cash generation of a business over decades that determines shareholder value (and in turn, share prices).

Independent statistics point to the typical age of an S&P500 company being just above 20yrs (down from the 35yrs in the mid-1970s[1]). This means that at typical valuations, investors need to make judgments about the entire cradle-to-grave lifecycle of a company. In a context such as this, it is even more important that investors pay attention to assessing the competitive advantage period (the period over which a company earns super-normal returns on investment) and find assets which can endure. Longevity is a vital component of quality.

The spectrum of quality

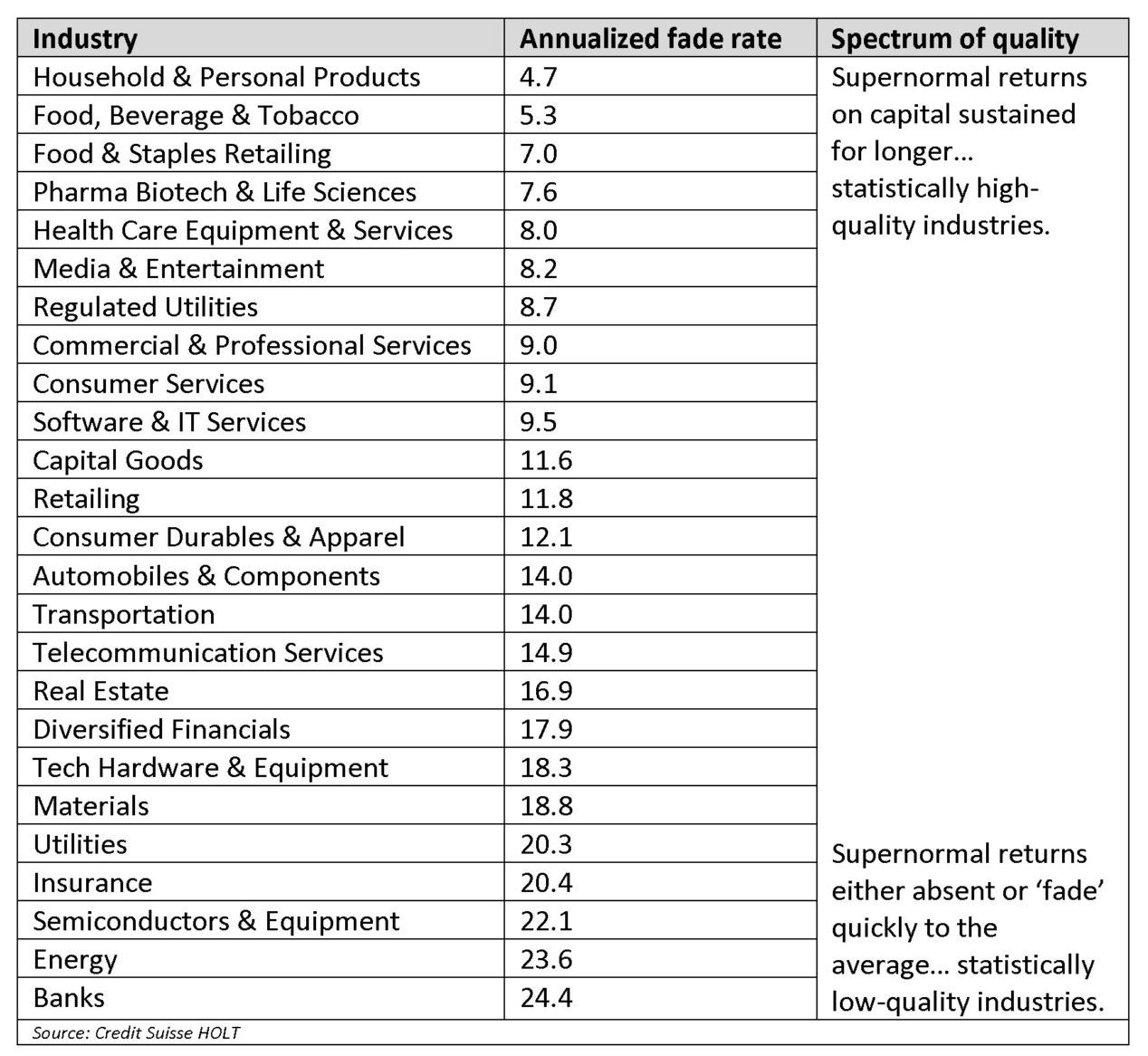

The prevailing economic theory surrounding the ‘competitive advantage period’ suggests that there are certain industries where companies have disproportionately high odds of delivering persistently high returns on capital. The table alongside is typical of the results produced by academic studies of corporate performance and valuation theory.[2]

Given this, it is natural that students of quality business models are drawn to industries near the top of the table that seem to be ripe hunting grounds for consistent compounders. We submit however that duration can be found in somewhat opposing corners of the business world. They can be in highly consolidated industries or in their exact opposite – highly fragmented industries. Paradoxically, the opposite of a good industry can also be a good industry to find durable assets. Like with many discoveries in the natural sciences, there is even an aesthetic quality to this fundamental truth.

Given this, it is natural that students of quality business models are drawn to industries near the top of the table that seem to be ripe hunting grounds for consistent compounders. We submit however that duration can be found in somewhat opposing corners of the business world. They can be in highly consolidated industries or in their exact opposite – highly fragmented industries. Paradoxically, the opposite of a good industry can also be a good industry to find durable assets. Like with many discoveries in the natural sciences, there is even an aesthetic quality to this fundamental truth.

Same but different

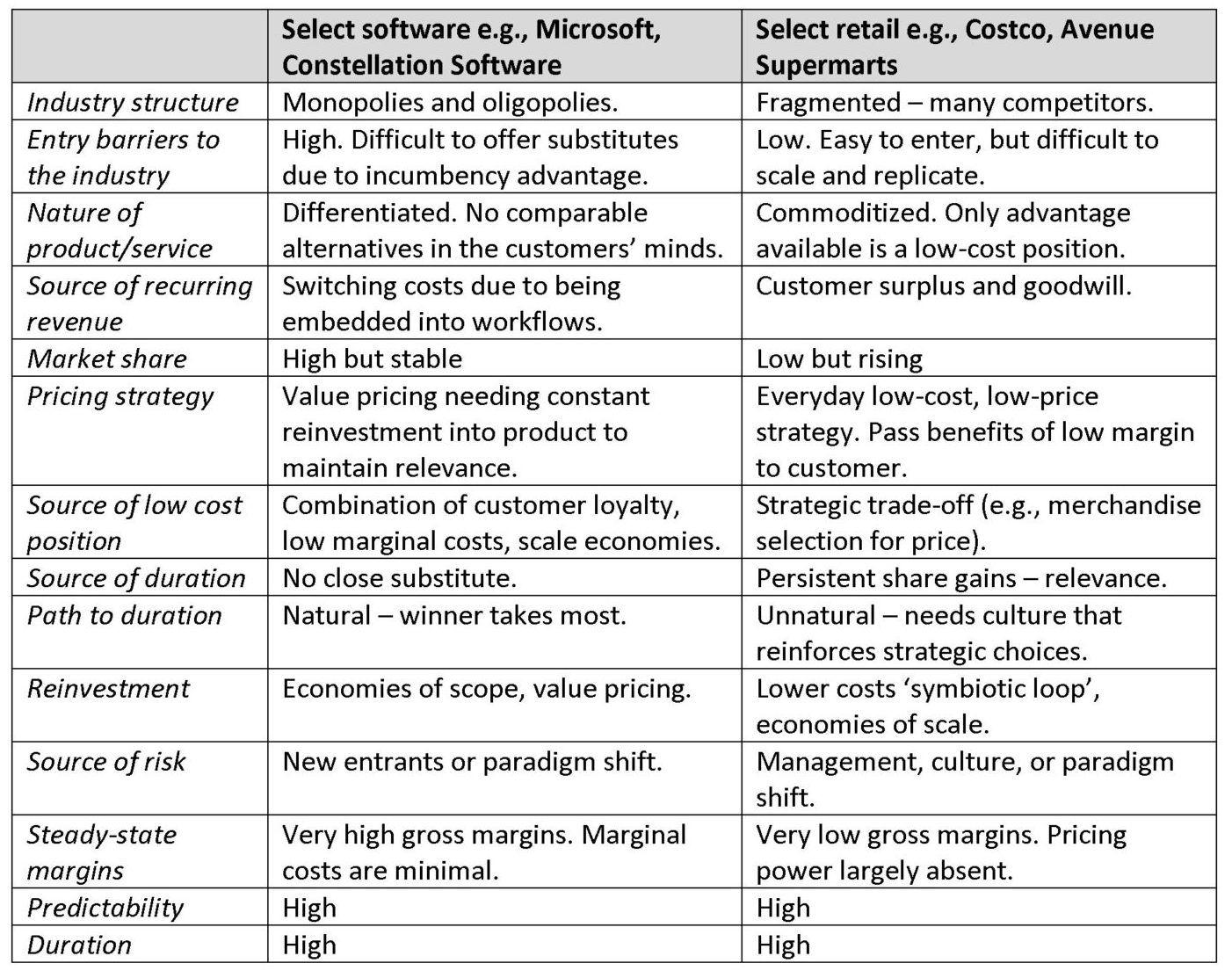

To illustrate, consider select enterprise software juxtaposed with select retailers. The many attractions of the former and the enormous entry barriers seem evident as offering true ‘duration.’ Retail is not as glamorous an industry – there is largely no differentiation in the products being sold and these are companies selling everyday essentials with no venture capital dollars chasing world-changing innovation. Nevertheless, we think from the perspective of ‘duration’, even the apparent differences lead to similar longevity.

A more generalizable pattern can be drawn out here.

There are some industries with high entry barriers which have duration, e.g., enterprise software, infrastructure assets, aerospace, medical devices, select consumer brands. We could refer to these as ‘Distinctive’ businesses and the common features here tend to be some form of products or services which have no close substitutes (real or perceived). The natural evolution of these industry structures tends to be oligopolistic (or even monopolistic) with high margins and significant barriers to entry. Students of Warren Buffett will recognize Moody’s, See’s Candies and Burlington Northern as exemplars of this.

However, there are some industries with low entry barriers which can and do house idiosyncratic companies which also have high duration, e.g., retailers, insurers, banks and homebuilders. We could call these ‘Commodity’ businesses. Our observation is that they are almost always structurally low-cost operators (usually with a management team and culture that safeguards and reinforces this) who consistently and persistently take share allowing a long reinvestment runway and duration. Amazon, Ryanair, and the early Wal-Mart spring to mind.

The underlying risks and points of fragility across three important facets (new entrants, growth runway/market shares and management) are an interesting study in contrasts too. These become important considerations as you are building duration into your portfolio in two very different ways.

New entrants. The key threat to quality (and hence value) in ‘Distinctive’ businesses tend to be new entrants that disrupt the monopoly or oligopoly characteristics of the businesses. These could be demand-side (consumer behaviour shifts that diminish market shares for a product or service – say, TikTok and its effect on Meta/Netflix) or supply-side (a new entrant offering a cheaper or better alternative – Adobe/Figma comes to mind). On the contrary, in ‘Commodity’ businesses, the risks one worries about are not so much from new entrants. Whereas new entrant risks tend to be keenly watched in enterprise software, you fret less about supply-side risks in owning Costco, as there is plenty of competition in retail!

Penetration and growth runway. These end to be more easily observable in ‘Commodity’ businesses too, since the quality thesis rests on consistent and persistent improvement in market shares. Whereas this is the exact opposite if you’re the industry standard in an enterprise software workflow – you’re already a dominant market share holder and that is the very feature that underpins duration.

Managerial culture. Tends to be disproportionately important in ‘Commodity’ businesses. Disciplined capital allocation, a long-term view and obsession on customer value must remain front and centre. Failure to do this will generally have dire consequences. Think of low-cost airlines expanding into new unprofitable routes, insurers writing dubious contracts to grow premiums or a retailer selling shelf space to the highest bidder rather than offering the best value product to consumers. ‘Distinctive’ businesses tend to emphasize the robustness of the business model with surplus profits generally re-invested into defending their position, through R&D or advertising for example.

Many roads lead to duration

We find it fascinating that duration can be found both in companies operating in industries with high entry barriers, monopolistic market shares and very high margins as well as those with low entry barriers, fragmented industries, and low margin structures. The very best “commodity” businesses turn the very fragility of operating in a difficult industry into a strength.

Franco-Nevada operates in a commodity industry (quite literally). As a streaming and royalty company in the precious metals space, its fate should have been mediocre. But the business model found a way to turn the very weaknesses of extractive commodity industries (high capital requirements, unpredictable op-ex, limited optionality) into strengths by being exposed to the opposite side of all the poor characteristics typical of miners. It takes no op-ex risk, has perpetual exploration upside without putting up new capital and has created an oligopolistic structure thanks to the intangible reputational entry barriers it has erected around itself. The result is that it has free cash flow margins that are multiples of Alphabet.

Once this truth is internalized, we see deeper patterns within business models that underpin durability. Costco is a retailer but has customer retention rates akin to the best enterprise software companies. The management clearly understand that their business is a ‘volume game’ rather than a ‘margin game’. This leads to better long-term growth, associated scale economies and, crucially, around 30% ROE despite the razor thin margins they operate at. Low margins don’t mean poor economics. Cosmos Pharmaceutical in Japan has a similar approach, managing their business to a 20% GPM (with no membership) to offer the best possible value to consumers. Despite the, perhaps obvious, benefits of this approach, very few retailers globally follow this model as it requires short-term pain (lower margins) for long-term gain (durability, growth, and cash generation).

This brings us back to the importance of managerial culture. We would argue that Berkshire Hathaway clearly demonstrates the power of a culture, structure and an incentive structure which prioritise deferred gratification. This is evident at Burlington Northern which has lower margins and higher cap-ex than its main competitor Union Pacific (and is gaining volume share as a result); at Geico which continues to gain share by re-investing its low cost base into superior pricing; at Berkshire Energy which is investing all of its available capital (and more) into long dated renewable assets; and at the re-insurance business whose ratio of surplus capital to premiums is multiples of its peers as their culture emphasises profitability and resilience over premium growth.

Although we will always be on the look-out for “distinctive” companies operating in rational oligopolies, widening the aperture of our analytical framework has allowed us to develop a focus on duration, which we believe is the deep truth of equity investing. Many roads lead to Rome, and thinking in first principles can isolate the underlying features behind industries and investments that lead to duration.

[1] Source: Statista, 2021

[2] Some of the highest quality literature on sustainable competitive advantages and the persistence of supernormal returns on capital can be found it a few sources: (1) Credit Suisse HOLT Corporate Performance Handbook; (2) Prof. Aswath Damodaran’s work at NYU Stern; (3) ‘Valuation: Measuring and Managing the Value of Companies’ by Koller, Wessels et al (‘the McKinsey valuation book’)

About The Author: Ben Beneche

Benjamin Beneche, CFA is a Senior Investment Manager at Pictet Asset Management Limited. He joined the firm in 2008 and is in the EAFE Equities team with a specific focus on Asian equities. Mr. Beneche began his career as a graduate within PAM Equities then as a Junior Investment Manager on the global equities fund with an emphasis on the energy sector. Mr. Beneche is a Chartered Financial Analyst charterholder. He graduated with a first class honors degree in Economics and Economic History from the University of York.

More posts by Ben Beneche