This article is excerpted from a white paper by MOI Global instructor Benjamin Beneche, senior investment manager at Pictet Asset Management Limited. Ben is an instructor at Asian Investing Summit 2018, the fully online conference featuring more than thirty expert instructors from the MOI Global membership community.

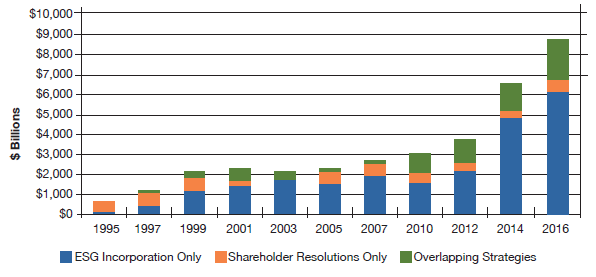

The investment management industry is currently awash with ESG – Environmental, Social and Governance, initiatives. Dedicated funds are being launched and awareness of these factors in a portfolio context is being highlighted by several of our counterparties.

Sustainable, Responsible and Impact investing in the United States, 1995-2016

Source: US SIF Foundation, as of 12/31/2016.

Your fund is currently making a concerted effort to incorporate a more systematic approach towards these factors into our investment process. The reasons, however, have little to do with the prevailing industry trends but more to do with our core belief that they are integral to the assessment of the intrinsic value of business. In fact, it’s interesting to see that companies which score highly in ESG factors tend to outperform the broader market and vice-versa.

We do not, however, believe in an overly constrictive or systematic approach to this endeavour. In fact, we would argue that many core aspects of ESG investing are already incorporated into our process.

Firstly, your fund focuses on cash flow generation over accounting earnings. We believe there are various merits to this but none more important than the ability to sniff out accounting shenanigans. Profit and loss statements hinge on a concept known as accrual accounting; the matching of revenues and costs. In reality, a lot of businesses, particularly capital intensive businesses, have significant mismatches. This is not necessarily a cause for concern but it does allow some leeway in things like asset life assumed for depreciation and recognition of revenues for services rendered. With cash, however, there is no lying. When cash is spent it is recorded, when it is collected from clients it is recorded. The end sum of free cash flow is broadly the amount added to a company’s bank accounts over a given period. In theory cash flow and earnings should equal one another over time but in several cases this is not the case. It can be manipulated for a while, the management of Enron were famous for being ‘laser focused on EPS growth’ but over the very long term free cash flow and net income converge one way or another. Our focus on cash generation means that any aggressive accounting policies designed to enhance earnings or EPS should become quite apparent.

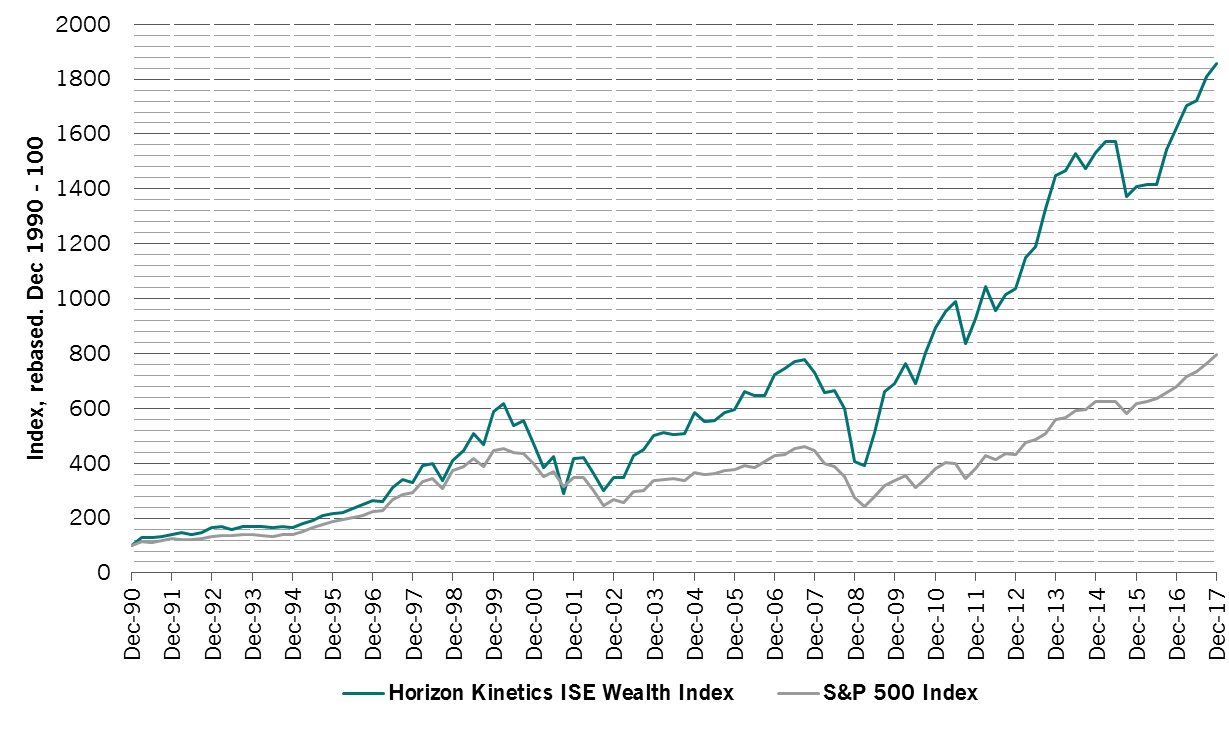

Secondly, our search for businesses which generate higher returns on capital indicates a clear focus on capital allocation decisions made by management and the board. This, again, is central to good corporate governance. Third party service providers often take a somewhat dogmatic view on corporate governance with criteria such as number of independent board members, age or gender of those board members etc. Our assessment is based on a holistic assessment of the track-record of management, the incentive structures they have and our discussions with them in person. In general, we actually favor owner-operator businesses where management incentives are both highly aligned and long term in nature. We’ve written about our preference for these management teams in the past with several examples in your portfolio today; Johann Rupert of Richemont, Vincent Bollore of Bollore and Masayoshi Son of Softbank to name a few. Over time, this alignment has also created economic value;

Horizon Kinetics Owner-Operator Index

Source: Bloomberg.

The two examples above really focus on the governance side of the equation. Environmental and social issues are perhaps harder to pin-point but do ultimately lie at the heart of our long term assessment of a business. We believe the world is becoming increasingly transparent. Consumers have better access to information, switching costs are lower and capital requirements for companies are often minimal in an online environment. With this being the case, for a company to sustain high returns often requires more than scale and access to capital, it requires a product or service which provides real economic utility to all of its stakeholders. One example here would be JD.com. JD.com is the second largest e-commerce company and largest direct procurer of consumer goods in China. Despite its scale, it only generates a 9% gross profit margin on its core business and remains on the cusp of operating profitability. This compares to bricks and mortar peers who generate on average 19% gross margins and a solidly profitable. The reason is simple: JD.com is offering both the cheapest prices to customers and procuring at attractive prices for manufacturers. In fact, one of its main suppliers said JD.com recently told us they were the only profitable channel they have. Richard Liu, the founder of JD.com is obsessed with offering the best deal to his stakeholders with the belief that, over the long term, they will leverage their scale advantage and wholly owned logistics to deliver a 5% margin over time, just about the cost advantage they have over their competition… no more ! This approach makes it almost impossible for the competition to keep up as JD.com continues to grow at phenomenal rates as a preferred channel for all of its stakeholders. In this end this very socially aware approach to business just makes sense and represents a key competitive advantage for JD.com.

We want to stress, however, that ESG considerations matter for us to the extent that they impact the long term health of a business. This is absolutely critical. Let’s consider one of your fund’s largest positions, Japan Tobacco (JT). Intuitively this really does not ‘tick’ and ESG box and certainly would not feature in a thematic portfolio. However, in our assessment of business value these factors featured heavily, in fact one could argue that they drive the investment case! Japan tobacco generates 55% of its operating profit from two markets, Japan and Russia. These are both markets where smoking rates are high, around 30% of Japanese men and 50% of Russian men smoke. The reason, to significant degree, is due to the high affordability of cigarettes in these countries; at 4USD a pack in Japan and 2USD a pack in Russia. These levels are amongst the cheapest relative to GDP/capita in the world.

Our assessment of JT’s value hinges largely on the fact that the governments of Japan and Russia will gradually increase the taxation of tobacco in an effort to reduce smoking rates. The volume of cigarettes sold will be 3-5% lower per annum but importantly, the tobacco industry is likely to take price in excess of the tax hike and will save costs due to a lower costs ; both manufacturing and raw materials. In aggregate, free cash flow is likely to increase in the mid to high single digit range. In the end, the social pressures to lower smoking rates are actually what we believe will drive the success of Japan Tobacco over the long term. We should also highlight that there are plenty of instances where ESG considerations do prevent us from investing; where we feel these business risks are not captured in the valuation. Some examples would include various pharmaceutical companies whose drug prices do not reflect their utility to society, Japanese utilities with a heavy focus on nuclear in the wake of the Fukushima disaster or even our avoidance of traditional automotive manufacturers which we feel valuations do not necessarily reflect the long term risks associated with electric vehicles and higher emission standards.

In conclusion, although we wholeheartedly embrace a more focused and disciplined assessment of ESG factors we believe that, as always, the thorough assessment of business is not a mechanical task but a case by case analysis of the internal and external factors which will allow a company to grow its cash flow per share over the long term. For our longstanding investors, we hope that sounds familiar!

About The Author: Ben Beneche

Benjamin Beneche, CFA is a Senior Investment Manager at Pictet Asset Management Limited. He joined the firm in 2008 and is in the EAFE Equities team with a specific focus on Asian equities. Mr. Beneche began his career as a graduate within PAM Equities then as a Junior Investment Manager on the global equities fund with an emphasis on the energy sector. Mr. Beneche is a Chartered Financial Analyst charterholder. He graduated with a first class honors degree in Economics and Economic History from the University of York.

More posts by Ben Beneche