This post is authored by MOI Global instructor James Fletcher, founder of Ethos Investment Management, based in Salt Lake City.

James is an instructor at Best Ideas 2022.

The following article has been excerpted from a recent Ethos letter.

We believe that investing in high-quality businesses with sustainable growth prospects, led by excellent management teams that are purchased at reasonable prices, will achieve excess returns over a complete market cycle. We take a long-term, business-owners, approach to investing and invest only in our highest conviction 30-50 ideas.

Investing in Emerging Markets

Why am I focusing on EM small and mid-cap stocks (SMID)? The short answer is that over my 17-year career in investing, I have found this opportunity set of EM SMID to be the most attractive and inefficient (i.e. opportunistic for alpha) in terms of finding excellent structural growth companies trading at attractive valuations.

Emerging markets is home to 85% of the world’s population, now accounts for over 59% of the world’s GDP, yet comprise only 12% of global market cap and less than 6% of global institutional investors’ allocations.[1] Over time, I expect these numbers to continue to converge in favor of EM. As structural growth trends continue of a rising EM middle class, growth in innovation sectors, and access to capital, EM seems poised to continue its growth trajectory. What is especially exciting to see is that while developed markets have seen the total number of companies listed on exchanges decline over the past decades as fewer companies go public and more delist, EM has seen the number of companies listed in Consumer, Technology, and Healthcare sectors more than triple over the past decade (from 455 in 2010 to 1,622 in 2020).

Over the past 20 years, starting Nov 2001 to Nov 2021, all Indices, both EM and DM have delivered nearly identical annualized USD returns. (EM has delivered 9.85% IRR since 2001, EM SMID has delivered 9.81%, compared to S&P500 at 9.31% IRR, in USD). This is despite the recent underperformance in EM.

In terms of valuations, EM is currently trading at historical record discounts now to their counterparts in US and Europe, trading at over 60% discount on a P/E basis.

I feel that we are getting a great entry point into emerging markets right now and expect we can buy some high-quality businesses with long-term structural growth at good valuations which equates to better than average expected future returns. Of course, there are risks. Rising inflation, heightened regulatory, and geopolitical risks in China and other countries, the ongoing COVID-19 pandemic, and global supply chain shortages are all key risks that we need to weigh in the balance when underwriting any investment into the portfolio.

China vs. India

The underlying dynamics are leading us to have higher exposure than the EM Index in China, Taiwan, and Brazil. And leading us to have lower than market exposure in Southeast Asia, slightly lower in India and lower in Eastern Europe. Below I have highlighted China and India.

China

China, is expected to be our second largest market in the portfolio, behind Taiwan. While 2021 has been a tumultuous year for many listed Chinese equities, with heightened regulatory risks in sectors such as education, e-Commerce, and health care being negatively impacted, the long-term trends in China remain promising. We find that many great, high-quality businesses with low regulatory risks and high pricing power are now trading at attractive valuations in China. I’ve personally been travelling to and investing in China for nearly two decades and having lived in Hong Kong for the past five years, I’ve seen both bull and bear cycles over the period, including the bear markets of 2008, 2015, and 2018 in China. Despite the cycles, China has remained undaunted in its structural growth, rising urbanization trends, investment in innovation and access to capital benefitting from a large consumer market, high domestic savings rates, and low external debt levels. Many are surprised to know that since the year 2000, China has created more unicorns than any other country in the world, including the US.[2]

It has been an imperative that companies are aligned with President Xi’s “common prosperity” goals. As part of our ESG and Quality Scorecards, we do deep dives into the regulatory risks, pricing power, and societal risks of all the businesses that we analyze. This has helped us avoid many of the problematic sectors that were exposed in 2021 such as property and education, where we had no exposure. In the end, China and President Xi have been clear in their statements and 5-Year plans that that will continue to encourage economic growth, but they want businesses and regulators to promote:

- Fairer competition

- Reducing income inequality

- Social well-being

- Data Protection

In my opinion, these are not absurd goals. In fact, Charlie Munger was recently questioned at the Sohn Australia Conference about China’s crackdown on speculation and corruption, and he said “China is right to step out, step hard on booms and to not let them go too far. The extent that my country doesn’t do that, we’re inferior to China. They’re acting in a more adult fashion”.[2]

Whether “adult” or not, what we can’t dispute is China has undergone incredible economic growth over the past two decades, and we still see a market full of innovation, access to capital, and long-term strategic thinking. There are high-quality businesses in China that succeed in meeting all of Xi’s priorities and that we believe benefit from long-term structural growth trends in the market. And currently, many of them are trading at quite attractive valuations, due to the recent selloff.

India

India has had an exceptionally strong run in 2021, as YTD through 30 November, the India SMID Cap Index is up +41.7% in USD. We believe India has a lot of attractive long-term characteristics: a large and entrepreneurial population, a rising middle class, ongoing structural reforms led by Prime Minister Modi, and global leadership in sectors such as pharma, technology, and healthcare.

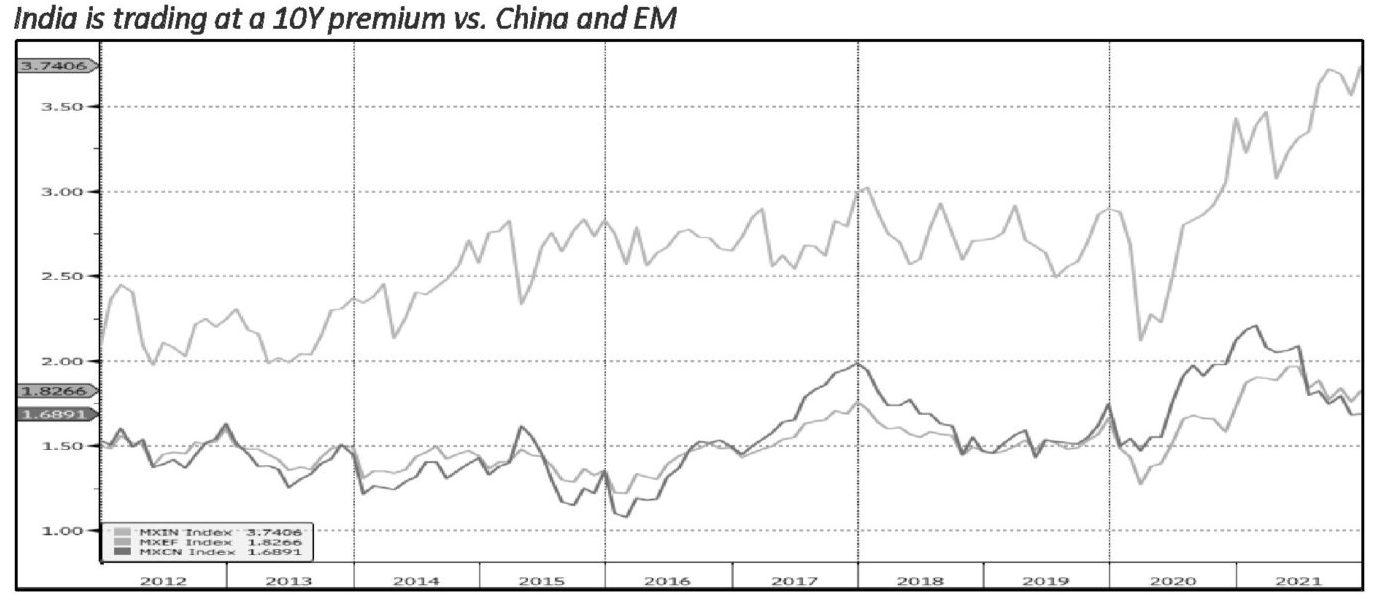

We find numerous businesses in India that we think are exceptionally high quality led by great managements with long-term growth potential. We expect our exposure to be slightly underweight India relative to the Index due to heightened valuation levels (India is 15% of the Index). The graph below shows that MSCI India now trades at a 10 year high relative to MSCI China and MSCI EM on a P/Book basis.

[1] Data is obtained from FactSet, MSCI and eVestment, as of December 2020.

[2] https://fortune.com/2019/10/22/china-us-unicorns-beijing-silicon-valley/

Read the legal disclaimer.

Members, log in below to access the restricted content.

Not a member?

Thank you for your interest. Please note that MOI Global is closed to new members at this time. If you would like to join the waiting list, complete the following form:

About The Author: James Fletcher

James Fletcher is the founder of Ethos Investment Management. He is a portfolio manager with nearly two decades of equity research experience. Prior to starting Ethos Investment Management in 2021, James was Director and Senior Portfolio Manager of the EM SMIDcap fund at APG Asset Management where he oversaw $1 billion AUM through a concentrated, high-conviction approach. James earned a B.S. in Finance from Brigham Young University, where he graduated summa cum laude and with University Honors. He is a CFA charterholder. He is also the founder of Young Investors Society (www.yis.org), a non-profit organization that teaches financial literacy and investing concepts to over 8k high school students across the world.

More posts by James Fletcher