This article is authored by MOI Global instructor Francesco Castelli, Portfolio Manager at Banor Capital, based in London. Francesco is an instructor at Wide-Moat Investing Summit 2019. His presentation on European banks, including Credit Suisse and Intesa, will be featured at the conference on Friday, June 28 at 10:30am ET.

A decade ago, my job would command respect and admiration; today, when I introduce myself as “bank analyst”, I spark an amusing range of different reactions: some people will compassionately comment “oh, I’m sorry” as if I were in the nuclear waste business. At a fintech conference, a new acquaintance frowned with disbelief, asking “do bank analysts still exist?”. Others will politely cut the conversation short: “I lost so much money with banks, I am never investing in the sector again”. I don’t blame them: European banks shares have been a terrible investment for quite a long time; their weight in the benchmark indices has more than halved since the 2007 peak. But history tells us that widespread, aprioristic scepticism is one of the typical sources of variant perception: investors hate losers and will avoid declining prices at all costs, even when they miss the best investment opportunities.

A bit of background: I survived 2008 as my mandate – at the time – was flexible and allowed me a zero weight in banks. As a fund manager, I spent a good deal of the last decade investing in bank bonds, and our investors profited from the lucrative rally in subordinated securities. But I think the time has come to seriously reconsider European banks equity as a core investment theme. I will offer a quick overview of key themes detailing why I believe European banks have become too cheap to ignore and offer highly attractive opportunities over the next decade.

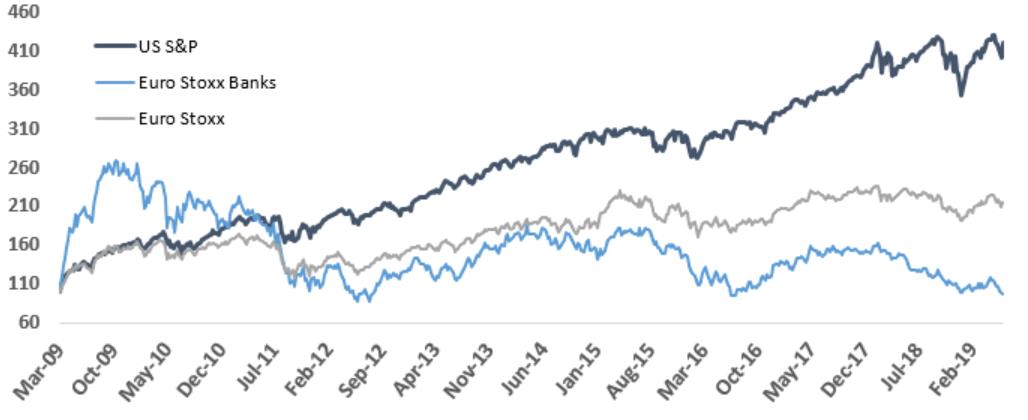

European banks lost 80% between the end of 2007 and the beginning of 2009, but that was just the beginning as they spent the following decade massively underperforming the market. An extremely lucky or very skilled investor, putting money on the Euro Stoxx Banking Index exactly at the post-crisis bottom (6th of March 2009), would today sit on a (slightly) negative return (even though they would have enjoyed a cumulative dividend stream equal to 45%, or roughly 4% per year).

In the meantime, the all-sector Euro Stoxx Index has doubled, and the US market has quadrupled, with global banks up 150%.

This unprecedented underperformance has stemmed from a combination of different factors: a decade of lacklustre growth, a huge increase in regulatory tightening, sovereign risk crisis and the final blow of negative interest rates.

Recent market developments have offered little support: the Euro Stoxx Banking Index managed to lose a further 28% in 2018 (once again the worst sector) despite a bottom line increase of 6%. A derating in excess of 30% is somewhat rare, even in the context of the financial sector.

One of the most common pushbacks I get is “European banks are underperforming because they keep on losing money”. Which – in some cases – is true. On average though, the Return on Tangible Equity for a European bank exceeds 9% (and banks are, on average, trading at a discount to book value). Dividend Yield is in excess of 6% and the P/E is at a hardly demanding level of 9. The sector is so cheap that, according to a recent research paper by Goldman Sachs, the multiples already imply a further 20% decline in earnings per share.

Investors are probably requiring an extra level of compensation for a combination of the following risks:

– Macro unknowns: The (lack of) European growth is morphing into a “Japanification”; recent improvements in Cost of Risk are likely to reverse in a protracted downturn

– A resurgence of sovereign turbulence: Italexit would hit all of the banks in the continent hard (BTPs are a common investment in many systemic banks [BTP Italia is a government security that provide investors with the protection against an increase in the level of prices in Italy])

– Negative rates: They will continue to produce an implicit “tax on banks” costing several dozen billion per year

While scepticism is understandable, banks have learned how to survive and thrive in an unsupportive environment. They have profoundly adapted their business model, with branch closures, redundancies, billions spent on new technologies and entire business lines abandoned due to lack of profitability or inefficient capital requirement. Take Banca Intesa, the largest Italian bank: a domestically focused business commanding almost a quarter of the Italian market, survived both 2008 and the Italian recession (2011-2014) without the need of a capital increase, thanks to its prudent credit standards. Its management has relentlessly improved efficiency (driving cost income down to 50%, one of the lowest in Europe). It is one of the capitalized entities under ECB supervision (CET1 of 13.6%) and has gradually reduced its reliance on traditional lending, shifting the workforce towards more lucrative and capital efficient activities, such as wealth management and insurance. In the meantime, the company has achieved an impressive return on capital: dividend was skipped in 2008, but it has steadily grown since then and exceeded 3 billion EUR in 2018 (equivalent to a 10% dividend yield).

I often hear from investors that banks are an endangered species and the fintech revolution will destroy the industry. Certainly technology is and will continue to transform the banking business (in fairness, technology will have a major impact on virtually ALL sectors!). But the idea that banks are sitting on the fence and waiting to be slaughtered by an inexperienced crowd of programmers is completely misplaced:

– With the exception of payment systems, fintech is attracting a lot of capital but is failing to delivering meaningful returns (“run like Uber”)

– Banks are an active player with their own fintech investments (BBVA owns Denizen, a direct competitor to Revolut, Standard Chartered is rolling out its native digital bank in 10 African countries)

– Several fintech businesses started as disruptors, but are now becoming suppliers for existing banks instead of competitors

Fintech will be a revolution, and it will put several institutions out of business, from the too slow to adapt to the too small to afford the required investments. But it will also be an opportunity for large incumbents to reassert their dominance by delivering a better service at a lower cost.

IT investments and regulatory costs are clearly redefining economies of scale: smaller operators are likely to survive only when they have identified a niche where they can form a competitive edge. The rest of the market is likely to be dominated by a relatively limited number of players (3 to 5 per country). Cross border consolidation – on the other side – is not going to play a big role in Europe, at least under the current regulatory framework (still fragmented country by country, without an EU-wide deposit insurance scheme).

The best returns will be made either investing with market leaders or identifying specialty players with a specific competitive advantage. Credit Agricole is a good example of a leading bank that has been able to adapt and has consistently made money (despite fierce competition and the presence of other big, respected players in its home market). It offers a sustainable dividend in excess of 6%, with a price equating half of its book value.

KBC is an interesting combination of market leadership combined and emerging market flavour: it was hit hard during the Great Financial Crisis due to its structured credit exposure, but the bank accepted extensive government support and started to restructure its activities. Nowadays it is focused on retail banking in 6 different, smaller markets (Belgium, Czech Republic, Slovakia, Hungary, Bulgaria and Ireland). In order to build its successful international group, the bank has invested only in countries where it is able to achieve a leadership position. It currently offers a 6% dividend and is exposed to selected, higher growth markets.

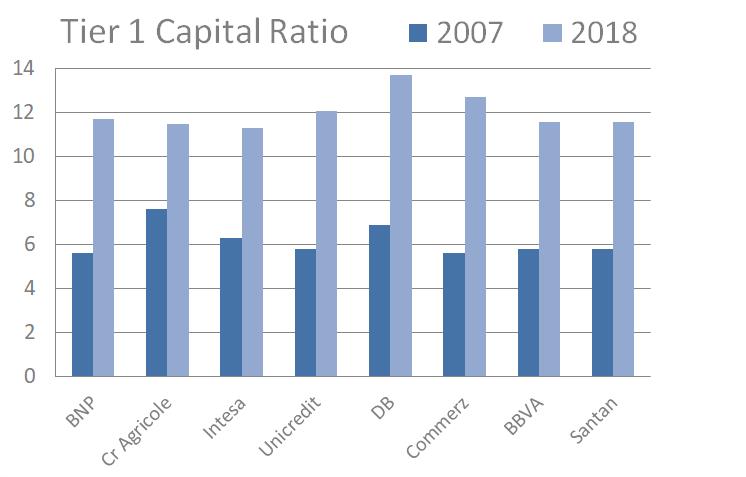

Let me address one final concern: the lack of capital and banks’ credit exposure in a downturn. While insufficient equity was a key driver during the last decade, capital levels have doubled since 2008 through a combination of retained earnings and an endless string of painfully dilutive capital increases.

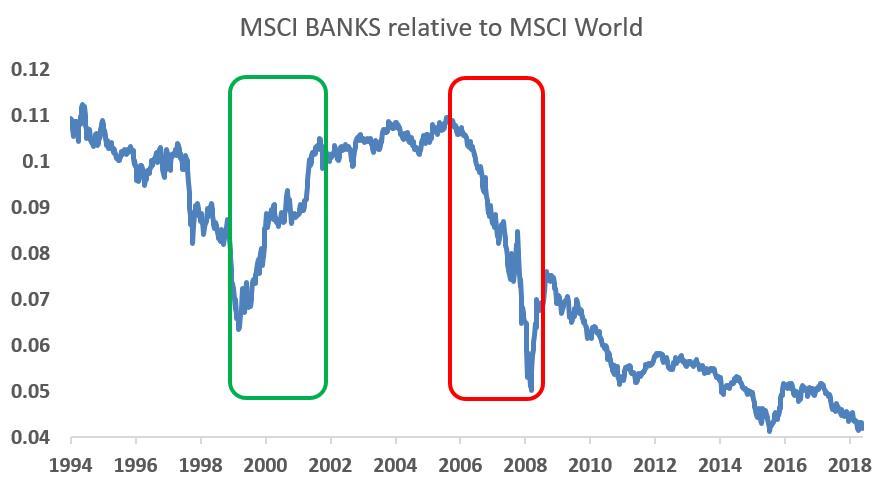

The sector today is much better equipped to withstand a downturn; and on top of this, a relentless tightening of banking regulation and an intrusive supervision approach have profoundly altered the composition of the banking book: capital and liquidity are considerably stronger, the overall credit exposure is lower, and the quality of borrowers is much higher. For this reason, I believe they will not underperform in the next recession; and whilst their share price may fall in a downturn, they stand a decent chance of decoupling from weaker sectors. Banks are not high beta by nature: we all remember how painful it would have been to be overweight in banks in 2008, but we rarely remember that being long banks was a winner during the 2001-2003 downturn.

The previous examples show that value opportunities exist within the current market. On the other side, before we see a sector wide repricing, we will need evidence of a more reliable sector. Improving banks results, in a slowing economy, may work as a catalyst and will be the first signal for the nascent bull market.

About The Author: Francesco Castelli

Francesco Castelli is the Head of Fixed Income at Banor Capital and manages the Banor SICAV Euro Bond and Aristea SICAV Enhanced Cash funds. With over two decades of experience, Francesco previously worked with groups such as Zurich Investments, Sanpaolo IMI and Kairos Partners. He has an Economics degree from Università Luigi Bocconi in Milan and qualified as a Chartered Financial Analyst in 2003. He specialises in financial bonds and capital securities.

More posts by Francesco Castelli