This article is authored by MOI Global instructor Danilo Santiago, portfolio manager at Rational Investment Methodology, based in New York.

Danilo is a featured instructor at Best Ideas 2021.

There is an adage that says, “fish where the fishes are.” The obvious parallel with the stock market is that investors should look for investments – on the long-side – when several good companies are trading at undervalued levels. At the end of 2020, RIM’s [Rational Investment Methodology] CofC [Circle of Competence] shows that we are in an unfriendly environment for long allocations.

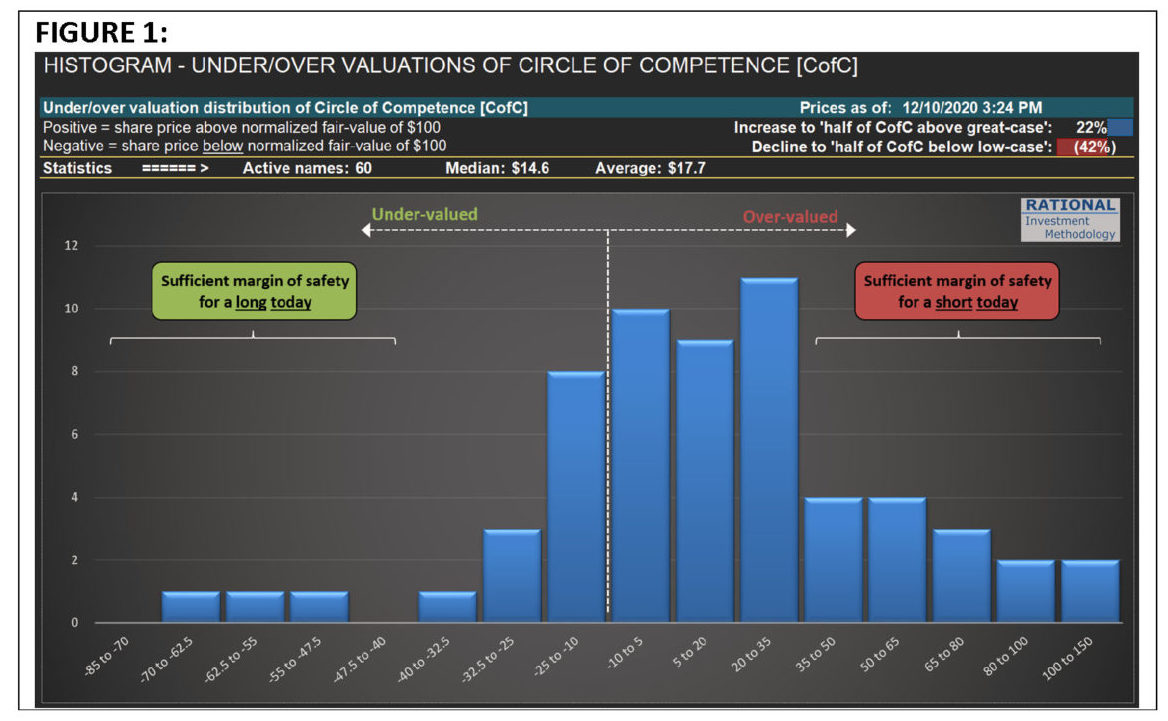

The statement above comes from observing the histogram in Figure 1 below, which shows the under/overvaluation of 60 companies that comprise RIM’s CofC. First, note how skewed to the right the histogram is, meaning that as of now, most companies are above their base-case fair-value.

To produce this chart, I normalize each’s companies fair-value to $100 per share. I.e., if a company’s base-case fair-value is $50 share, I multiply it by two to reach such normalization. Conversely, if a company’s base-case fair-value is $200 per share, its value is divided by two. Also, note that there are only three companies on the far-left side of the curve.

They are all turnaround stories that are taking years to confirm the thesis. One is a consumer goods company that has been losing market share for years. Another is a materials company that has been working to fix its balance sheet for a decade. The last one is a packaging company that has been fine-tuning its assets mix over the years, leading to very complex financials. In other words, there is no simple/reliable business selling at a deep discount to intrinsic value.

At RIM, a deep discount means a stock that is offering an IRR [Internal Rate of Return] – for a hypothetical investor that would hold the company forever, willing to receive dividends in perpetuity – of mid-teens returns.

It is noteworthy to call your attention to a particular number in the chart above. You can see a -42% figure at the upper-right corner, with the legend “Decline to half of CofC below low-case.”

This figure means the following: If the market were to fall today, indiscriminately (i.e., all positions falling by the same amount), by 42%, Odysseus (RIM’s portfolio construction tool) would buy half of the companies on RIM’s CofC. Owning half of the companies I follow is what I consider a “cheap market.” Not to be confused with an “absurdly cheap market,” which we had in 2009 – if we were to witness a market level close to the levels seen during the Great Financial Crisis, more than 80% of the names on RIM’s CofC would become longs.

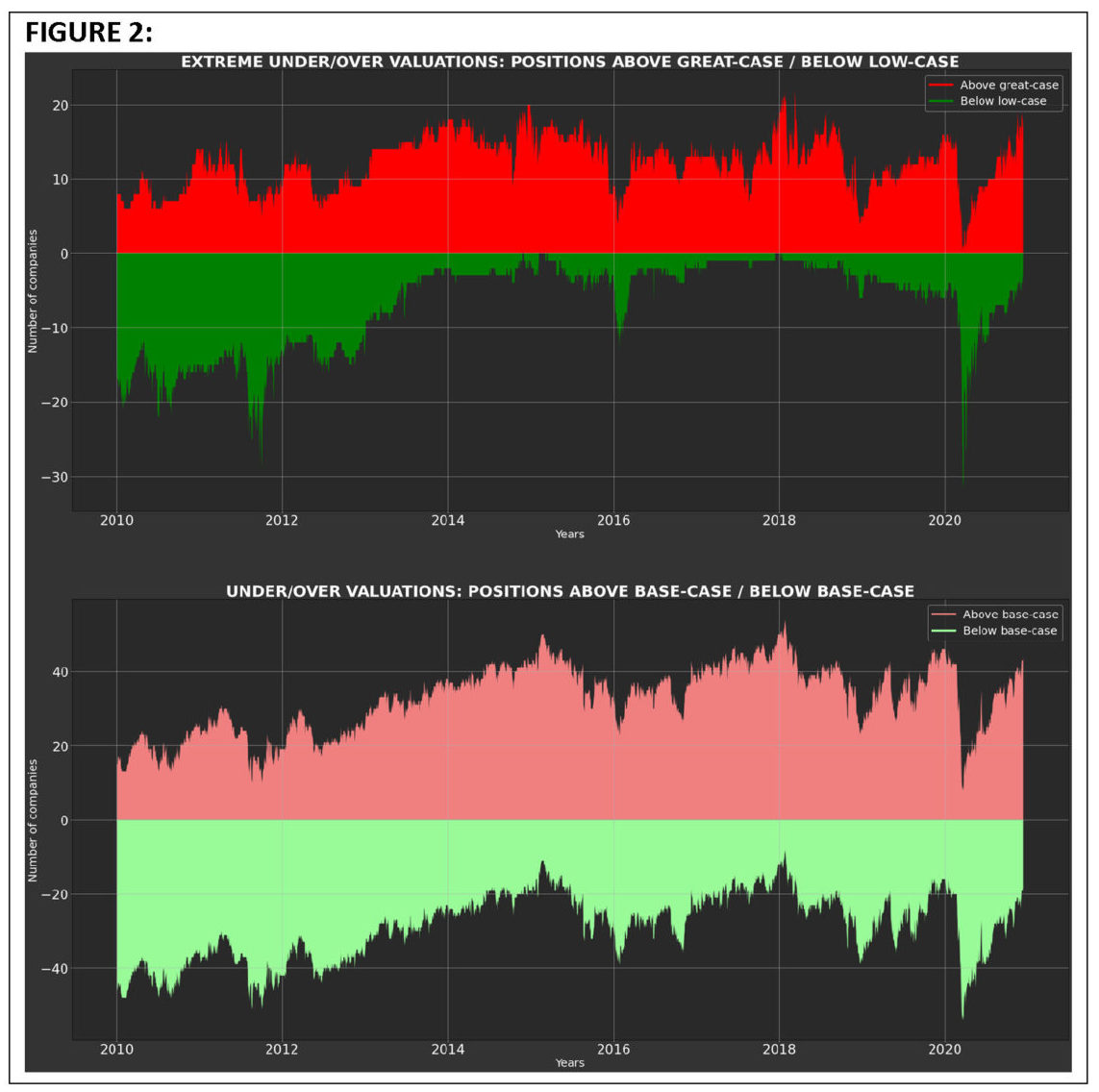

Now, how frequently has this histogram looked similar to what we have today? To answer this question, look into the chart in Figure 2 – it comes directly from Odysseus, a powerful tool developed — in-house — in Python (the most productive and sophisticated programming language I ever worked with). On top of simulating a portfolio strategy for more than a decade in less than ten seconds, Odysseus plots a series of charts that allow me to check for inconsistencies in RIM’s approach or even a data reading error when running simulations.

The subplot at the top shows extreme valuation cases. The area in red represents how many names are above their respective great-case fair-values. I.e., when a company’s share price reaches such a level, Odysseus would start a short position on the stock. The green area represents how many names are below the low-case fair-value. In such cases, Odysseus would include a new long position in the portfolio. The subplot at the bottom represents all names in the CofC. I.e., it is closer to the histogram showed in figure 1, as both include all companies of RIM’s CofC. The light-red area represents names above their base-case fair-values (but that might still be below a great-case fair-value).

On the other hand, the light-green area represents names below their base-case fair-values (but that might still be above a low-case fair-value). In other words, the light-red and light-green areas represent – over-time – the number of companies that are on the right/left, respectively, of the vertical line you see in the histogram in figure 1. The critical point here is to observe that the red/light-red areas are close to prior peaks achieved during the last decade.

What does all this mean for investors today? RIM’s count of under/overvalued names is not a timing tool – i.e., there is nothing that prevents The Market from paying up for something that is already expensive. However, if the fundamental analyses conducted are correct, when there is an abundance of companies selling at prices that would imply a low IRR (vs. historical norms) to the owner, investors are better served by having less exposure to the overall market. For instance, RIM’s long-short strategy is, as of now, only 9% net-long. The long-only construct has 40% in cash. It is essential to note that “as of now” means mid-December of 2020, a completely different environment from March of 2020.

As you can see in the subplot at the top in figure 2, ~30 companies were below their respective low-case fair-value in mid-March. Some companies were in such a state for just a few days – so Odysseus didn’t trigger a buy to all of them (it needs, for a variety of reasons, to observe the share price below a company’s low-case fair-value for ten days before buying its shares). But it was able to increase the long side of the book to 18 names, leading the net-long exposure to its maximum of 60%. The long-only strategy was roughly 80% net-long. The exposure change – plus some superb individual buys – lead to a YTD gross performance of 31.6% and 36.5% for the long-short and long-only strategies, respectively (as of December 10th). These results are the best ones achieved by these strategies – if adjusting for net-exposure – since the first implementation of RIM’s methodology in 2008.

However, a few companies have been neglected by the market, usually because their business assessment is difficult and complicated. At moments like this is when fact-based advice makes a difference. If you were to own something in a market that is predominantly selling assets significantly above a reasonable base-case scenario, make sure you allocate resources to a company that has a significant chance of generating a disproportional amount of cash in your favor. If The Market goes through a correction, you will have the courage – as you will be well informed – to increase further the number of shares you own (as even your well-researched idea will sell-off with the rest of the market). Hence, my recommendation is to focus your attention on sources that can provide detailed fundamental analysis for various businesses, like the MOI Global events.

Alas, if you decide to focus on pie-in-the-sky stories, which are abundant today, and eventually realize you were wrong in your assessment of the business potential of the securities you own, permanent losses of capital will be a certainty. So, make sure the oasis where you are fishing is not a mirage!

About The Author: Danilo Santiago

Danilo Santiago is the founder of Rational Investment Methodology (RIM), that focuses on a quasi-static group of approximately 60 publicly traded, liquid US stocks - most of these companies, defined as RIM’s Circle of Competence, have been followed for more than a decade. RIM employs extensive industry research and analysis, building highly detailed proprietary discounted-dividend models, which are used to determine “fair values” of companies based on different scenarios. Lastly, RIM constructs “rules-based” model portfolios (long-short, long-only or long- aggressive) with a company-specific margin of safety relative to “fair value”, using its proprietary Odysseus Portfolio Construction Tool. Selected model portfolios are replicated into clients’ accounts, using Interactive Brokers’ platform, adjusting the number of shares in each client’s portfolio in a pari-passu manner. Mr. Santiago is a MBA from Columbia University and has a B.S. in Electrical Engineering from the University of São Paulo.

More posts by Danilo Santiago