This post is authored by MOI Global instructor Jeff Auxier, president of Auxier Asset Management, based in Lake Oswego, Oregon.

Jeff is an instructor at Best Ideas 2022.

A young generation of investors who have seen essentially nothing but good times for the market are speculating on exciting and high-risk stories. Instead of valuing sustainable earnings and consistent cash flows, many new investors are focusing on small penny stocks and options, hoping for substantial price appreciation in a short period of time.

In February 2021, over-the-counter markets saw 1.9 trillion transactions, an increase of 2,000% from the previous year. As a result of the influx of cash into the markets throughout the year, there were record levels of mergers and acquisitions (M&A) and Initial Public Offering (IPO) activity during the quarter.

Global M&A activity during the [third] quarter [of 2021] was over $1.5 trillion, up 38% over Q3 2020, and was the highest ever recorded for a single quarter (NASDAQ). Year-to-date, M&A transactions surpassed $4.3 trillion which is higher than the $4.1 trillion in annual M&A in 2007.

In just the first nine months of 2021, there have been 770 US IPOs, over three times the 10-year average of 205. The capital raised through US IPOs has surpassed both 1999 and 2008 levels. This means a plethora of supply.

Just as fossil fuels are starved for capital today, many areas of new innovation and technology are incredibly exciting but also lead to dangerous levels of competition and supply. Thematic ETFs like ESG (environmental, social and corporate governance) can lead to gluts and shakeouts.

The euphoria surrounding the legalization of marijuana led to irrationally excessive planting, which has decimated growers.

The history of transportation bubbles dates back to canals, railroads, airlines, bicycles, etc. The first electric car was developed in 1890 and ended by the 1930s. From 1900 to 1919, two thousand companies were involved in the production of autos in the US. Today, largely due to government mandates, many manufacturers are committing to a fully electric future. The massive mandatory capital investment required make it a very high-risk proposition.

In 1999 two popular themes were internet hosting and fiber optic. We flooded the market with fiber optic supply and ended up using less than 20% of the capacity. In the decade from 1999-2009, the S&P 500 was down 9%, but the biggest and most exciting tech stocks fell over 50% during that same time (Financial Times).

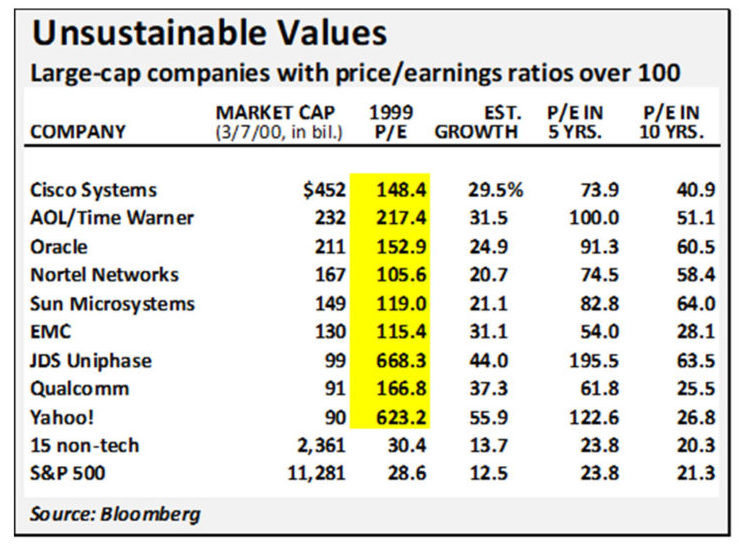

This chart from Bloomberg demonstrates how, despite having compelling stories in the year 2000, some of the biggest companies were materially overvalued and experienced substantial multiple compression in subsequent years. In referencing this chart, I remember the period like yesterday. In March of 2000 the level of greed, envy and frenzy was the highest I had ever witnessed. The technology fundamentals looked like they would be growing for years into the future. Then the supply caught up with demand; many stocks with exciting concepts went bankrupt leading to a bursting of the bubble and subsequent 80% decline in the NASDAQ.

The Auxier Focus Fund was up over the three years 2000-2002 while many funds that had doubled in the late 1990s went out of business. As mentioned in our prior letter, AOL and Yahoo, two of the most popular stocks at the time, were sold this past year by Verizon after declining 95% from their 2000 peak.

During the 1999 tech bubble, those who looked past the bubble priced companies and focused on value were rewarded. For example, the deeply discounted energy sector gained nearly 150% during the decade from December 1999 to 2009. That was also the best ten-year period for the Fund in relation to the market, with a gain of 84% vs. -4% for the S&P.

Cryptocurrency Risks Could Lead to Regulation

The cryptocurrency market has exploded in 2021 and reached a total market cap of nearly $2 trillion, a year-to-date gain of 156%. Much of the crypto boom has been due to the growth and popularity of Bitcoin, but alternative options have gained traction as the year has progressed.

At the start of 2021, Bitcoin accounted for approximately 70% of the entire market but it now accounts for only 43%. Companies like Visa and Mastercard have begun to embrace the technology with an eye on potential disruption in the future. Visa has partnered with over 50 crypto platforms to allow their customers to eventually use Visa cards to pay with cryptocurrency. Mastercard has partnered with cryptocurrency firm Bakkt to allow their users to hold and pay for card purchases with cryptocurrencies.

However, even with increased adoption from reputable businesses, the rapid growth and unpredictability of cryptocurrency has brought with it the risk of increased regulation. In September, the Chinese government announced that all cryptocurrency transactions in the country were illegal. The US has taken a less aggressive approach with Fed chair Jerome Powell saying that he has no intention of banning cryptocurrency. Increased regulation is critical to build confidence and credibility. We are carefully studying the evolution of the blockchain. The decentralized digital ledger could potentially be a disrupter to many centralized cloud-based models.

China Fundamentals

China has $52 trillion in bank assets or 56% of world GDP. Their number two real estate developer, Evergrande, binged on easy money. With $300 billion in liabilities, it now faces bankruptcy. Other major developers are facing a similar challenge. 29% of China’s economy is tied to real estate and construction, with most savings in apartments. Vacant apartments could house as many as 80 million people.

The Chinese government has been aggressive in reigning in excessive borrowing, poor accounting and monopolistic behavior by many of the major platform companies. In addition, they are suffering from severe energy shortfalls. This has led to some bargains in powerful franchises such as Alibaba.

In Closing

We are on pace to see over 104 management teams this year. We strive to know the fundamental earnings power of the companies we own. There is good value in smaller and midsized businesses with high integrity management teams. Most businesses we talk to are seeing robust demand, strong pricing and good margins.

Inflation appears to be up across the board with labor increasing 3.5%. For restaurants, wages are growing around 5.5% and over 10% in hospitality. Government mandates for vaccines and green energy are adding to the shortages for labor and fossil fuels. The service side of the economy is very robust. Companies with strong franchises are able to raise prices and so far, the customers are paying up. Inflation seems to be more persistent as wages are hard to retract and we are seeing rents, which are a large part of the consumer price index, showing double-digit increases coast to coast.

Companies that are executing with proven business models have been rewarded with huge premium valuations. However, higher inflation historically acts to compress valuations for all stocks, especially those speculative names with little earnings. With vaccinations widely available and the potential for the Merck antiviral, economic conditions should continue to recover from the worst pandemic in 100 years.

Politically there remains a sharp divide. Gridlock can be a good thing, as it can mitigate the potential damage of unconstrained government spending and onerous taxation.

About The Author: Jeff Auxier

Jeff Auxier began lessons in finance early–at age 11, mowing the lawn of Robert Pamplin Senior the former long-time CEO of Georgia Pacific and recipient of the “World’s Top CEO Award”. Mr. Pamplin tutored Jeff on living a life of ethics. As Jeff puts it, “Mr. Pamplin always put his shareholders first and believed business should be transparent. He said the language of business is accounting, and that if you can’t speak the language, you can’t make money.” In 1981, Jeff graduated with honors from the University of Oregon with a degree in Finance and an emphasis on accounting. Immediately, Jeff began calling or personally meeting with some of his investment heroes, long before they became today’s financial rock stars. Names like Warren Buffett. Not yet known as the Oracle of Omaha, Mr. Buffett graciously took several of Jeff’s calls and offered advice, most notably, “Number one don’t lose your principal and number two, never violate the first rule.” To this day, the cornerstone of the Auxier Focus Fund is respect for the power of compounding.

More posts by Jeff Auxier