This article by Matthew Sweeney is excerpted from a letter of Laughing Water Capital.

Gaia Inc (“GAIA”) is a situation where Mr. Market appears willing to pay you several million dollars to own a nichey, asset light, negative working capital, highly scalable streaming video on demand (“VOD”) business that is led by an owner operator serial entrepreneur with an enviable track record. The VOD business has reached scale and can be profitable at growth rates of ~30%, but the company is forecasting subscriber growth of 50-80% per year over the next 3 years, and funding this growth means that the business will lose money in the near term. However, this is an appropriate strategic decision that is more reflective of the vagaries of GAAP accounting than any problems with the business itself. In short, the business could be cash flow positive with the stroke of a pen by simply choosing to grow less quickly.

Admittedly this business is difficult to value, but I am quite certain it is NOT worth less than $0, the CEO has clearly demonstrated that he thinks the stock is worth more today than $7.75 per share (20+% upside from current prices), and the company believes they can achieve $60 million in pre-tax income and $2.50 per share in EPS in 2021. These are lofty goals, and investors are right to view them skeptically. However, if achieved, GAIA will likely be worth somewhere between $600 and $900 million in 2021, representing gains of 500-800% from today’s prices. Most important from my view, an investment in GAIA today comes with theoretically no down side due to cash and property on the balance sheet, making the VOD business a free lotto ticket. Notably, the value of the cash and property do not presently appear on the balance sheet preventing the automated screeners that rule the markets in an era where “stock picking is dead” from identifying the true economic value of the assets. This will change when the company releases Q3 numbers on 11/3, representing a hard catalyst.

Background

A few short months ago GAIA reported in two segments, Gaiam, a branded products business focused on selling yoga related products (“yoga products”), and Gaia (formerly Gaiam TV), a money losing video on demand (“VOD”) service that has more than 7,000 titles “focused on yoga, health and longevity, seeking truth, spiritual growth and conscious films & series.” Additionally, the company owned a stake in a travel business known as Natural Habitats.

It is logical to assume that investors who owned GAIA a few months ago owned it because of the yoga products business, and were barely focused on the travel or the VOD businesses except to the extent that they were not happy that VOD was losing money.

After previously toying with a spinoff, in May the company announced that they would be selling the yoga products business for $167 million and the travel business for $12.85 million. Following the sale, the remaining company would essentially be the VOD business. We will talk more about GAIA’s founder and CEO later, but as a teaser, consider that the travel business was purchased for $600,000 in 2002, representing a CAGR of approximately 24% and indicating that the CEO is a skilled capital allocator.

Concurrent with the sales, the company announced that they would use the proceeds to finance a tender offer for 12 million company shares at a price of $7.75 per share for a total of $93 million.

The company further announced that following the completion of the sales of the yoga products and travel businesses and the tender offer for $93 million they expected to have approximately $60 million on the balance sheet.

Recent Weakness

It is important to note that legacy shareholders are left owning something they never intended to own; they thought they owned yoga products, instead they own a VOD business. This may help explain why shares have been under indiscriminate selling pressure lately. This seems especially relevant when considering the largest shareholders, several of whom are index or quant oriented. A complete change in business model by a portfolio company likely requires these holders to sell. While it is likely that they participated in the tender offer to some extent, it is possible they are presently dumping remaining shares on the open market. Additionally, management has not made any attempts to reveal the true value of their assets to shareholders, presumably because they would like to re-purchase more shares in the near future.

Hidden Asset #1

While the company intended to repurchase $93 million worth of shares, the tender offer was under subscribed, and the company was only able to deploy $74,685,572 for 9,636,848 shares and $1,368,472 for 842,114 options, which equals ~40% of the company. Curiously (deliberately?), the sale of the businesses closed on July 1, meaning that the company’s balance sheet has not been updated in the latest Q to reflect the cash from this sale. Additionally, while the tender offer fell short by $17 million dollars, the company did not update their estimate of cash on the balance sheet during a September road show. Simple math suggests that if the plan was to spend $93 million on the tender offer and have $60M cash remaining, they should now have $77M in cash, or approximately 81% of the market cap.

Hidden Asset #2

GAIA owns a building in Louisville, CO, that they purchased in January of 2008. The building sits on their balance sheet at $17.2 million (purchase price of $13.2 million plus improvements that saw it initially appear on the balance sheet for $19.4 million), and management has stated that they think it is worth, “at least $20 million.” However, I believe that this vastly underestimates the true value of the building.

Louisville is approximately 40 minutes north-west of Denver, and is just east of Boulder. The population of Colorado is growing at 2x the national average, and the Boulder area is consistently listed as one of the most desirable places to live in the United States. The population is young, educated, and highly active, which likely explains why Boulder is quickly becoming known as a technological hub, with a thriving startup community and representation from several of the big tech employers. The young, educated population attracts employers, and employers attract more young, educated people and so on.

Boulder’s geography and love of open space has created a unique real estate environment. To the west of Boulder lie the Rocky Mountains, and residents are fiercely protective of their views. Local ordinances prevent construction of buildings taller than 55 feet, and the area to the west of Boulder is insulated from development by “the blue line” which was established in 1957, and restricts water service to elevations above 5,750 feet. According to a recent article in the NY Times, the growing population and limited land open for development has led to property values rising 60% over the last 5 years.

As you may have guessed, if you can’t expand up, and you can’t expand to the west, expanding south and east become more attractive (north of course is an option as well, but south and east are considered more attractive due to their proximity to Denver and major travel corridors). According to a local real estate professional, this effect is likely to be exacerbated in the coming years because Google recently built a campus east of the traditional down town center, which will, “push the center of Boulder eastward.”

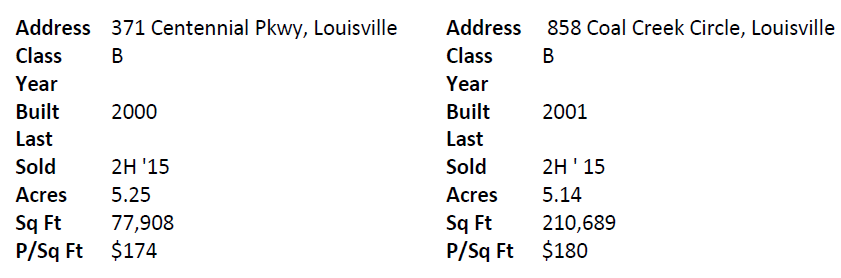

Accurately valuing commercial real estate is difficult because each building is unique, and is essentially worth what a buyer will pay for it. However, examining recent comps can be illustrative.

These properties are 2.5 miles from the building that GAIA owns and about 8.5 miles from Google’s campus.

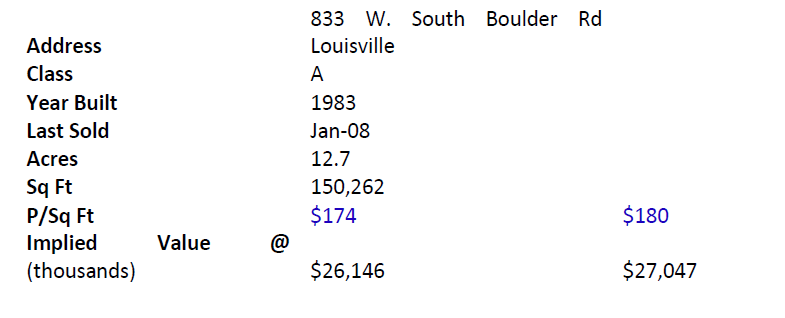

Information on the GAIA building (about 7.5 miles from Google’s campus) is presented below, as are implied prices if the above 2 comps are applied on a P/Sq Ft basis.

There are of course several other factors to evaluate when considering if the P/Sq Ft from the comps is relevant. Of note, the first two buildings are within spitting distance of the Denver Boulder Turnpike, while the GAIA building is about 2.5 miles away. Proximity to the highway is likely regarded as attractive due to ease of access for commuting employees and delivery trucks to the extent that delivery trucks are relevant. That being said, 2.5 miles away from the highway hardly seems an insurmountable distance. Also of note, the GAIA building is quite a bit older than the comps, but the age difference is mitigated because according to local news reports from the time (since confirmed by management) the building was purchased for $13.2M, but entered on the balance sheet at $19.4, indicating that a multi-million dollar renovation was completed subsequent to the purchase. This renovation likely contributes to the GAIA property being a Class A facility as opposed to lower quality Class B facility like the comps above. The fact that the GAIA property has an onsite cafeteria and gym also likely contributes to its Class A rating. The 12.7 acre property that the GAIA building sits on is likely highly valuable as well as it includes expansive parking, as well as green spaces and the like – a must for those going for the true “campus” feel when looking for an office space, and a feature that makes this property unique in the area. As such, I think it is reasonable to think that the P/Sq Ft estimates from the recent comps are a decent starting point for valuing the building. If one then considers that the comp sales took place a year ago and commercial-office space in the Louisville area is up more than 5% YoY, something in the neighborhood of $28 million starts to sound right, and it is not difficult to make a case for something in the low-mid $30 million range when one considers the Class A rating, the size of the property, and its unique attributes.

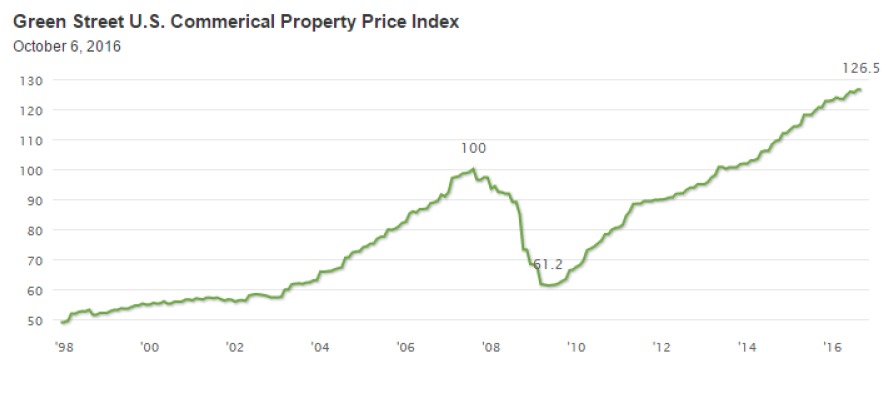

This may sound crazy in light of the $13.2 million purchase price less than a decade ago, but there are several factors to consider that take the edge off of crazy. Notably, the 2008 10-K valued the building plus improvements at $19.4 million and notes that the company believed that the purchase price of the building was “well below its replacement value.” Examining national trends in commercial property prices as provided by Green Street Advisors from January of 2008 through today suggests that the property should have appreciated by more than 35% (January of 2008 indexed at 93.4).

35% appreciation from $19.4 million carrying valuing suggests a present value of $26.2 million, but it is highly likely that properties in the Denver – Boulder area have over indexed over the last 8 years for reasons cited previously, which suggests a 35% increase from January 2008 levels is conservative. The area has simply exploded over the last few years, as evidenced by Office Vacancy rates in Boulder County that are below 4% presently.

Further evidence that 35% appreciation is conservative comes from the fact that GAIA seems to have scored a bargain purchase price. The seller was Conoco Phillips, a $50B behemoth who was conceivably not price sensitive, and the sale took place as the housing crisis was brewing and the real estate markets were falling apart. While January 2008 purchases index at 93.4 on the Green Street Commercial Property Price Index, January 2009 purchases index at 68.2. If Conoco was eager to exit (which seems likely), they likely hit a low ball bid from GAIA. Also worth considering is that the buyer was Jirka Rysavy, founder and present CEO of GAIA, who has proven over the last few decades that he is a savvy business man & investor who likely viewed the purchase as not just an office building, but an investment. All of these considerations serve to validate suggestions from recent comp sales that the property owned by GAIA is worth substantially more than $20 million.

Streaming Video Business For Less than Free?

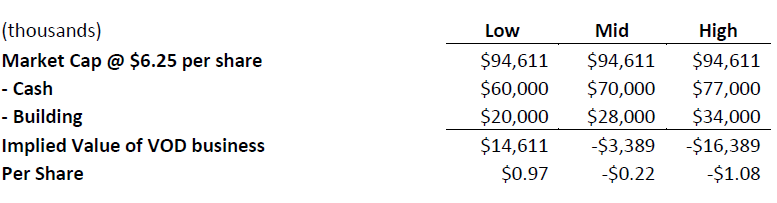

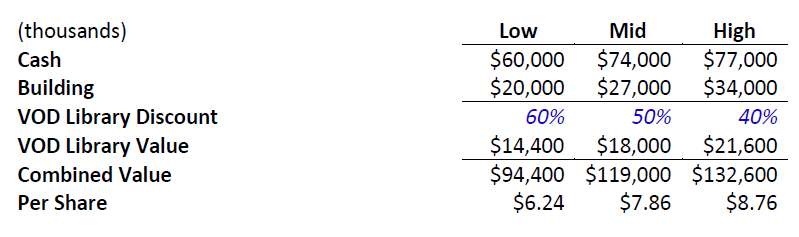

Combining the presumptive value of the cash that will soon be revealed on the company’s balance sheet and the assumed value of the building that the company owns reveals the implied value of the VOD business in a variety of scenarios.

Although the low case above is what the company has been touting, I consider it to be extremely conservative for the reasons laid out previously. The high case is arguably aggressive as it assumes that the VOD business will not have burned any cash in the quarter and that the building and associated real estate are trophies (although this is mitigated by the assumption that the value of the real estate is likely to continue to grow at mid-single digits for the foreseeable future). It is also worth noting that GAIA has indicated they were open to selling the building in the past and following the recent sale of the other businesses, the building is less than 20% used by GAIA, making a sale in the near term a very real possibility.

Worst Case Scenario…

When considering an investment that is essentially just a ton of cash and a building, investors are right to be skeptical. Tales of un-incentivized management teams treating their businesses as personal piggy banks, paying themselves high salaries and squandering the cash on foolish acquisitions are legion, and should be considered the worst case scenario in situations such as these. I suggest investors use this backdrop as a starting point when considering GAIA and its cash rich balance sheet. Now I suggest doing a 180 degree turn and considering the exact opposite: the best case scenario.

Following the recent sales and tender offer, GAIA is 38% owned by Jirka Rysavy, who neglected to participate in the tender offer, essentially doubling down on his investment in GAIA. Rysavy is thus clearly motivated to focus on share price. For additional evidence that Rysavy is unlikely to bleed the company, consider that this is a man who for years lived in a cabin in the woods with no electricity and no plumbing… while he was CEO of a Fortune 500 company. Suffice to say he is not driven by material trappings, but rather by entrepreneurial success, and on this front, his resume is impressive.

Rysavy came to the United States from Eastern Europe in the early 1980s with no money and a limited ability to speak English. He started a business known as Corporate Express which focused on selling recycled office products using the Walmart model (sell cheap!) as his blue print. He grew this business into a Fortune 500 company with 27,500 employees and sold it to Staples (SPLS) for $4.7 billion in 1998. During the early days of Corporate Express he also founded a natural foods store known as Crystal Market which he later sold to Wild Oats, which Whole Foods later attempted to buy. Gaiam, the predecessor company to GAIA, was also founded during the early days of Corporate Express, although Rysavy did not devote his full energy to the project until after the sale of Corporate Express. Rysavy has started and invested in several other businesses over the years, suggesting that he is a serial entrepreneur driven by business success, not money. This is an important backdrop when considering the downside case of an investment in GAIA. If we start with the assumption that the VOD business will fail, what we are left with is a highly motivated serial entrepreneur with a track record of success who has access to a pile of cash and his own skin in the game. I thus consider it highly likely that if it becomes clear that VOD is a failure, Rysavy will not continue to pour good money after bad, but will rather pivot and do something else intelligent with the cash.

The VOD Business

Having established that the market apparently thinks the VOD business is worth less than $0, it is worth considering what the market is so pessimistic about. In brief, GAIA is a globally available content provider with 170,000 existing subscribers and 7,200 hours of content, 93% of which is exclusive to GAIA. Broadly, the content falls into four categories, “yoga,” “seeking truth” (focused on metaphysics, ancient wisdom and answering the question “why are we here?”), “transformation” (focused on deepening the mind, body, spirit connection), and “films and documentaries.” The base rate for a monthly subscription is $9.95, and GAIA is available through all the major platforms like Apple TV, Roku, and Amazon, as well as to Comcast and Verizon customers. This is clearly niche content, and the company believes that in 2020 their total potential audience will be 11.5 million people, which represents 7% of the forecasted global “Over The Top” (OTT) video audience. The company presently has customers in 120 countries which represent 33% of their subscriber base. However at the moment language translation is limited, but set to expand beginning this quarter. Longer term the company believes that 60+% of their subscribers could be international. The company has in house production facilities at the previously discussed Boulder property, which contributes to them being able to keep production costs at a comparatively low 20% of revenue (vs 70% at NFLX).

At first glance, it is difficult to claim that this business has any sort of “moat” as barriers to entry appear to be limited. For example, there is nothing stopping Netflix or Amazon or others from entering the space tomorrow. The counterpoint to this however is that content of this sort is already abundant and freely available on YouTube. There are countless yoga studios that stream their content, and no shortage of people willing to soliloquize on their views of the world. Despite this broad availability, GAIA has been able to grow subscribers at rates between 30 and 90% annualized in recent history, suggesting that their content is high quality, and possibly that paying for the content imbues it with higher value. Over time it is likely that the presenters on GAIA’s platform become the moat, as subscribers develop a pseudo relationship with them. This should not be considered a deep or wide moat, but given the low stock price, existing library, proven production capabilities, and existing subscriber base, if Netflix, Amazon or other deep pocketed potential competitors wanted to enter the space, it would arguably be much easier to buy GAIA rather than build out a new offering. Additionally, Netflix and Amazon have much bigger battles to fight in the quest to become the dominant content provider, and niche content such as that provided by GAIA is likely low on their priority list.

So What is the VOD Business Worth?

As investors in NetFlix (NFLX) know, VOD can be a very attractive business. Clearly GAIA’s offering of yoga and lifestyle centric content has nowhere near the scale potential of NFLX, but the two businesses are similar in that they have tremendous embedded operating leverage, and are highly scalable. One Important positive difference between GAIA and NFLX is that while NFLX spends a fortune (~70% of revenue) on content costs, GAIA’s content costs are less than 20% of revenue, making GAIA significantly less capital intensive and allowing GAIA to benefit from negative working capital. These factors contribute to growth in revenue dropping almost directly to the bottom line, which means that pursuing growth is the right strategy for the long term, even if it can lead to operating losses in the short term. If you need further evidence that this strategy is wise, consider that it is estimated that Netflix will burn $1.2 billion in the coming year pursuing growth through marketing and content costs. Despite this massive cash burn, NFLX is awarded a 7x EV/Trailing Sales multiple by the markets, while GAIA trades at ~1x EV/Trailing Sales (excluding real estate), despite the fact that it is likely to grow more than 2x as fast as NFLX in the coming year.

VOD – Asset Value

The company has more than 7,200 hours of content, and production costs presently hover around $5,000 per hour of content. Replacement value would thus equal $36 million, but this type of content is essentially worth whatever someone will pay for it, and we can’t know in advance how much that is. For skeptics that might think this nichey content is worthless, consider that people want and actively acquire all sorts of content. For example, CONtv is a streaming network focused on “comic conventions.” That’s right. A dedicated streaming network focused on people who like to dress up in costumes and pretend they are super heroes. On days other than Halloween. In the interest of conservatism, it is appropriate to assume a discount to production cost of somewhere between 60 and 40%.

I believe that these numbers are a reasonable representation of what GAIA would look like in a liquidation scenario, suggesting that even under pessimistic assumptions downside is negligible.

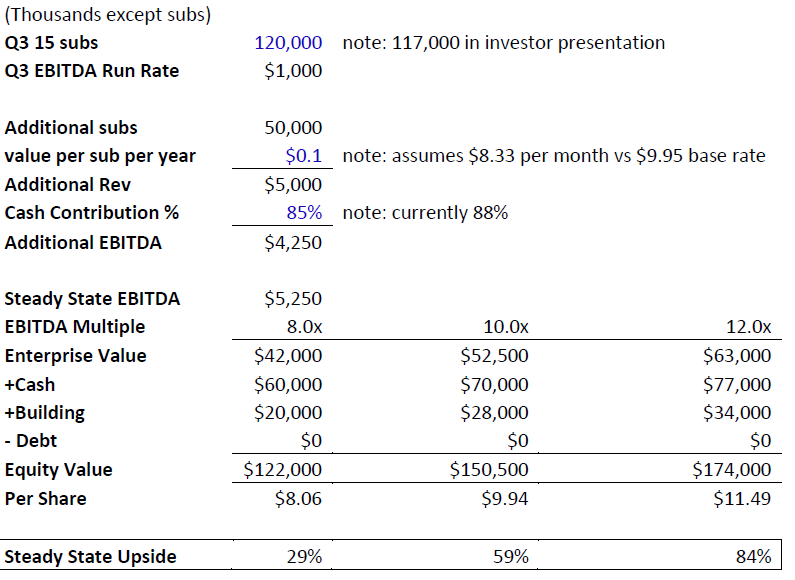

VOD – Theoretical Steady State

Valuing the VOD business as a going concern is no easy task. Skeptics will claim that at present GAIA resembles a venture capital investment following a fund raising round, where the risk is that the company will quickly burn through cash. There may be some legitimacy to this fear, although as discussed previously, this risk is tempered by the fact that nobody has more to lose than the skilled capital allocator at the helm. Perhaps more importantly though, the company has proven that the VOD business – which will lose money in the near term – could be profitable right now if they so choose. In fact, the business broke even in Q2 2015 and was profitable in Q3 2015 at run rate revenues of ~$14.5 million, while growing subscribers 30-35%. Profitability was a deliberate decision made by the company in advance of the contemplated spin-off between VOD and the yoga products business which was meant to isolate their respective values. According to the company, growth levels of 30-35% which would allow the company to be currently profitable require spending approximately 25% of a customer’s life time value on marketing.

However, the company does not plan to be profitable in the near term because they plan on ramping up marketing spend in order to return to subscriber growth rates of 50-85% per year, which they hit in 2014. According to the company, growing at this rate requires spending half of a customer’s life time value on marketing. In my view, aiming for this incredibly rapid growth is a bold decision that could only be made by an owner operator who is more concerned with long term value than pleasing Wall Street analysts in the short term. Additionally, it is worth noting that Rysavy has indicated that they never spend more than half of a customer’s life time value, which further insulates against the risk that the company will simply burn through their cash pile.

To understand the relationship between growth and short term profitability at GAIA, consider that under GAAP accounting, rapid revenue growth in a subscription business fuels near term operating losses, and thus topline growth – obviously a long term positive – is a negative contributor to the company’s earnings in the short term. This is because under GAAP, customer acquisition costs must be expensed immediately, while revenue from new customers is only recognized ratably. In simple terms with illustrative numbers, if a customer costs $50 to acquire, and spends $10 per month on a service once acquired, in the first quarter after the customer signs up the income statement will show revenue of $30, and cost of $50, for a loss of $20. However, the true value of the customer is not represented by this loss of $20, but rather by the present value of the revenue they generate over their lifetime. If a customer spends $10 a month for 12 months, revenue attached to this customer is obviously $120, while expense attached to this customer is $50, for a gain of $70. Rysavy himself has commented on this reality:

If you breakeven you can grow like 20% to 30%. Anything over that did, it’s investing into the new customers, because we don’t capitalize the customer so all the hits from the market [subtract]. So it — too much anything over like that 20% to 30% would take from the P&L.

– Jirka Rysavy, CEO – Q4 2015 conference call

As such, accurately valuing the business and its future growth requires investors to step away from the confines of GAAP and consider duration of subscription and customer churn. This is just common sense, but common sense is uncommon on Wall Street. Importantly for investors, the computer driven investing models that dominate the markets these days are incapable of making common sense distinctions when screening for stocks to buy, which helps explain why this opportunity exists.

The company does not fully disclose information on how long customers stick with the product or churn rates, but based on the company’s profitability in mid-2015, recent subscriber growth, and the company’s claims that new customers have 85% cash contribution margin, we can estimate what the business would look like today if they were to abandon plans to grow at 50-85% per year and focus on current profitability.

The company has indicated that in mid-2015 they were able to run-rate at $1 million in EBITDA (which in a capital light, debt free business with NOLs is a fair approximation for cash) with ~120,000 subscribers. Since then the company has added more than 50,000 subscribers who are presumably generating $100 in revenue per year.

Note that in mid-2015 when the company was profitable they were still growing subs over 25%, but for our purposes here we are calling this “steady state,” which should add an additional margin of safety. For reference and comic relief, consider that NetFlix trades at an EV/EBITDA of 160x. Clearly GAIA is not NFLX and will never trade at the same multiples, but the high side estimate of 12x vs. 160x seems sufficiently punitive to account for GAIA’s smaller total addressable market and smaller size, especially when one considers that at present GAIA has a customer relationship with less than 1.5% of their total addressable market, while NFLX has already accessed 25% of their total addressable market (estimates vary).

VOD – Growth Potential

Accurately predicting GAIA’s future would require perfect knowledge of customer acquisition costs, customer growth rates, churn rates, and duration, none of which are available to investors. Even with this information, it would be impossible to accurately forecast several years in the future. What is important is that whatever growth potential GAIA might have is free to current investors, yet it is likely to be very valuable. On a macro level, it seems clear that the trend toward Over The Top (OTT) television is only gaining speed. Additionally, there is a clear trend toward more nichey content and increasing evidence that consumers are willing to pay for it – for example, 60% of NFLX subscribers subscribe to more than 1 streaming platform, with 18% of households subscribing to 3 or more platforms.

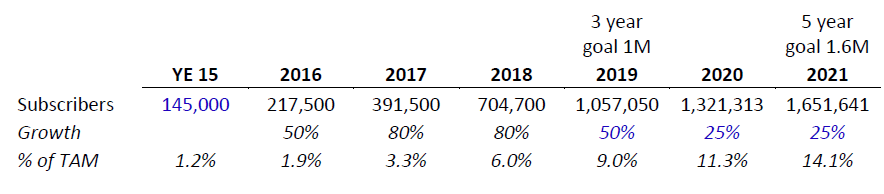

A GAIA initiated marketing study suggests that by 2020 there will be 300 million OTT subscribing households globally, with 165 million of those households interested in at least one GAIA topic. Of that 165 million, the company believes their total addressable market (TAM) is 11.5 million, or 7%. As of their most recent investor presentation, the company has set a goal of 1 million subscribers in 2019, and 1.6 million in 2021. To achieve these numbers, the company has forecasted growth of 50%, 80% and 80% in 2016, 2017 and 2018. According to the company, reaching these levels of growth requires spending approximately half of a customer’s life time value on marketing. Based on these estimates through 2018, we can estimate what the company believes growth may look like through 2021.

On their face, these numbers are obviously aggressive. However, the company is starting from a low base, is only now beginning to roll out foreign language service, and has proven they can grow at high rates in the past. For example, as of Q1 2016, the company was growing at a 90% annualized rate, well above their target of 50% for the year.

1.6 million subscribers is about 14% of what they have identified as their TAM which seems reasonable, if not conservative. For reference, the WWE (WWE) professional wrestling network currently has around 1.5 million subscribers. It seems reasonable to assume that globally there are more people interested in yoga and “seeking truth” than professional wrestling, although it is also likely they are less rabid than WWE fans.

If the company is able to reach 1.6 million subscribers, they believe they will achieve 85% gross margin, 90% cash contribution margin, and 40% pre-tax margin, which will generate $60 million in pre-tax income and $2.50 per share in earnings. Capital light, negative working capital businesses demand high multiples, even before considering growth, so I think P/E multiples in the range of 20-25x, implying a stock price of $50-62.50, are appropriate.

It is far from certain if the company can achieve these goals, and if they can, it will no doubt be a bumpy ride beset by setbacks. What is more certain however, is that at current prices investors are not paying for this potential growth, and in fact are arguably being paid to expose themselves to this potential growth.

Conclusion

GAIA is an investment opportunity with an extremely skewed risk/reward profile. The risk is protected by hard assets controlled by a clearly incentivized owner operator with an impressive track record, and the upside reward is the potential for 900% appreciation over the next 5 years. Importantly, this investment could be a success today if the company simply chose to reduce their growth rates.

Risks

– Competition from deep-pocketed new entrants

– Failure to rein in spending if it becomes clear that the growth strategy is not working

Disclaimer: This document, which is being provided on a confidential basis, shall not constitute an offer to sell or the solicitation of any offer to buy which may only be made at the time a qualified offeree receives a confidential private offering memorandum (“CPOM”) / confidential explanatory memorandum (“CEM”), which contains important information (including investment objective, policies, risk factors, fees, tax implications and relevant qualifications), and only in those jurisdictions where permitted by law. In the case of any inconsistency between the descriptions or terms in this document and the CPOM/CEM, the CPOM/CEM shall control. These securities shall not be offered or sold in any jurisdiction in which such offer, solicitation or sale would be unlawful until the requirements of the laws of such jurisdiction have been satisfied. This document is not intended for public use or distribution. While all the information prepared in this document is believed to be accurate, Laughing Water Capital, LP and LW Capital Management, LLC make no express warranty as to the completeness or accuracy, nor can they accept responsibility for errors appearing in the document. An investment in the fund/partnership is speculative and involves a high degree of risk. Opportunities for withdrawal/redemption and transferability of interests are restricted, so investors may not have access to capital when it is needed. There is no secondary market for the interests and none is expected to develop. The portfolio is under the sole trading authority of the general partner/investment manager. A portion of the trades executed may take place on non-U.S. exchanges. Leverage may be employed in the portfolio, which can make investment performance volatile. The portfolio is concentrated, which leads to increased volatility. An investor should not make an investment, unless it is prepared to lose all or a substantial portion of its investment. The fees and expenses charged in connection with this investment may be higher than the fees and expenses of other investment alternatives and may offset profits. There is no guarantee that the investment objective will be achieved. Moreover, the past performance of the investment team should not be construed as an indicator of future performance. Any projections, market outlooks or estimates in this document are forward-looking statements and are based upon certain assumptions. Other events which were not taken into account may occur and may significantly affect the returns or performance of the fund/partnership. Any projections, outlooks or assumptions should not be construed to be indicative of the actual events which will occur. The enclosed material is confidential and not to be reproduced or redistributed in whole or in part without the prior written consent of LW Capital Management, LLC. The information in this material is only current as of the date indicated, and may be superseded by subsequent market events or for other reasons. Statements concerning financial market trends are based on current market conditions, which will fluctuate. Any statements of opinion constitute only current opinions of Laughing Water Capital LP, which are subject to change and which Laughing Water Capital LP does not undertake to update. Due to, among other things, the volatile nature of the markets, an investment in the fund/partnership may only be suitable for certain investors. Parties should independently investigate any investment strategy or manager, and should consult with qualified investment, legal and tax professionals before making any investment. The fund/partnership is not registered under the investment company act of 1940, as amended, in reliance on an exemption there under. Interests in the fund/partnership have not been registered under the securities act of 1933, as amended, or the securities laws of any state and are being offered and sold in reliance on exemptions from the registration requirements of said act and laws. The S&P 500 and Russell 2000 are indices of US equities. They are included for informational purposes only and may not be representative of the type of investments made by the fund.

About The Author: Matthew Sweeney

Matthew Sweeney is the Founder and Managing Partner of Laughing Water Capital. The firm employs a concentrated equity strategy while focusing on companies that are dealing with some sort of structural or operational difficulty that is judged to be easily solved by an incentivized management team if given enough time. Matt began his career at Cantor Fitzgerald where he focused on equity idea generation for institutional clients. He received a Bachelor of Arts degree in History from the College of the Holy Cross, and a Masters degree in International Relations focused on the Middle East and Terrorism from Seton Hall University. Matt is a Chartered Financial Analyst (CFA), and former Vice Chair of the New York Society of Security Analysts (NYSSA) Value Investing Committee.

More posts by Matthew Sweeney