This article is authored by London-based MOI Global instructor Massimo Fuggetta, founder, chairman and chief investment officer of Bayes Investments, advisors to the Made in Italy Fund, a mutual fund exclusively focused on Italian small-cap stocks.

Massimo authors the popular Bayes blog, named after Presbyterian minister and mathematician Thomas Bayes, who, in An Essay Towards Solving a Problem in the Doctrine of Chances, first formulated the theorem that bears his name.

Lord Darlington. What cynics you fellows are!

Cecil Graham. What is a cynic? [Sitting on the back of the sofa.]

Lord Darlington. A man who knows the price of everything and the value of nothing.

Cecil Graham. And a sentimentalist, my dear Darlington, is a man who sees an absurd value in everything, and doesn’t know the market price of any single thing.

(Lady Windermere’s Fan, Third Act)

The value of an asset is the discounted sum of its future payouts.

This definition is essentially tautological. All it says is that a tree is worth the fruits it bears, and that an apple for sure today is worth more than an apple maybe tomorrow. For most financial assets, payouts are in cash, so we say their value is the discounted sum of future cash flows, or DCF. But payouts can be non-monetary: Gold and works of art, for instance, repay the owner with security or pleasure. Live-in properties spare their owners the payment of a rent. I leave it to you to figure out the payouts of Bitcoin.

Payouts should not be confused with the proceeds from the sale of an asset. A sale just transfers the right to the payouts from the seller to the buyer. It is an exchange at an agreed price. The price might be higher or lower that what the seller paid to acquire the asset. But the entailed gain or loss comes from the sale, not from the asset. Who would buy a fruitless tree, if not with the intent to sell it to a greater fool who would also buy it for the same purpose?

Investors do not, or should not, disagree on what value is. But they do differ in the use they make of the concept, and in particular in the distinction they make between value and price. In this respect, we can divide them into three groups:

1. Grahamians. They place great significance on the concept of value, as distinct from the notion of price. They believe that values can and often do differ from prices.

2. Cynics. They place no significance on the concept of value. They believe there are no values, only prices.

3. Bogleheads. They are indifferent to the concept of value. They believe that, apart from some fleeting anomalies, there is no difference between values and prices.

Notice the similarity between Grahamians and Bogleheads: they both believe there is a magnetic force attracting prices to values. But Grahamians see the force as weak and variable, thus allowing other forces to open gaps between values and prices. While Bogleheads see it as strong and overpowering, thus preventing any significant gaps to open in the first place.

Cynics, on the other hand, believe there is no such a thing as value. They think prices are subject to various forces, but value magnetism is not one of them. In this sense, then, there is also a similarity between Cynics and Bogleheads: they both ignore value. Cynics see it as a pointless concept. Bogleheads think that, whatever it is, it is inseparable from price.

Their ignorance shows up whenever Cynics and Bogleheads talk about value. The most common misconception that unites them is the confusion between value and valuation. This is typically exemplified by their definition of a ‘value’ asset – e.g. a company stock – as one exhibiting a low ratio between its market price and some item on the company’s balance sheet, such as Net Income and Shareholders Equity. A ‘value stock’ – so they say – is one with a relatively low Price/Earnings or Price/Book Value ratio. Notice this is not what they believe: remember Cynics think there is no such a thing as value, and Bogleheads do not distinguish between value and price. But it is what they believe Grahamians think is a ‘value stock’. That is, they believe Grahamians think that value can be reduced to some function of E and BV, and that, therefore, a low P/E or P/BV is an appropriate measure of the gap between value and price.

This is obviously a gross misrepresentation. Any self-respecting Grahamian knows that “The whole idea of basing the value upon current earnings is inherently absurd“. The value of an asset is the discounted sum of its future payouts, and a company’s stream of payouts depends on its ability to earn a return on equity above its cost of capital, and on the value of equity increases accruing from its future investments (here is a sketch of how I look at it). To say that the value of a company can be represented by a number on its balance sheet is like saying that the value of an apple tree can be gauged by the look of one of its apples.

Still, the idle notion that lower P/E or P/BV stocks are ‘value stocks’ is pervasive, even beyond Cynics and Bogleheads. And so is the even sillier notion thar higher P/E and P/BV stocks are ‘growth stocks’. Worse, asset managers whose portfolios have stocks with lower than average valuation ratios are labelled ‘value managers’, while those invested in stocks with higher than average ratios are marked as ‘growth managers’.

Serious Grahamians know this is nonsense. A value stock is one whose true value is significantly higher than its market price. This has nothing to do with lower valuation ratios. Obviously, given anything at the denominator, a lower ratio means a cheaper stock – believe it or not, paying a lower price is better than paying a higher price. But a value stock can have any valuation ratio, including a negative P/E if a company is currently loss-making, or a high P/E if earnings are temporarily depressed or if they are deemed to grow at a fast pace in the future. Conversely, a low P/E or P/BV stock is not necessarily a value stock, as it may be a value trap, i.e. a stock whose true value is even lower than its low price.

Thus value versus growth is a false dichotomy, and the ensuing categorization of stocks and asset managers based on valuation ratios is a persistent source of confusion.

Far from being a semantical subtlety, the value-growth jumble has real consequences. As it is often the case, much of it revolves around the cynical Bogleheads duo par excellence, Eugene Fama and Kenneth French. Under pressure from an avalanche of empirical failings of the Efficient Markets Theory and the associated Capital Asset Pricing Model, in the early 1990s the duo came up with a Three-Factor Model, with the objective of ‘explaining’ the behaviour of stock returns while salvaging the totem of market efficiency. One of the three factors in the model is HML, which stands for High Minus Low book-to-market ratio. In their words: ‘Returns on high book-to-market (value) stocks covary more with one another than with returns on low book-to-market (growth) stocks’ (Fama and French, JEP, 2004, p. 38). That’s it: low P/BV=value stocks, high P/BV=growth stocks.

The other cornerstone of the model is SMB, or Small Minus Big: ‘Returns on the stock of small firms covary more with one another than with returns on the stocks of large firms’. Unlike HML, SMB does not carry a semantic baggage – small and large are just that: different market capitalisations. But they both have the same connotation: they are risk factors. Ever obedient to their EMT faith, Fama and French do not imply that investors should buy low P/BV ‘value’ stocks and small cap stocks: what they are saying is that the extra return they would get by doing so is ‘explained’ by the usual all-embracing EMT panacea: extra risk. Nevertheless, since the Fama-French launch, a flood of evermore plethoric ‘Multifactor models’ has generated a whole industry of ‘Factor Investing’. Their overt message to investors: we’ll get you better returns. Their covert message – often obscure to ‘factor’ investors themselves: we’ll get you extra returns by exposing you to extra risk.

The mantra ‘A higher return always comes with a higher risk’ is the central pillar of the EMT. Factor investors get sucked into it by construction: they are more or less self-aware Bogleheads. Cynics are cynical: they know their trades can go wrong, and hedge their bets accordingly. Plus they know that the more they bet, the higher their gain or loss – and leave it at that. But Grahamians are cerebral. They ask: what is risk? And why should it be positively related to expected return? Their view on the subject is very different from the EMT mantra. They define risk as the probability of a permanent loss of capital, and think that more risk means a lower, not a higher probability-weighted expected return. To a Grahamian the risk of an asset is proportional to the size of the gap between its true value and its market price. The wider the gap, the bigger is the Margin of Safety of an investment, and the lower its risk. A bigger Margin of Safety increases the magnetic force that attracts price to value. Of course, value can change, in a positive or negative direction, and so can its assessment. Hence the investment is and remains risky, despite the size of the value gap. But why should that risk have anything to do with P/BV or market cap?

Fama and French’s reasoning about P/BV is disarmingly circular. They essentially say: a low P/BV means that the market is placing a relatively low value on the company’s equity. This must be because the market considers the company riskier. That is: a company is riskier because the market says so. Or: The company is riskier because it has a low P/BV, and it has a low P/BV because it is riskier. This wouldn’t pass Excel. As roundabout as it is, however, the P/BV argument bears at least some relation to price and value. But what about size? Why should a small company be riskier that a large company? Here the argument reiterates the flimsy sophistry used to ‘explain’ Rolf Banz’s (1981) size effect: small companies are riskier because they are younger and therefore more fragile, while large companies are safer because they have been around for longer and are therefore more robust. No matter their price or value. So for instance the small caps in our Made in Italy Fund are a lot riskier than Tesla. Oh well.

Like factor investors, Grahamians want to get better returns – but with less risk, not more. This raises the outrage of EMT faithful, to which the proposition is anathema. Better than what? – they ask, with the smug assurance that, whatever the answer, it will be wrong. Well – say Grahamians – better than the average returns of asset managers investing in the same universe. So, for example, if we invest in US stocks our aim is to get significantly better returns than other US managers – not every quarter or even every year, but certainly over a 5-to-10-year period. Before you say so, that includes passive investing Bogleheads, whom, we agree with you, are strong contenders, as they tend to get better than average after-costs returns. And since all that Bogleheads do is to replicate the composition of some index – the S&P500 in the case of US stocks – we also want to outperform the index. And look at our track record: that’s what we have done – say successful Grahamians (it should go without saying that it is not enough to call oneself a Grahamian to be a successful investor).

Ah, but which index? – is the standard retort. Echoing the Three-Factor Model, an army of index providers and performance analysts use intricate grids of boxes to place funds and fund managers along HML and SMB spectrums. The most prominent is SPIVA – S&P Indices Versus Active. For each fund they ask: is it Value, Growth, or Core? Is it Large Cap, Mid Cap, Small Cap, or Multi Cap? Their message: When placed in the right box (or ‘style’, in their ludicrous parlance), most ‘active’ funds underperform their assigned index.

Grahamians shrug off such classifications. They think value versus growth is a misnomer, and they don’t regard market cap as a relevant criterion to assess the true value of an investment. Still, their funds are forced into one of the boxes, based on the HML and SMB scores of their holdings. And – like Native Americans protesting against being called Indians – Grahamians rejecting this nonsense are simply ignored.

This messy Babel can be traced back to Grahamians’ characterisation of one of the major forces they see as creating gaps between true values and market prices: the average investor’s tendency to be carried away by sentiment. As Benjamin Graham put it: the stock market is a voting machine rather than a weighing machine. This works both ways: negative sentiment can push stock prices below true values and positive sentiment can pull them above. Grahamians are attracted by the former: in this sense, they tend to regard low valuation ratios as a sign of excessive pessimism. But only a lazy Grahamian would confine himself to simply casting a net amidst low ratios in the hope of catching as many value stocks as possible. A serious Grahamian would perhaps screen for low ratios, but would thereafter know that his job has, if anything, just started. Likewise, Grahamians are deterred by positive sentiment, which – as an earlier Graham, Cecil, put it – sees an absurd value in everything and knows the price of nothing. Hence they tend to regard high valuation ratios as a sign of excessive optimism. But again only a lazy Grahamian would stop there and simply avoid high valuation stocks. A serious Grahamian would be interested in them and would want to check whether high ratios are perhaps justified by high true values, possibly above market prices.

In doing so, he is aware that excess optimism is a tougher nut to crack than excess pessimism. When excess pessimism drives a stock price below what a Grahamian thinks is its true value, all he needs to do is to buy the stock and wait for value magnetism to work. If it doesn’t, he needs to decide whether to wait a bit longer or admit he has caught a value trap, take a loss and move on – an error of commission. But when excess optimism drives a stock price above its supposed true value, a Grahamian will either do nothing or, if he is so inclined, short the stock, again waiting for value magnetism to take effect. If it doesn’t, however, being short means dealing with a time-sensitive, potentially indefinite and expanding loss. And, if he is not short, he needs to deal with the growing anxiety of having missed the boat – an error of omission that many Grahamians who never managed to bring themselves to buying Amazon are sorely familiar with. In addition, while the value that excess pessimism tends to neglect is often a hard, tangible one, embedded in existing assets, the value that excess optimism tends to overblow is usually an uncertain, impalpable, non-linear condensation of future growth opportunities. Grahamians are naturally more confident dealing with the former and more sceptical about dealing with the latter: value traps are bad enough, but growth traps – where one surrenders to sentimentalism and buys a meteor only to see it crushing down to earth – can be devastating. Yet, a serious Grahamian knows he needs to handle both risks, and that his job is a great deal more complicated than the lazy reliance on a couple of balance sheet numbers.

So there it is: Cynical Bogleheads think that all Grahamians are as lazy and disinterested in value as they are. They aren’t.

These considerations have been inspired by Aswath Damodaran’s three posts on Value Investing.

Like many, I am a regular reader of Damodaran’s blog. I find his posts interesting, sharp and thought-provoking. So were the Value Investing posts. I thought, however, they were marred by some degree of confusion, which I would like to address.

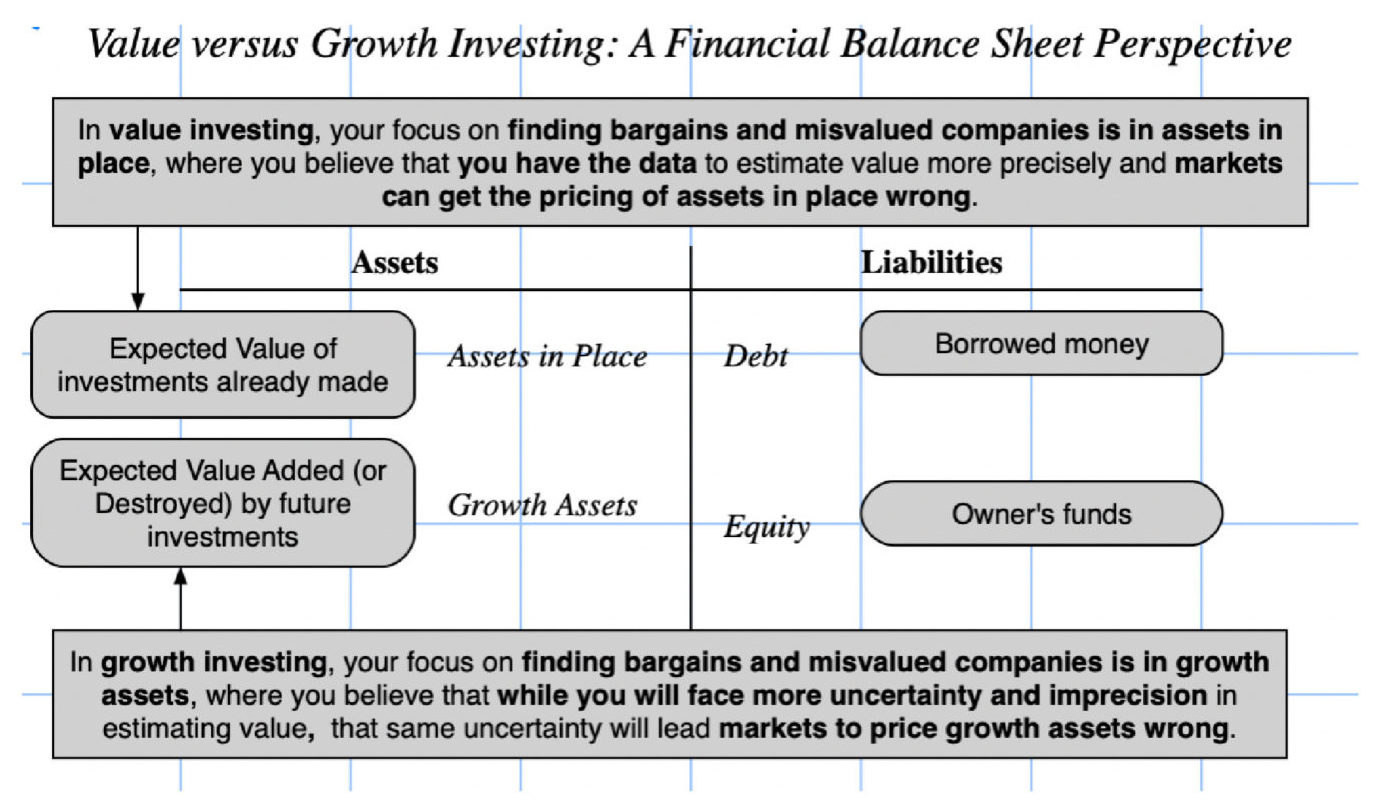

The first post sets the stage with the following picture, which Damodaran puts forward as a general approach that encompasses his other classifications of Value Investing:

Value Investing is defined as the search for bargains that arise when the market undervalues a company’s existing assets. This is contrasted with Growth Investing, defined as the search for bargains that arise when the market undervalues a company’s growth assets, i.e. assets that are currently not in place but are expected to be generated by future investments.

As I said in my post, I think this is a false dichotomy. As Damodaran himself puts it: ‘the contrast between value and growth investing is not that one cares about value and the other does not’. Investors who care about value are all Grahamians: they invest in stocks where they see a significant gap between true values and market prices, irrespective of whether such values derive from current or future assets.

Grahamians believe that Mr Market can be carried away by sentiment – excess pessimism that drives market prices below true values and excess optimism that drives them above. Depending on the company, true values can be mostly embedded in existing assets or mostly condensed in future assets – or a varying combination of the two. The difference is that assets in place are, to an extent, observable and quantifiable, whereas assets-to-be are not. But Mr Market can misjudge both, and in both directions. It can undervalue current assets, thus presenting a bargain to a Grahamian who can properly quantify them; or it can undervalue future assets, thus providing an investment opportunity to a Grahamian who is able to anticipate the value creation to be brought about by future investments. The first is a more common image of a Value Investor. But the second is as much a Value Investor as the first, and to call him a Growth Investor is a persistent source of confusion. Likewise, Mr Market can overvalue current assets as well as future assets, thus prompting a Grahamian who can see the mistake to stay away from them or, if so inclined, short them. Here the common image is that of a Value Investor shunning the sentimentalism of Pindaric flights of fantasy that exalt future growth opportunities while neglecting gravitational threats. But avoiding investment in overvalued current assets is as much a trait of an accomplished Grahamian.

The observability of current assets explains why Grahamians are more comfortable dealing with them rather than with the inherent impalpability of growth assets. The value of current assets can be measured – Book Value being its coarsest approximation – while growth assets can’t. But, as we know, ‘Not everything that can be counted counts, and not everything that counts can be counted.’ Valuing growth opportunities is more difficult, rife with uncertainties and therefore more prone to error. But serious Grahamians accept the challenge – indeed that’s what Damodaran does regularly and expertly, in his blog and elsewhere. He himself is the proof that value versus growth is a false dichotomy!

Hence it is puzzling to see him sticking to it in his second post, where he embarks in an historical evaluation of their relative performance, based on the flawed classification: low P/BV=value stocks, high P/BV=growth stocks. Damodaran recognises that P/BV is just a proxy for value, and that ‘low PE and low P/BV stocks would not be considered true value investing, by most of its adherents’. Indeed, in his first post he defines low multiples investing as ‘Lazy Value Investing’ – a term I borrowed in my post – as opposed to ‘Cerebral Value Investing’, where screening for low multiples may be the starting point but final choices depend on a host of other criteria. But then in the second post he uses SPIVA data to show that most mutual fund managers who claim to adhere to Value Investing fail to beat their assigned value index. That is: most Cerebral Value Investors underperform Lazy Value Investing. Notice that, with equivalent Bogleheaded simplicity, one can use the same SPIVA database to show that most mutual fund managers who claim to adhere to Growth Investing fail to beat their own assigned index. That is: Cerebral Growth Investors underperform Lazy Growth Investors (or Crazy Growth Investors – a better term for investors who would purposely buy high multiples stocks).

An erudite Grahamian like Professor Damodaran should not be drawn into these fruitless comparisons. There is no Value versus Growth Investing, no Value versus Growth performance or Value/Growth cycle. Value does not ‘work’ according to whether low multiples stocks outperform high multiples stocks. Value always works: it is the central concept to a Grahamian investor who believes that it can and often does differ from market prices. Whether a company’s value resides more in its current assets or in its growth assets depends on the company, not on the investor.

Indeed, this is the focal point of Damodaran’s third post, where he calls for a ‘Reinvention’ of Value Investing. It seems to me, however, that what he proposes as ‘A New Paradigm for Value Investing’ is nothing more than what serious Value Investing has been all along, once one looks at it without the distorting lens of the spurious value/growth opposition. In fact, one can take Damodaran’s first post picture we started with and label it ‘Value Investing’ rather than ‘Value versus Growth Investing’. Or – in the name of Reinvention – name it Grahamian Investing, in homage to its chief architect, who, with a touch of condescension, preferred to call it Intelligent Investing.

Grahamian Investing is a great deal more complicated than careless academics – who have no qualms calling low multiples stocks ‘value stocks’ and concocting a ‘factor’ out of them – purport it to be. They should go back (or go) and read Chapter 1 of Security Analysis: ‘It is a great mistake to imagine that intrinsic value is as definite and as determinable as is the market price’. Grahamians are aware that value is an elusive concept, impervious to exact appraisal: ‘There is no such thing as the “proper value” of any given common stock’, and therefore there is no readily quantifiable value parameter – despite academics, index providers and performance analysts pretending otherwise. That is why Grahamians place as much significance on the concept of Margin of Safety. They don’t need to know the exact value of an asset, but they want to make sure – as much as they can – that such value is considerably higher than the market price, i.e. that there is a comfortably ample gap between value and price. Equivalently, they want to minimise the probability that the market price is right.

Grahamians regard the Margin of Safety as the most appropriate measure of investment risk. The wider the Margin of Safety, the lower is the probability of a permanent loss of capital. In this respect, Damodaran rightly observes that ‘the margin of safety comes into play only after you have valued a company, and to value a company, you need a measure of risk’. But it should be obvious to a Grahamian that none of the common measures of risk – standard deviation, beta and all their CAPM-derived ratios – are of any use. These are proper measures of risk only in a Boglehead world, where values coincide with prices, markets are efficient and higher returns are ‘explained’ by higher risk. In a Grahamian world there are many risks, but they have to do with real things like business conditions, competitive threats, accounting accuracy, balance sheet integrity, management skills, and many others, none of which are accurately quantifiable. That is why the Margin of Safety needs to be wide enough to accommodate them.

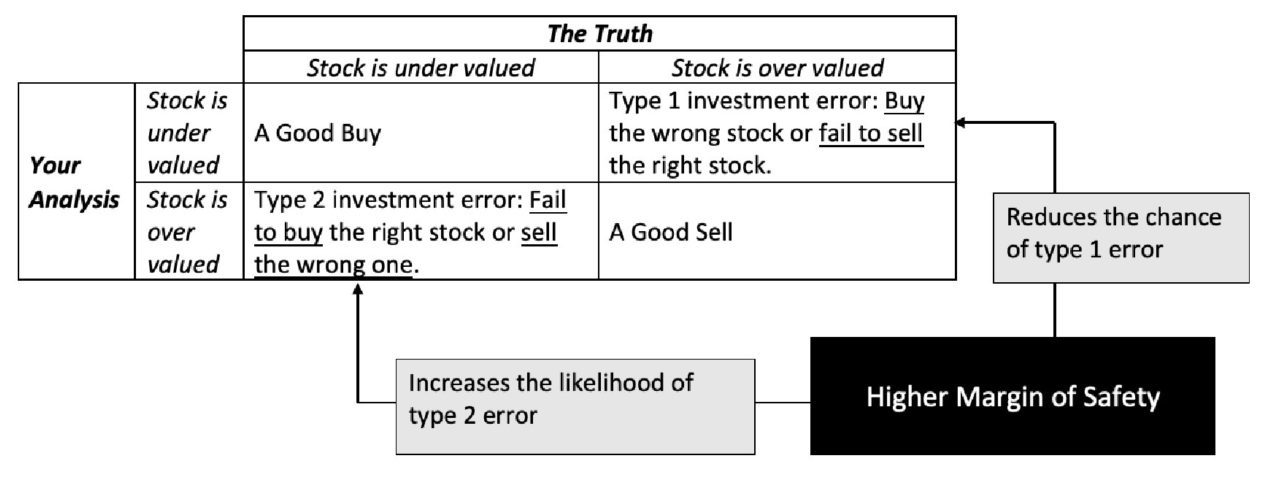

The Margin of Safety determines the real risk/reward trade-off facing a Grahamian investor. If he sets it too narrow, he increases the risk of buying a dud – a value trap or a ‘growth’ trap – thus losing capital, time or both. If he sets it too wide, he increases the risk of holding too much cash and performing poorly. The trade-off is depicted in the following picture on Damodaran’s third post:

It is essentially the same picture I presented (almost nine years ago – scary) in my Pearls and pebbles post. A Grahamian’s primary concern is to avoid a Type I error – a False Positive. It is Warren Buffett’s Rule No. 1: Never Lose Money or, as I called it, the Blackstone Principle of Intelligent Investing. But that needs to be balanced with a secondary concern: to avoid a Type II Error – a False Negative. We can call it Rule No. 2: No pain, no gain.

In order to avoid a Type I error, the Margin of Safety needs to be wide enough. As Warren Buffett put it: better ten strikes than one wrong swing. But to avoid a Type II error the Margin of Safety cannot be too wide: no swing, no return. The first is an error of commission – make an investment that turns out to be wrong. The second is an error of omission – decline an investment that turns out to be right. A Grahamian investor needs to find the right balance between the two – a much more meaningful decision than the sterile and potentially dangerous return/volatility trade-off prescribed by ‘efficient’ frontiers.

This is only one of the many dimensions in which Grahamian investors – which are often wrongly depicted as a homogeneous bunch – differ from one another. In fact, we come in many shapes and forms: different focus, interests, temperament, risk attitude, portfolio construction rules and, of course, experience, track records and success. But one thing unites us: we place great significance in the concept of value, as distinct from the notion of price. This sets us apart from Cynics, who believe there are only prices, and Bogleheads, who believe there is no difference between the two. I believe that this tripartite classification fills the space of mutually exclusive ‘investment philosophies’, and that all other finer distinctions can be traced back to one of the three groups.

One last point, where I thoroughly agree with Professor Damodaran. While I naturally sympathise with the Value Investing community, I share his view that it has a tendency to become rigid, ritualistic and righteous.

1. Rigid. These are what we have called ‘lazy value investors’, stuck to simplistic and restrictive rules based on current accounting measures, impervious to venturing into any consideration of future growth assets, and thus worthy of the disparaging caricature that academics, Cynics and Bogleheads make of them.

2. Ritualistic. Like Damodaran, I have made the pilgrimage to Omaha only once, to satisfy my curiosity. I have enormous admiration and respect for Warren Buffett but much less for his devotees, who hang on his every word and are incapable of any criticism, even when the oracle is evidently wrong.

3. Righteous. As embarrassingly obvious as it is, some investors need to be reminded that calling oneself a value investor is not enough to be a successful one. ‘Value always works’ does not mean that every value investor is able or entitled to make it work.

So here is my proposal to reinvent and reinvigorate Value Investing: let’s call it Grahamian Investing.

About the author:

Massimo Fuggetta is the founder, Chairman and Chief Investment Officer of Bayes Investments.

Massimo started his investment management career in 1988 at JP Morgan Investment Management in London, where he rose to become Head of the Global Balanced Group, with responsibility for international balanced portfolios. In 1999 he left JPMIM to become Chief Investment Officer, Director General and then CEO at Sanpaolo IMI Asset Management in Milan. He left the company in 2001 to start Horatius, an investment advisory company incorporated in 2004, which in 2007 became an asset management company. He left Horatius in 2012 to go back to London, where in 2014 he founded Bayes Investments.

Massimo holds a Doctorate (DPhil, 1991) and Master’s Degree (MPhil, 1987) in Economics from the University of Oxford. He graduated in Economics at LUISS, Rome in 1984. He taught Behavioural Finance in the Master in Economics course at Bocconi University in Milan in 2000-2002 and in the same period served in the Editorial Board of the Financial Analysts Journal.

In 2012 Massimo started the Bayes blog, which has acquired popularity in the Value Investing community.

About The Author: Massimo Fuggetta

Massimo Fuggetta is the founder, Chairman and Chief Investment Officer of Bayes Investments. Massimo started his investment management career in 1988 at JP Morgan Investment Management in London, where he rose to become Head of the Global Balanced Group, with responsibility for international balanced portfolios. In 1999 he left JPMIM to become Chief Investment Officer, Director General and then CEO at Sanpaolo IMI Asset Management in Milan. He left the company in 2001 to start Horatius, an investment advisory company incorporated in 2004, which in 2007 became an asset management company. He left Horatius in 2012 to go back to London, where in 2014 he founded Bayes Investments.

Massimo holds a Doctorate (DPhil, 1991) and Master’s Degree (MPhil, 1987) in Economics from the University of Oxford. He graduated in Economics at LUISS, Rome in 1984. He taught Behavioural Finance in the Master in Economics course at Bocconi University in Milan in 2000-2002 and in the same period served in the Editorial Board of the Financial Analysts Journal.

In 2012 Massimo started the Bayes blog at www.massimofuggetta.com, which has acquired popularity in the Value Investing community.

More posts by Massimo Fuggetta