“Markets can remain irrational longer than you can remain solvent” –John Maynard Keynes

The investment environment continues to be challenging. I hauled out Keynes’ comments again—I’ve used this quote before, but it seems appropriate now. We find new companies every day in which to invest. The only problem is the stock prices are out of whack. Which is my technical term for being overvalued. We just need an extra helping of patience in this environment.

After eight years of upward-marching markets, the key in our view is to usually be wary of market darlings, and seek opportunity in neglected or downtrodden areas. This approach hasn’t paid for a number of years, but markets have a way of changing just when the status quo seems inviolable.

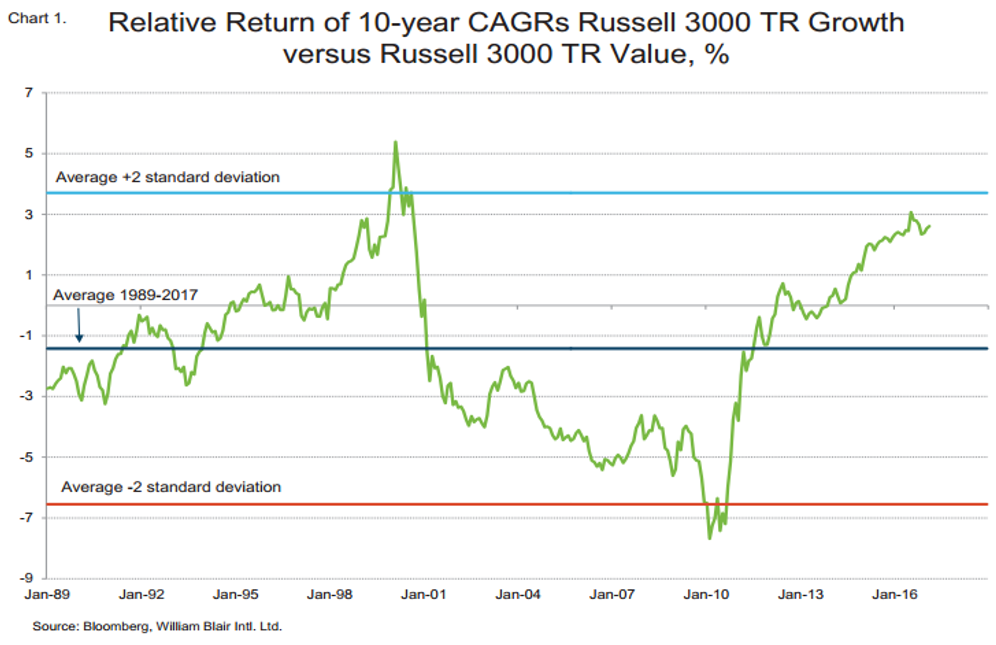

The chart below illustrates our thinking regarding risks and opportunities. It depicts the differences in relative returns between two schools of investment thought—Growth and Value. While we aim for both growth and value, many investors still divide the world into these two competing camps.

Growth stocks have earned around 3% per year more than Value stocks for the past 10 years. The “norm” for Growth stocks? Around 1% per year less than Value stocks over the past almost 3 decades. There’s this little thing called “reversion to the mean”, which in this case means years of outperformance can lead to years of underperformance. Likewise, weak performance can be followed by stronger results. This happens because investors tend to overestimate future growth prospects, while avoiding businesses with moderate or lackluster current results. Eventually the world reverts to long-term equilibrium valuations. The chart below demonstrates, and Mr. Keynes succinctly describes the challenge for investors—it can take years for reversion to occur:

Why the investor fixation on Growth stocks for so many years? It’s no coincidence that the period of Growth outperformance corresponds to the slow-growth world since the Global Financial Crisis of 2008. A variety of reasons have been offered for this state of affairs. These include weakened financial institutions unable or unwilling to lend, an aging global population reluctant to spend, and widespread consumer and government indebtedness, contributing to a subdued global economy.

In response, investors have sought companies demonstrating the ability to grow despite weak global growth. “Growth” stocks have been the place to be, as the previous chart demonstrates. Only the equally ebullient “dot-com” boom of the late 1990’s has shown such strong demand for Growth stocks compared to “Value” stocks, as the chart on the previous page also shows.

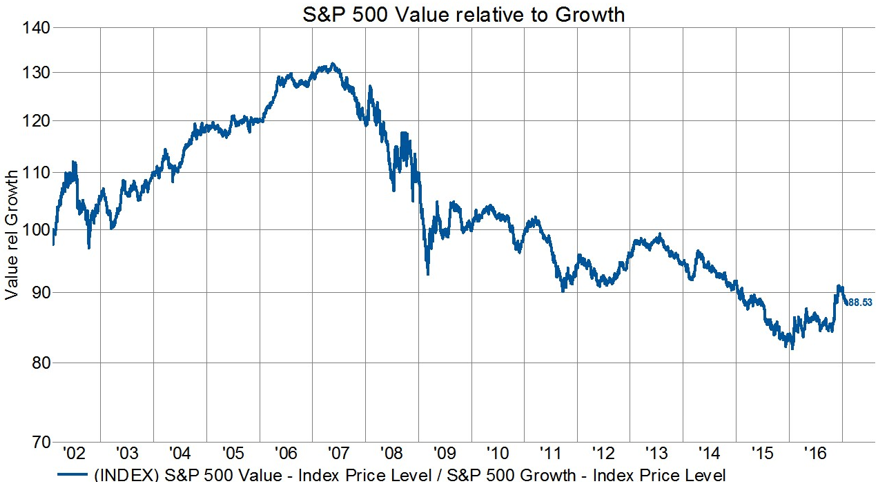

The chart below depicts the same phenomenon from the opposite vantage point—the downward trend since 2007 depicts weakness for Value stocks relative to Growth. According to this measure, it’s been a Growth-led market for the past ten years:

What’s a growth stock, you might ask? Companies with above-average growth prospects, usually in businesses with lots of apparent long-term promise. Areas such as Technology, Healthcare, Social Media, etc. I’d add, with investors who don’t pay as much attention to the price being paid to invest. The rationale? “I don’t have to pay attention to the valuation, this company is gonna grow for years!” Sometimes that’s correct. But history has shown that frequently, it’s wrong.

In contrast, value stocks represent more mundane enterprises. Think Industrials, Energy, Financials, Materials, etc. Fuddy-duddy stuff for some folks. Slower growth, or companies with temporary business challenges, usually with more modest valuations. As in many aspects of life, it’s a trade-off.

Now, you might be wondering, who wouldn’t like a heaping helping of growth? We love growth, as it’s hard to earn a return from a business that doesn’t grow over long periods of time. But growth has a price, and lately many investors have ignored the cost of acquiring growth in the stock market.

Warren Buffett has said, “you pay a very high price in the stock market for a cheery consensus”. Which means, be careful how much you pay for growth. Many investors, hoping to catch the next big thing, have ignored valuations and piled into a relatively narrow group of high-growth businesses, irrespective of the asking prices for participation.

It might seem difficult to avoid such temptations, but we strive to be rational and invest your capital when the rewards seem appropriate given the risks. Put another way, when the price paid represents a significant discount to our expectations for future business value. And no more than that.

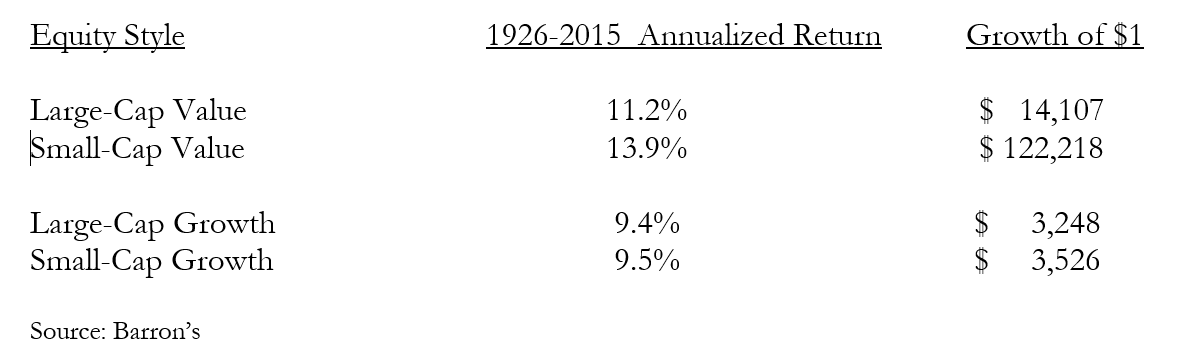

We believe history is on our side. The returns from various investing styles look like this:

As can be seen, the Value style has trounced Growth over the past nine decades. Large or small company, it doesn’t matter. While the differences look small, over nine decades they’re enormous, as the growth of a single dollar over that period demonstrates.

How can that be? Shouldn’t higher growth lead to higher returns? Theoretically, yes. Practically speaking, no. What gets in the way is that old bugaboo, human nature. Investors tend to bid growth stocks up to irrational levels. But that’s only part of the problem. In our competitive capitalist system, investors also overestimate the ability of a company to sustain high growth rates for a long period of time. Capitalist competition works. The result? High prices get paid for growth that often disappoints.

We don’t know when these conditions will change, although given it’s been almost eight years we’re due for a change in leadership. But, perhaps we’ve entered a new era of sustainable growth as far as the eye can see. But the four most dangerous words in the investing world are these: “it’s different this time”. Just when investors start to believe this, is when investors are about to get their proverbial heads chopped off.

Our stock portfolios today could be classified as firmly in the Value camp, and we own both Large and Small companies among our holdings. We like our odds over the next few years.

This post has been excerpted from a letter of Triad Investment Management.

The securities discussed herein do not represent all of the securities purchased, sold or recommended for each strategy during the quarter. The reader should not assume that an investment in these securities was or will be profitable. Inherent in any investment is the possibility of loss. Past performance is no guarantee of future results.Triad Investment Management, LLC claims compliance with the Global Investment Performance Standards (GIPS®). Triad has been independently verified by Ashland Partners & Company, LLP for the period from the strategy’s inception, April 30, 2008, through December 31, 2016. Triad is an SEC-registered investment adviser. The composite includes all fully discretionary separately managed accounts that follow the firm’s Concentrated All-Cap Equity investment strategy, including those accounts no longer with the firm. Triad’s strategy is to invest in a concentrated portfolio (usually holding 20 to 30 securities) of common stocks, unrestricted as to market capitalization, of both domestic and international companies. The U.S. Dollar is the currency used to express performance. Past performance is not a guarantee of future results, and there is a risk of loss in investing in equities. Results are presented net of fees and include the reinvestment of all income. Investments made by Triad for its clients differ significantly in comparison to the referenced indexes in terms of security holdings, industry weightings, and asset allocations. Accordingly, investment results and volatility will differ from those of the benchmarks. As of June 30, 2013, the Triad Equity Composite was renamed the Concentrated All-Cap Equity Composite. For more information or for a copy of the firm’s fully compliant presentation and the firm’s list of composite descriptions, please contact us at (949) 679-3991.

About The Author: John Heldman

John Heldman brings over 30 years of experience to the management of investment portfolios. Prior to founding Triad, he was a Senior Vice President and Portfolio Manager with Neuberger Berman. John has also managed institutional and individual investment portfolios for Deutsche Bank, Scudder Investments and Bank of America, including managing equity funds and serving on the Equity Strategy Committee. He obtained his Bachelor of Science degree in Finance and Master of Business Administration from California State University, Long Beach. John is a CFA charterholder, and a member of CFA Institute and CFA Society Orange County.

More posts by John Heldman