This article is authored by MOI Global instructor Henrik Andersson, partner and fund manager at Didner & Gerge, based in Stockholm.

Aalberts is a €5 billion market cap Dutch-based corporation involved in a number of attractive end-markets with a strong environmental focus that the company articulates very well. More than 65% of sales can be traced directly to four sustainable development goals, which will steadily increase not the least because of 100% of capex being directed into these products and services.

The company is active towards four end markets

- Eco-friendly buildings

- Semicon efficiency

- Sustainable transportation

- Industrial niches

We believe the company has just begun its journey towards quality-industrial type margins and profitability. Furthermore, this is a company that is not that well-known outside of the midcap-crowd in Europe, but have every opportunity to change that during the next mid-term plan which we expect to be presented at the company’s CMD in December, 2021.

Aalberts was founded in 1975 by Jan Aalberts, with a base in the steel industry that dominated a lot of the Benelux industrial scene at the time. Think Arcelor and its satellite suppliers. Slowly the company branched out into other areas – piping systems for buildings for instance – and these efforts were multiplied starting in 2012 when the current CEO Wim Pelsma succeeded Mr. Aalberts.

We think the entire management team acts very long-term, shows integrity and honesty in its communications and has installed a system based on decentralization in its ten operational niches. The company has definitely modeled some of its modus operandi on other successful “HoldCo”-structures like Lifco of Sweden. While a success like that is rare to come by, it is our belief that Aalberts have the odds in its favor for very good value creation in the next decade and beyond.

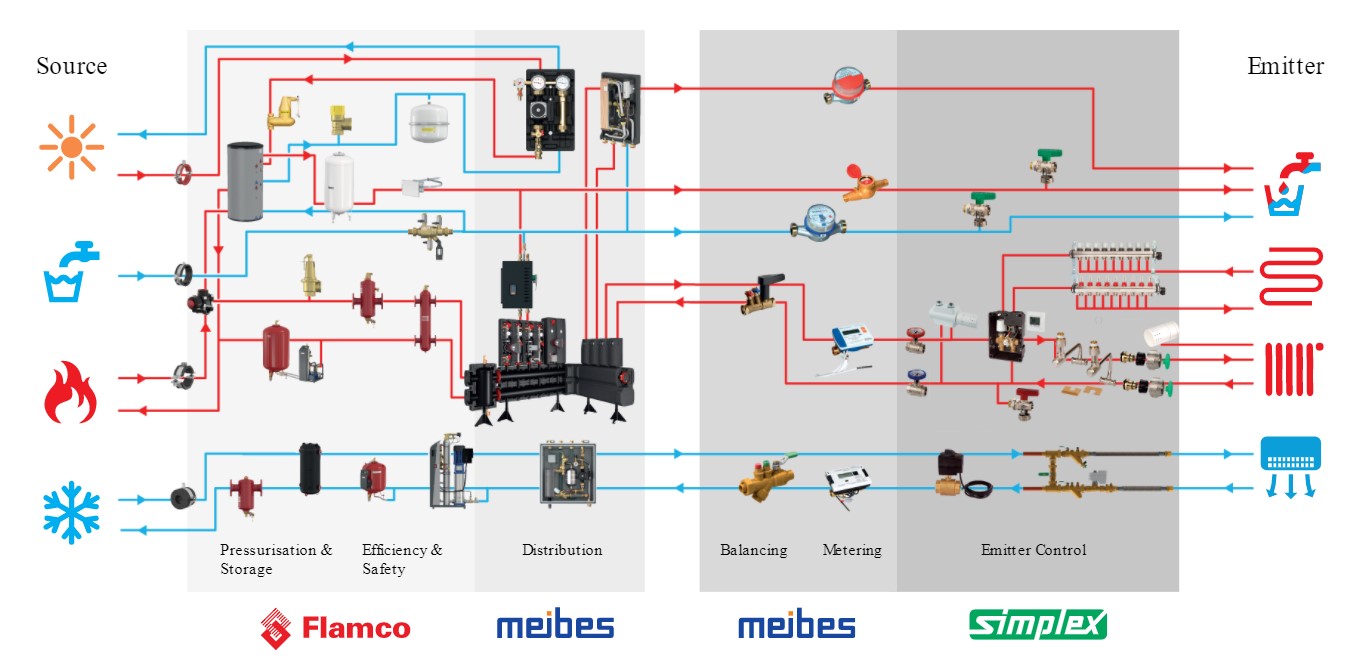

Aalberts Product Portfolio: From Source to Emitter

The current business plan was presented at a capital markets day in 2018. Its most crucial targets were organic growth of >3%, EBITA margins of >14%, and ROCE of >18% before December 2022. The first two have already been met, whereas ROCE most likely will pass the target in 2022. While these numbers are very good in their own right, we believe the company is primed for more given the leading position of its brands and the buoyant end-markets in especially eco-friendly buildings (where they supply products spanning “from source to emitter”, see picture) and semiconductors (the main client is ASML).

Our base case is for organic growth of around 5% and ROCE of 20%, which certainly would push Aalberts up the ladder towards Europe’s high-quality industrial businesses. Along these lines; R&D, pricing power and client relationships are also very much improved.

Saving the best for last – this being a conference for value investing! – Aalberts at around €50 is trading at a P/E of 17-18x. Cut differently, the valuation assumes slightly lower returns of capital than today and growth at around 3 percent. Very beatable numbers, in our opinion!

Finally, where did we source this idea? From an article announcing “The World’s Greenest Building”, which gave the award to Aalbert’s head-quarters! The company puts its money where its mouth is.

Members, log in below to access the restricted content.

Not a member?

Thank you for your interest. Please note that MOI Global is closed to new members at this time. If you would like to join the waiting list, complete the following form:

About The Author: Henrik Andersson

Henrik has worked within a framework of investing in quality franchises in a concentrated portfolio setting since the early 2000s. After five years as an assistant fund manager and analyst at Handelsbanken Asset Management, in 2003 he launched a discretionary portfolio named European Quality with 15 holdings, inspired by Peter Cundill's approach of “never shoot into the broom”. That later branched out to a family of funds named the Selective Funds. In 2011 he joined Didner & Gerge, an employee-owned asset management boutique, to launch a Global Equity Fund together with a colleague. D&G Global is now applying the same principles they have used for over a decade in trying to identify sustainably great companies with an appealing valuation starting point. Over the years, an increased emphasis has been put on corporate leadership with a clear preference for owner-operated companies with a history of outstanding operations.

More posts by Henrik Andersson