This article is authored by MOI Global instructor Will Thomson, managing partner of Massif Capital, a value-oriented partnership focused on the small- and mid-cap space, with special attention on industrial and commodity-related businesses.

“A finite game is played for the purpose of winning, an infinite game for the purpose of continuing to play.” –James P. Carse

Most companies believe they are in a finite game, playing against a timeline of quarterly earnings with known competitors and known rules for determining a winner. A 2005 study from Duke University found that close to 80% of Chief Financial Officers of the 400 largest publicly traded U.S. companies would rather sacrifice the firm’s economic value to meet quarterly expectations. The “game” of business is an infinite game and sacrificing value for short-term market appeasement is a losing strategy. Long-term value is predicated on endurance and firms that use growth merely as a vehicle to sustain or appreciate the share price, will not survive.

Introduction

When we examine a new firm, we look to create a framework that allows us to study the long-term incentive structure and the capital allocation decision process of the management team. Additionally, a framework provides a template to identify the strengths and weakness of similar firms and more quickly assess the likelihood that a firm holds a competitive advantage relative to their peers.

An often-overlooked business model is the hybrid public-family business. Hybrid public-family businesses (“family business”) are publicly traded, family-controlled firms. Families need not necessarily have founded the firm, although they often do, nor do they need to be majority shareholders, but usually are. These firms often defy simple categorization – not only do they include multi-billion-dollar corporations in almost every industry, but also include a significant percentage of all small and mid-capitalization companies globally.

Family businesses today are a diverse and adaptive collection of organizations that often get criticized for corporate backwardness, paternalism, and operational weaknesses. Many family businesses are the backbone of emerging economies and remain at the core of most developed countries small and medium-size business ecosystems. Despite the presumed shortcomings, these firms tend to outperform other publicly traded business with other corporate structures.

What follows is a proposed framework that highlights the inherent strengths of family businesses and how those strengths closely align with our view of an enduring organization that can deliver long-term value to shareholders. One of the reasons we find the framework so appealing is that successful family businesses seem to be a highly distilled version of the traits of many successful long-term enterprises, be they family businesses or not.

Family Business Context

Family businesses are characterized by a combination of two institutions, the family, and the business. Historically this form of business organization not only contributed significantly to economic development but was the worlds principal business structure. This is especially true for economies before the emergence of a large-scale manufacturing business in the United States in the 1870s.[1]

The second industrial revolution, which is generally considered to be the period from 1870 to 1914, is perhaps best characterized by the resulting spread of capital-intensive industries with complex production and distribution channels. The growth in complexity and capital intensity was accompanied by (or perhaps necessitated) a shift from family capitalism to financial capitalism, and the emergence of “modern management practices.” According to Alfred Chandler, this transition was the beginning of the end for the dominance of the family firm as “no family or financial institution was large enough to staff the managerial hierarchies required to minister modern multiunit enterprises.”[2]

The post WW2 period has seen the public perception of the family firm as being in a state of permeant decline. Family firms were incapable of competing since the advent of the large, professionalized managerial enterprises solidified, especially in the volumes of literature on business structure and management practices. As Danny and Isabel Miller noted in their in-depth study of the competitive advantages of family businesses, Managing for the Long Run, the public perception seems strange given the numerous examples of successful family firms discussed in the voluminous literature on how different companies succeeded, such as In Search of Excellence and Built to Last.

The Miller’s highlight this oddity stating: “When, via a mutual friend, we passed on this observation [the observation that so many examples of successful firms and businesses as family-run firms] to one of the authors of these books [In Search of Excellence], his response was, ‘The companies were successful despite being FCBs [Family Controlled Business].’ Like many businesses scholars, he seemed to be missing the point.”[3] We agree business scholars seemed to have missed the point.

The failure of business scholars begins with their inability to recognize the flexibility of the family business model. Specifically, the inability to grasp that while family businesses in a traditional sense persist as essential parts of the economy, the hybrid public-family business model does as well, for example, the Lundin Group of companies, or any number of Asian family-owned industrial conglomerates. In the case of the Lundin Family, whenever they decided to develop a resource, be it a mine or an oil and natural gas deposit, the family utilized the hybrid public family business model: retaining management control for the family while turning over technical tasks to more-experienced companies and drawing on capital from retail and institutional investors around the globe.

The Framework

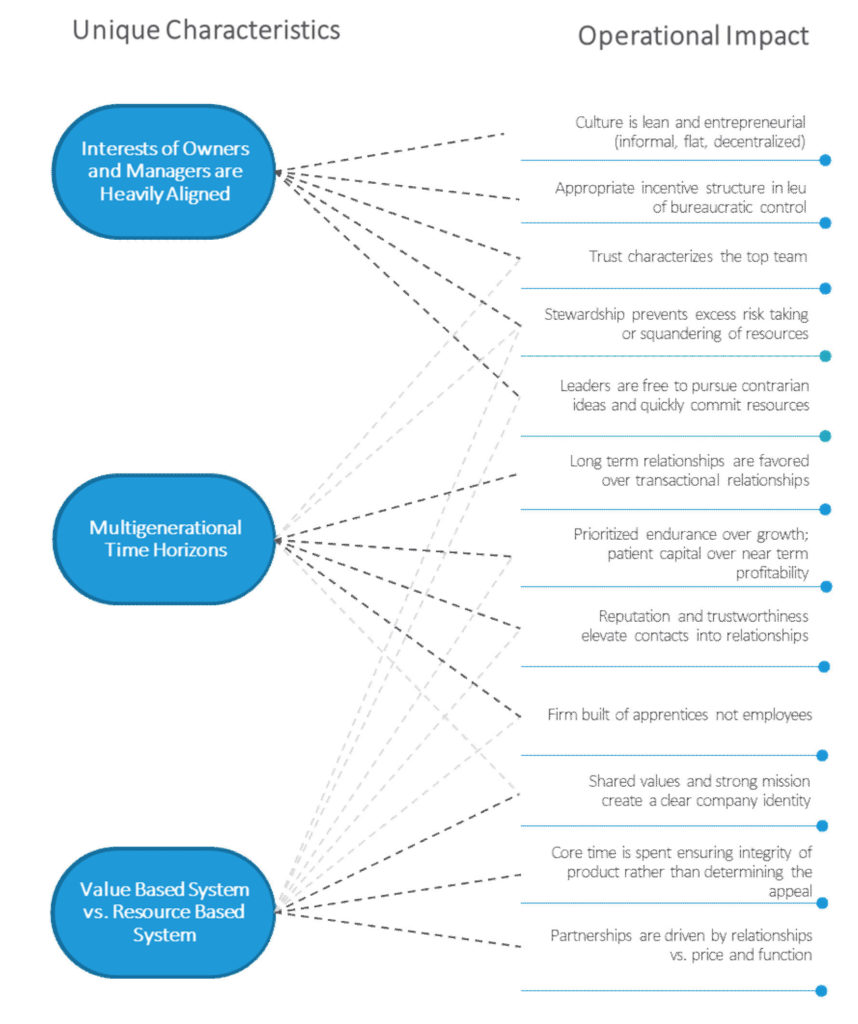

There are three unique characteristics we identify in a hybrid family business model that are at the core of their success:

1. An inherent alignment of owner and manager interests;

2. The presence of multigenerational time horizons, and;

3. The implementation of a value-based system versus a resource-based system.

Each characteristic has a subsequent impact on operations. The operational impact of these traits not only govern how the firm is managed but also impact its reputation and its earning power. Ultimately, we believe these operational impacts produce real value.

Within family business groups, owners and managers are often synonymous. The resulting alignment creates an environment where risk and reward are understood as one in the same. Drawing parallels to ‘skin in the game,’ managers must manage risk knowing they are exposed to its consequences. Similarly, they are motivated to pursue greater earnings, understanding that they will share in the reward.

Ownership provides a simple, effective, and often inexpensive method to prevents excess risk-taking while creating an environment where leaders are free to pursue contrarian ideas and quickly commit resources.

Ownership though is not the same things as owning stock because of a compensation arrangement. This is a point missed by most. Stock options, the most common source of compensation for management teams at publicly traded companies, is a financialized derivative, an abstraction masquerading as ownership. Ownership typically requires hard work and is accompanied by illiquidity, a lack of diversification and a lack of concern regarding the moment to moment liquid value of something. These are characteristics of ownership that bring focus to management activities. Ownership also tends to come with the weight of history.

Multi-generational ownership comes with a sense of responsibility and stewardship. Growth is too easily pursued at the expense of a balance sheet in a world awash with money and is too often thought of as the “end goal’ or “objective.” Growth is merely directional guidance though and does not indicate “why” a firm is growing, or “where” it is looking to grow to. Preservation of inherited assets and a deep sense of responsibility to protect the long-term health of the company are often paramount for family businesses. Endurance is prioritized over growth; patient capital is deployed at the expense of near-term profitability. While the result may not yield the new darling of Wall Street, it provides investors who care about the preservation of capital an excellent store of long-term value.

Finally, hybrid family businesses tend to make decisions based on a set of values, often passed down from the founding entrepreneur. Most businesses have some semblance of a value statement or mission, but very few allocate resources based on those values. In periods of market volatility or intense competition, companies will often allocate resources to mirror what their successful counterparts are doing. In a value- based system, the market and competitors are certainly important input variables; however, they do not govern the actions of the firm. Shared values create a clear company identity, and resources are spent ensuring the integrity of the company rather than the short-term appeal.

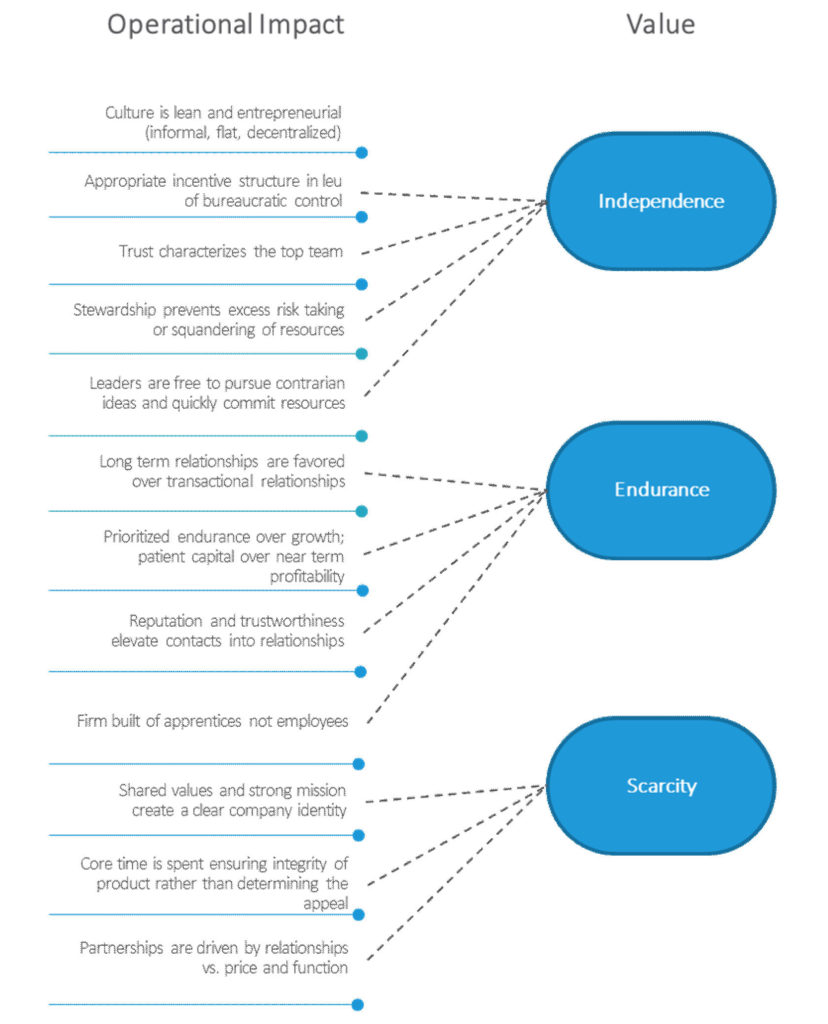

The alignment of owners and managers, multi-generational time horizons and value-based decision making all have operational impacts that produce long-term value. Value is frequently discussed in the context of a listed market price relative to the firm’s estimated intrinsic value; looking beyond price, a firms value can be assessed through the lens of a firm’s independence, endurance, and scarcity. For example, firms, where leaders are free to commit and allocate resources efficiently, have healthier balance sheets then firms weighed down by bureaucracy, and an inability to produce succinct and focused decisions. Similarly, firms that can monetize their reputation and trustworthiness and then nurture and prioritize that relationship are built to endure. A firm that focuses intently on their ability to endure, not merely to grow are often excellent companies to consider for a long-term store of value.

Finally, firms that have an intense value system and allocate resources accordingly, often produce products of such quality that they create market scarcity. In the long run, they serve an economic or social need that creates natural barriers to entry for industry competitors.

It would be inaccurate to presume that all hybrid family businesses share these characteristics, yet many do. While success can always be attributed to a product, an individual, or market dynamics, we believe the traits we have outlined above often define hybrid family businesses and lay a foundation for an enduring company.

[1] The History of Family Businesses 1850 -2000, pg. 6.

[2] Managerial Hierarchies. Comparative Perspectives on the Rise of the Modern Industrial Enterprise.

[3] Managing for the Long Run, pg. 13.

Disclaimer: Opinions expressed herein by Massif Capital, LLC (Massif Capital) are not an investment recommendation and are not meant to be relied upon in investment decisions. Massif Capital’s opinions expressed herein address only select aspects of potential investment in securities of the companies mentioned and cannot be a substitute for comprehensive investment analysis. Any analysis presented herein is limited in scope, based on an incomplete set of information, and has limitations to its accuracy. Massif Capital recommends that potential and existing investors conduct thorough investment research of their own, including a detailed review of the companies’ regulatory filings, public statements, and competitors. Consulting a qualified investment adviser may be prudent. The information upon which this material is based and was obtained from sources believed to be reliable, but has not been independently verified. Therefore, Massif Capital cannot guarantee its accuracy. Any opinions or estimates constitute Massif Capital’s best judgment as of the date of publication and are subject to change without notice. Massif Capital explicitly disclaims any liability that may arise from the use of this material; reliance upon information in this publication is at the sole discretion of the reader. Furthermore, under no circumstances is this publication an offer to sell or a solicitation to buy securities or services discussed herein.

About The Author: William Thomson

Will Thomson is currently a Managing Partner at Massif Capital, a value-oriented investor partnership focused on global opportunities in the small and mid cap space, with special attention given to industrial and commodity-related businesses. He has previous energy and mining related work experience in private equity, credit analysis, insurance and government policy. Massif Capital combines a fundamentals based approach to individual company assessment with in-depth capital cycle analysis to find compelling investment opportunities.

More posts by William Thomson