This article is authored by MOI Global instructor Steven Gorelik, portfolio manager at Firebird Management, based in United Kingdom.

Steve is an instructor at Best Ideas 2023.

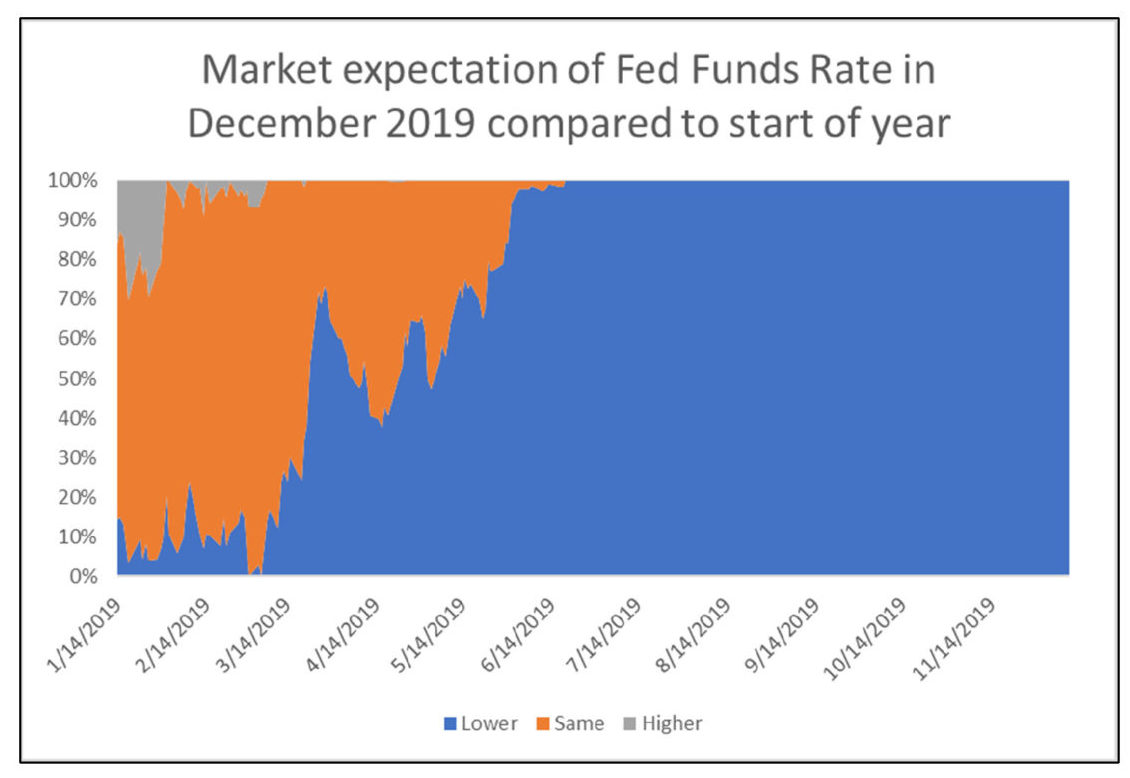

The beginning of each calendar year is an opportunity for strategists from major investment banks to confidently predict capital market performance over the upcoming twelve months. At the beginning of 2022, the analysts expected the market to go up by about 1%[1], while at the end, S&P was down roughly 18%. As we enter 2023, the analysts are again predicting an increase in valuations of approximately 3-5% on average.[2] These predictions usually end up wildly wrong, but nevertheless, the process is repeated every year. One of the more famous occasions from the debt markets was the 2019 expectations for the fed funds rate. At the beginning of that year, the market believed there was a 90% chance that the rates would be the same or higher by year-end. Instead of going up, by December, the rates went down by 0.75% due to emerging concerns about the global economy’s health.

I will resist the temptation to join the chorus. Still, I think it is valuable to analyze the main drivers for performance over the last twelve months and to consider what will likely influence stock prices in the near future. While much time was spent analyzing whether the economy is about to enter a recession, last year’s 18% drop in US equity valuations can be fully explained by the increase in the risk-free rate. As a result of a correction, estimated equity returns went up by roughly 3%, but so did the 10-year US interest rate.

For 2023, the market once again expects[3] the fed funds rate to be flat or slightly higher by year-end, though less confidently than four years ago. Futures are pricing with a 60% chance of rate increases and a 13% likelihood that they will be lower by year-end. That said, I will go out on a limb and suggest that the main story in the next twelve months will not be interest rates but corporate profit margins.

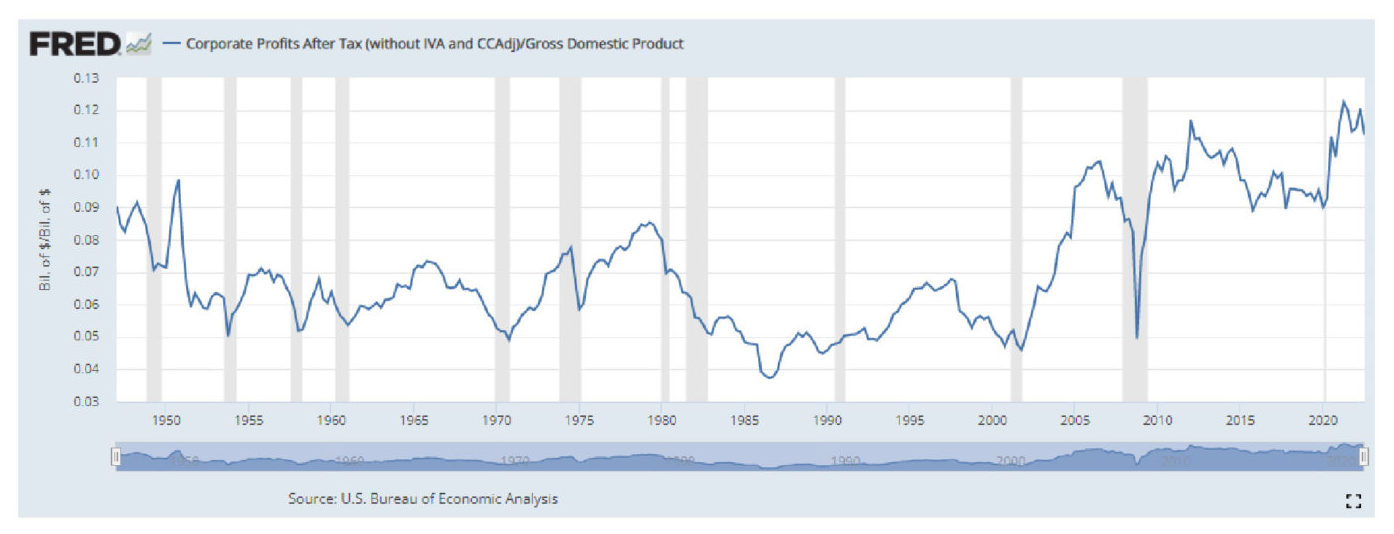

Since the 1990’s US companies have increased profitability, as measured by the percentage of GDP, from 5% to 11%. Some of the improvement is explained by changes in the corporate tax rate, which seem to be sustainable (for now). But other reasons for the change, like lower interest rates on debt, corporate efficiency, etc., may prove more fleeting – the same way they did in the 1960s, 1980s and 2010s. At 11%+, corporate profits as % of GDP are more than two standard deviations from the historical average of ~7%.

The profitability has been strong for most of the last two decades, so why raise the concern now? The reason is that I believe that market expectations are becoming increasingly out of touch with reality at a time when the pressures on profitability are building. Low unemployment and potential recession could weigh on corporate margins over the short and medium term. High inflation is another concern, especially considering that historically price rises have negatively correlated with corporate margins.

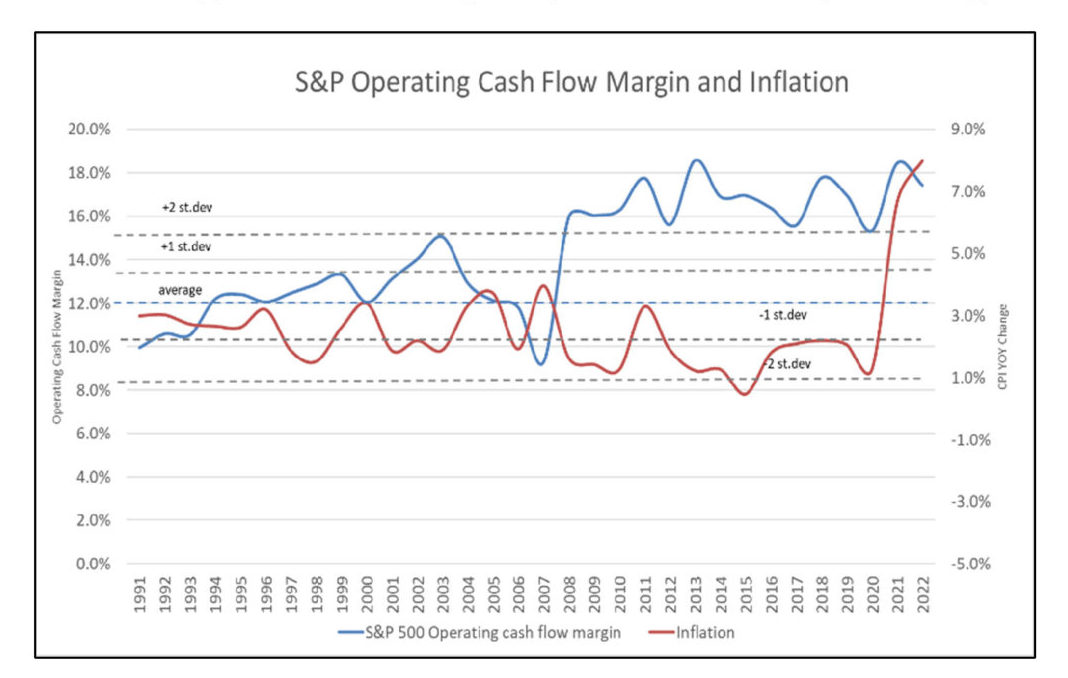

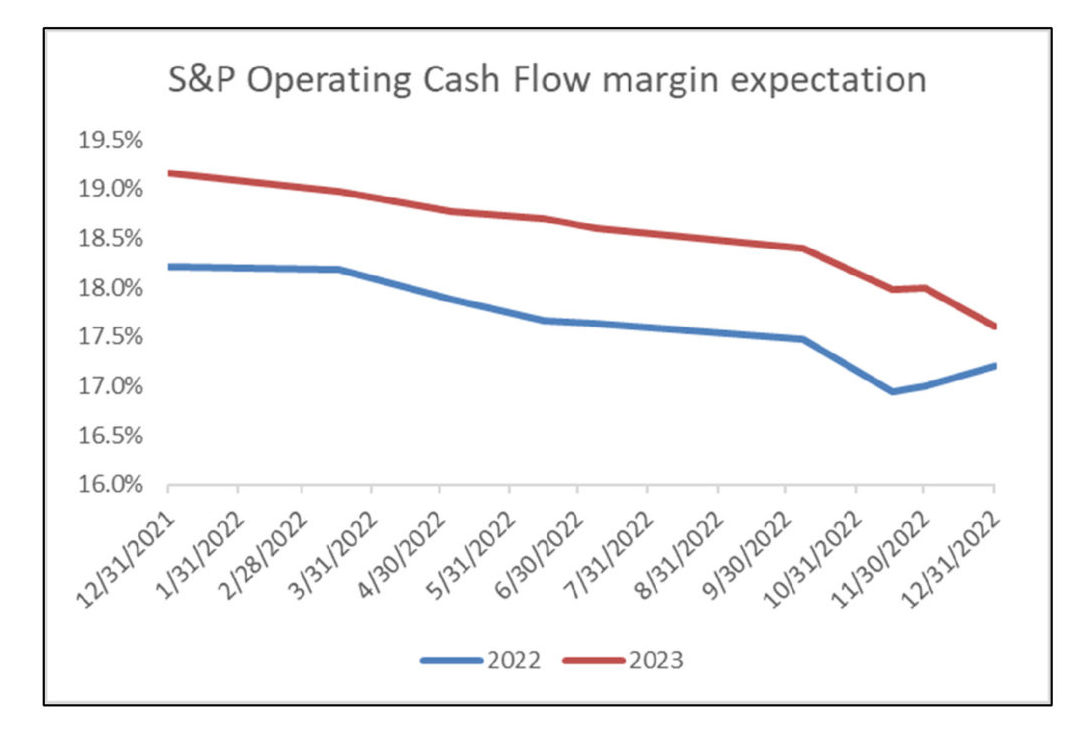

While the pressure on profits is building, the forward estimates remain blissfully optimistic. Looking at the S&P 500, operating cash flow as a percent of the sale is expected to come in at 17.6% (1.2 standard deviations away from the historical average) in 2023 at 18.8% (1.7 standard deviations away).

At the beginning of 2022, the profit expectations were similarly high but proceeded to come down dramatically over the year – especially for FY 2023, where margin expectations fell from 19.2% to the current 17.6%.

Lower margins may impact stock performance due to negative revisions of short-term expectations and views on longer-term profitability, which feeds through the multiples. Despite last year’s correction, the market multiples remain elevated from historical norms.

In the environment of higher-than-normal profitability and rising pressures, we look for companies that should do well independent of overall market conditions. Historically, the critical ingredient for such investments is identifying businesses with strong underlying demand facing temporary difficulties. Such firms are often undervalued due to short-term uncertainty. This undervaluation gets resolved as business results recover, providing a double benefit to investors.

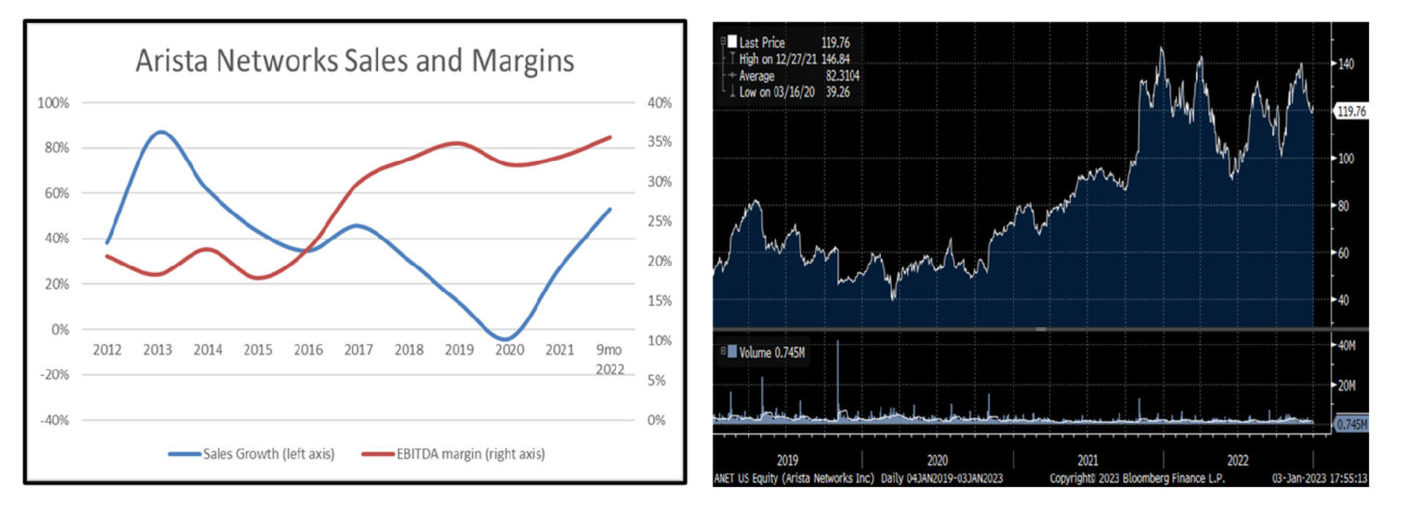

Case Study: Arista Networks

A recent example of such a situation is Arista Networks, a company that manufactures high-end switching equipment used in data centers. In 2019, their primary customers, Amazon and Microsoft, paused purchasing equipment while working on designs of next-generation data centers capable of addressing ever-growing data storage and transfer needs. Arista’s investors, accustomed to 30%+ annual sales increases, faced prospects of a significant slowdown in revenue growth and voted with their feet sending the shares down by almost 50%.

Meanwhile, company engineers were actively involved in the customer’s design decisions which included their state-of-the-art 400GB switches. In 2021 and 2022, as the global economy was recovering from COVID, networking equipment purchases came back, and so did Arista’s growth. In 2021 sales increased by 27% and are on track to grow by 30%+ this year. At the same time, Arista’s investors that stuck with the company were rewarded with increasing operating margins and share price that is up 3x from 2020 lows.

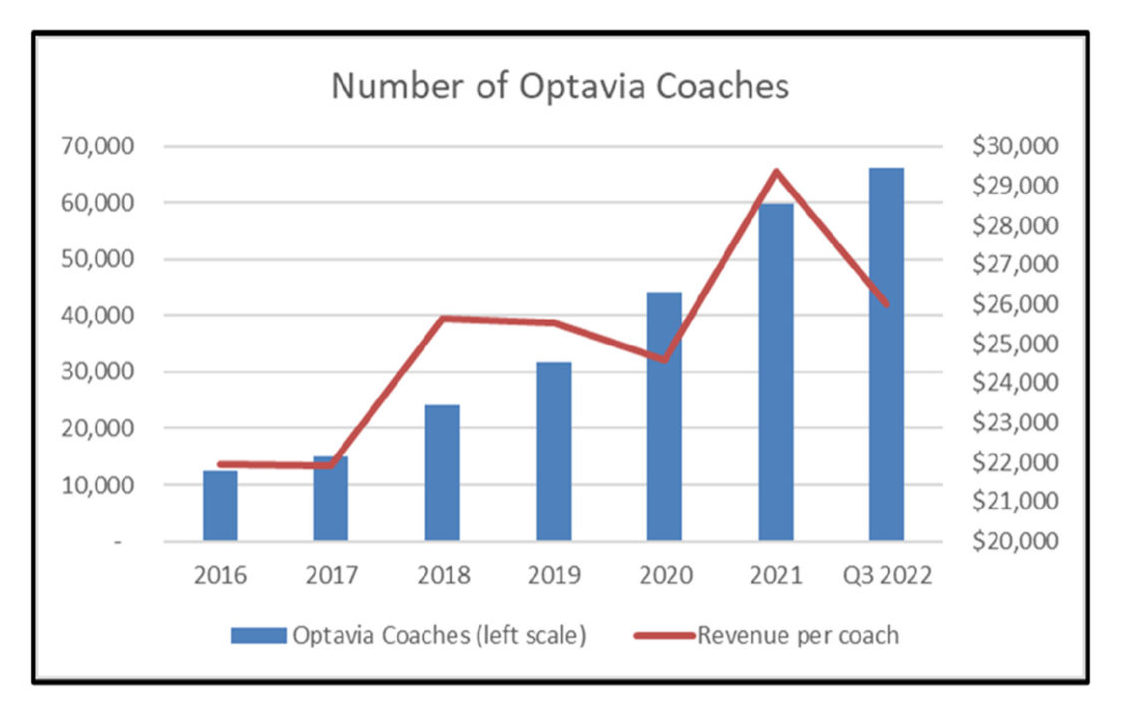

Case Study: Medifast

Looking forward, I believe Medifast, Inc, could provide similar extraordinary returns if their difficulties are temporary. Medifast is a weight loss management company helping people lose weight through meal supplements and a coaching model. Unlike similar plans, like Herbalife, Medifast’s Optavia is sold by coaches who provide guidance and support.

Medifast historically generated 30%+ growth rates primarily due to an increase in a number of coaches that earn roughly twice of Herbalife distributors without taking on inventory risk.

2022 has been a year of slower growth due to the high base effect of COVID and people’s desire to enjoy life a bit more coming out of the pandemic. As a result, Medifast’s sales are expected to grow in the low single digits, and shares are down by almost 50% over the last year (sounds familiar?). At the same time, the need for weight management solutions has never been greater, with 70+% of the US adult population considered overweight or obese.

Like in Arista’s example, I expect short-term pressures to dissipate and sales growth to reaccelerate to double-digits in the medium term. Medifast has plenty of runway for growth in the United States and hasn’t even started selling its products internationally – a source of up to 70% of revenue for companies like Herbalife and Weight Watchers.

With shares trading at multi-year-lows on EV/EBITDA basis (5x) and free cash flow yield (11%+), I believe Medifast provides a unique opportunity to invest in high-quality business at a reasonable price. History suggests that demand for company products is not particularly sensitive to overall economic conditions and, on the contrary, could prove recession-proof. If the growth comes back, Medifast’s shareholders will be well rewarded for sticking with this company.

[1]https://www.nytimes.com/2022/12/16/business/economy/stock-market-forecast.html

[2]https://www.investors.com/news/stock-market-forecast-2023-challenges-abound-for-sp500-dow-jones-stock-pickers-can-shine/#:~:text=Most%20stock%20market%20forecasts%20for,closed%20the%20year%20around%203840

[3]https://www.cmegroup.com/markets/interest-rates/cme-fedwatch-tool.html

About The Author: Steve Gorelik

Steve Gorelik is the Fund Manager of Firebird U.S. Value Fund as well as portfolio manager of Firebird’s Eastern Europe and Russia Funds. He joined Firebird in 2005 from Columbia University Graduate School of Business while completing education from a highly selective Value Investing Program. Prior to business school, Steve was an operational strategy consultant at Deloitte working with companies in various industries including banking, healthcare, and retail. He holds a BS degree from Carnegie Mellon University as well as a CFA (chartered financial analyst) charter and a membership in Beta Gamma Sigma honor society. Steve serves on the boards of Teliani Valley (Georgia), Arco Vara (Estonia), and Pharmsynthez (Russia). He speaks Russian, English and his native Belarussian.

More posts by Steve Gorelik