This article is authored by MOI Global instructor Krish Mehta, investment analyst at Enam Holdings, based in Mumbai.

Krish is an instructor at Best Ideas 2023.

India is poised to grow at a staggering pace and become a $10 trillion economy by 2035 as per CEBR from its current $3 trillion size. With more than half the population under 25 and national median age of 28.4, India’s demographic dividend is the engine that will propel the country’s push to become the third largest economy in the world by 2037 from being fifth currently.[i] Credit markets will play a pivotal role in fueling the engine for growth in India over the coming decades with banks forming the bedrock for sustainable growth and credit markets.

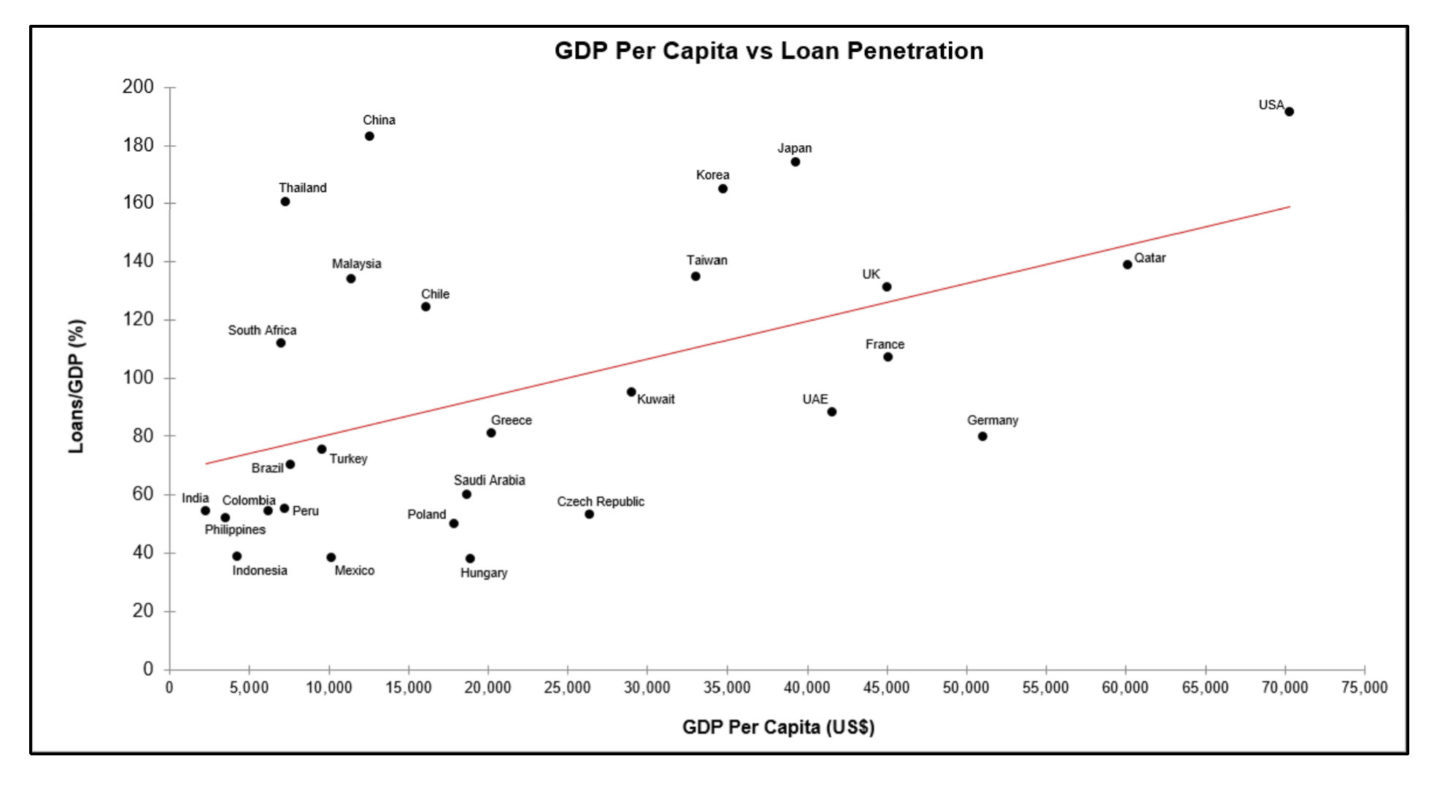

The chart above shows how underpenetrated the Indian market is from a credit perspective. As India’s GDP grows and the demographic dividend kicks in, the GDP Per Capita vs. Loan Penetration will move higher up across the slope.

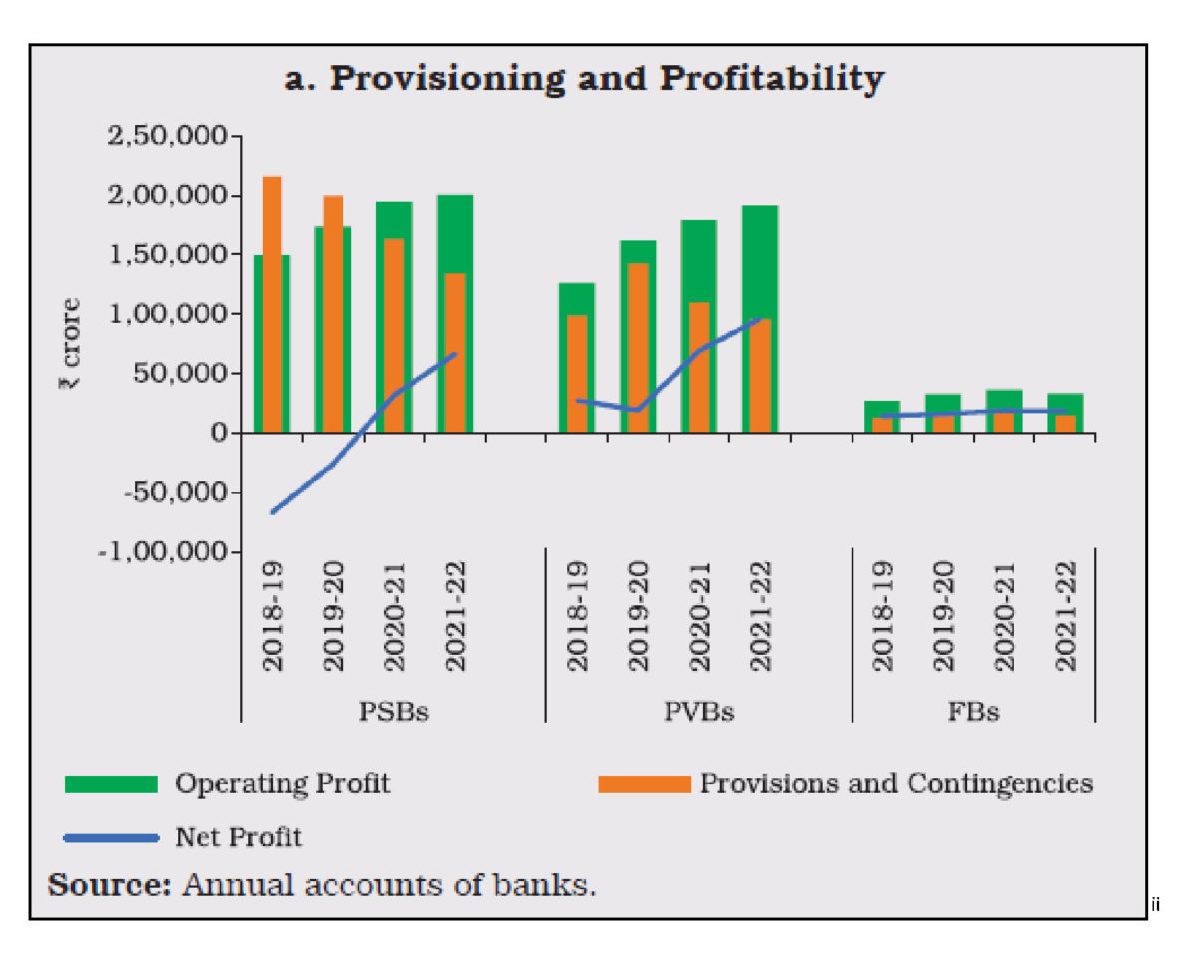

The silver lining to the pandemic has been the broad based clean up of balance sheets that has taken place across sectors in the Indian markets. The record profits that companies have made after the reopen following the COVID-19 outbreak has been transformational since it’s enabled several leveraged entities to deleverage and repair their balance sheets substantially. Moreover, the strong earnings growth and free cash flow generation across corporate India in the last couple years has aided the sustainability of balance sheet strength. This has translated to a rise in profits and improvement in quality of earnings for banks given the drop in provisions, NPAs, and slippages.

[ii] The provisioning and profitability data for Indian Banks reflects the clean up and inspires confidence in the banking system. The bad loan cycle that had plagued Indian banks in the previous NPA cycle is behind us. A key area of focus for the entire banking sector seems to be on the liability side to support the strong credit growth. Several analysts and economists have highlighted the liability side of bank balance sheets as a potential bottleneck in the system. However, I view it as a temporary phenomenon resulting from the structural lag in the transmission of deposit rate hikes that has partly driven NIM expansion across banks given the favorable ALM mix with loans getting repriced faster. With deposit rates being hiked as we are currently witnessing, the incremental deposits should address the concerns on the liability side for banks. The rise in cost of deposits will be more than offset by favorable ALM, higher LDR driven by strong credit growth, and the pass-through of earlier rate hikes, thus enabling sustained NIM expansion. Loan growth drives deposit growth in a fractional banking system as is the case in India, which provides comfort on the sustainability of managing a prudent LDR.

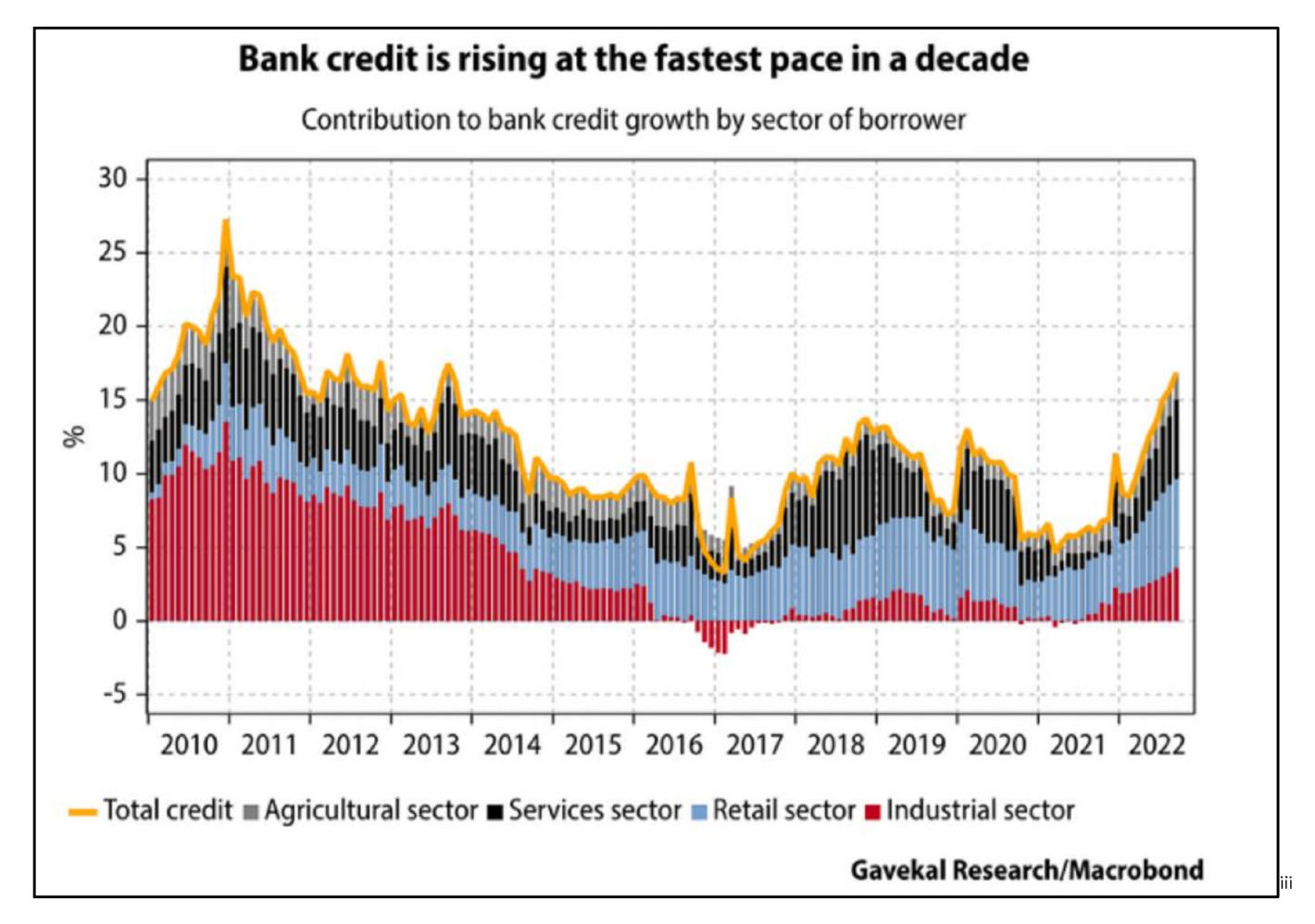

[iii] Lastly, from a financial stability point of view we are still in the early stages of the credit cycle. As highlighted in the RBI’s latest report on trend and progress of banking in India, “empirical estimates for India suggest the existence of a threshold beyond which higher bank profitability may be detrimental to financial stability. The NIM of SCBs at 2.9% at end-March 2022 remained much below the threshold (around 5%).”

India is well placed to capitalize on its inherent economic strength accompanied by global factors such as China+1 that have substantially increased the attractiveness of India as a global destination. Credit growth will be the fundamental pillar for the $10 trillion ambition. Large private sector banks with wide moats, strong culture, well capitalized and bullet-proof balance sheets, robust lending processes, high productivity metrics and strong growth, ROA and ROE generation potential remain our preferred avenue to play this credit cycle. HDFC Bank ticks all these boxes accompanied by its attractive valuation.

[i] https://www.forbes.com/sites/williampesek/2022/12/30/indias-10-billion-economy-dream-risks-turning-into-nightmare/?sh=332d41777b1a [ii] https://rbi.org.in/Scripts/AnnualPublications.aspx?head=Trend%20and%20Progress%20of%20Banking%20in%20India [iii] Gavekal Research

About The Author: Krish Mehta

Krish Mehta is a value investor from Mumbai, India. He is an Investment Analyst at Enam Holdings in Mumbai, a reputed family office. Enam runs a concentrated book and takes five- to ten-year views on businesses, practicing a long-term value-focused investment philosophy. Krish’s role at Enam is conducting bottom-up, fundamental research of Indian and global equities across sectors, portfolio management, and covering global macro. Krish graduated from the NYU Stern Undergraduate School of Business in 2019 with a BS in Finance and Accounting and interned at a long/short hedge fund in London, Theleme Partners, for two summers prior to joining Enam.

More posts by Krish Mehta