This post by Daniel Gladis is excerpted from a letter of Vltava Fund. Daniel, based in the Czech Republic, is a global value investor and long-time MOI Global instructor.

We are witnessing today a trend of investors massively moving their money from actively managed funds into passively managed funds, also known as index funds. The active‑versus‑passive debate is not new. It has been periodically recurring for decades, with each party alternating in dominance. Just now, it seems that passive investing is winning and the trend of shifting money into passive funds has in fact accelerated in recent years. What does this mean for us? Should we jump onto the bandwagon or should we instead take advantage of opportunities to which this trend gives rise? This letter is all about answering that question. Let’s begin by looking at some numbers. We will focus mostly on the US market, because that is where this trend has advanced furthest.

Money flows into index funds

Index funds endeavour to mirror the returns of a certain basket of equities or of an index. This is not at all a new product, but it has witnessed a real upsurge in recent years. According to Credit Suisse, the sum of money invested in US investment funds rose from USD 287 billion in 1989 to USD 8.7 trillion at the end of 2016. Over the same period, the volume of money in index funds increased from USD 3 billion to USD 2 trillion, and it doubled in just the past 4 years. In 1989, index funds accounted for approximately 1% of the market, but today they account for 23% of assets under management in investment funds. In the last ten years, USD 1.2 trillion flowed out of actively managed funds and USD 1.4 trillion flowed into index funds.

This unprecedented movement of money is deforming the market, changing its dynamics, and bringing both immense risks and opportunities. Before we get to those, let’s take a look at how indices are actually created.

How indices are created

We’ll take as an example a broad and most widely used index, the S&P 500. This is composed of the 500 leading US companies, which together represent approximately 80% of the entire US stock market. Individual companies are represented within the index in proportion to their market capitalisations. The largest weight goes to Apple, whose market cap is approximately USD 800 billion, whereas the smallest company in the index has a capitalisation of USD 2.7 billion. The ten largest companies account for 19.1% of the entire index.

Very important, however, is that the index’s composition is not permanent. Rather, it changes almost constantly. The weights of the individual companies in the index are continuously adjusted in accordance with changes in their market capitalisations. The more a share increases in price, the greater its weight within the index. A greater weight in the index means that more money flowing into the relevant index fund is directed to that stock. This brings us to the first important point: The more expensive a share is, the more money that flows into it. I call this the perverse cycle of index investing. When a share is rising in price, its weight within the index grows, which means more money passively invested into the index is allocated to it, which causes its price to rise even more, its weight in the index further increases, and thus it attracts even more money. The cycle is a closed one and feeds upon itself like some kind of perpetual motion machine. This simultaneously means that money tends to flow away from shares which are becoming steadily cheaper.

GM vs. Tesla

You will surely remember that at our last annual shareholders’ meeting we were discussing the valuation of two car manufacturing companies – GM and Tesla. At that time, they had approximately the same market capitalisation of USD 50 billion. We took a little survey then. An investor has USD 50 billion at his or her disposal and must choose whether to buy the entirety of GM or the entirety of Tesla. The investor who chooses GM can expect to obtain USD 9 billion in profit at the end of the year, whereas the investor who chooses Tesla will have to put in another USD 2 billion at the end of the year just to keep it alive. When we put it to a vote, there was no one who would have chosen Tesla and everyone voting sided with GM.

The “wisdom” driving the operation of index funds, however, keeps pushing GM’s share price down and Tesla’s share price up. GM achieves large profits, pays a big dividend, and is massively buying back its own shares for prices at around six times its annual earnings. This is decreasing the number of shares in circulation, its market capitalisation is not growing, and the weight of GM shares in the index is dropping. On the other hand, Tesla needs more and more money every year just to cover its losses and must repeatedly issue new shares. Because the market is so far ignoring Tesla’s inability to generate a single dollar in profit, not only does the share price keep increasing, but, due to the issues of new stock, its market capitalisation and weight in the index continue to grow at an even faster pace. Paradoxically, due to passive investing, at least on a relative basis, money flows away from shares of inexpensive and profitable companies and flows into shares of an expensive company constantly making losses. How many passive investors realise this?

Problem number one – dearness of the index

According to The Wall Street Journal, 41% of this year’s growth in the S&P 500 index is due to the rising prices of just five stocks: Facebook, Amazon, Apple, Google, and Microsoft. This simply results from the way indices work. The most money flows into the stocks of the largest companies regardless of how expensive they are. And they are indeed expensive. In one debate forum, Jan Dvořák recently asked an interesting question: what would be the PE of a single company combining Facebook, Amazon, Apple, Google, and Microsoft? I immediately set about to calculate this and came out with 30.6. That’s pretty high, isn’t it?

Some may object and insist these market leaders deserve this high valuation because they have a great future ahead of them. This may be true, but, to that point, I would like to recollect an article in Fortune from August 2000 headlined “Ten Stocks to Last the Decade”. These were the market leaders at that time: Nokia, Nortel, Enron, Oracle, Broadcom, Viacom, Univision, Charles Schwab, Morgan Stanley, and Genentech. Back then, it seemed that the future belonged to them and the fact that their stocks were expensive according to all reasonable measures was also disregarded. Over the following 12 years, these stocks lost 74.3% of their market value.

There is no idea in investing which would be good or bad under all circumstances, but the price of the investment is always crucial. And this is the main problem with today’s index investing. According to data from Standard and Poor’s website, the PE of the S&P 500 index is currently 24.1. This is measured using actual reported earnings (and not from numbers variously massaged and restated by the companies and stockbrokers) as at the end of March 2017. The index’s earnings were USD 100.29 and the index’s value at the end of June was 2423.41. This results in a PE of 24.1. When the market is this expensive, we believe we can expect the index to provide returns of around 2% per annum over the next ten years. My ideas about attractive investments are rather different from that. Those investing today into the S&P 500 unwittingly are buying into very low future returns. I think it is no coincidence that the US market is the most expensive among the big markets and that index investing has advanced the furthest there. There is certainly a relationship between these two facts. Other markets are substantially cheaper, and this is why we have only approximately one‑third of our portfolio invested in the US market.

Crowding

The massive influx of money into index funds brings even additional risks. The two main risks are those of crowding and low liquidity. When the originally simple and good idea of passive investing is seized upon by the masses and pushed to its extreme, this results in crowding. For example, the Nasdaq index and certain sector indices are places where crowding is presently the most serious.

Every transaction needs two parties: a buyer and a seller. Here, the buyers are index funds into which money is currently flowing, whereas the sellers are actively managed funds out from which money is flowing. As we know, the nature of index funds is to buy especially the most expensive stocks. Actively managed funds are selling them willingly. At present, it still seems that index funds are nothing less than the Holy Grail itself. In fact, index funds are essentially the sole buyers. This is especially true regarding the most expensive companies losing the most money. When this trend reverses itself, to whom will the index funds sell these stocks? To the active funds? Not at those prices – but only when the share prices will be maybe 30% or 50% lower. Perhaps it will be altogether impossible to do so. In a situation where index funds go from the position of sole buyer to that of sole seller and the crowds of investors start pushing to get out the doors, the index funds will encounter an immense problem of illiquidity and an impossibility to sell their stock. The same commentators who are now shouting “Index funds forever!” will start to bellow “Index funds never more!”

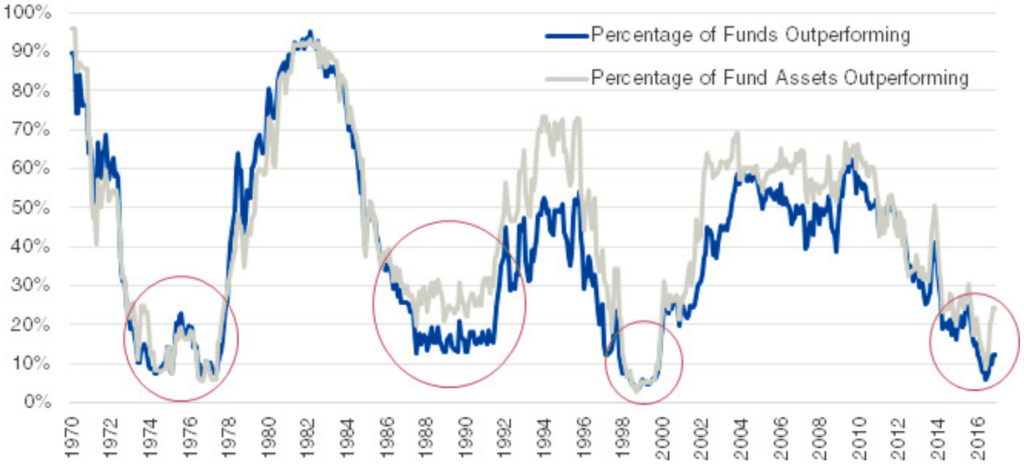

Cyclicity

Will such a turnaround come to pass? I think there is no doubt about it. After all, this will not be occurring for the first time. Take a look at the following graph. Relative performance of passive and active funds is cyclical and the trend often reverses itself at major market turning points as explained next.

Percentage of Funds (Fund Assets) Outperforming S&P 500 on Five-Year Basis

Source: Nomura Instinet, Joseph Mezrich.

So, the question is not whether but when. The longer this takes the more dramatic the reversal will be. Imagine an absurd situation wherein 100% of all money would be invested in passive funds. This means that no one on the market would be interested in the price of anything. The market would collapse and chaos ensue. It is clear that such an extreme situation will never occur. The market would start collapsing much sooner than that. Even today’s 23% market share of passive funds bears a high risk. In fact, there is a lot more passively invested money even than that, because a number of active funds in practice index their portfolios without advertising it to the public. I believe that we are far beyond the level of what the market could absorb in the case of a trend reversal.

Many things in the market are cyclical in nature. Since the early 1990 s, when I started out in the markets, there have been several changes in investor behaviour trends regarding active and passive funds. Active investment was praised in the mid-1990 s, around 2004, and immediately after the Great Financial Crisis. In contrast, passive investing was dominant in the early 1990 s, at the end of the 1990 s, just before the Great Financial Crisis, and today. Notice that people favour active investment after major market crashes whereas they cling to passive investment before them.

This is rather easily explained. Passive investing fares well when a market is rising over the long term. That is especially true towards the end of that rise, when more and more investors are jumping into indices, lured by the seeming ease of making money on the bull market. Active investing is preferred after market crashes. That means investors respond once again to past development even though they should be doing exactly the opposite and preferring active funds at the close of a bull market. The absolutely best sign of an approaching reversal is when active investing is pronounced dead, as is often heard today.

Oftentimes, however, investors do not see this cyclicity. Instead, they extrapolate the current trend and essentially buy what they should have bought much earlier. The present trend of shifting money into index funds must end sooner or later. This is unavoidable, because there is a finite amount of money in active funds. Paradoxically, it would be best for investors massively moving into index funds if the trend would reverse itself sooner rather than later. The sooner this happens, the lower their losses will be. When all index investors decide that it is time to leave index funds, I would not like to be in their shoes.

Is passive investing merely a myth?

Jeff Gundlach, a renowned investor, holds that passive investing is in fact only a myth. As we know, an index is not some independent and objective measure of market performance. Its composition changes based on the development of that market, which is to say depending on what it should itself be measuring. Moreover, it is influenced by decisions of a committee within the company compiling and managing the index.

In fact, passive investors are not even behaving passively. Judging by the name “passive investing”, one would think that a passive investor buys an investment and then does nothing with it for a long time. That is passive. In contrast, active investors are expected to intervene actively in the composition of their portfolios. Facts, however, indicate precisely the opposite behaviour of these two investor groups. Jack Bogle himself, the founder of The Vanguard Group and the leading proponent of passive investing, statesthat average turnover of stocks in ETFs (exchange‑traded funds) is 880% per year. This means that passive investors hold their investments for about 7 weeks on average. In comparison, the average stock holding time in the US is about 10 months (and at Vltava Fund it is much longer).

So, is passive investing really the norm or is it only a myth? We don’t know. But do you know anyone who bought an index 20 years ago and who holds it to this day? Or better still, someone who started buying an index 20 years ago and was buying every month to this day no matter what happened on the markets? I don’t. Index investing sounds reasonable in theory, but in practice I don’t know anyone who would be able to apply it over the long term. It seems to me that index funds are instead a magnet to speculators who like the ease of trading them. The fact that index funds are much more frequently used by speculators than by long‑term investors is also supported by the analysis from Credit Suisse. It states that the ten‑year return rate of the S&P 500 (represented by the ETF with the ticker SPY) for the period beginning in 2016 was 6.9% p. a. and the dollar‑weighted return for investors in this fund was only 3.5% p. a. Index funds are evidently used primarily as a means for short‑term speculation.

Difference between small and large investors

Some well‑known investors sometimes publicly recommend to individual investors to use predominantly index funds. One tends to forget, however, to whom they are actually speaking. They often have in mind the “average small investor”. In the Czech environment, we could consider this an investor earning approximately double the average wage and his or her annual investments may range in the tens of thousands of crowns. For such an investor, it probably truly is better to strive towards building a passive portfolio. For larger, more sophisticated investors, however, I believe it is better to use active asset managers and diversify across several basic types of assets.

Even Buffett often speaks of the advantages of index investing for typical small and less‑experienced investors, but I have not found a single case of Berkshire Hathaway ever investing into an index.

In fact, passive investing is much more difficult than it appears. To be successful, it requires that the investor have an iron will, resilience, patience, and an indomitable conviction as to its correctness. This combination of human characteristics is very rare. Co‑operation with an active money manager can shift a part of one’s worries from the investor to his or her manager. This may be a more feasible approach for many investors, and even for more sophisticated ones.

What does this mean for our investing?

The question you may be asking now is: Does the current preference of investors for passive funds present opportunities or dangers for us?

The answer is wholly unambiguous. For us, this trend is absolutely fantastic and we welcome it almost gleefully. In its study of active and passive investing, Credit Suisse states the following:

Excess return = skill × opportunities.

It is entirely clear that the boom in passive funds brings opportunities. What situation could be better than when an ever‑increasing part of the market unthinkingly is buying whatever is represented in indices and with complete disinterest as to its price? The vast majority of passively invested money is “managed” by three companies: BlackRock, Vanguard, and State Street. The word “managed” is probably a misnomer, because there is not much management in the case of passive investing. I should rather say “administered”. These three companies are focused on hoarding assets rather than managing them. Essentially, it is difficult to say whether or not they would care at all about the results of those investments. After all, they are required to invest as dictated by the composition of the index, and it is that which determines their returns.

They are not much concerned with pricing, contemplating the values of the individual companies, or even risk management. The index is the index and that’s that. We enjoy investing in such an environment and with such rivals. The more money there is in the passive funds, the less efficient the market will be in valuing the individual stocks and the more active we will be. Our greatest competitive advantage is patience and a long‑term perspective.

There is no question that passive investing deforms the market and creates new opportunities for active investors. Every day verifies this for us. At the same time, we realise that the present trend may still endure for some time and it may seem from the outside that our conviction as to the correctness of our investments is not reflected into the price of our portfolio. This can happen, and it would be nothing out of the ordinary. In any case, this would constitute only a passing phenomenon. This brings to mind a story from 20 years ago.

A story 20 years old

In the 1990 s, I was a co‑owner of Atlantik FT and was working as a broker serving foreign investment funds investing on the Czech market. Among my clients was the company GMO. Almost exactly 20 years ago, I was sitting in their office in San Francisco, discussing the market with one of their portfolio managers. He was complaining to me that the US market seemed to them overly expensive and that they would rather hold back. At the same time, he was telling me that they were under great pressure from their clients, who were scolding them for not being aggressive enough. The clients wanted them to buy the stocks everyone else was buying and argued that the prices would keep on going up and so the funds should disregard such meaningless details as that the companies had no profits and were trading at valuations which essentially could not in any way be justified.

Many years later, I read in some text from Jeremy Grantham (the “G” in the company’s name) how this had all worked out in the end. GMO had stood its ground. For three years it appeared as though they were completely unskilled, because it was so easy to make money in stocks! Then came the year 2000 and a dramatic market crash. Due to its conservative approach, GMO fared very well and its portfolio’s performance strongly validated what it had done. Meanwhile, however, it had lost half of its clients. I don’t know how things turned out for those clients, but my guess is that they probably lost most of their money.

I have great admiration for GMO. They faced up to great pressure and preferred being the target of criticism for poor returns than to be criticised for risking too much. We want to follow this example in our own investing. It would be very easy to make some quick money by aggressively buying the largest stocks in the main indices, closing our eyes to the fact that they are overpriced, and hoping that some even greater and greedier fool would later buy them from us. I think you know very well that we will do no such thing, and I believe that we clearly understand one another in that regard.

Comparison with an index

On the topic of indices, the question arises as to whether it makes sense to compare the performance of funds with an index. Of course it makes sense, but there also are a number of pitfalls in that. First of all, which index is appropriate for comparison? We are a global equities fund, and therefore we use the MSCI World Index. We are not a European fund, a US fund, or an emerging markets fund, and therefore such indices would be meaningless for comparison. A second question, then, is in what currency the performance should be compared. Our fund calculates returns in Czech crowns and hedges against currency risk. This means that it does not bear one large risk characteristic of global investing, and that is the risk of currency movements. Eliminating that risk has its price, of course, and these costs also should be reflected in any comparison with the index.

Another thing that needs to be accounted for is that the returns of our fund will differ markedly from those of the index over the short term. Whereas the index is rather broad, our fund is concentrated in approximately 20 stocks. Therefore, if in some short period the Fund’s returns are approximately the same as those of the index, this is probably an exception. Most of the time the returns will markedly differ. In our worst year, we came in 45% below the index, whereas in our best year we exceeded it by 179%. I would think we will not exceed either of these percentages in future, but the returns in the individual periods will certainly differ.

Comparison is one thing, but trying to beat the index is quite another. If a fund manager strives to continuously beat the index at all costs this necessarily leads to sometimes investing too aggressively and taking on undue risk. Therefore, we undertake to do no such thing and are not intending to do so. There are periods when it is much better to hold back and give preference to controlling risk. As we have written in the past, in early 2009 we changed the Fund’s strategy to the one we are applying to this day. In the context of this strategy, it can be expected that the Fund will lag the index in periods of a substantially bullish market while faring better in periods of market declines. This is what feels right to us.

Changes in the portfolio

We sold Deere and IBM.

Deere is a cyclical company. We bought it in a period when the market was overestimating the impacts of a cyclical downturn and now we sold it because it seems the market is beginning to overvalue the impacts of cyclical recovery. Our return was 42%.

We started selling IBM just after the US presidential election and sold the last remaining shares in spring. Due to Trump’s victory, there surprisingly occurred a possibility for tax reform the main component of which would be to decrease the corporate income tax rate. We started to reflect this possibility into valuations of US companies. IBM has an effective tax rate of around 15%, and therefore it will realise almost no benefit from such tax decrease as compared to companies having effective rates of 35%. Therefore, IBM suddenly became a much less attractive investment opportunity than it was before the election.

After a long time, we have no investment in the technology sector. Here is a small recapitulation of our investment forays into tech stocks since 2009: In that time, we bought and sold Oracle (2×), Seagate (2×), Microsoft, Hewlett Packard, and IBM.

Here is an overview of returns:

Oracle +16%

Seagate +56%

Seagate +32%

Microsoft +70%

Oracle +33%

Hewlett Packard + 123%

IBM −6%

We were rather careful with tech stocks. After all, this is a dynamically changing sector and one can easily stumble. In the end, the returns are not bad, even though they could be attributed in part to the fact that we were in a bull market the entire time and only in part to our stock‑picking. We will never know this precisely.

This is well illustrated by the example of Microsoft. When we were buying it at USD 22, there was a prevailing opinion on the market that this was a company nearing its demise. You may remember discussing it at the shareholders’ meeting. We did not share this opinion, and therefore we bought the stock. It took a while, but then the market’s opinion started to change. The stock went up by 100% and then another 100%, then put on a bit more still. An interesting thing is that overall profits today at Microsoft are lower than when we bought it, and earnings per share are approximately the same due to share buybacks. The entire large price increase was due only to overpricing by the market.

We have bought the stock of a private equity company. Private equity can be a good business, but it depends on the people involved. We believe the company we bought into is at the top of its field, and it has been for more than 30 years. Its basic activity is to invest its capital into companies that are not publicly traded. One can easily become a party to this by buying its stock. Thus, we avoid two common disadvantages of private equity investments, which are frequently high fees and a necessity to remain invested for a number of years. In this case, we pay no fees and we can sell or buy more of the shares at any time. In addition, the company externally manages rather large private equity funds and the fees for their administration more than sufficiently cover all expenses for its operation. We really like this combination.

Original disclaimer: This document expresses the opinion of the author as at the time it was written and is intended exclusively for promotional purposes. The investor should base his or her investment decision on consideration of comprehensive information about the Fund, which may be found in the Offering memorandum. Only a qualified investor pursuant to § 272 of Act No. 240/2013 Coll. may become a shareholder of the Fund. Persons who are not qualified investors pursuant to the aforementioned provision of the Act shall not be allowed to invest. The value of an investment may increase and decrease. Neither return of the amount originally invested nor increase in the value of such investment is guaranteed. The Fund’s past performance is not a reliable indicator of future investment returns. Our estimates and projections concerning the future can and probably will be incorrect. You should not rely upon them solely but use also your own best judgment in making your investment decisions. The information contained in this letter to shareholders may include statements that, to the extent they are not recitations of historical fact, constitute forward‑looking statements within the meaning of applicable securities legislation. Forward ‑looking statements may include financial and other projections, as well as statements regarding our future plans, objectives or financial performance, or the estimates underlying any of the foregoing. Any such forward‑looking statements are based on assumptions and analyses made by the Fund based upon its experience and perception of historical trends, current conditions and expected future developments, as well as other factors we believe are appropriate in the given circumstances. However, whether actual results and developments will conform to our expectations and predictions is subject to a number of risks, assumptions and uncertainties. In evaluating forward‑looking statements, readers should specifically consider the various factors which could cause actual events or results to differ materially from those contained in such statements. Unless otherwise required by applicable securities laws, we do not intend, nor do we undertake any obligation, to update or revise any forward‑looking statements to reflect subsequent information, events, results or circumstances or otherwise. Before subscribing, prospective investors are urged to seek independent professional advice as regards both Maltese and any foreign legislation applicable to the acquisition, holding and repurchase of shares in the Fund as well as payments to the shareholders. The shares of the Fund have not been and will not be registered under the United States Securities Act of 1933, as amended (the “1933 Act”) or under any state securities law . The Fund is not a registered investment company under the United States Investment Company Act of 1940 (the “1940 Act”). The Fund is registered with the Czech National Bank as a foreign alternative investment fund for offer only to qualified investors (not including European social entrepreneurship funds and European venture capital funds) and managed by an alternative investment fund manager. Investment returns for the individual investments are not audited, are stated in approximate amounts, and may include dividends and options.

About The Author: Daniel Gladis

Daniel Gladis, based in the Czech Republic, has amassed a market-beating track record since starting VLTAVA Fund in 2004. VLTAVA Fund is a value-oriented, research-driven investment fund focused on investing in good companies run by quality management. Previously, Daniel was Director and Chairman of the Board of Directors of ABN AMRO Asset Management (Czech) from 1999–2004. He was also Director and founder of Atlantik finanční trhy, a.s., a member of the Prague Stock Exchange. Daniel is a graduate of VUT Brno and has authored the best-selling book Naučte se investovat (Learn to Invest).

More posts by Daniel Gladis