This article is excerpted from a letter by MOI Global instructor Elliot Turner, managing director of RGA Investment Advisors, based in Stamford, CT and Great Neck, NY.

2018 was a watershed year for turning this formerly illegal activity into a regulated, legal activity. Many regular people cheered and entrepreneurs greeted the news with enthusiasm. Meanwhile, the stock market hardly noticed. From the first two sentences, you may have thought we were writing a prelude to a marijuana company pitch, but you need not worry, we have yet to find an investment even tangentially related to marijuana that is not inflated with hot air. Instead, we will use this space to present to you our investment in sports betting.

On May 14, 2018 the Supreme Court of the United States ruled 6-3 in favor of striking down The Professional and Amateur Sports Provision Act of 1992 (PASPA). PASPA effectively made sports betting illegal in any state who had not already commenced a sports betting system (the four grandfathered in states were Nevada, Oregon, Delaware and Montana, though only Nevada actually had a single-game betting regime in place).[1] [2] The case was commenced in 2011 following a New Jersey referendum in favor of legalizing sports betting in Atlantic City. Consequently, once SCOTUS overturned PASPA, New Jersey was the first new state ready to take a legal bet in a decades. On August 1, 2018, in New Jersey, DraftKings became the first company in the United States to take a legal sports bet through a mobile app ever.[3] That historic bet was powered by a company named Kambi Group PLC, the subject of this writeup.

Rarely can one find companies like Kambi that are well-positioned in an industry undergoing dramatic change, while also reasonably valued in the market. There are a few reasons this opportunity exists as it does. First, Kambi’s ownership base is predominantly European and the European sports betting market is far more mature on the regulatory and technology fronts. Familiarity with the US market and the regulatory regime is complicated and challenging for some Europeans to fully grasp. Second, US investors intrigued by sports betting hardly have Kambi on their radar. In our informal survey of other investors on the space, we have yet to encounter anyone who has heard of the name before, even those who have invested in companies premised on their exposure to the sports betting opportunity. Good evidence of this is a Bloomberg article boasting how “Draftkings’ Legal Betting Shows How Big Gambling Can Be.”[4] There is not a single mention of Kambi, though there is much excitement about the scale of the opportunity. In the hundreds of articles we have scoured from mainstream sources like Bloomberg and the Wall Street Journal, there is hardly a mention of Kambi anywhere. We are quite fond of this setup.

In gold rush industries, the saying goes: “invest in the picks-and-shovels, not the gold miners” and we think the sports betting industry is no different. Kambi is the “picks-and-shovels” in the form of a SaaS provider of the tools the “gold miners” (aka the sports books) need in order to conduct their business. We have always been fond of the SaaS business model for its recurring revenue nature and high customer-level margin profile; however, given the market shares this infatuation multiples have become incredibly stretched at US-listed SaaS companies. Worse yet, many of these high valuation SaaS companies have yet to prove their business models can be profitable over the long-run. Kambi is different. They are both profitable and valued at a fraction of the sales multiple of the more glamorous SaaS names.

Kambi has a $430 million market cap and a $402 million enterprise value. The company is headquartered in Malta, and listed in Sweden on the NASDAQ OMX under the symbol KAMBI, with a pink sheet ADR in the US under the symbol KMBIF. Kambi boasts many of the qualities we often espouse in our commentaries: the people operating the business own meaningful equity, have a history of innovating in product and business model in their sector, are applying technology to old industries, benefit from strong secular tailwinds, boasts high margins and even higher incremental margins, and multiples that are downright reasonable. In fact, while Kambi’s stock has compounded at around 32% since its June 2014 IPO, its EV to Forward Sales (EV/S) multiple has contracted from about 4.5x to 3.25x. In other words, the returns in Kambi’s stock since inception have come from increasing the value of the business itself.

Kambi’s origins:

Kambi was founded in 2010 as part of a larger company formerly known as Unibet (today Kindred Gaming). Kambi CEO Kristian Nylen and his cofounders at Unibet saw an opportunity to take the prowess they had developed in setting lines and managing risk for the Unibet sports book and packaging it as a full service, business-to-business backend for both established and aspiring sports book operators. Founding essentially meant bringing in a customer who was willing to pay for the services other than Unibet and giving 80 employees a seat in the new division. By 2014, Kambi had established meaningful relationships with growing sports book operators, demonstrating robust top line growth and a scalable cost structure. The concept was thus proven and in 2014, Unibet decided that Kambi would need independence in order to achieve its highest ambitions. Independence from Unibet would be instrumental in Kambi’s go-to-market strategy of trying to win business with operators who may be competitors of Unibet in some or all jurisdictions. It would also afford Kambi its own institutional imperative and opportunity to forge its own unique identity separate and apart from a parent, while aligning incentive structures for employees. As such, on May 20, 2014, shares of Kambi were spun off to Unibet shareholders and Kambi became an independent public company.

Kambi’s business model is smart and aligned with their front-end partners. Partners who use Kambi have a better menu of possible wagers, can offer more lines in more situations, and are ultimately more profitable. The company charges a take rate in the low to mid-teens percent of net gaming revenue in exchange for providing their services. Net gaming revenue is the revenue an operator earns after deducting all regional and federal taxes and promotional activity offered by the operator from gross gaming revenue (GGR). Kambi’s revenue can be calculated as follows

Kambi Revenue = (GGR – promotions) * (1-tax) * (take rate)

The Industry Landscape:

Stated simply, the industry is highly complex. The complexity itself is multi-faceted. This is an industry with black, gray and legal markets. In places where sports betting is legal, investors and operators must contend with a highly fragmented regulatory regime, where each domicile has different rules and taxes. Plus, there are multiple layers of companies operating in the industry who in some respects look like competitors, while in other respects they may be partners. Establishing an addressable market for the industry, let alone a given company focusing in a niche is thus a complex endeavor itself.

Essentially there are three ways sports books make lines (the following three are paraphrased from The Logic of Sports Betting by Ed Miller and Matthew Davidow)[5]:

1. Algorithms that rely on troves of data to estimate probabilities.

2. Scraping lines from publicly available betting sites on the Internet.

3. The market making price discovery function.

None of these are mutually exclusive and the best bookies rely to some degree of all three. For bookies where the algorithms drive the lines, human traders add an overlay and reassess changes in model inputs that a computer simply cannot see on its own.

A recent example illustrates why this is so important:

[6]

[6]When Andrew Luck announced his sudden retirement on August 24, 2019, the Borgata sports book, (run by GVC) held its lines related to the Colts for extended periods of time. Any time a quarterback will miss time, especially one with the skill of Andrew Luck, betting lines related to the team should change. This mistake at the Borgata afforded the opportunity for some sharp bettors to place action on stale lines, reflecting imperfect information. The bettors gain in this case is the book’s loss.

The landscape in the United States offers a nice microcosm for the challenges the entire industry faces. While the repeal of PASPA opened the door for legalized betting on the state level, the Interstate Wire Act of 1961 (The WIRE Act) effectively makes interstate sports betting efforts illegal.[7] As a result, even if sports betting were legalized in each and every state individually, there would be challenges in operating a national sports betting business.

Here is a good map that as of the time of this writing, shows where each state stands:

[8]

[8]Even if every state does eventually legalize sports betting, each state has taken its own approach to creating an industry structure. Effectively there are three distinct market structures states can choose from:

1. Open competition. Allowing any and all worthy operators with a license the opportunity to compete.

2. Monopolistic/oligopolistic licensing structure. So far this typically evolves in states with an existing, but limited brick-and-mortar betting industry, where operators are given the right to launch their own sports books.

3. The lottery structure whereby the state owns and operates the book itself.

Each state has approached the distinction between brick-and-mortar and mobile licensing differently. Some have only legalized brick-and-mortar, some have fully legalized mobile, while others have legalized mobile with the requirement that either funding or withdrawal be done at a brick-and-mortar location. As for the parties that actually take bets, there are two basic business models: those who are fully integrated and make their own menu and betting lines, and those who rely on an outsourced provider for the menu and lines. No two operators in either bucket are exactly alike.

The front-end, in general (whether it be for integrated operators or pure front-ends) is a low margin, highly competitive business, while the back-end is structurally higher margin with considerable operating leverage and meaningful points of differentiation between offerings. While front-ends primarily invest in customer acquisition, back-ends invest in research & development in order to build out their capabilities and enhance their offerings.

Scale is incredibly important in making good lines; however, the balkanized regulatory regime makes scale a complex challenge. With greater scale, a book can take less “proprietary trading” risk and end up with better matched markets. A scale operator sees more flow and has insight into whether their lines are priced appropriately. An important value in seeing this kind of scaled flow is how the operator can build customer files and know who is a “sharp” bettor. If all the “sharps” are coming in on one side, it becomes a strong tell that a line is mispriced. Pulling this all together, scaled operators have less variance in their daily, weekly and monthly profitability. Further, scaled operators can offer a bigger menu because the costs to build out each pillar of the betting business are largely fixed. The quest for scale is even more important insofar as in-game betting is concerned (discussed more below), where lines must be priced every second, requiring distinct technology for both the estimation of probabilities and the acquisition, incorporation and delivery of the information.

One of the big distinctions industry people talk about in sports betting is the “European vs Vegas model.” The Europeans tends to focus on user experience and the entertainment angle to sports betting, whereas Vegas is far more interested in the skill and quantification thereof. Kambi put this rather succinctly: “So from the end-users’ perspective, we believe that we are in the entertainment business. We help our customers to provide a service to our end users — or not a service but an experience to our end users. And if the end users do not find that experience compelling, they will easily move to another sports book and put their bets there.”[9] Vegas is more purist and idealistic in the “American” way, thinking the “best odds” (aka lowest vig) are what win customers at a book. These differences in perspective have consequence, because in the early stages of regulation in the US market, the European companies have had a considerable advantage getting to market. European companies are already profitable, with scalable technology infrastructures. In contrast, American ones (represented colloquially as “Vegas”) were never built for scale and never had the opportunity to open up for in-play betting.

Kambi’s solution:

Kambi offers its partners two essential services that are related to one another—1) they build the menu and set the lines, and 2) they manage the risk. Here is Kambi’s explanation for how the process works:

What you do when you deliver this end-user product called sports betting? You can look at it this way, somewhere in the world 300,000 events per year is played in all various types of sports. They may have some relevance to some end users to bet on. We buy data from all these events in realtime. And this date then streams into our system and our organization. So there we work with a mix of specialist traders and algorithms. So we use that data to — for any really type of occurrence of what can happen here to predict the outcome. So I think we heard before, we — today, we do in a month 480 million predictions like that, which is what we call odds spin. That’s about 100 predictions per second.

And we actually don’t think that we get this right every time. It is impossible to, at that scale with a quite small margin, get that probability right every time. And that leads us onto the third part here, which is really a core part of what we do, and that’s the risk management. So in the lifecycle of an odd as we publish it on the site, a lot of new information comes. You have bets being placed, you have market movements, you may have injury news, you may have a really big bet or you may have really a high accumulated risk for one operator. And our risk management is about really optimizing at all times the price given this new information that we get.

At the heart, really, of risk management for us comes what we call player profiling. So this is about for every end user really that does something with our product, we build a profile of future profitability of that player. In around 98% of the cases here, we don’t really act on the information from end users from a risk management perspective. But around 2% of the players, they actually come with new information to us that we use in the trading. So adapt the price.

Further, Kambi gives their partners great latitude in how they want to use the platform for their own differentiation:

“How Kambi differs from its competitors is that it offers this freedom, this flexibility, to innovate, to create and to build a sportsbook as desired. Kambi takes all the heavy lifting through the provision of sophisticated technology, a powerful sportsbook core and an experienced trading and risk team to deliver exciting sports betting experiences, while the operators, if they so wish, can work with us to co-create how those experiences are packaged and presented, as well as what levels of vig are applied per sports and per market.”[10]

Kambi’s edge stems from their ability to offer large scale, leading partners, across geographies:

- Easy integration using Kambi’s APIs

- A scalable software platform with little down time

- Integrity

- Quick access to markets following regulatory change.

- A broad menu of diverse betting options, priced appropriately

- A fair operator margin

Key partners (in no particular order) include Kindred, 888 Sports, BetPlay, Draftkings, Rush Street, Penn Gamin and more adding up to about 25 total relationships.

Back-end is the SaaS end:

“I think the biggest change that has happened for us here — the last 4 years is when we really moved over from delivering a service including a front-end client. We then started also delivering a service where you don’t need to take our client, you can work directly on our APIs. You have our full product either end to end with a mobile and web client or you can work directly on our APIs and create this yourself.”[11] – Erik Logdberg, Deputy CEO & Chief Business Development Officer

In the call following the announcement of Flutter Entertainment’s merger with The Stars Group (TSG), there was an insightful exchange on the lack of synergy between a front-end and back-end in sports betting:

Edward Young, Morgan Stanley, Research Division – Equity Analyst

I’ll ask 2 genuine questions. The first one is could you just elaborate a little bit what you meant on the conservative API approach to tech integration? And does that affect your capacity to generate additional synergies above that GBP 140 million target? And the second one is, are there any gray markets that TSG operates in that you or the Flutter Board would consider exiting?

Jeremy Peter Jackson, Flutter Entertainment PLC – CEO & Director

Okay. Thanks, Ed. Look, in terms of the first question about a conservative API approach, if I look at how we manage the Paddy Power Betfair integration work, we effectively had to turn the Betfair technology stack into something that could operate on a certain multi-brand, multi-jurisdictional basis. And we then migrated all of Paddy Power onto its back, and it’s a big, complex thing to do.

Since then, we’ve actually been able to separate our front-end and back-end platforms such that our front-end platforms communicated our back-end platforms by APIs. And that will allow us under this transaction — this proposed transaction to effectively allow teams with their own front-end platforms to maintain those product road maps, but then just to fit into a back-end betting platform and our global risk and trading capability, which we think will allow us to maintain momentum into the business, maintain individual identities associated with the brands but still deliver some considerable cost savings.

Jonathan Stanley Hill, Flutter Entertainment PLC – CFO & Executive Director [4]

The only thing I’d add there is it also — we feel is a much better customer proposition for enabling the front — the local teams and the brand teams to maintain their own identity and deliver really what the customers are after. [emphasis added][12]

Following the completion of the Flutter and TSG merger, the combined entity will be the largest sports betting company in the world. The foremost synergies in the deal come from “API based technology integration” though that effectively means that TSG will no longer run its own platform and all incremental investment to improve the product will be foregone and narrowed. The entirety of the synergies add up to 7.3% of TSG’s revenue run-rate (and even less so on the 3 year forward revenue guide, in the year in which synergies are actually meant to be achieved) and 3.7% of the combined company’s revenues. Simply put, the synergies are a fraction of the rationale behind the deal, with cross-selling the customer file serving as the primary motivation.[13]

The fact that the back-end’s relationship with the front-end, even at the largest sports book in the world, is so “complex” is the ultimate validation of Kambi’s raison d’etre and strategy. In effect, within Flutter, you have two separate companies with little vertical synergy, relationship or cross pollination between the teams. Front-ends have fundamentally distinct skill sets from back-ends. Front-ends have customer files and marketing prowess, whereas the back-ends are the technology. The Flutter team makes it abundantly clear that the front-end and back-end are essentially two entirely different businesses. Meanwhile in the industry there is only one other back-end who can adequately service both retail and mobile needs (SBTech) and a few others who do well at retail but suffer mightily online (William Hill/IGT, Don Best, NYX). If you want the best multi-jurisdiction sports book, Kambi is essentially the only option for a high quality operator.

A look at the common-sized income statement of Kambi (a pure back-end) versus Kindred (a pure front-end) paints a clear picture of the distinct differences in the two business models:

Note the higher EBIT and EBITDA margins at Kambi, despite boasting well over double the top line growth rate, in an investment phase. The two highlighted lines are the big points where Kambi must spend more than Kindred, but importantly, these are the two lines with the most leverage on the income statement. As Kambi grows, the highlighted expenses will shrink, while Kindred will remain in steady state in aggregate. The clear difference between the front and back-end here is how the back-end invests in its human and technological capital (human capital is captured in “Administrative Expenses” where just less than half of the line is covered by personnel and personnel related expenses), while the front-end invests in marketing. This is the skill divide between the two: back-ends are competent in technology, while front-ends are competent in customer acquisition. Flutter’s emphasis on “cross-selling” with 18 references littered throughout their merger call hammers home this distinction in competency.

The beauty of the SaaS model from Kambi’s perspective is how it translates to very high incremental margins. There is very little incremental cost to onboard a new partner. Instead of charging customers a fixed fee per month, Kambi charges a take-rate on NGR of approximately 15%. We do think there will be some modest atrophy to somewhere around 13% over time as some larger customers achieve their scale ambitions, while remaining on Kambi in order to protect the front-end’s own profitability. Meanwhile, Kambi can continue to invest in product development and share the benefits of that investment with their partners. Kambi has 700 employees today, which includes 250 traders and 200 developers. The trading team is the non-SaaS piece; however, that is already at its mature size. Meanwhile, the company is recruiting more developers in order to continue enhancing the technology side. A key area within technology is risk management, where you need a higher degree of control to make sure no one has better information and better stakes. The infrastructure to aggregate, analyze and apply data is also a key area of investment. As of today, Kambi makes 450 million odds changes per month. In order to accomplish this feat, you need exceptional technology and people behind it. The investment is considerable and few, if any front-ends have the scale in order to do it on their own.

Partner with Integrity, Build Industry Knowledge:

“And the reason why is because we have that one solution and what it includes in it is about challenging mindsets, it’s about educating. And what we focus on is that second point there. Don’t turn up for meeting with the CEO or a Chairman or Board member or anyone if you haven’t got something insightful for them to take away from it. They may not buy from Kambi then, they might not buy in the next 3 years, but if they come to see Kambi, they’re coming to some get information and insight because they know Kambi really understands what they are doing. And that’s the difference. That opens doors. That’s what makes us stand out. We’re not there to just try and sell from — straight from the beginning. They will understand through our insights, “You know what Kambi knows something that we have don’t.” So even if they’ve got full trading solutions themselves internally, you go, “Hey, I really understand that Kambi could help us here, maybe we should consider things, maybe we should take more meetings, maybe we should meet the CEO of Kambi, let’s have more conversations.”[14]—Max Meltzer, Chief Commercial Officer.

“First of all, our unwavering commitment to integrity and corporate probity. Kambi is a [NASDAQ] listed company and therefore holds itself up to the highest of standards. For example, since our inception we have been careful to avoid markets where gambling is prohibited. This was a conscious and long-term decision as, not only is it the right thing to do, but we realized it was likely to be looked favorably on by regulators when moving into new territories in the future – particularly in the U.S. which has always been a key part of our long-term business strategy.”[15] –Max Meltzer, Chief Commercial Officer.

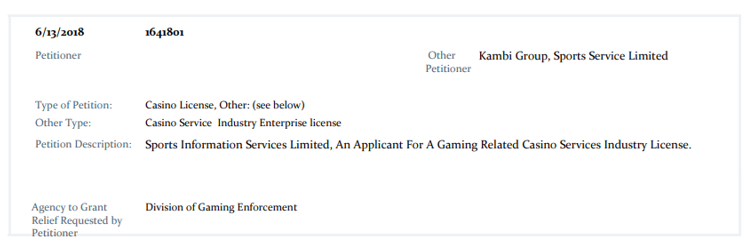

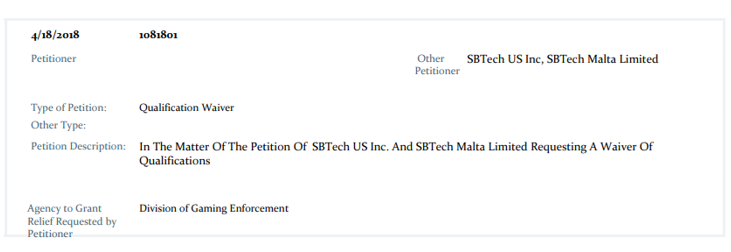

Kambi is discriminant about who they are willing to partner with and will only partner in regulated markets. This is important for both regulators and prospective partners, as their primary competitor in the pure-play back-end is not nearly as discriminant. SBTech is the company’s foremost competitor and was recently rumored to be in late stage talks to be acquired by Draftkings. Nylen has pointed out that he “think[s] it’s positive rather than negative that we have a good competitor nowadays, and I think the market is definitely large enough for both (SBTech) of us. But so far I am very pleased that we have been able to win our top targets.” Competition offers Kambi the opportunity for differentiation and one of the key pillars has been on integrity. While some of this can change, it is notable how Kambi received an actual license as a “Sports Information Services Limited…For A Gaming Related Casino Services Industry License” whereas SBTech settled for a temporary “Qualification Waiver.”

[16]

[16] [17]

[17]Pennsylvania, the other large, early legalizer of sports betting on the state level gave SBTech conditional approval and cited concerns with the company’s partnership relationships that enable betting in Iran.[18] While SBTech is insistent they do not facilitate operators in Iran, their response perhaps implicitly acknowledged they know some of their operators function in what the betting world calls “gray markets”: “To be very clear, SBTech does not operate in any black markets.”[19]

Scale + Time = Compounding Advantages

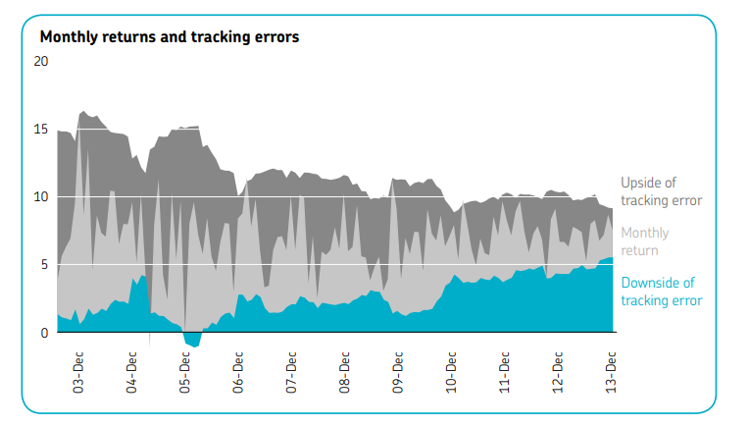

The two outside lines illustrate the upside and downside tracking error representing a 95% confidence interval. The selected confidence interval indicates that on average, for 19 months out of 20, the actual return should be between the two tracking error lines.

Over time the tracking error band has become narrower, indicating that the monthly margins have become more stable. The increased stability is primarily due to a relative increase of live betting, which is less volatile than pre-match betting, and a stabilizing effect resulting from Kambi’s risk management tools becoming increasingly sophisticated in identifying and managing different customer segments.

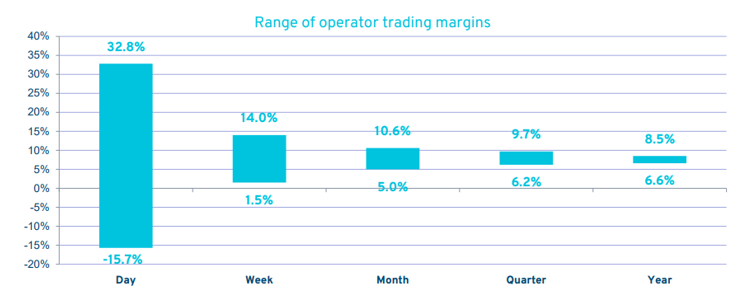

While Kambi has not revisited this specific chart, they have shown what the daily, weekly, monthly, quarterly and annual distribution of operator margins looks like:

[20]

[20]This is the nature of a business relying on assessment of probabilities. You can set the right probability for an outcome to happen, yet still lose. Without skill, the longer time-frames would also be random; however, with skill the longer timeframe would smooth the outcomes. That is clearly the case here. While the day-to-day can be volatile, the range of outcomes narrows as the timeframe is extended. We have spoken to industry experts, including employees at Draftkings involved in onboarding Kambi and at Kambi involved in managing the Draftkings relationship. One fundamental truth we have seen acknowledged on both sides is that Draftkings would be less profitable at their sports book and would take a period of three years before they can get their models up to Kambi’s skill and stability today. Meanwhile Kambi will continue improving, such that Draftkings would be trying to catch a moving target.

This risk management side is especially compelling. Kambi is phenomenally good at using anonymized information in order to hunt down people who are sharp betters and have figured out ways to whittle down the book’s edge. Sharp bettors find this especially frustrating and have come to facetiously call the company “Kan’tBet” for how little action they are willing to take from the experts; however, this is exactly why front-ends use Kambi. Notably, Kambi will take action from these people, but in small amounts, because learning their intents help in the process of refining their own line making.

Vegas as often been more willing to take this kind of action and the sharp bettors claim this is the fundamental flaw in the European model. Kambi brings their distinctly European model to the front-end operators they work with, even in the US. On their capital markets day, they pointed out how:

Ever since I started in 2005, we have looked at this chain being about one thing. And that’s not about margin, that’s not about accuracy and probability predictions. In the end, it is about user experience, it is about delivering entertainment. So our quant analyst, for instance, they’re not tasked with the sort of theoretical challenge of only predicting probability, they’re tasked with a challenge of delivering a fantastic experience. —Erik Logdberg, Deputy CEO & Chief Business Development Officer

Handicapping the probabilities is obviously an important endeavor, but so too is managing the user experience. Kambi does not exist to serve as a counterparty for sharp bettors. If a book consistently provides opportunity to those with an edge, the book will lose money. There are hedge funds and advanced quant strategies launching in an attempt to take advantage of inefficiencies in betting and the beauty of it from Kambi’s perspective is how the adverse selection bias of skill in risk management will ensure that those books who are not good at identifying sharp bettors will ultimately perish before the harvests of the industry landgrab are reaped.

Kambi is not resting on its laurels as a European Model innovator. Instead, the company is opening its first US office in Philadelphia, a strategic location given both Pennsylvania and New Jersey are the large, early-adopter states.[21] In keeping with management’s culture of shareholder value, Philadelphia was strategically selected for its lower costs than New York City or other technology hubs, its passionate sports fanbase and its many high quality universities offering a good opportunity set on the hiring front. The company is “ hoping to take people who have a passion for sports — maybe they’re in another business like finance or whatever — and convert that into what we need from an operational perspective — trading, risk management, sales, partner success.”[22] To date, Kambi’s progress in US markets has come without an on-the-ground premise here. The US office opened in Q2 and is in the process of staffing up. This will only help as more states legalize and regulate betting.

Adding it all up to shareholder value:

Kambi boasts large insider ownership and is operated by its founders, with a shareholder friendly management team and aligned interests. They both say and do the right things:

“Moving on to our shareholders. On top of what I’ve talked before, which is naturally also important for our shareholders, is to have a return on their investments. And one of the absolutely most important task for us, as the management team, is to have a very stringent and sophisticated approach to our capital and resource allocation with the ambition of securing a high return on investments for our shareholders.”[23] –Cecilia Wachtmeister EVP of Business & Group Functions

The company has a mandate to think long-term in capturing the large opportunity, while remaining anchored in establishing measurable, deliverable goals:

“and we have further evolved it during the last year, a very established strategy process where we set our long-term strategy on the 3 years horizon. We break that down to company performance target on a yearly basis, which in turn gets broken down into quarterly key objectives. And that gets actually broken down to departmental and team level within the company. And in that way, we’re really having the connection between what we want to achieve as a company and what is expected from each and every one of the employees. It’s a very, very solid and thought-through process. And we, as the management, we monitor this on a monthly basis how the progress is and where we are.”[24] –Cecilia Wachtmeister, EVP of Business & Group Functions

This will help innovate Kambi develop and tailor products that are more sanguine for the US sporting environment and create a local salesforce in the pursuit of partnerships.

Sizing up the TAM:

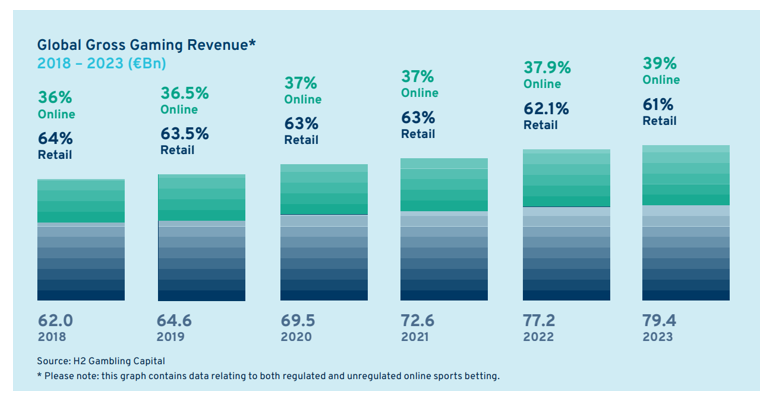

In Kambi’s 2018 annual report they offered the following estimate for global sports betting GGR in 2018 and five-year forward forecast:

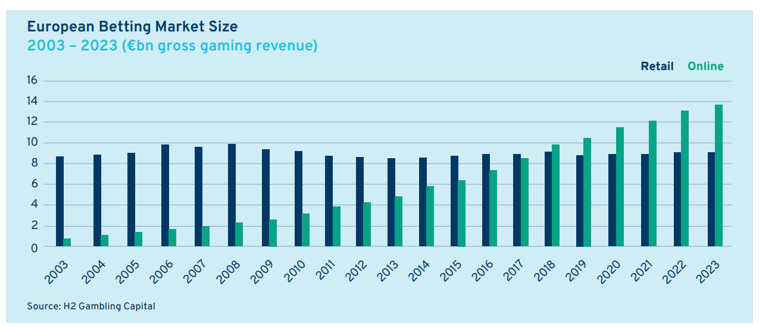

[25]

[25]Historically, Kambi has operated primarily in Europe, which is about a €20b plus GGR market. 2018 was the first year where online betting exceeded retail in Europe and this trend of growth coming from online will only continue to accelerate:

[26]

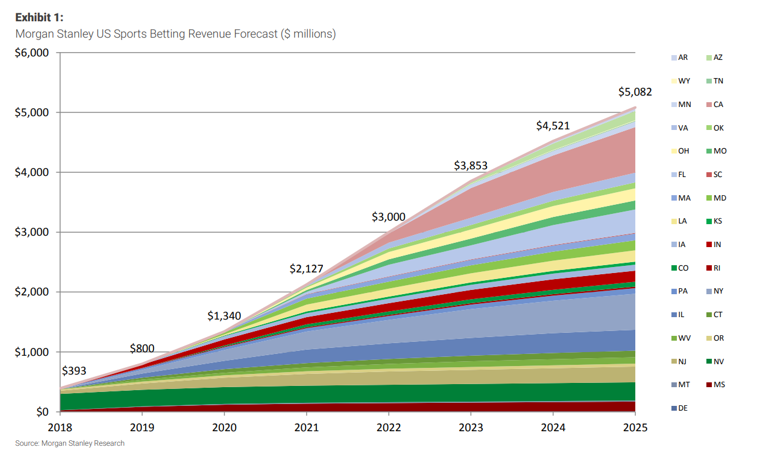

[26]The repeal of PASPA makes the US perhaps the most compelling market and largest opportunity the industry has ever encountered. Shortly after the SCOTUS ruling, Morgan Stanley pegged their base case 2025 revenue opportunity (in this case, revenue is a proxy for GGR) by 2025 at $5 billion:

[27]

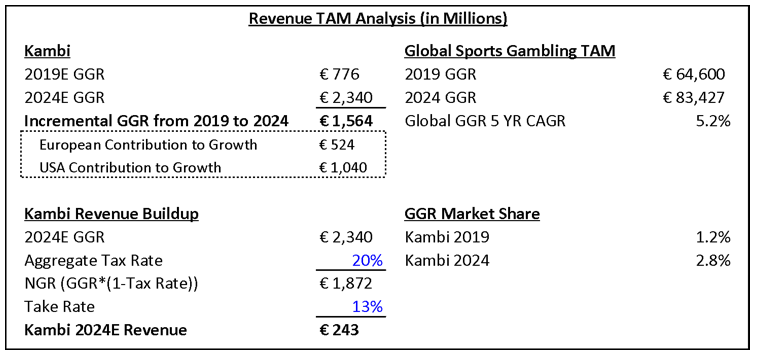

[27](Please note, while the above chart is in US Dollars, much of the below conversation on TAM is covered in euros given that is the reporting currency for Kambi. Pay attention to the currency, for we change from euros to dollars depending on the source). The entire regulated market globally generated €5.4b in GGR in 2018 and is expected to grow to €11.5b by 2023 (a 16% CAGR). In order to translate that into a revenue opportunity for Kambi we need to know both the average tax rate across all their regimes and the company’s take rate; however, neither is precisely knowable. We will visit the assumptions later, but for now let us work with a 20% all-in tax rate (arguably on the high side) and a 13% take rate in order to translate GGR into Kambi’s revenue TAM.

Today at €5.4b, Kambi’s revenue TAM is approximately €562m, while in 2023 that number jumps up to €1.196b. Inevitably TAM will be highly sensitive to the cadence of regions legalizing sports betting. And thus far there are pieces of evidence that show regulated market GGR could exceed expectations. We think there is a degree of conservatism embedded in these numbers and that is a good thing insofar as planning corporate strategy and analyzing risk/reward in investments goes. For example, the American Gaming Association believes the illegal sports betting market size in the US to be “at least $150 billion annually.”[28] It is incredibly challenging to size up an illegal market.

When we think about addressable market, the upside of converting a black market to a regulated market is intriguing. This is true for several important reasons, mainly built around the idea that establishing trust in a regulated market is far easier than in an illegal bookie scheme. Some people simply won’t engage in an illegal activity even if the general idea is appealing. Some people may just hold back on the actual volume they would like to play. Most importantly though is the innovation and creativity that legalizing these markets unleashes for the industry. In Europe, it is said that over 70% of all sports betting occurs “in-game” versus less than 5% of US-based action occurring in-game pre-PASPA repeal.[29] In-game creates novel experiences and relies heavily on technology ranging from challenges in data and speed to building sharp algorithms to price probabilities in real-time and managing risk, while adding a human overlay in order to adjust to rapidly changing circumstances. For example, were a starting QB to leave the game with injury, the odds of the next play being a completed pass would be drastically different than immediately before the injury. It’s simply impossible for an illegal bookie to even contemplate offering in-game betting, meanwhile in many respects, this is Kambi’s specialty. In-game betting is basically entirely novel to American sports bettors, yet in some respects, our favorite sports are perfectly suited for this opportunity.

As a result of these unknowns, the range of potential TAMs is incredibly wide. Most US analysts expect somewhere between a $7.5-12b TAM in the US, base-case, while the American Gaming Association pegs the US market size at $150b total wagers (or the equivalent of $75b in GGR).[30] We do our work based on the low end of these estimates, while viewing any upside as incremental to our expectations.

Valuation:

Our valuation process starts with working backward to solve for the embedded assumptions in Kambi’s stock price. At todays price of around $14.50 USD, the market is pricing top line growth to slow down to a 9% 5 year CAGR and a 10x terminal EBITDA multiple all discounted at a 12% WACC. We think these results are highly achievable, even with the loss of Draftkings as a customer. Before the US market even legalized sports betting, Kambi was growing its top line at a 13.8% rate. That growth was lumpy and was slowing in the later periods; however, its core markets in Europe as of today are still growing at ~8% GGR. Meanwhile its partners are taking share with a combination of organic and inorganic growth, supporting base rate growth assumptions of around 12%. By our estimates, the US business has contributed nearly half of 2019’s 22%+ growth rate. Draftkings has accounted for a little less than half of the US contribution.

One thing to consider in valuation is the asset value and replacement value. Kambi is a truly unique asset and management and ownership recognizes this. As such, they have a convertible note held at Kindred which is effectively a poison pill to prevent a hostile takeover attempt. Draftkings perhaps would prefer to acquire Kambi than SBTech, but no way management is selling. Meanwhile, the rumored Draftkings acquisition of SBTech quoted the prospective price tag as between $300-500 million, essentially bracketing Kambi’s market cap today.[31] SBTech is not public, so their financials are not disclosed though it is well established that they are smaller than Kambi and revenue estimates peg the run-rate at approximately $24 million USD (less than 1/3rd that of Kambi’s).[32] One other point of reference for replacement value is the price Scientific Games paid for NYX and Don Best in order to accelerate their own attempt to get into the sports betting industry. Scientific Games spent $632 million for NYX and around $40 million for Don Best, meanwhile they have no key partnerships to show for it, are suffering from employee exodus and an offering that is sub-par at best.[33]

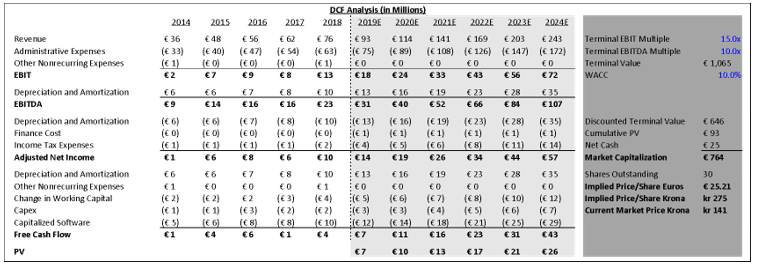

To value Kambi directly, we rely predominantly on DCF. While Kambi does not disclose the GGR or NGR metrics for their operators, we can back into a rough approximation of the historical numbers and forecast them going forward. The key assumptions that we need to make in doing so are on the tax rate, the level of promotional activity and Kambi’s tax rate. Tax rates are the most challenging assumption here because we do not know the geographical distribution of GGR and tax regimes vary widely. Even within the US there is a high degree of variance. For example, Delaware and Rhode Island are lottos with the state getting a direct revenue share equivalent to a 50% tax rate, while New Jersey has an 8.5% tax at land-based sports books, 13% for casino-operated online sports books and 14.25% for racetrack operated online sports books.[34] Pennsylvania, another early adopter, has a 36% tax rate.[35] The UK recently raised their betting tax rate (which includes sports books) from 15% to 21%.[36] We cite these numbers here as illustrative examples. For the backwards numbers we apply a 15% tax rate to build up to our GGR estimate and for 2019 on, we use a 20% tax rate. Our purpose with this analysis is not to precisely nail down the GGR that Kambi’s partners generate, but rather to estimate roughly how much total GGR Kambi needs to capture over the coming five year period in order to rationalize our financial estimates for the company.

As for take rate, we know from triangulating around industry sources and company conversations that today they are in the mid-teens and take rates have come down modestly in the past few years. With some smaller operators, early on, take rates have been as high as the low 20s. Kambi has cited SBTech’s emergence on the competitive front as putting pressure on take rates, though the market is now approaching a degree of stability. Some of the US operators were more insistent on joint venture relationships which have an even higher implicit cost than a take rate, for even lower quality. In a lot of respects, we think of Kambi’s value much like programmatic DSPs for advertising and we would note that the highest quality operator in that sector (The Trade Desk) earns a 20% take rate. Long-term, we expect some modest degradation, though think working with an approximate 15% rate today makes sense. We take that down to 14% in 2021 and 13% thereafter under the assumption that some of the larger operators with long-term deals and little volume as of yet (like Penn Gaming) have come on with more favorable rates than the existing book of business. Here is where we think GGR has come from and where it will go:

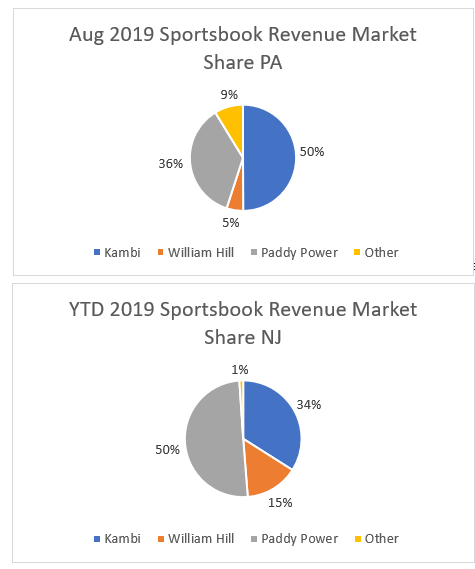

The most important takeaway from this chart should be how much incremental GGR Kambi’s partners need to receive in order to underwrite out-year earnings expectations. In order for Kambi to compound top line at a rate just above 20% for the next five years, their partners need an incremental €1.7b, or $1.9b of GGR. That $1.9b of GGR can come from the US and Kambi’s operators. With the more mature, European online business expected to grow at ~8% annualized (5% tailwind in global GGR w/ excess capture in transition from black/gray markets to regulated) , that means Kambi partners need to capture about $1.2 billion of the US opportunity over the next five years. Given most industry estimates peg the opportunity between $7.5-12 billion in GGR over that time, that means Kambi partners need to capture anywhere from 10-16% of the US opportunity. As of today, Kambi’s market share is well above these levels. Here is how Kambi’s suite of partners stacks up in revenue share in the more mature New Jersey and Pennsylvania markets:

[37]

[37]While we hardly expect these market shares to remain constant over time, we think with its crop of partnerships Kambi has cemented its place as a key provider in the US sports betting industry. Importantly, we see upside not just for the base case market shares, but also for the potential size of the US market. Rather than incorporating that into our estimates, we will leave any upside for optionality on top of our base expectations. Plus in effect, this “US” number we are using here is the rest of the world outside of Europe. Kambi sees great potential in Latin America and APAC though given we are less familiar with those markets and the sporting industry in general is far less mature there, we are not willing to incorporate that into our expectations.

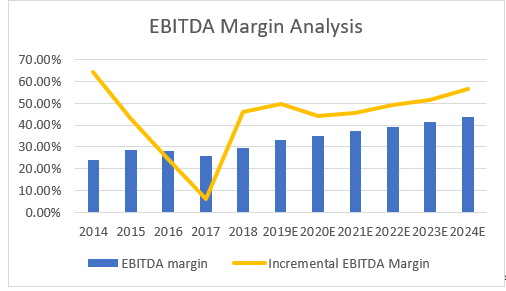

In the investment phase of US market launches, Kambi had formerly guided to 4-6% quarter over quarter growth in operating expenses. That has been taken down this year to 3-5% growth given “in some states, it’s actually going to be slightly lighter-touch application and therefore, by implication, a slightly lower cost for us.”[39] By and large, the operating cost structure is fixed once Kambi launches in a state. As of today, the company need not hire more traders (as discussed above), with incremental investments flowing predominantly into state-by-state launches and technology. The launch costs will roll off and incremental technology investments will continue, though with benefits of scale affording more overall technology investment at a lower percent of revenues. Incremental EBITDA margins are in the mid-40 percents. We expect a low 30 percent EBITDA margin in 2019 that gradually walks up to a low 40% margin in out-years. This adds up to about 200 bps of EBITDA margin leverage per year.

[40]

[40]For our purposes here, beyond EBITDA, we assume fairly modest leverage on technology expense (which is not incorporated into EBITDA) to the tune of 100 bps over the next five years. Pulling it all together, this is how we think about the value in Kambi:

We see a path to a 275 krona stock in Kambi, based on today’s value, which would represent 95% upside to recent closing prices. It is important to emphasize that while the model is close to a straight-line CAGR, the reality for Kambi will be very different. Embedded in here are assumptions on future states legalizing and then regulating betting, including California. Consequently, there will be considerable lumpiness to the actual path. Additionally, sports betting itself is cyclical, with notable spikes around major events like the World Cup and varying degrees of interest in events like the Super Bowl depending on the teams involved. The key takeaway is what the company will likely look like in 2024 once more states have had the opportunity to legalize and regulate sports betting and the United States becomes the most important global market for sports betting. In order to achieve the run-rate we would apply our 15x EBIT multiple (equivalent to 10x EBITDA), Kambi would need to capture the $1.9b of incremental GGR, $1.2b of which comes from the US.

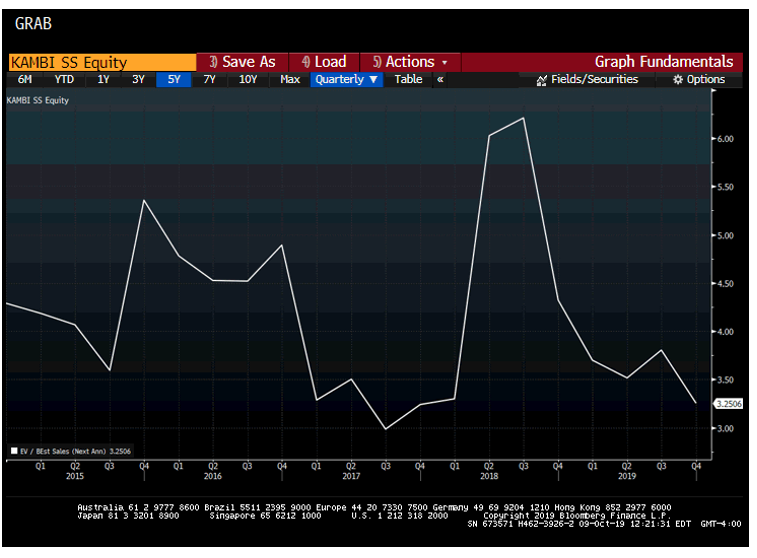

If the US market does not develop as contemplated, the stock today trades at reasonable values. Growth will still register low double-digit levels, on near all-time low multiples at 3.25x EV/2020 S (see chart below) and EBITDA margins registering in the mid-30s. Multiple expansion is unnecessary for a good return, for the company’s top line and cash flow generation would support where the stock is trading today:

The adverse scenario in the US market would still result in a stock that is undervalued on DCF, cruising along as a rule of 40s SaaS operator with long-term margin leverage. The core sports betting market globally continues to grow at about 5%, with the dual uplifts of regulatory acceptance and digitization enabling a better, more engaging experience.

Risk factors:

1. Competition. This can come either from new entrants in B2B or more large suppliers buying or building their own backend. SBTech in particular competes with a broader suite of services including marketing services and digital casino games, while Kambi operates as a pure sports operator.[41] IGT in the US packages in their sports offering with slot machines. Neither boasts the quality of Kambi; however, both use other levers to try and capture their share of the sports business.

2. Regulation. This can manifest in several ways. States can be slower to legalize sports betting than expected. States (and countries) can also be more aggressive on the tax front. The impact of taxes hits twice. Taxes factor directly into the calculation of odds, so higher tax rates make odds less favorable, which translates to lower betting volumes, plus operators must give up more of that volume.

3. Integrity fees. Leagues are strategizing on how they can monetize betting and while no outright integrity fees have been demanded from US leagues there are intimations that leagues will use data in order to grab their cut.[42] Kambi passes these costs on to front-end operators; however, this could negatively impact aggregate GGR.

4. Customer concentration. Kindred Group is an especially large partner globally while Draftkings is a large US partner. Kindred risk is mitigated by virtue of the corporate history, a shared concentrated owner in Anders Ström and a long-term partnership agreement.

_____________________

[1] https://www.law.cornell.edu/uscode/text/28/3704

[2] https://www.legalsportsreport.com/18718/nj-sports-betting-case-2/

[3] https://www.reuters.com/article/us-usa-betting-draftkings-new-jersey/draftkings-launches-mobile-sports-betting-in-new-jersey-idUSKBN1KM60H

[4] https://www.bloomberg.com/news/articles/2019-08-23/draftkings-soaring-legal-betting-shows-how-big-gambling-can-be

[5] We strongly recommend reading The Logic of Sports Betting by Miller and Davidow for anyone looking of a detailed overview for how sports betting itself works, what kind of bets are possible and how sports books make their lines.

[6] https://twitter.com/darrenrovell/status/1165583562025951232

[7] https://www.law.cornell.edu/uscode/text/18/1084

[8] https://www.wsj.com/articles/mobile-sports-betting-is-the-moneymaker-as-more-states-legalize-11567445689

[9] Kambi Capital Markets Day, Sentieo.

[10] https://www.pennbets.com/kambi-interview-max-meltzer-sports-betting/

[11] Kambi Group PLC Capital Markets Day, May 20, 2019. Sentieo.

[12] Edited Transcript of Flutter Entertainment PLC M&A conference call presentation, October 2, 2019, Sentieo.

[13] https://www.flutter.com/sites/paddy-power-betfair/files/documents/Investor-Presentation.pdf

[14] Kambi Group PLC Capital Markets Day, May 20, 2019. Sentieo.

[15] https://www.pennbets.com/kambi-interview-max-meltzer-sports-betting/

[16] https://www.nj.gov/oag/ge/docs/Petitions/2018/06152018.pdf, page 8.

[17] https://www.nj.gov/oag/ge/docs/Petitions/2018/04302018.pdf, page 4.

[18] https://floridianpress.com/2019/04/online-gaming-company-could-have-business-ties-to-iran/

[19] https://www.vegasslotsonline.com/news/2019/06/19/oregon-pay-27m-controversial-sports-betting-operator-sbtech/

[20] Kambi Capital Markets Day – May 20, 2019

[21] https://www.inquirer.com/business/sports-betting-bookmaker-kambi-sets-up-shop-philadelphia-sugarhouse-parx-20190708.html

[22] Ibid.

[23] Kambi Capital Markets Day, May 20, 2019. Sentieo.

[24] Kambi Capital Markets Day, May 20, 2019. Sentieo.

[25] https://www.kambi.com/sites/default/files/Documents/Annual-Report-2017/Kambi%20Group%20plc%20Annual%20Report%202018.pdf page, 19.

[26] https://www.kambi.com/sites/default/files/Documents/Annual-Report-2017/Kambi%20Group%20plc%20Annual%20Report%202018.pdf page 19

[27] “US Sports Betting: Who Could be the Winners?” Morgan Stanley Research. June 26, 2018. Page 6.

[28] https://www.americangaming.org/new/97-of-expected-10-billion-wagered-on-march-madness-to-be-bet-illegally/

[29] https://www.si.com/mlb/2018/10/11/ryan-howard-sports-betting-game-app-investments

[30] https://www.americangaming.org/new/97-of-expected-10-billion-wagered-on-march-madness-to-be-bet-illegally/

[31] https://ayo.news/2019/07/01/draftkings-about-to-fully-acquire-sbtech-for-up-to-500m/

[32] https://www.zoominfo.com/c/sbtech/348729494

[33] https://www.reuters.com/article/us-nyx-gaming-group-m-a-scientific-games/scientific-games-to-buy-nyx-gaming-in-c775-million-deal-idUSKCN1BV1Q9

[34] https://www.thelines.com/betting/revenue/

[35] Ibid.

[36] https://www.onlinepokerreport.com/32913/uk-gambling-tax-increase/

[37] https://www.playpennsylvania.com/sports-betting/revenue/

[38] https://www.playnj.com/sports-betting/revenue/

[39] Kambi Q2 2019 Earnings Call, Sentieo.

[40] Sentieo for historical financial data and RGA Investment Advisors for estimates.

[41] https://sbcnews.co.uk/partners/sbtech/2018/02/01/richard-carter-sbtech-solving-mansions-vertical-challenge/

[42] https://www.bloomberg.com/news/articles/2019-08-12/nfl-takes-first-major-gambling-step-with-sportradar-data-deal

Past performance is not necessarily indicative of future results. The views expressed above are those of RGA Investment Advisors LLC (RGA). These views are subject to change at any time based on market and other conditions, and RGA disclaims any responsibility to update such views. Past performance is no guarantee of future results. No forecasts can be guaranteed. These views may not be relied upon as investment advice. The investment process may change over time. The characteristics set forth above are intended as a general illustration of some of the criteria the team considers in selecting securities for the portfolio. Not all investments meet such criteria. In the event that a recommendation for the purchase or sale of any security is presented herein, RGA shall furnish to any person upon request a tabular presentation of: (i) The total number of shares or other units of the security held by RGA or its investment adviser representatives for its own account or for the account of officers, directors, trustees, partners or affiliates of RGA or for discretionary accounts of RGA or its investment adviser representatives, as maintained for clients. (ii) The price or price range at which the securities listed.

About The Author: Elliot Turner

Prior to joining RGA, Elliot was a Principal and Managing Director at AustinWeston Asset Management LLC, a value-driven investment management firm, where he specialized in discovering and analyzing long-term investment opportunities and strategic portfolio management. His professional asset management career began as a Proprietary Equities Trader at Chimera Securities, LLC, where he developed his own unique trading strategy, integrating both fundamental and technical analysis. Mr. Turner then joined T3 Capital Management, LLC to continue his trading career on T3’s Equities Desk and to develop the T3Live Blog. From T3, Elliot joined the Wall St. Cheat Sheet, a financial media website specializing in news and analysis on events in the investment and entrepreneurship space. As Managing Editor at the Wall St. Cheat Sheet, he authored numerous columns on investment ideas and philosophies, macroeconomic policies, and trends in technology and innovation. His works and opinions have been published on Yahoo! Finance, TheStreet.com, Marketwatch, Business Insider, and Seeking Alpha. While still at the Wall St. Cheat Sheet, Elliot rejoined Chimera Securities, LLC to manage the firm’s first long/short investment portfolio. Elliot holds the Chartered Financial Analyst (CFA) designation as well as a Juris Doctor from Brooklyn Law School. He is admitted to practice law in New York State. He also holds a Bachelor of Arts degree from Emory University where he double majored in Political Science and Philosophy.

More posts by Elliot Turner