This article is authored by MOI Global instructor Yaron Naymark, Portfolio Manager at 1 Main Capital, based in New York City.

Given my generally long-term focus when evaluating businesses and preference for investments that can compound earnings over time, I view the high level of turnover in the top five positions of the Fund to be uncharacteristic and unlikely to occur consistently. There are two reasons I prefer long-term compounders over short-term re-raters.

The first is that I view investing in long-term compounders as less risky than short term re-raters. Following the same business for a long time allows me to get more familiar with an asset than I could in situations with a shorter investment horizon. The benefit of following the same company for multi-year periods, having a history with a management team and analyzing the operating performance of a business in real time as it happens cannot be overstated.

On top of that, compounders tend to predictably grow their value at a steady pace, which leaves the Fund with a larger margin of safety with respect to the multiple I use in valuing the business.

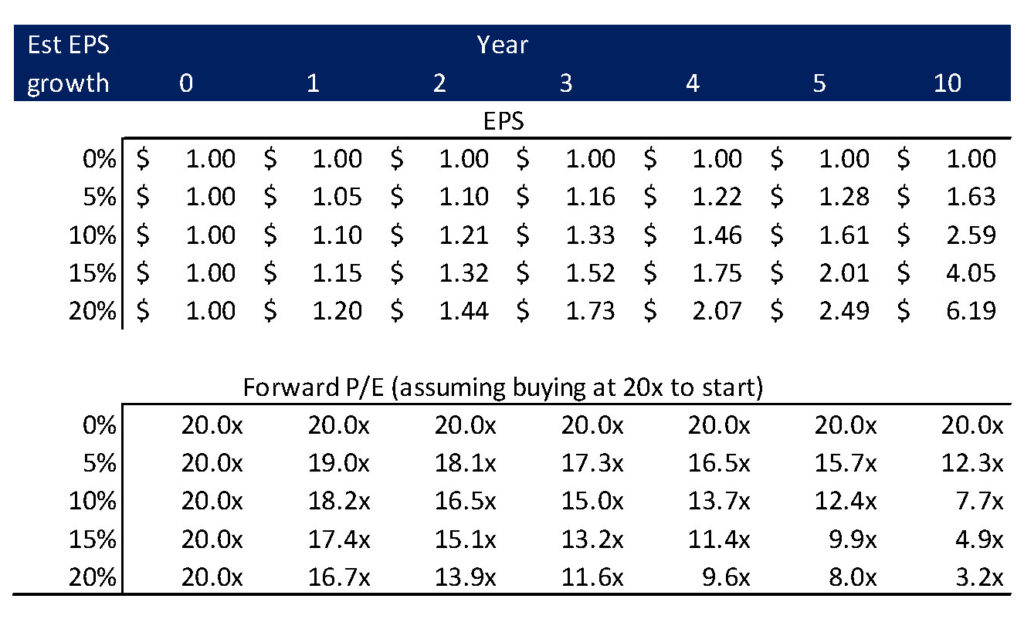

To elaborate further, when looking one year out, investor perceptions of the near-term earnings power of a business don’t tend to vary significantly, but opinions about the multiple that the business deserves do. However, when looking further out, the differences in estimates and valuation multiples become more pronounced as market participants’ varying assumptions compound.

Because of this, the shorter one’s time horizon, the more likely it is that they are betting on the multiple of earnings that a company deserves, and the less they are betting on the earnings themselves.

Using the illustrative table above as an example, if the Fund pays 20x earnings for a 20% long-term compounder in year 0, the corresponding margin of safety on my assumed exit multiple in year 10 is materially higher; we will likely be satisfied with the outcome whether the business is valued at 10x, 15x or 20x earnings given the 3.2x effective forward purchase multiple on our investment. The same can’t be said for a business with little to no growth.

As such, having confidence in the long-term earnings trajectory of a business is one of the strongest forms of edge an investor can have in the marketplace, and one of the hardest types of alpha for others to arbitrage away. Basically, if I am right about a compounder, which I define as a business that can sustainably grow its earnings at above average rates over long stretches of time, then the Fund is most likely buying the business at a very low multiple of future earnings.

The second and more obvious reason that I prefer long-term compounders over short-term re-raters is that long-term compounders are significantly more tax efficient than short term re-raters. Not only is the tax rate on long-term gains lower than on short-term gains, but the longer we hold a compounder, the longer we defer paying any tax at all and the more we can let our investment compound tax-free. As stated previously in this letter, a majority of my net worth is invested in the Fund. As your partner, my goal is to maximize our collective after-tax returns.

However, I want to make it clear that I will not hold onto a position that I no longer find attractive simply for tax deferral. It should also be clear that although I prefer compounders, I will continue to pursue special situations when I have a strong conviction and when the risk/reward appears favorable.

Important Disclosures: In general. This disclaimer applies to this document and the verbal or written comments of any person presenting it (collectively, the “Report”). The information contained in this Report is provided for informational purposes only and does not contain certain material information about 1 Main Capital Partners, L.P. (the “Fund”), including important disclosures and risk factors associated with an investment in the Fund, and no representation or warranty is made concerning the completeness or accuracy of this information. To the extent that you rely on the Report in connection with an investment decision, you do so at your own risk. Certain information contained herein was obtained from or provided by third-party sources; although such information is believed to be accurate, it has not been independently verified. The information in the Report is provided to you as of the dates indicated and 1 Main Capital Management, LLC and its affiliates (collectively, the “Manager”) do not intend to update the information after its distribution, even in the event the information becomes materially inaccurate. No offer to purchase or sell securities. This Report does not constitute an offer to sell, or the solicitation of an offer to buy, and may not be relied upon in connection with the purchase of any security, including an interest in the Fund or any other fund managed by the Manager. Any such offer would only be made by means of such fund’s formal private placement documents, the terms of which shall govern in all respects. Performance Information. Unless otherwise noted, any performance numbers used in the Report are for the Fund’s Class A Interests, and are net of any accrued incentive allocation, management fees and other applicable expenses, include the reinvestment of dividends, interest and capital gains, and assume an investment from inception of such Class. As such, the performance numbers do not reflect the performance of any particular investor’s interest and you should not rely on it as a statement of your actual return. Past performance. In all cases where historical performance is presented, please note that past performance is not a reliable indicator of future results and should not be relied upon as the basis for making an investment decision. Risk of loss. An investment in the Fund will be highly speculative, and there can be no assurance that the Fund’s investment objective will be achieved. Investors must be prepared to bear the risk of a total loss of their invested capital. Portfolio Guidelines/Construction. Information contained in this Report, especially as it pertains to portfolio characteristics, construction, profiles or investment strategies or objectives, reflects the Manager’s current thinking based on normal market conditions, and may be modified in response to the Manager’s perception of changing market conditions, opportunities or otherwise, in the Manager’s sole discretion, without further notice to you. Any target strategies, objectives or parameters are not projections or predictions and are presented solely for your information. No assurance is given that the Fund will achieve its investment strategies, objectives or parameters. Index Performance. The index comparisons are provided for informational purposes only. The S&P 500 Total Return Index (SPXT) is a capitalization weighted index that is designed to measure the performance of the broad U.S. economy through changes in the aggregate market value of 500 stocks representing all major industries. There are significant differences between the Fund and the index referenced, including, but not limited to, risk profile, liquidity, volatility and asset composition. The index reflects the reinvestment of dividends and other income, are unmanaged, and do not reflect a deduction for advisory fees. An investor may not invest directly into an index. For the foregoing and other reasons, the performance of the index may not be comparable to the Fund’s and should not be relied upon in making an investment decision with respect to the Fund. No tax, legal, accounting or investment advice. The Report is not intended to provide, and should not be relied upon for, tax, legal, accounting or investment advice. Logos, trade names, trademarks and copyrights. Certain logos, trade names, trademarks and/or copyrights (collectively, “Marks”) contained herein are included for identification and informational purposes only. Such Marks may be owned by companies or persons that are not affiliated with the Manager or any the Manager managed fund and no claim is made that any such company or person has sponsored or endorsed the use of such Marks in the Report. Confidentiality/Distribution of the Report. The information in this Report is confidential. By accepting any portion of the Report, you agree that you will treat the Report confidentially. It is intended only for the use of the person to whom it is given and the Manager expressly prohibits its redistribution without the Manager’s prior written consent. The Report is not intended for distribution to, or use by, any person or entity in any jurisdiction or country where such distribution or use is contrary to law, regulation or rule.

About The Author: Yaron Naymark

Yaron Naymark is the founder and portfolio manager of 1 Main Capital, a boutique investment firm founded in 2018 that seeks to make concentrated investments in high-quality, reasonably valued businesses with long reinvestment runways, and special situations undergoing an element of change or temporary dislocation that will cause investors to revalue an investment in the near term. Prior to founding 1 Main Capital, Yaron spent ten years analyzing businesses professionally, including at multi-billion-dollar value-oriented public and private equity firms. Yaron is a South Florida native, a lover of the outdoors, and currently lives in New York City with his fiancé and dog.

More posts by Yaron Naymark