This article is authored by MOI Global instructor Patrick Brennan, portfolio manager of Brennan Asset Management.

Investment banking and real estate are the proverbial “cool kids” compared with this ostracized loser in the minds of investors. While we sound like a broken record, we think the following discussion is warranted, given our substantial exposure to this most hated of areas. To quickly recap, Liberty LILAK trades roughly 15-20% below the levels where John Malone purchased $37 million worth of stock last summer and ~7.3x 2018E EBITDA assuming Puerto Rican EBITDA 55% below 2016 levels. Prior to LILAK’s acquisition, Cable & Wireless disposed of a large number of subscale systems far worse than existing holdings at higher multiples…and obviously Chile is worth far more. While periodic blackout announcements suggest that Puerto Rico’s electrical grid is still fragile, substantial progress has been made since the start of the year. LILAK’s commentary regarding its anticipated year-end Puerto Rican run rate was well ahead of our estimates.

Meanwhile, across the pond, press reports confirmed Liberty Global is in talks with Vodafone over certain continental assets (Germany and Central/Europe and maybe 50% of Netherlands JV), yet investors keep selling. Adjusted for its minority interests/tax assets, LGI trades at roughly 7.8x 2018E EBITDA despite the asset sale discussions (and soaring pound and euro). The valuation is more incredible, given that the company sold its smaller Austrian operations for 11x EBITDA and likely will not sell its German operations for less than 11-12x. If LGI manages to sell Germany/CEE/Netherlands and if the share price does not move, the implied “stub” would trade at 5.8-6.2x, depending on assumed multiples. This metric is relevant as LGI will not be bashful in repurchasing shares. And then there is the ever loved DISCA. DISCA’s 2048 bonds still trade at par but somehow this investment grade company trades at ~5x our 2019E free cash flow per share. Meanwhile, formerly popular Charter reported strong fourth quarter results, including adding 15,000 video subscribers, but it has somehow fallen roughly 10% since the start of the year. By purchasing shares through GLIBA (formerly LVNTA), we estimate that we are buying CHTR shares near at an implied value of roughly $245. Please keep that number in mind when we discuss free cash flow per share a couple of years out.

Clearly, a new generation of video consumers watches far less linear television (i.e., a television set) and instead chooses to watch online video, Netflix, YouTube and other programming outside the traditional video cable package. It is also true that above-inflation increases for programming have driven video packages above the threshold of what certain users can afford or are willing to pay. While there is considerable debate on the speed with which these trends progress, there is little doubt they will accelerate over time and put additional pressure on the traditional cable video business. We do not dispute this fact set.

Instead, we simply dispute the degree of exposure to these risks. As discussed in past letters, video costs are vastly different outside the United States. Netflix’s positioning, while formidable, is not nearly as dominant as it is in the United States. Both LGI and LILAK can also drive growth through their broadband offering. Of the owned names, DISCA is the only content company and clearly the name most exposed to the cord cutting risks, but it has several offsets (library/synergies/international exposure, etc.) that we discussed in detail last quarter. We would also note that the tax reform provided a bigger benefit than many realize.

5G vs. Wireless Subscriber Gains: Which Sounds More Threatening?

The recent weakness in CHTR’s stock has been surprising to us. While cord cutting concerns are still present, many investors have previously been willing to accept that CHTR’s vastly higher-margin broadband growth story offers a substantial hedge in case video losses come faster than anticipated. We suspect that the more recent concerns generally center around threats to its broadband business from mobile broadband (5G1) and from some concerns about valuation levels, as CHTR is not as statistically cheap by cable investors’ preferred enterprise value/EBITDA metric.

In our 2017 Q1 letter, we discussed the multiple uncertainties surrounding setting the 5G standard, let alone the cost of any large scale rollout. CHTR executives have noted that the technology works well…when there is little rain, limited tree interference and clear visibility…a back-handed way of describing a fantastic in -the-lab product but perhaps a more difficult real-world application. CHTR CEO Tom Rutledge also noted that a full blown nationwide 5G rollout involving multiple small antenna would likely be as costly as a full fiber rollout. This is quite expensive considering the large dividends that Verizon (VZ) and AT&T (T) maintain, not to mention VZ’s less favorable experience with a fiber rollout (Fios). We also previously noted that it is tougher to interpret T’s planned acquisition of Time Warner or VZ’s reported interest in bidding for CHTR, as strong acts of confidence in the two companies’ standalone ability to compete with cable. Why issue shares if a new product will soon be able to take meaningful share in a ~90% gross margin business? And if this is not enough, Chinese telecom provider Huawei, a 5G pioneer whose supposed dominance in the new technology was cited as one of the justifications for blocking Broadcom’s acquisition of Qualcomm, recently noted at an industry conference that most consumers would not see any material difference between 5G and existing LTE service. Nevertheless, we suspect that Verizon’s rollout of 5G service in Sacramento later this year (quite a convenient location for us!) likely planted some doubt into certain cable investors’ minds. This may prove to be ironic, as it is conceivable that the required fiber backhaul needed for 5G services ends up being a substantial opportunity for the very cable names that the service is supposed to displace. And what if we are completely wrong and Verizon can successfully hit its 30 million home rollout target by 2022? Well, a recent report from Morgan Stanley suggested that roughly 0.5 million subscribers (representing 1% of CHTR’s cable EBITDA) would be threatened…in over 4 years.

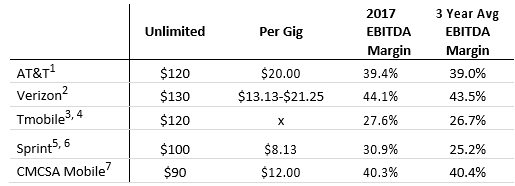

Interestingly, the fear over 5G has likely diverted investor attention away from the substantial competition coming in the wireless space as CMCSA (currently) and CHTR (later this year) execute mobile virtual network operator (MVNO) agreements with Verizon to essentially rent their network and offer mobile services to subscribers.2 As we have previously noted, the mobile offering can substantially reduce churn and thus can be priced more aggressively versus a company trying to maintain 40%+ margins in order to protect its sacrosanct dividend. While one can read about pricing in analyst reports and stare at Excel models, we find it helpful to experiment with the underlying product. We recently became Comcast mobile subscribers after spending several hours on the phone with the company and its various competitors. We show the cost of unlimited versus shared plans for two people in the chart below:

All plans are pre-tax unless otherwise noted and are quoted for 2 lines and assume auto pay; per GB based upon data offering available (i.e., some offer 4GB, others 5G, others 8G).

1 Per GB=$100 for 5G

2 Per GB=$85 for 4G or $105 for 8G

3 Receive $10.99 Netflix subscription per month taking unlimited down to $109 – taxes are included. Including the value of each, the price would be approximately $100

4 Tmobile would not initially sell per gig; when we asked on CMCSA pricing, they offered us two lines for $100 at 2G per line or $25 per G

5 The “unlimited” plan covers 23G of data

6 Per GB=$65 for 4G; If a customer goes beyond 4G, he/she can purchase 1G for $15. Sprint fiscal year ends 03/31

7 CMCSA margins are for its cable business

As one might imagine, there are hurdles3 for the initial rollout, and CMCSA does not have its “A” marketing game together currently. There are separate bills for mobile versus cable, and CMCSA representatives were often less knowledgeable about their own product and even sent us to Xfinity stores that couldn’t handle mobile. That said, CMCSA’s offering is 31% cheaper than Verizon’s price on an unlimited basis and 9-44% on a per GB basis with the CMCSA plan having more flexibility to swap offerings. Again, CMCSA is using Verizon’s network for its service, so the two products are identical4. These marketing kinks strike us as far easier to work out versus a time consuming 5G rollout, especially when there are still concerns about whether the technology actually works. It is true that wholesale revenue will offset some of these customer losses, but not every carrier will have this revenue stream. If mobile prices decline industry-wide, it seems reasonable to believe that valuations will follow. If the cable companies can build any scale in mobile, perhaps they will have an opportunity to eventually snag wireless assets on the cheap. In Europe, LGI has achieved enormous savings in the markets (Belgium and Netherlands) where it replaces MVNO wholesale arrangements with an owned network.

The mobile companies are certainly not blind and will discount to protect their core business. VZ will offer content with its mobile product, while T will meaningfully discount DirectTV or HBO (the latter, assuming the TWX deal goes through). Both companies will lay some fiber and package their products in overlapping areas, but both need to keep substantial powder in order to continue funding the large dividends. Additionally, unlike Europe, US cell phone companies do not have nationwide fixed networks and generally have less densely populated coverage areas. If consumers are primarily interested in receiving higher-speed broadband offerings, it could prove challenging to attract and maintain customers no matter how much one discounts the copper. As just one example (often repeated across the country), we currently have download speeds of over 400 Mbps with our standard triple-play CMCSA package versus a comparable offering of 30 Mbps through AT&T. The offerings are simply incomparable, and therefore it makes a switch challenging, even at 50+ percent discount levels.

While it is far from clear that VZ could actually acquire CHTR (or that CHTR would have any interest in accepting…or that VZ could trump possible other bids for CHTR), it is worth considering which of the following is a worse outcome from VZ’s standpoint:

- Making a wildly overvalued bid for CHTR, but securing a differentiated product offering (and longer-term dividend coverage)?

- Facing questions from a coupon clipping shareholder base about dividend security if cable companies secure meaningful wireless market share?

We encourage readers to give some thought to the above when viewing cell phone bills.

How to Value an Unregulated Utility?

But what about valuation? CHTR currently trades at ~9.5x 2018E EBITDA, a level at the high end of historical trading ranges and above that of other cable companies. When CHTR first announced the acquisition of TWC in 2015, one could see a path towards substantial free cash flow as synergies were realized and capex declined over time. Given the owners, this cash flow stream was likely going to be used for share repurchases and therefore the per share metrics would skyrocket. Since that time, tax reform was passed, which not only lowered the underlying corporate tax rate to 21%, but also allowed the immediate expensing for tax purposes of the substantial capital investments. Or said differently, not only would the domestic cable companies pay a lower rate, but the actual amount of income subject to taxes was less because of the capex shield.

To go deeper into the weeds, say CHTR can generate something close to $18-$19 billion in EBITDA by 2020. CHTR had roughly $10.5 billion in depreciation last year, including $3-4 billion of non-deductible merger-related amortization that runs off at a declining rate. We show capex dropping to roughly $6-$ 6.5 billion by that time. This might imply that roughly 60-70% of income is shielded from taxes before applying the interest deduction, let alone the significantly lower tax rate. One caveat to this analysis is that there are differences between the tax and GAAP depreciation schedules and investors do not have access to this level of detail. But, our quick analysis suggests that the tax assets might shield the company from most cash taxes beyond the preliminary 2021 guidance. This reform has occurred while CHTR has refinanced debt at lower levels and while the stock has now declined over the past year. To be intellectually honest, we assume that CHTR would be forced to repurchase shares at substantially higher share prices to roughly match our anticipated ~20-25% IRR. After recalibrating the starting repurchase price and after adjusting for the tax law changes, we think it is possible that CHTR ultimately earns closer to $40 per share in free cash flow by 2021 versus an original assumption of $30-$33.

How should this be valued? If we assume that CHTR should never trade above 9x EBITDA, this would imply that shares would ultimately trade at 8-10% free cash flow yields (and “only” mid-teen IRRs). Does this make sense? Some investors would argue yes, citing the company’s debt levels. Others (ourselves included) would question how an unregulated utility could trade so far below the broader market (~20x) on a price/free cash flow basis. Thought of another way, we project that CHTR will grow EBITDA at least 7% on a CAGR basis over the next 4 years versus a current cash interest expense (with a weighted average tenor of over 9 years) of just 5.7%. These two numbers are interesting when thinking about Dr. Malone’s quip that “if you grow faster than your interest cost, your value is infinite.” At the very least, it is tougher to see how this capital structure is irrational. Depressingly, we must concede that while cable faces far fewer risks than content companies, if investment grade DISCA can trade at 20% free cash flow yields, then 10% levels are possible for cable companies. That said, no pep talk is required for this team to repurchase stock. Finally, investors should remember that four different parties expressed interest in acquiring CHTR.

In summary, we remain frustrated with the stock prices of some of our holdings, but we do believe value is being created and that discounts to intrinsic value will not last forever. We do not have sentimental attachments to any of the names mentioned above and we will change our opinion if the facts change. We would like to conclude the letter by thanking Larry Cunningham for letting us participate in his latest in his last project The Warren Buffett Shareholder: Stories from Inside the Berkshire Hathaway Annual Meeting. Larry is an astute financial observer and fantastic writer. We got to know him through The Creighton Value Investing Panel during Omaha’s Berkshire weekend. We’ve been fortunate to work with Larry on a couple of Liberty Media themed articles and we hope to continue our collaboration on a larger project. We believe value investing aficionados will surely enjoy the book’s collection of essays.

—-

1 5G is the term used to describe the next generation of mobile networks beyond the 4G LTE mobile networks of today.

2 On April 20, 2018, CMCSA and CHTR announced a partnership agreement to develop back-end software to support services for their Xfinity and Spectrum mobile offerings.

3 Up until the start of this year, CMCSA mobile customers would have to purchase a new phone to be eligible for a mobile offering. This policy changed earlier this year as customers could swap carriers on certain phones. For AT&T customers, old iPhones (6) worked but newer iPhones already on the T network did not, nor did Android devices. These restrictions were not a problem for VZ customers looking to swap to CMCSA mobile.

4 While our sample size is small, it is less clear that VZ representatives we spoke with were clear that CMCSA was using the VZ network for its service.

Disclaimer: BAM’s investment decision making process involves a number of different factors, not just those discussed in this document. The views expressed in this material are subject to ongoing evaluation and could change at any time. Past performance is not indicative of future results, which may vary. The value of investments and the income derived from investments can go down as well as up. It shall not be assumed that recommendations made in the future will be profitable or will equal the performance of the securities mentioned here. While BAM seeks to design a portfolio which reflects appropriate risk and return features, portfolio characteristics may deviate from those of the benchmark. Although BAM follows the same investment strategy for each advisory client with similar investment objectives and financial condition, differences in client holdings are dictated by variations in clients’ investment guidelines and risk tolerances. BAM may continue to hold a certain security in one client account while selling it for another client account when client guidelines or risk tolerances mandate a sale for a particular client. In some cases, consistent with client objectives and risk, BAM may purchase a security for one client while selling it for another. Consistent with specific client objectives and risk tolerance, clients’ trades may be executed at different times and at different prices. Each of these factors influences the overall performance of the investment strategies followed by the Firm. Nothing herein should be construed as a solicitation or offer, or recommendation to buy or sell any security, or as an offer to provide advisory services in any jurisdiction in which such solicitation or offer would be unlawful under the securities laws of such jurisdiction. The material provided herein is for informational purposes only. Before engaging BAM, prospective clients are strongly urged to perform additional due diligence, to ask additional questions of BAM as they deem appropriate, and to discuss any prospective investment with their legal and tax advisers.

About The Author: Patrick Brennan

Patrick Brennan is the founder and portfolio manager of Brennan Asset Management, a Registered Investment Advisory firm based in Napa, CA, which utilizes a concentrated value investing strategy. Patrick has given presentations at multiple value investing conferences, including presentations to The New York Society of Security Analysts (NYSSA), The Nebraska Society of Securities Analysts and presentations on various names at the VALUEx Vail Conferences. Patrick coauthored an article on tracking stocks with Lawrence Cunningham for The Financial History Magazine and Patrick was featured in a write-up of Liberty LILAK in The Private Investment Brief. Prior to founding Brennan Asset Management, Patrick managed portfolios and led research efforts at two value investing firms in California: Hutchinson Capital Management and RBO & Co. Previously, Patrick worked at Mark Boyar & Company, where he led the firm’s research team and helped manage $800 million of assets across individual portfolios, institutional accounts and a mutual fund. Patrick also worked for six years in investment banking and equity research with Deutsche Bank, CIBC World Markets and William Blair & Company. Patrick graduated summa cum laude from the University of Notre Dame with a degree in economics and was inducted into Phi Beta Kappa. Patrick received the Chartered Financial Analyst (CFA) designation in 2002 and is a member of the CFA Institute (formerly AIMR). Patrick is originally from Omaha, Nebraska.

More posts by Patrick Brennan