This article is authored by Sebastián Miralles, Managing Partner at Tempest Capital, based in Mexico City, Mexico.

“Arise! ye spirits of the storm” –The Tempest, Thomas Linley[1]

In our 2018 year-end letter we delved passingly on the absurdly high levels at which developed market buyout transactions were occurring. Since we were of course talking out book, a great many of our investors and colleagues expressed surprise and disbelief. We decided to take some time this Summer to take up the issue in further detail. Given the skepticism regarding Latin America and its perceived political risks, we thought it is critical to show our investors the implicit trade-off whereby they are forgoing LATAM risk in favor of the perceived lower risk associated with Developed Market Buyout and similar levered strategies.

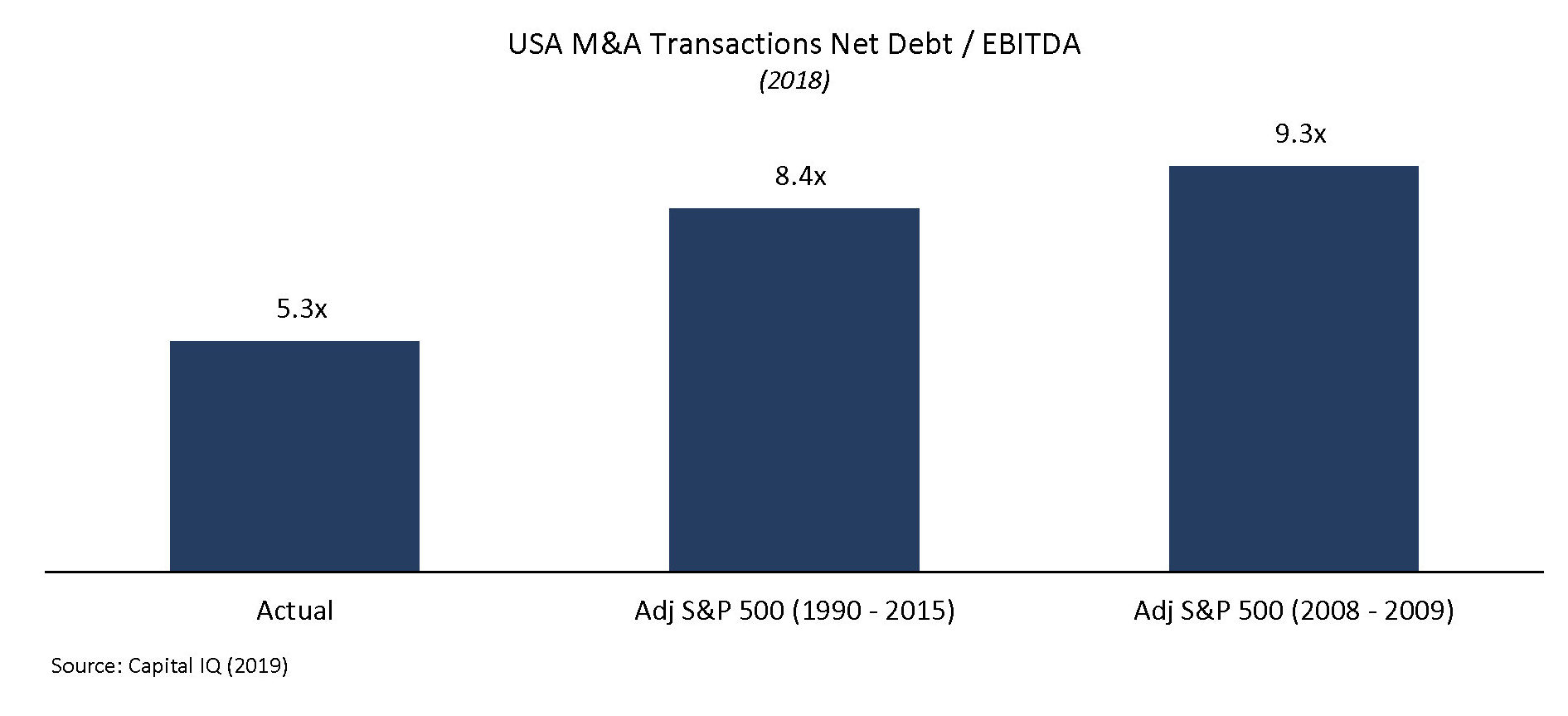

The numbers are not encouraging. US M&A transactions are occurring at an average of 5.3x net debt to EBITDA. This number by itself should give allocators pause, however this is not the whole story. Current EBITDA margins are at historically high levels. If we normalize EBITDA margins to the 1990-2015 average margins, this same ratio goes up to a whopping 8.4x.

But just like a trite infomercial, that is not all folks! It can and will likely get worse. If we assume a recessionary environment akin to the 2008-2009 Great Recession, then EBITDA margins contract further to gift us 9.3x net debt / EBITDA. A truly frightening prospect given we are entering the first stages of a recession (Tempest “victory lap”: you may recall we predicted a US recession beginning in 2019 H2 back in our 2017 year-end letter).

We would need to write a paper on its own to delve into the specific opportunities and risks intrinsic to each country in Latin America (we hold it is a grave mistake to think of it as one single region). However, we could simplify our argument by stating our belief that that local government and country specific risks can be mitigated through diligent target company selection.

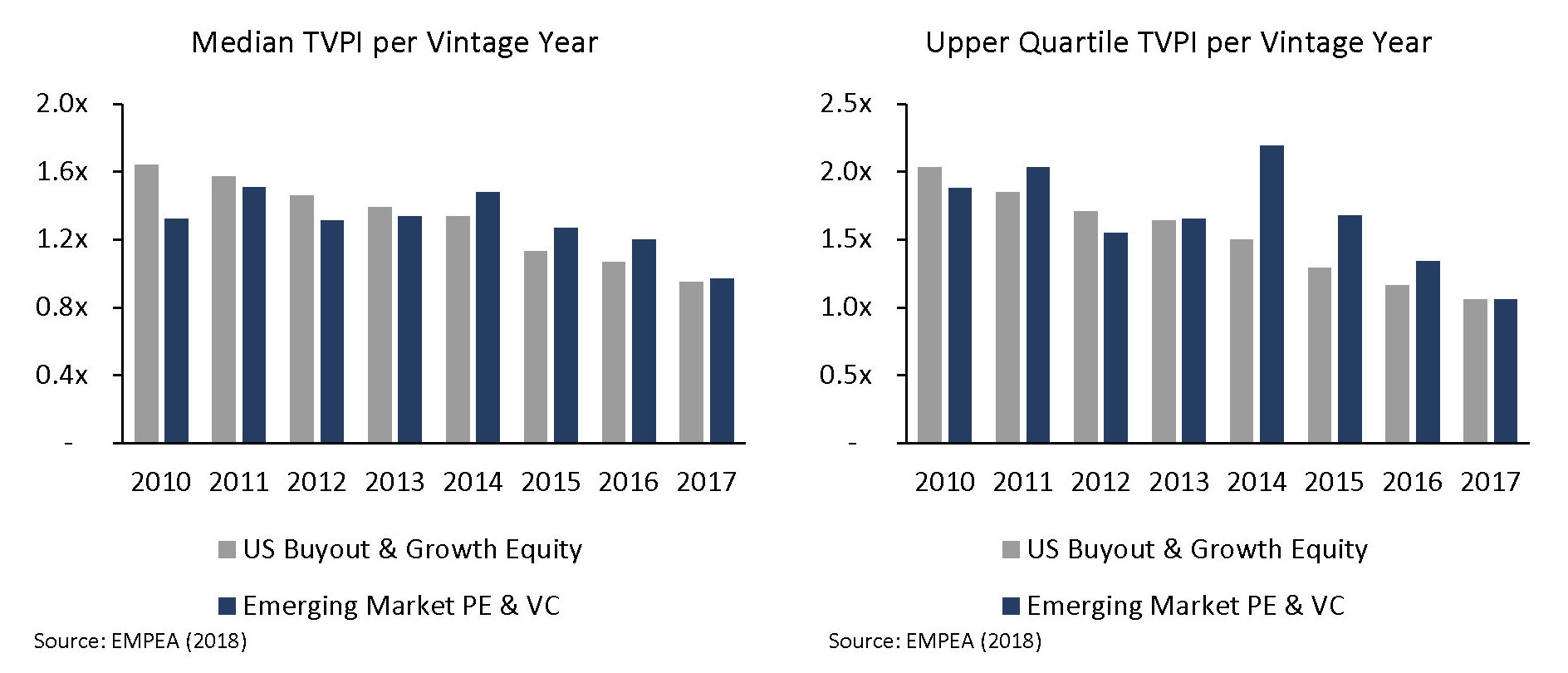

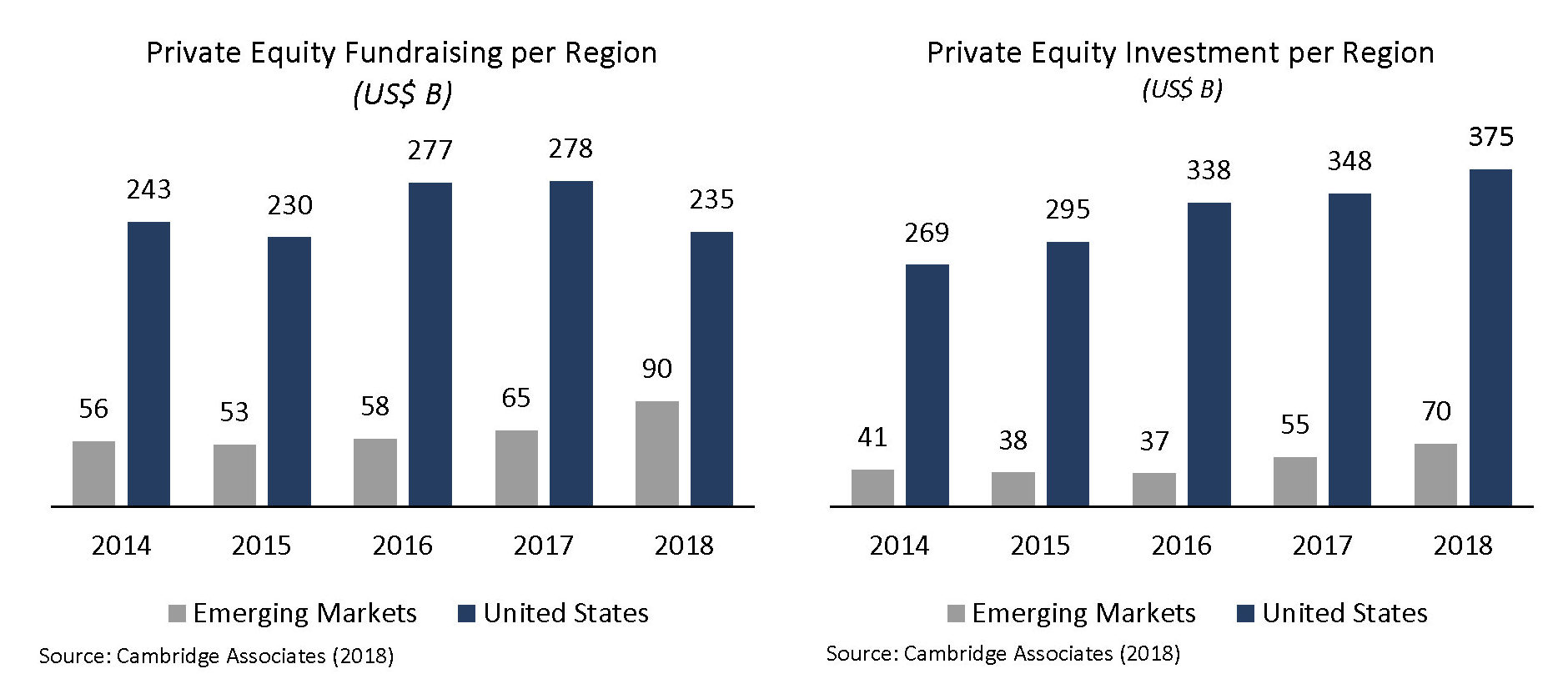

Emerging Markets Have Outperformed the US with Less Allocated Capital

Since 2014, emerging markets have consistently outperformed the US centric PE strategies. Though small, bear in mind that this outperformance has been occurring with only a fraction of the leverage available to US buyout strategies.

Despite this outperformance, in the past five years, investors have allocated 3.9x more capital to the US private equity than to the entirety of emerging markets. When viewed as investments, the situation is even more glaring with 6.7x more capital deployed than that deployed in the emerging markets.

Clearly, investors are significantly overweight United States and developed markets. Investors appear unaware they are trading off political risk for financial risk.

Hidden Financial Risk in the US Allocations

USA buyout has performed well in the past years and attracted increasing amounts of dry powder. To keep up with return expectations, it seems managers have resorted to ever increasing leverage, and subscription lines. The level of risk hidden in these portfolios, may be significantly higher than is apparent at first sight.

In 2018, M&A transactions crossed at an average net debt-to-EBITDA of 5.3x. However, we must remember that margins are at historically high levels. If we assume mean reversion to average historical levels, adjusted net debt-to-EBITDA shifts to 8.4x. This is a nose-bleed level of leverage that would keep up at night a great many portfolio manager.

However, the situation could be worse; much worse. A great many investment professionals would agree that we are currently heading into a recession. If we adjust current EBITDA margins to the average EBITDA margin of the Great Recession, we arrive at a net debt-to-EBITDA ratio of 9.3x.

Conclusion

The high liquidity environment in developed markets buyout is clearly encouraging managers to add increasingly more aggressive levels of leverage. This game of debt musical chairs can only continue for so long as the economy continues to expand. As we approach the end of this business cycle, the strategy´s sustainability should be questioned. The entire strategy could be sitting on a powder keg of insolvencies and a contraction of exit multiples.

Allocators are either blissfully unaware of these underlying risks, or they are placing an even larger premium on emerging market political risk. The latter seems unwarranted. Political risk is not entirely unpredictable, and its impact on industries can often be priced into transactions.

Furthermore, political risk is no longer exclusive to developing markets. Populism and political risk have become rampant throughout developed and developing economies with the only difference that in LATAM, investors are being paid to bear it.

Members, log in below to access the restricted content.

Not a member?

Thank you for your interest. Please note that MOI Global is closed to new members at this time. If you would like to join the waiting list, complete the following form:

Legal disclaimer: This research note is for information purposes and should not be construed under any circumstances as a public offering of securities in any jurisdiction. Tempest does not guarantee the accuracy or completeness of information which is contained in this document and which is stated to have been obtained from or is based upon proprietary best estimates, trade and statistical services or other third-party sources. Any data on past performance, modelling or back testing contained herein is no indication as to future performance. Certain statements in the research note are forward-looking. These forward-looking statements are based on certain assumptions and reflect Tempest current expectations. As a result, forward-looking statements are subject to a number of risks and uncertainties that could cause actual results or events to differ materially from current expectations. There is no assurance that any forward-looking statements will materialize. You are cautioned not to place undue reliance on forward-looking statements, which reflect expectations only as of this date. Except as may be required by applicable law, we disclaim any intention or obligation to update or revise any forward-looking statements. This Research Note contains confidential information and is intended for the exclusive use of the Recipient. You may not be copy, fax, disclose, forward or distribute to third parties in its full or partial form without prior written authorization of Tempest Capital S.C. Reception and acceptance of the document should be considered as acceptance of the confidentiality of the document.

About The Author: Sebastian Miralles

Sebastián is the Founder and Managing Partner of Tempest Capital. Throughout his career he has participated in 54 transaction totaling almost US$4.0 billion. He previously was the Managing Director of the Venture Capital and Mezzanine Division of Fondo de Fondos, leading investments in LP interest, direct equity and mezzanine deals. Sebastián also played a transformative role as the Principal coordinating the Private Equity team of CAF Development Bank of Latin America. Prior to CAF, Sebastián worked with the Global Value Equity team of Morgan Stanley and as a senior consultant in the Financial Services Group of Kroll. He earned an MBA from IESE Business School and was valedictorian in his undergraduate class in international business at Universidad Panamericana. Sebastián holds both the CFA and the CAIA designations. He is a founding member of the CFA Society of Mexico, Board Member of Jada the Fund of Funds of Saudi Arabia - a PIF portfolio company, Investment Committee Member of the Saudi Jordanian Investment Fund, and a member of Mexican Council on Foreign Relations.

More posts by Sebastian Miralles