This article is authored by MOI Global instructor Stuart Mitchell, investment manager at S. W. Mitchell Capital, based in London.

Stuart is an instructor at European Investing Summit 2022, to be held fully online from October 11-13. Members enjoy complimentary and exclusive access.

“Old economy” earnings continue to impress. Whilst just over a half of all companies surprised in the second quarter, a whopping 100% of energy, 69% of materials and 68% of financial companies beat expectations. And… those sectors make up 40% of our fund today. If we include our shipping investments, “old-economy-beaters” make up just under half of the portfolio.

Our highest second-quarter-earnings-beaters were as follows:

The Great Technology Bubble has resulted in the squandering of trillions of dollars of capital in the quest to find the next Amazon or Google. So great has been this squandering of capital that we are now in the situation where many older economy industries such as oil & gas and shipping have been so starved of capital that their supply-demand dynamics are now tighter than anything that we have seen for decades. Indeed, many hitherto well supported companies have been so shunned by investors that they have invested significantly below depreciation rates for well over a decade.

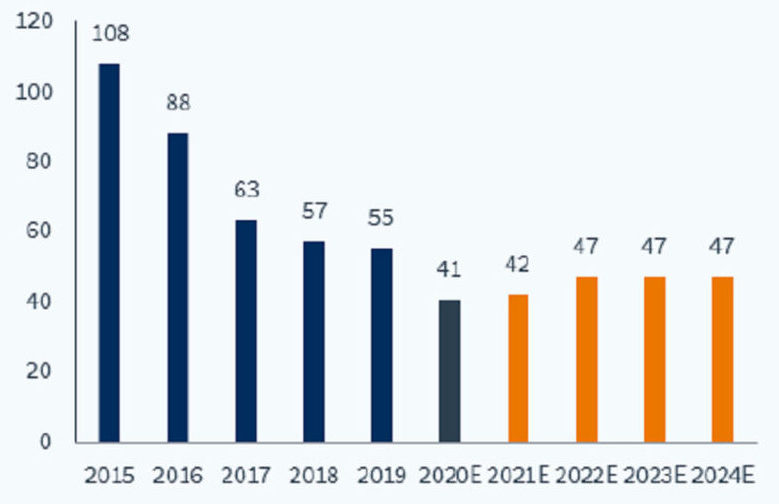

European Big Oil’s capex to remain slightly below $50 billion by 2024E

Sources: Kepler Cheuvreux, S. W. Mitchell Capital.

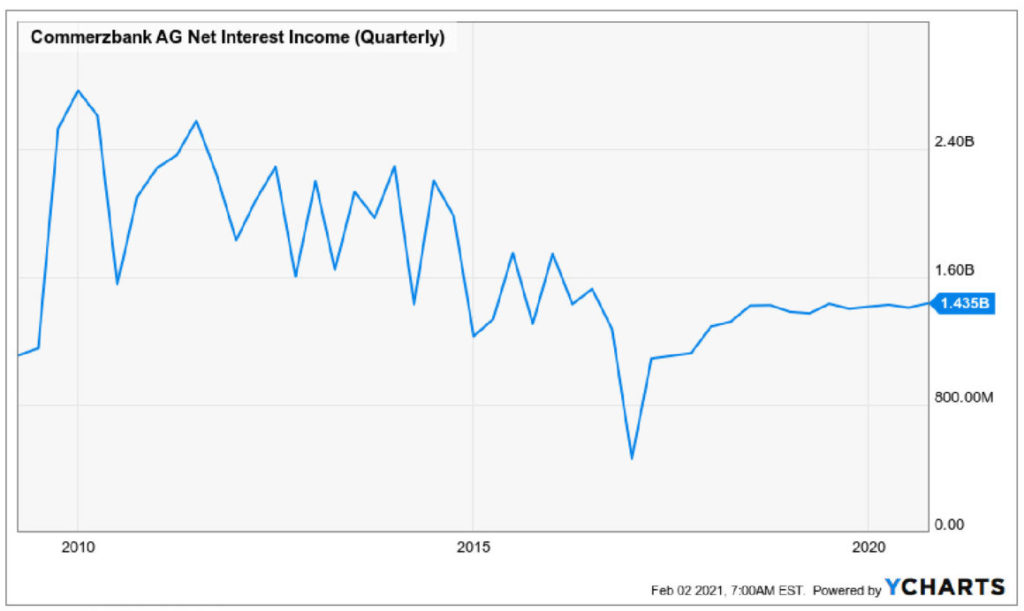

But perhaps the sector most detested by investors is the banks. The Global Financial Crisis led to significant write-downs of mortgage backed securities, and many were forced to seek aid from their governments.

Source: S. W. Mitchell Capital.

But at the same time as banks were struggling to meet minimum capital requirements, the industry was then forced to double Tier 1 equity capital to over 13%… And all this happened at a time when interest rates were falling, squeezing net interest margins significantly.

But this is changing. The industry is now benefiting from higher interest rates. As you know, European banks’ funding costs are largely fixed; extra income generated from rising interest rates passes directly to the bottom line. The impact is most dramatic for the German banks: in the case of Commerzbank, a 1% rise in rates will lead to a doubling in net interest revenues.

In addition, banks have also worked hard since the Global Financial Crisis to cut costs through branch closures and digitalisation. And crucially, banks’ balance sheets are now much stronger whilst bad debts have come down significantly and lending standards have been greatly tightened. We have written previously in some detail about this in the recent past. Our thoughts can be found here.

And yet, investors remain reluctant to invest in the old economy. Most investors remain wedded to technology and “growth-at-any-price”. As interest rates fell, many investment managers rushed to brand themselves as growth managers, unaware that they were feeding the bubble further. But the bubble has now finally burst…

At first it was the impact of higher interest rates on the valuation of these fantastically rated companies. But now earnings expectations are also beginning to drop. The result of the wanton throwing of vast quantities of capital at a number of new industries such as food delivery has led to “unexpectedly” fierce competition. This has already resulted in many 70%+ share price falls. But this is just the beginning. In areas like semiconductors the recent doubling in capex spend by the industry could lead to a return to losses for many; most investors find this hard to imagine…

So hard that old economy companies continue to trade at extraordinarily compelling valuations.

| 2022 | |||

| PER (X) | FCF yield (%) | Yield (%) | |

| Oil, metal and shipping | 4 | 24.2 | 15.5 |

| European IT sector | 25 | 1.8 | 1.8 |

| Valuation premium/discount (%) | -84 | -92 | -88 |

Source: S. W. Mitchell Capital, Kepler.

* * *

Finally, I urge you all to read Piers’s new thought piece, The future is on our plate, a thought-provoking examination of the future of how the world produces and consumes its food, and how this will change, with surprisingly drastic investment impacts.

And we will be publishing a further two thought pieces in the autumn. Lukas will be writing on the various fuel options for the next generation of ships, and I will be writing on the level of copper prices needed to generate new investment in the industry.

Members, log in below to access the restricted content.

Not a member?

Thank you for your interest. Please note that MOI Global is closed to new members at this time. If you would like to join the waiting list, complete the following form:

About The Author: Stuart Mitchell

Stuart is the Managing Partner and CIO of S. W. Mitchell Capital and the Investment Manager of two funds, as well as a number of managed accounts. Prior to founding SWMC in 2005 Stuart was a Principal, Director and Head of Specialist Equities at JO Hambro Investment Management (JOHIM, now Waverton Investment Management). At JOHIM he set up and managed the Charlemagne Fund, a long/short European fund, and the JOHIM European Fund, a long only European fund. The JOHIM European Fund was number 1 rated by Micropal within its sector and three star ranked by S&P.

More posts by Stuart Mitchell