This post by Robert Leitz has been excerpted from a letter of iolite Partners.

Jumbo is the leading digital retailer of lottery tickets in Australia. The company is licensed to sell lottery tickets online and through mobile apps. In essence, it’s a digital version of the traditional kiosk and the main source of income is ticketing fees (Australian lottery tickets do not include retailer sales commission; purchases are not to the whole dollar). Jumbo runs its own IT infrastructure.

Market

Lotteries are a major source of government income and help fund a diverse mix of community projects. In Australia, the government-licensed monopolistic national lottery operator is Tatts. Tatts’ annual overall sales are AUD 2.9 billion, about 50% of which goes to the government. Jumbo’s current (and growing) share of Tatts’ AUD 2.1 billion lottery revenue is about 7%, with a total transaction volume of around AUD

160 million. About 14% of Tatts’ lottery sales are digital, which has continued to grow market share. Tatts is in the process of merging with Australian gaming company Tabcorp (ASX:TAH).

Competition

Jumbo has two meaningful domestic competitors: (1) Tatts: the incumbent player, it operates its own online kiosk with limited success and recently took a stake in Jumbo, and (2) Lottoland: a disruptive synthetic lottery business with an official Australian license to offer bets on lottery outcomes worldwide. Lottoland is taking away market share from Tatts as well as from all retailers of lottery tickets such as Jumbo.

Moat

Jumbo’s website and app have become the go-to point for people looking to buy lottery tickets online, and its customers are sticky (brand awareness, subscription models, etc.). The business benefits from significant scaling benefits, as there are no meaningful variable costs beyond marketing/customer acquisition expenditure. Jumbo’s competitive position is further protected by significant up-front licensing, technology and marketing investments required to replicate the business. Given the platform-type business model, Jumbo’s competitive strength and value grows exponentially with every new subscriber added.

Jumbo’s customer database is of material strategic value to any more vertically integrated player such as Tatts or Lottoland, as lottery operators run at much higher margins. While Jumbo’s EBITDA margin is about 10% of transaction volume, Lottoland should easily be able to operate Jumbo’s database at margins of 25% or more. A publicly listed competitor of Lottoland, Zeal Network (formerly: Tipp24), is operating at an EBITDA margin of close to 40%.

Growth

Jumbo’s sales have been growing at about 10-20% p.a., driven by (1) real and nominal growth of the Australian lottery market (good pass-through of inflation) and (2) the growing relative share of electronic ticketing. Note: the frequency of large jackpots causes some short-term volatility and the twelve months up to June 2017 saw an unusually weak run of jackpots.

Over the last few years, Jumbo’s reported profitability was severely depressed as the company kept investing all the cash it generated in its core market (Australia) into new geographies (Germany, USA, Mexico). Unfortunately, all these international expansion projects have failed. The founder & CEO, who owns an 18% stake, has now pulled the plug on his ambitious expansion plans and is winding down all international projects. Over the next couple of years, Jumbo will likely see a sharp improvement in earnings, as it is shutting down the lossmaking international expansion projects while continuing to grow market share at marginal extra cost in its Australian home market.

Recent Events

- On April 24, Lottoland disclosed the acquisition of 3.1 million shares (7%) at AUD 2.42 per share.

- On May 12, Jumbo issued 6.6 million shares (15%) and another 3.5 million share options (subject to shareholder approval) to Tatts at a significant discount to the market price that day (AUD 2.37 vs 2.75). In return, and in addition to the cash raised, Jumbo renewed all reseller agreements with Tatts for five years and gained access to a new product (“Set for Life Game”).

- On May 31, Jumbo increased its dividend payout ratio to 85% of NPAT.

- On June 30, Lottoland sold its entire stake at AUD 2.55 per share, apparently to institutional investors.

Valuation / Outlook

While I am frustrated that management decided to side with Tatts very early in an emerging takeover battle, and that management issued shares at a material discount to both market price and intrinsic value, I am happy to keep holding my shares at their current price.

At AUD 2.65/share (fully diluted market cap of AUD 105 million, net of unrestricted cash), the company is trading at a forward P/E ratio of 7.1x (4.1x EV/EBITDA, 5.0x EV/EBIT) based on my forecast for the full year ending December 2018 (EBITDA 20.5 million, NPAT 11.9 million). Assuming a conservative exit P/E multiple of 15x, the upside for the equity is still 70%.

Jumbo has no debt, unrestricted cash is about AUD 30 million (almost 25% of current market capitalization), and the business is expected to see strong earnings growth going forward, due to a number of factors: normalization of jackpots, closure of failed international expansion projects, continued market share gains in Australia at marginal extra cost, and an improved product offering given the recent Tatts’ deal (expected immediate revenue uplift of about 10%). At the current share price and given the positive earnings outlook, the expected dividend yield is a very healthy 10%.

The downside is protected by the significant cash balance as well as the implied Tatts/Lottoland put. Tatts is now a co-owner, and it makes strategic sense for Tatts to help Jumbo grow as best as it can – to then fully acquire and integrate the business as soon as possible. In the unlikely event Tatts loses interest or plays difficult, a competing synthetic lottery operator such as Lottoland could fill the gap.

Risks

The recent deal with Tatts gives Jumbo a cash war chest that it doesn’t need. This raises the risk of poor capital allocation, something that has plagued the company in the past.

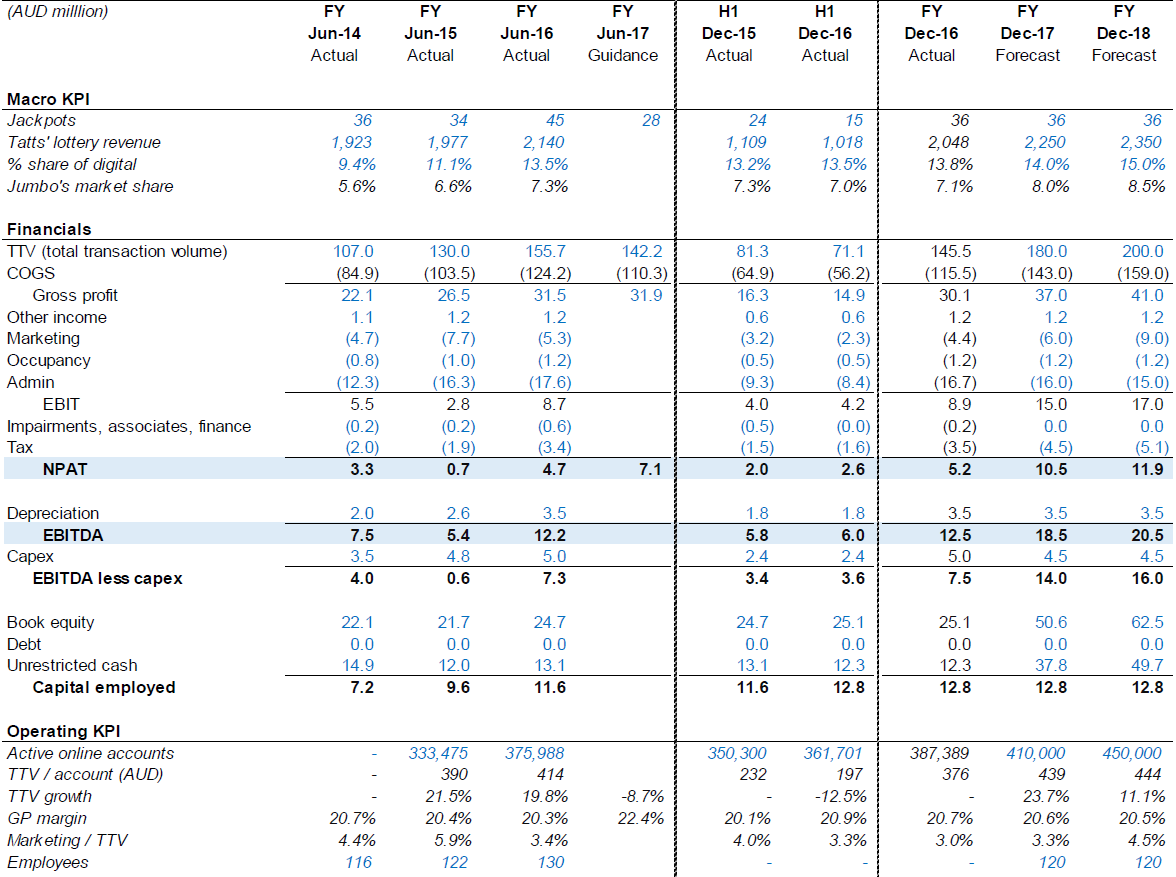

Jumbo Interactive — Financial Model

Source: Robert Leitz.

About The Author: Robert Leitz

Robert Leitz is the sole owner of and sole investment professional at iolite. Before iolite, he held positions at Glencore (the world’s largest commodity trader) and various financial institutions, including TPG Credit (a hedge fund), Goldman Sachs’ European Special Situations Group, and KPMG Corporate Restructuring. Robert graduated from the University of St. Gallen (HSG), Switzerland, with a Master of Science in Business Administration and Economics, and wrote his master’s thesis under the guidance of Prof. Eli Noam at Columbia University, New York.

More posts by Robert Leitz