This article by Jake Rosser has been excerpted from a letter of Coho Capital.

“In normal markets you can have Pepsi and Coke. In technology markets in the long run you tend to only have one…. The big companies, though, in technology tend to have 90 percent market share. So we think that generally these are winner-take-all markets. Generally, number one is going to get like 90 percent of the profits. Number two is going to get like 10 percent of the profits, and numbers three through 10 are going to get nothing.” –Venture Capitalist Marc Andreessen

The dominance of Facebook and Google is astonishing. Together, the two companies have 64% share of the digital ad market with Facebook at 33% and Google at 31%. Despite their dominance, both companies are growing their reach, with Google capturing 60% of all digital advertising growth and Facebook the remainder of 40%. All other digital online marketers and ad tech platforms are losing share. Such dominance could be reason for caution if the digital ad market were mature. However, we expect growth to remain explosive as advertising share of old media remains well above its proportion in digital media.

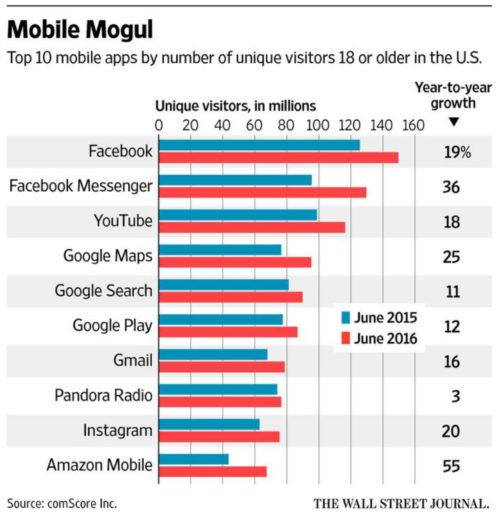

Google and Facebook’s stranglehold on the digital economy extends to apps as well with the two companies combining for eight of the top ten mobile apps.

We think both companies possess durable moats and are underpriced.

“Man is by nature a social animal.” –Aristotle

The world has never seen a company with the reach of Facebook. The company’s social network has 1.8 billion users with 1.2 billion of those users, or a sixth of humanity, using the service daily. Over a billion people use its messaging platform WhatsApp, which is the second most popular app in the world, after Facebook at number one. Facebook’s other messaging platform, Facebook Messenger, also surpassed one billion users last year. For those counting, that is three apps with over a billion users each. Facebook’s fourth platform, Instagram, may become the fourth, having grown to 600 million users last year and still experiencing rapid growth.

With incremental margins of 70% and revenue of over $3 million per employee, Facebook possesses a monopoly-like profit engine. We think Facebook is still early in its monetization opportunity with inherent operating leverage and multiple pathways to drive profits through software enhancements and enhanced data utilization.

Facebook is akin to a multi-level marketing company, yet it does not have to peddle product. There is nothing untoward about what Facebook does, but like a multi-level marketing company it leverages its users’ social networks. Instead of product, however, Facebook sells advertising and media feeds. Users freely turn over their data every time they use the site, creating a rich stream of data to mine for profits. It is no wonder Facebook enjoys such lush margins, considering the company is the world’s largest media distribution platform—and does not pay for any of its content.

Despite the company’s global reach, its monetization efforts are nascent. In a worldwide advertising market of $700 billion, Facebook has less than a 4% share. We expect to see a dramatic acceleration in advertising market share as Facebook gets more adept utilizing data. Recent market data confirm our thesis with social network ads accounting for 3.6% of Internet traffic to retailer sites over the holidays, approximately 10 times the 0.25% share they garnered last year.

Facebook is the perfect example of network effects in action. The greater the number of users on Facebook, the greater its utility for all users. Like Google, there is a virtuous aspect to its operations. The more we use Facebook, the more data we provide its software algorithms, which in turn become smarter in tailoring news and advertising toward us. This data creates a rich vein for Facebook to mine for optional services.

With many of its users engaged across its multiple platforms, Facebook becomes in effect a mobile operating system (OS), offering a menu of choices to remove friction from users’ lives. Why open separate apps, when you can order an Uber, play games, exchange photos, stream videos, and make payments all through the same software interface? China’s most popular messaging platform, WeChat, has executed on messaging as a mobile OS brilliantly. Recent updates to Facebook Messenger capabilities, along with the hiring of WeChat executives, suggests Facebook seeks to execute the WeChat playbook on a global scale.

Facebook properties dominate the mobile economy. Its scale and user base extend across geographies and nearly every conceivable demographic. We think the company is just scratching the surface on utilizing its treasure trove of data to grow profits. [The Street has focused on slowing ad loads as well as bungled advertising metrics, but this is a wonderful business.]

Alphabet (Google)

“Google has a huge new moat. In fact, I’ve probably never seen such a wide moat.” –Charlie Munger

It should be clear from our discussion of Facebook and Alibaba that technology is a platform driven world. Those with the most used platform win due to exponentially lower costs as platform users scale. This is again a core differentiation between a hardware-centric technology marketplace and a software-centric technology marketplace. While there are hardware standards, there are rarely hardware platforms. A platform requires scalability and a transaction nexus for users, something much more difficult to pull off via hardware.

Google is one of the most relied upon utilities in the world, with over three billion searches a day. According to NetMarketShare.com, Google has a 78% share of global desktop search and over 90% share in mobile search. Every search refines Google’s search results, improving search optimization. Perhaps this is why competitors have not been able to make a dent in Google’s market share. After years of effort and billions of dollars spent by Microsoft, Amazon and others, there remains no acceptable substitute for Google. Further, Google has sealed off potential breaches to its moat by establishing dominance in browsers (Chrome has over 50% share in desktop browsers) and mobile operating systems (Android has a 78% share of the mobile phone market operating system).

As with Facebook and Alibaba, Google aggregates data across its ecosystem of services to serve up more precise advertising and create additional opportunities for monetization. If data is the oil of the 21st century, then Google is John. D. Rockefeller. Apart from search, Google has six separate products with over a billion users including YouTube, Gmail, Google Maps, Google Play Store, Android and Chrome. Google’s ability to mine data across its properties, as well as to quantify results, makes it the most effective advertising channel in the world. Emarketer, a market research company, expects digital advertising to grow at a 40% annual clip over the next five years, suggesting Google can continue to grow earnings at a heady clip.

Google has been competitively entrenched for so long that the company acquired a high-class problem – it was making so much money that financial discipline was an afterthought.

Businessweek detailed the company’s efforts to instill more financial discipline under new CFO Ruth Porat in a recent cover story.

“Adwords meant advertisers only paid for ads that worked. The result revolutionized media and advertising, and gave Google a revenue stream that almost seemed limitless. Googlers have a name for its ad business: the ‘cash machine.’” –Businessweek, Budgeting Google’s Moonshot Factory

Google’s Other Bets, or non-alpha bets (there can be only one ALPHAbet and it is search) lost $3.6 billion last year. Ms. Porat has been culling speculative bets and insisting upon a realistic path to profitability, while removing redundancies. We think a bit more financial supervision was needed and should provide a nice tailwind to earnings.

As for Google’s core search business, it recently completed its 20th straight quarter of 20% growth. Put another way, Google has doubled its search business in less than a year, for five straight years!

Apart from its search business, Google has attractive future monetization opportunities in its cloud business, maps and YouTube.

Google CEO Sundar Pichai has called YouTube the “primetime of the mobile era.” He is right. The site is an advertisers’ dream reaching ten times more 18-49-year-olds during primetime than the top ten shows combined. More than a billion people watch YouTube videos each month with 80% of those users outside the U.S.

The future is mobile and YouTube is tailor-made for mobile with more than half of its video clips watched on mobile devices. It reaches more Millennials than any cable network. Generation Z, those born during 1995 or after, consume 2-4 hours of YouTube a day, compared to less than an hour of traditional television. Eight hundred twenty million people use YouTube for music streaming, seven times more than its next largest competitor, Spotify. As advertising dollars continue to shift from linear television to digital, YouTube should be a prime beneficiary.

Google’s cloud business (Google Cloud Platform or GCP) is currently a distant third to Amazon and Microsoft. Nonetheless, the company has a few arrows in its quiver to capture market share. Most importantly, technology infrastructure is not an impediment with Google controlling 30% of the world’s web traffic. The company’s global collection of data centers with homegrown servers, extensive fiber network, and world-class security ensures the company can deploy its infrastructure in an economically sensible manner despite its late start.

Google has spent two decades organizing massive amounts of data and knows better than anyone how to utilize data to unearth insights. We expect Google’s data analytics expertise will enable the company to make competitive inroads in cloud computing. As the world moves toward unlimited computing power and storage, it is hard to think of a company better positioned than Google.

Recent GCP product introductions suggest such a road map, with Google’s expertise in data analytics and machine learning being applied to language translation, image sorting and text contextualization.

About The Author: Jake Rosser

Jake Rosser is the managing partner of Coho Capital Management. He founded Coho in 2007 after working in equity research positions at the value-oriented Auxier Focus Fund and sell-side firm Pacific Crest Securities. He was also a strategy consultant at Alliance Consulting Group. Jake holds an MBA from Tuck and lives in Portland, Oregon.

More posts by Jake Rosser