This article is authored by Saurabh Madaan, member of MOI Global member and host of Investing Talks at Google.

Ben Graham has said that the stock market might be a voting machine in the short term, but is a weighing machine in the long-term. What does the weighing machine tell us about the long-term?

Over the long term, the earnings of S&P 500 have grown at ~6.7% per year since 1960, and the index has always crossed its previous peak after a recession. By my estimates, the current price of S&P 500 is 15% above trend-lines. In other words, the market is a little more than 2 years ahead of itself.

It is one thing to say that the market looks overvalued or undervalued, but whether such overvaluation (or undervaluation) will continue further before reversing itself is much harder to predict. Such fluctuations have happened before and sometimes persisted over several years. All one can infer is to be cautious.

An index-investor should continue to regularly invest, while an individual security analyst should focus on selectively sticking with undervalued businesses. It might be useful to be aware of the market’s high level data, but it is better to use it to be cautious, than to try and dance in-and-out of the market in panic.

Mr. Market – Hot or Not?

“Is the current market overvalued?” I have heard several variations of this question recently.

It is a futile exercise to try and keep step with every fluctuation of the market, so we aren’t going to do that. At the same time, the long-term behavior of the market provides some useful insights and is worth studying.

S&P 500 over the Long Term

I analyzed S&P 500 data from 1960 to 2016. This cuts across cycles of low and high interest rates, booms and busts, soft and tight markets in real estate and insurance.

Below are the salient highlights:

- On average, earnings have grown at a rate of 6.7% per year

- S&P companies also provide a ~2.5% dividend yield

- Every time the market has gone down, it has climbed back up beyond its previous peak

- An average investor would have earned 9-10% compounded returns through index investing over the long term

This data can also be triangulated with fundamentals. The US GDP has grown at ~3% unit growth + 2-3% inflation. US companies have also bought back their stock and increased productivity, culminating in the 6-7% earnings growth in total. Add the dividends and you get total growth of 9-10%, consistent with earlier results.

Market Valuations at Current Levels

In doing my analysis, I also ran a regression:

log EPS (year n) = log EPS_0 + n log (1+ r)

The values for EPS_0 and r were deduced from the model.

Two results:

- r = 6.7%, the year-on-year growth, referred above

- Average multiple of S&P companies since 1960 has been around 16x

Using this model, the trend-line EPS for S&P 500 in mid-2017 is $133. At 16x, S&P level is 2,128, and the number for September would be 2,217.

At the current levels of 2,575, the market seems 16% overvalued. However, you may not want to sell your stocks and go all into cash based on this. Below is why.

Implications

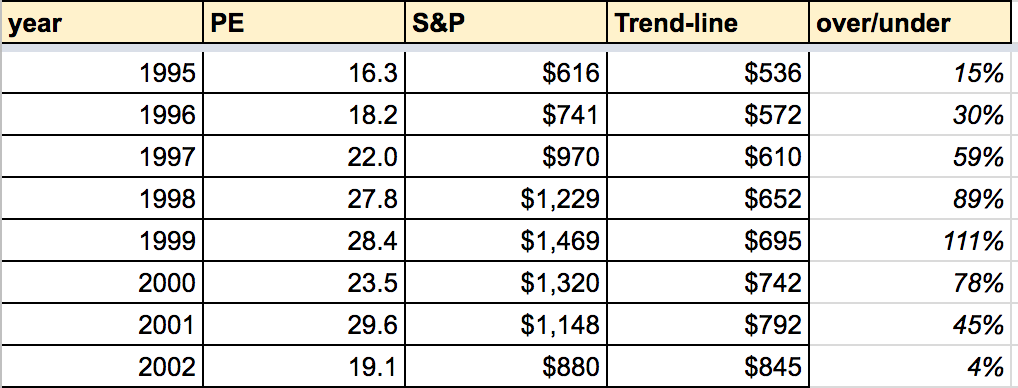

The market was similarly overvalued last time in 1995, and continued to climb higher at an even faster pace over the next 6 years, before culminating in the bursting of the Internet bubble in 2001-02.

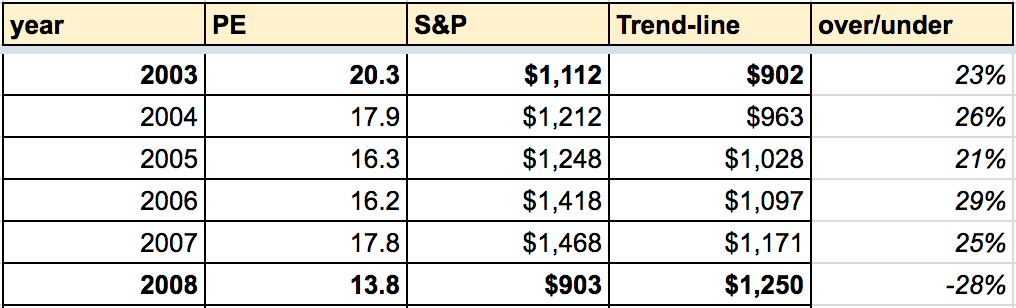

Similarly, the market began to look overvalued in 2003 and continued to rise for 4 more years before reversing back to trend-line in 2008.

Here is a two-point summary:

If you index, keep indexing at regular intervals without trying to time the market. Current valuations suggest some caution against putting a big chunk into the index at once.

If you invest in individual stocks, remember that the long-term behavior of the market is driven by underlying businesses. You are better off trying to select undervalued businesses, than match short-term fluctuations of the market. Of course, when things are egregiously overvalued, you will likely see that in the S&P valuations, as well as those of your individual holdings (which you would want to then sell).

My Personal Approach

I personally try and invest using a bottom-up approach: buy businesses that are selling below their fair value. In an overvalued market, such opportunities are rare and cash levels rise on their own. Conversely, when the market is undervalued, such opportunities abound and more capital can be put to use. As a result, the levels of cash in the portfolio are a by-product.

Nevertheless, I thought that it might be useful to have some sense of the long-term base rates, to prevent emotions from getting the better of you, resulting in panic-selling (or buying).

P.S. The above framework is inspired by Ed Wachenheim. The data used for analysis was taken from Prof. Aswath Damodaran’s website. All the faults in the analysis, inadvertent as they might be, are mine.

About The Author: Saurabh Madaan

Saurabh Madaan serves as Managing Director at Markel Corporation. He was previously a senior data scientist at Google and is a passionate value investor. While at Google, Saurabh hosted the Talks at Google series focused on investing. Access the YouTube playlist.

More posts by Saurabh Madaan