This article is authored by MOI Global instructor John Heldman, portfolio manager of Triad Investment Management. John is an instructor at Best Ideas 2018, the fully online conference featuring more than one hundred expert instructors from the MOI Global membership community.

What’s a Bitcoin? I’m not sure. It’s claimed to be a currency, just like the dollars in your wallet. Unless you’re a Millennial. They carry no cash. I know. I have two Millennials. My kids. But I digress.

A currency must pass several tests to be considered a viable currency: it must serve as a “medium of exchange” while also functioning as a “store of value” and a “unit of account.”

Think about it. If you are using pieces of paper, or digital money, you want something that will be accepted by others–the medium of exchange–and retains reasonable purchasing power over time–the store of value–while able to measure assets, liabilities, income, expenses–the so-called unit of account.

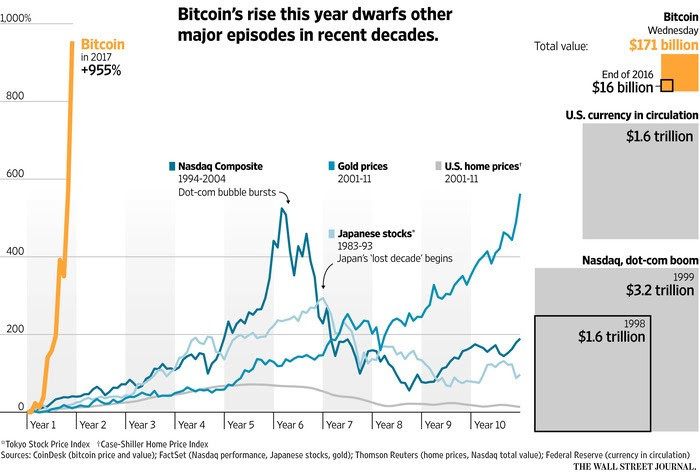

It could be argued that Bitcoin meets the definition of a medium of exchange. People use the digital currency to buy and sell stuff. But is it a store of value? The price of a Bitcoin started this year around $1,000. Today a Bitcoin can be had for about $10,000. Did the dollars in your wallet increase tenfold? Just a few days ago, Bitcoin was $11,500. Hold on, I just checked my computer. It’s now around $9,600. Is this a “store of value?” Not to me. But I’m susceptible to being an old fuddy-duddy. I guess I’m just not embracing the future fast enough.

As for being a unit of account, imagine you borrowed money in bitcoins. The price of bitcoin soars tenfold. When it’s time to pay back your bitcoin loan, you’d better have enough bitcoins to repay the loan. Otherwise, you’ll likely be paying up for more bitcoins to pay off your loan. That’s a problem.

If Bitcoins don’t fit the classical definition of a currency, then what might it be? Here’s another possibility.

Bitcoin just might be a good old-fashioned bubble, the kind that comes along after years of financial prosperity. The economy is humming along, stock markets are up, real estate prices are up, art prices are up; everything is up. Why not drop the hesitation and get on board the new thing?

How much of your net worth would you entrust to this Bitcoin thing? One hundred percent? Of course not, you say. How about 50%, or even 10%? Still too much? Why is that? Because most rational people have no idea whether Bitcoin, or any of the other “cryptocurrencies” will be around in five or ten years. Warren Buffett was recently quoted as saying “It does not meet the test of a currency. I wouldn’t be surprised if it’s not around in 10 or 20 years.”

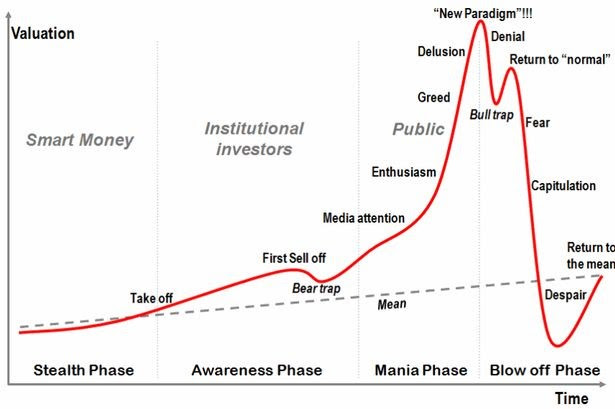

All bubbles go through stages, as shown below. First the smart money invests. Maybe not smart, just more adventurous. Invest is probably the wrong word. Speculates is better. The big institutions get on board. Finally, the public shows up, pushing prices ever higher. Awareness turns into a mania. At the top, it’s a sure thing, and everyone is convinced the “asset” is a one-way ticket to early retirement. Something for nothing.

Eventually, cracks appear. Prices slip. Selling commences. The selling starts to feed on itself. The same forces that drove prices into the sky, conspire to drive prices into the ground.

Why is this cryptocurrency phenomenon important? For those of us not involved, it’s probably not. But it’s important for the speculators who think there is an easy path to riches. And it’s another demonstration of the periodic madness of crowds. Otherwise rational people can get caught up in very irrational pursuits. The fear of missing out can be a great motivator. It can lead to financial reversals and even disaster for those who hang around the party too long.

If you do find yourself bitten by the crypto bug and the chance to make a fast buck, here’s a bit of advice. As in Las Vegas, only wager whatever amount you are willing to lose. These things usually don’t end well.

This post has been excerpted from a recent issue of The Triad Perspective.

Disclaimer: Past performance does not guarantee future results. Results are presented net of fees and include the reinvestment of all income. The opinions expressed herein are those of Triad Investment Management, LLC and are subject to change without notice. Consider the investment objectives, risks and expenses before investing. The information in this presentation should not be considered as a recommendation to buy or sell any particular security and should not be considered as investment advice of any kind. You should not assume that any securities discussed in this report are or will be profitable, or that recommendations we make in the future will be profitable or equal the performance of any securities discussed in this presentation. The report is based on data obtained from sources believed to be reliable but is not guaranteed as being accurate and does not purport to be a complete summary of the available data. Recommendations for the past twelve months are available upon request. In addition to clients, partners and employees or their family members may have a position in any securities mentioned herein. Triad Investment Management, LLC is a SEC-registered investment adviser. More information about us is included in our SEC Form ADV Part 2, which is available upon request.

About The Author: John Heldman

John Heldman brings over 30 years of experience to the management of investment portfolios. Prior to founding Triad, he was a Senior Vice President and Portfolio Manager with Neuberger Berman. John has also managed institutional and individual investment portfolios for Deutsche Bank, Scudder Investments and Bank of America, including managing equity funds and serving on the Equity Strategy Committee. He obtained his Bachelor of Science degree in Finance and Master of Business Administration from California State University, Long Beach. John is a CFA charterholder, and a member of CFA Institute and CFA Society Orange County.

More posts by John Heldman