This article is authored by MOI Global instructor Jim Roumell, president of Roumell Asset Management, based in Chevy Chase.

The following is an update to Jim’s detailed writeup on Tetra Technologies dated August 27, 2020. Please refer back to that article for deeper segment analysis. Jim also wrote an update on Tetra dated October 9, 2020.

We look forward to Jim’s presentation of Tetra Technologies at Best Ideas 2021.

Third Quarter 2020 Highlights

- TTI generated positive free cash flow for the fourth consecutive quarter.

- TTI indicated it currently has #1 water recycling market share in the Permian Basin.

- Strong uptake in Sandstorm technologies and market share gains.

- CCLP holds value, and TTI is considering “all options”.

- Reduced corporate general and administrative expenses by nearly 40% in one year.

TTI posted positive third quarter 2020 EBITDA, operating cash flow and free cash flow. The company appears, to us, to be in a league of its own posting positive results despite the brutal downturn in energy services. Every quarter this year they have generated positive free cash flow even without the benefit of monetizing working capital (receivables and inventory – meaning quarterly cash earnings continue to cover interest expense, cash taxes and all capital expenditures).

TTI Management publicly indicated its belief that the third quarter of 2020 represented the market trough and pointed to positive fourth quarter trends. TTI is well situated to gain share in multiple business segments during this downturn, while being highly leveraged to an upturn in energy services. TTI pointed to market share gains in water recycling (#1 in Permian Basin) and in sand remediation with 100% utilization of its new Sand Storm equipment. TTI signaled that it will invest to meet growing demand for its Sand Storm technology.

TTI announced that its Sand Storm sand filtration technology is in the process of displacing a competitor, after a head to head comparison, in Appalachia. We have spoken to a large, and highly reputable, Permian Basin client who is transitioning its sand recapture needs to TTI. This client expects upwards of 70% of its wells to be using TTI’s Sand Storm technology by the end of calendar 2020. TTI is gaining market share because of its technological innovation, backed-up by strong customer service.

Importantly, TTI is in the enviable position of being anchored by its non-energy industrial fluids and calcium chloride businesses. These non-energy related businesses accounted for about 36% of the completion fluids segment revenue in the third quarter of 2020. The first 9 months of 2020 is unchanged from the same period in 2019 despite a slowdown in the global economies. This business’s core ingredient, calcium chloride, is sold into multiple end markets including municipal services (TTI just won a new piece of dust control business), food, preservatives, paper bills and even beer. In fact, this is the company’s “gem,” albeit unappreciated because it is inside a deeply out-of-favor “energy” company. We believe this business provides material downside protection to a TTI investment given that we estimate it is an asset worth at least $150 million, i.e., 7.5x of our EBITDA estimated segment EBITDA of $20 million.

A recent Rystad report indicated an emerging, and meaningful, pick-up in deep water drilling. The report noted, “Considering all new production wells to be drilled for the top 10 most active deepwater drilling countries towards 2025, we see 1,570 well to be drilled, or 260 wells on average per year.” We assume roughly 10% of these wells are ultra-deep water, high compression CS Neptune candidates. Further, we assume 10% to 20% market share wins, or the potential of two to four CS Neptune wells per year. The company indicates that two or three ultra-deepwater wells adopting CS Neptune technology would be a giant win for TTI’s bottom line, albeit it does not provide margin information. TTI’s energy fluids business has #2 Gulf of Mexico market share (an estimated 35%), with growing North American Sea exposure.

Ultimately, we believe TTI’s management team will act like activists. We believe they are willing to divest assets in order to strengthen the balance sheet while focusing on its specialty chemicals and fluids business. Thus, in addition to deconsolidating CCLP, we believe the company is also willing to monetize its Water and Flowback business if the right opportunity presents itself. In our opinion, this asset, with its leading Sand Storm solution and remote monitoring technology, holds real value. In fact, we believe TTI will ultimately consider selling its non-energy industrial fluids business if that segment’s value fails to receive market appreciation.

On TTI’s investor call, we asked CEO Brady Murphy about rumors we’re hearing about non-energy industrial fluids businesses garnering 10x to 12x EBITDA multiples in the current environment. He confirmed that 1) While there are R&D synergies between the two segments, TTI’s energy and industrial fluids business are separable and 2) If the value of TTI’s industrial fluids and calcium chloride businesses are not appreciated in the marketplace in time, TTI would absolutely consider options to create shareholder value with this asset ($120 million plus in annual revenue with low 20% EBITDA margins).

Other Third Quarter 2020 Highlights for TTI

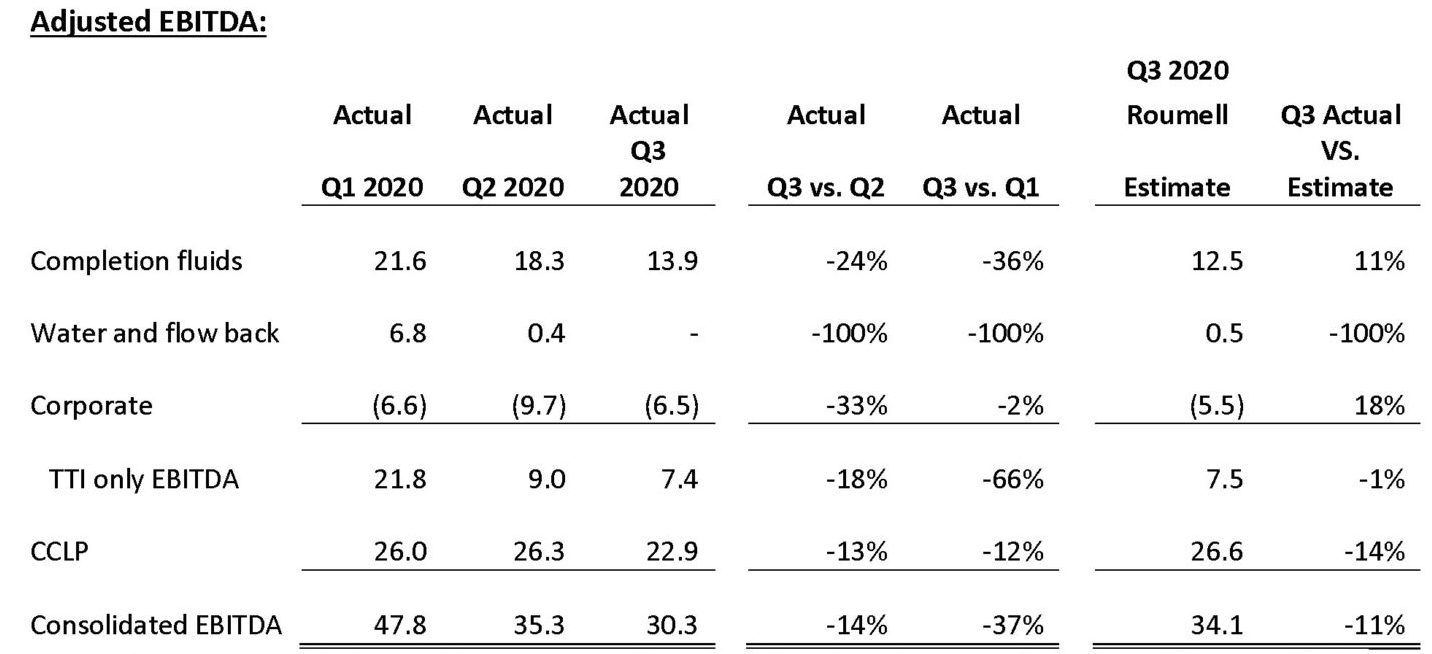

- Consolidated EBITDA (including CCLP) was $30.3 million in Q3 2020, down 14% from $35.3 million in Q2 2020. TTI-only EBITDA was $7.4 million in Q3, down 18% from $9 million in Q2. The primary reason for the decrease was a 24% drop in the Completion Fluids segment. This was expected as Q2 is the seasonally strongest quarter of the year in the Completion Fluids segment. As a comparison, TTI’s main competitor in the Water Management and Flowback Services business was $6.9 million negative. And TTI’s publicly traded peer on the offshore fluids market, Newpark, was approximately $10 million adjusted EBITDA negative. Comparing against these two publicly traded peers points towards TTI’s diverse business model with multiple revenue streams and competitive advantages allowing it to remain adjusted EBITDA positive while other have gone negative adjusted EBITDA.

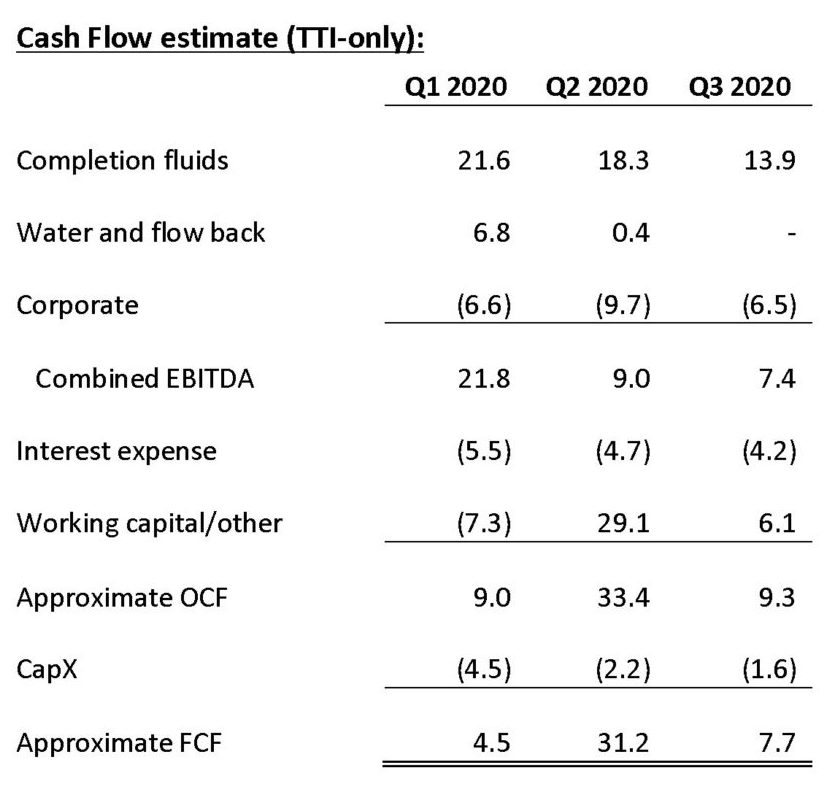

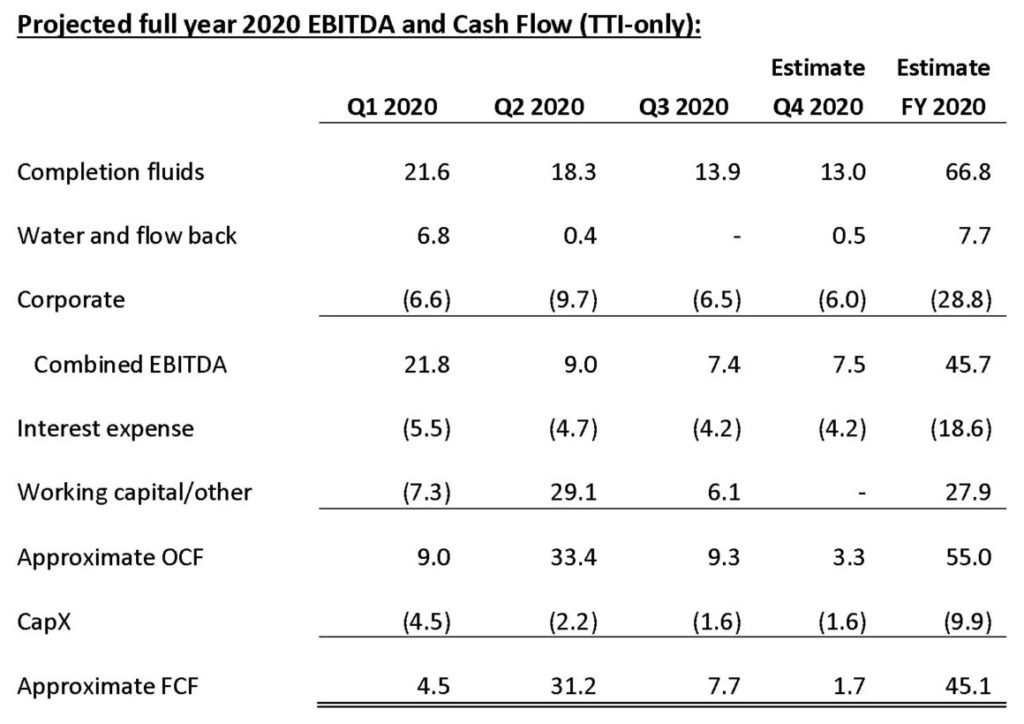

- TTI-only cash flow from operating activities was $9.3 million, while TTI-only adjusted free cash flow from continuing operations was $7.7 million. Thus, YTD, TTI has generated $51.7 million in operating cash flow and $43.4 million in free cash flow during a market turndown.

- It is encouraging that FCF has been positive during the very difficult operating conditions noted in the second and third quarters of 2020, before the benefit of working capital changes. However, it should be emphasized that working capital has contributed significantly to overall positive free cash flow. Of the $43 million of free cash flow approximately $33 million is from monetizing working capital and $10 million is from current period earnings.

- Brady Murphy, TETRA’s CEO, stated, “Third quarter activity continued to decline from the impacts of COVID-19 while hurricanes in the Gulf of Mexico added to this challenging environment”. However, he further noted on the Investor call that September and October were “much better” than July and August for the Water segment. He further noted that he believes Q3 2020 was the bottom for Water.

In our September write-up, out of an abundance of conservatism, we assigned no value to TTI’s CCLP equity ownership. We now believe it is an “option” worth valuing.

CCLP generated $26 million of EBITDA in the first quarter of 2020, $26.3 million in the second quarter of 2020 and $22.9 million in the third quarter of 2020. Additionally, CCLP recently updated its capital structure by pushing out significant debt maturities several years, reducing its liquidity risk. The company has a modest $80.7 million due in August ’22. The ’22 maturity should be relatively easy to resolve as the company will likely have $60 million plus of cash on its balance sheet at that time as a result of eliminating growth cap-ex and focusing on FCF generation. CCLP’s next maturity is not until 2025. The current depressed $105 million EBTIDA run rate (based on annualizing 2nd Q 2020), results in roughly $30 million in annual FCF.

Consolidation of CCLP’s highly-levered balance sheet with the accounts of TTI is not fully understood. A screen of TTI’s financial statements shows a highly-levered balance sheet. However, the consolidated balance sheet includes CCLP’s debt for which TTI has no responsibility with no cross defaults, no cross collateral and no cross guarantees. On a standalone basis, TTI has a much better balance sheet and two valuable business segments with no near-term debt maturities. TTI has indicated that it is supportive of actions to enhance shareholder value, including the potential to deconsolidate CCLP in the near term.

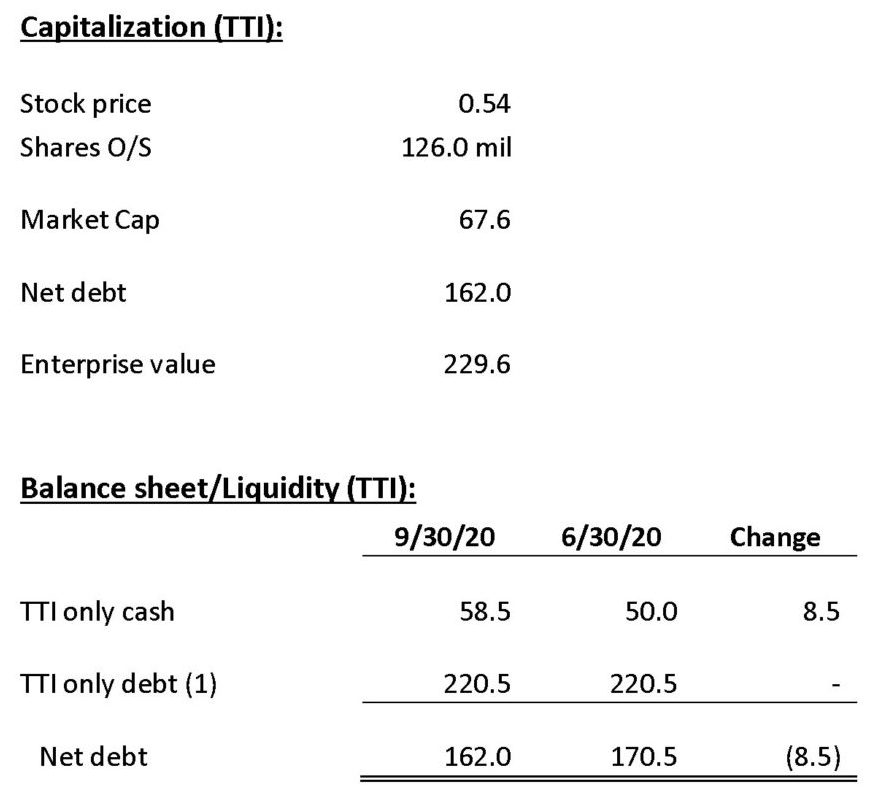

As cash builds, and CCLP’s leverage ratio declines, we believe value will be transferred from the company’s debt to its equity. 8x the current depressed EBITDA run-rate of $105 million translates into to $71.3 million for TTI shareholders ($105 mill * 8 = $840 million less $636.2 million debt = $203.8 million * TTI’s 35% ownership = $71.3 million), or roughly $0.57/share – versus today’s share price of $0.54. The above analysis ascribes no value to TTI’s 100% ownership of CCLP’s GP.

Recent M&A comparables in the compression sector have been between 8.0x to 10x EBITDA given the persistence and stickiness of these assets:

- Kodiak acquired Pegasus in Sept 2019 for a reported, but unverified, 9.0x EBITDA

- Archrock bought ELITE compression in June 2019 for an estimated 8.2x EBITDA

- EQT bought Kodiak in Feb 2019. According to Kodiak management, this was done at a 10.0x run rate EBITDA at the time of the transaction (based on Dec 2018 annualized EBITDA)

- USA Compression bought CDM from Energy Transfer in Jan 2018 for 10.0x EBITDA

- Enerflex bought Mesa Compression in mid-2017 for a reported 10.0x EBITDA

Third Quarter 2020 Highlights for CCLP

- CCLP’s Midland, Texas fabrication facility was sold in early July for $17 million in gross cash proceeds.

- CCLP believes its strategy to invest in higher horsepower equipment will allow it to maintain utilization rates above the low point of the last downturn, which was 75.2% in the third quarter of 2016. Equipment on standby improved significantly from a peak of 226,000 horsepower in May of this year (approximately 20% of the fleet) to 78,000 horsepower at the end of September 2020 (approximately 8% of the fleet) as customers started bringing production and units back online.

- As of September 30, 2020, service compressor fleet horsepower was 1,172,307 and fleet horsepower in service was 941,747 for 80.3% utilization.

- Aftermarket Services revenue declined 12% sequentially while gross margins improved 20 basis points to 14.8%. Aftermarket Services is expected to gain momentum in 2021 as deferred maintenance from 2020 is caught up.

- Equipment sales decreased from $24.3 million in the second quarter to $11.9 million in the third quarter as CCLP exits the fabrication business. Final shipments will be in Q4 of this year.

(1) Differs from the $206.3 million shown of the September 30 Balance Sheet. Note the contractual amount due is $220.5 and the balance sheet amount reflects GAAP accounting adjustments (valuation adjustments).

The decline the Completion Fluids segment reflects the fact that the second quarter of the year is the seasonal high for this segment.

Valuation

In our opinion, the simplest way to look at TTI is to back-out the sturdiest asset value from the company’s enterprise value, providing a clear picture of what an investor is paying for the company’s remaining assets. The company’s current enterprise value is $230 million.

Non-Energy Fluids Business (estimated $20 million ’20 EBITDA):

- 7.5x EBITDA $150 million

- 9x EBITDA $180 million

- 10x EBITDA $200 million

Remaining Assets:

- Energy Fluids Business (CS Neptune optionality)

- Water & Flowback Business

- CCLP Equity (analysis above, based on recent M&A transactions in the space, indicates a $71.3 million value to TTI’s 35% ownership).

An investor can “mix and match” the relative values he/she wants to use for each business segment. If we are roughly correct in our CCLP analysis, an investor is purchasing the company’s Energy Fluids and Water/Flowback businesses, which are both gaining market share, for nothing.

Summary

In short, we believe TTI provides a vehicle to own a strong, well-performing (non-energy) industrial fluids business, purchased cheaply, as a result of it being held inside a deeply out-of-favor energy services company. Additionally, the company’s energy-related services businesses are gaining market share and performing exceptionally well during a deep energy downturn. Finally, we rate management as blue-chip. Brady Murphy, CEO, spent 26 years at Haliburton, HAL, with his last position as Senior Vice President of Global Business Development and Marketing, and was a contender to become HAL’s CEO. Elijio Serano, CFO, spent 17 years at Schlumberger, SLB, and is a highly-regarded industry executive.

About The Author: Jim Roumell

Jim Roumell entered the securities industry in 1986. Before founding the firm in 1998, he was a Registered Principal at Raymond James Financial Services, Inc. Mr. Roumell is a frequent contributor to Manual of Ideas Global and has been featured in such publications as Barron’s, Kiplinger’s, Value Investor Insight, Financial Planning Magazine, and The Washington Post. He is listed and quoted in “The Art of Value Investing: How the World’s Best Investors Beat the Market.” Mr. Roumell was selected to participate in, and won, two consecutive Wall Street Journal stock picking contests in 2001 and 2002. He is a Board Member and Chairman of the Investment Committee of Wayne State University Foundation. He is also a Board Member and serves on the Investment Committee of Amalgamated Casualty Insurance Company. Mr. Roumell is a graduate of Wayne State University in Detroit, Michigan.

More posts by Jim Roumell