This article is authored by MOI Global instructor Stuart Mitchell, Investment Manager at S.W. Mitchell Capital, based in London.

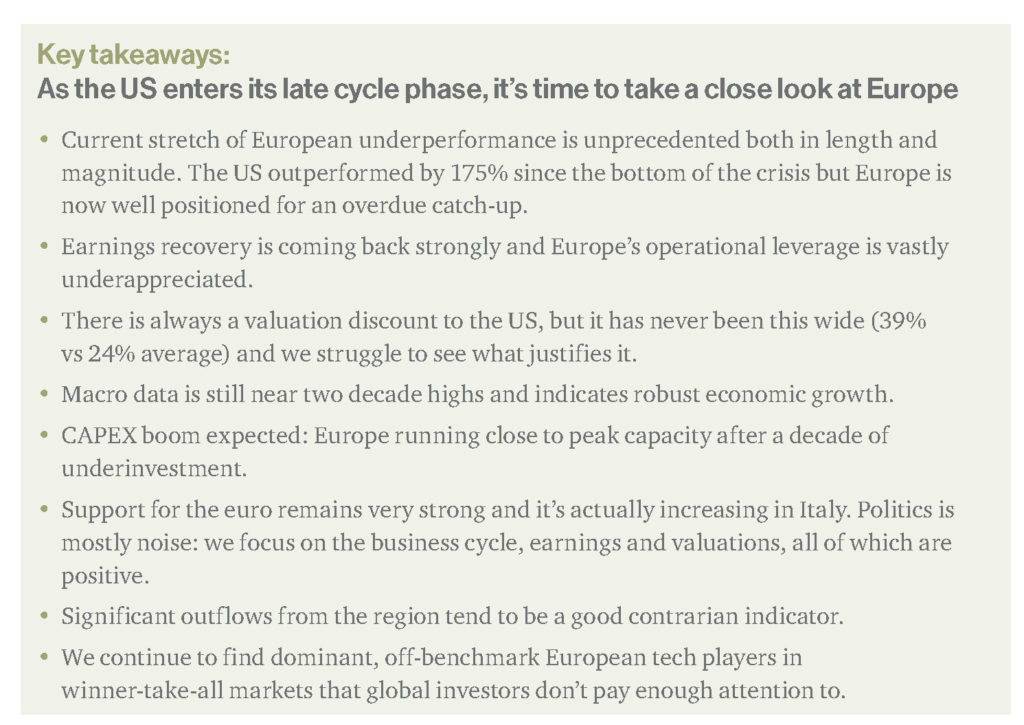

Over the last few weeks we met with a series of US investors to discuss why we believe the current opportunity in European equities is uniquely compelling. While on the one hand we’re seeing unprecedented interest in our strategies, we realize that many misperceptions still linger about Europe. Our goal for this piece is to recap our recent conversations and highlight why we think the outlook for European equities is the brightest it has been in over a decade.

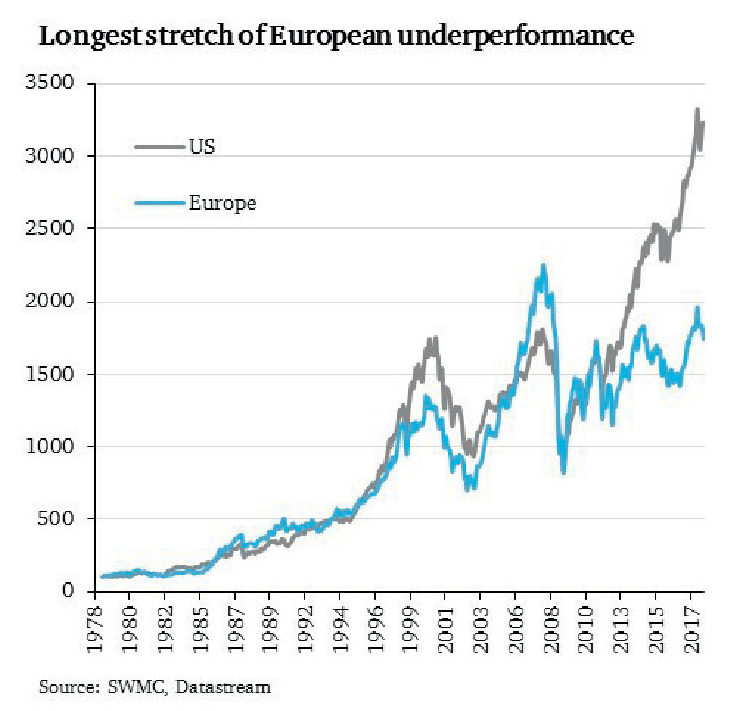

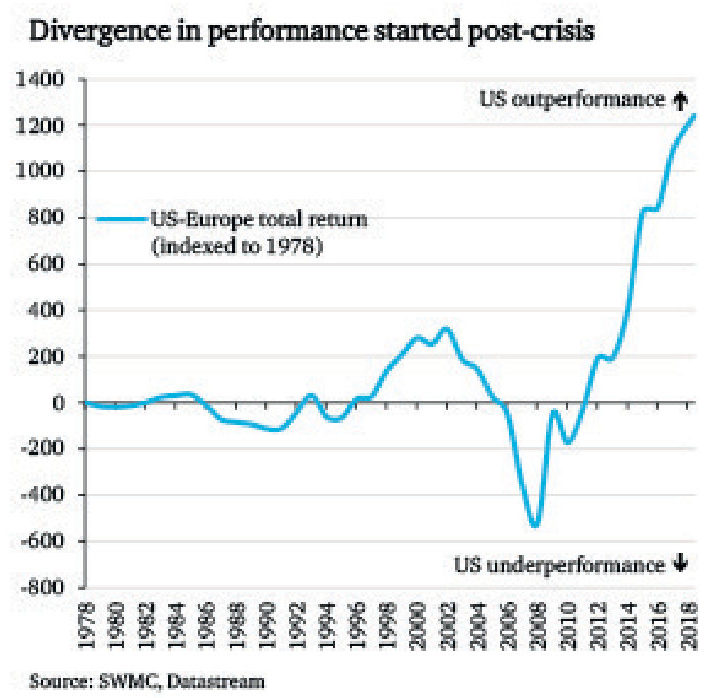

Myth: Europe always underperforms the US.

Reality: Not true historically and the current stretch of underperformance is unprecedented.

Europe and the US have moved in lockstep for decades and the stretch of significant European underperformance since the 2008 financial crisis is highly atypical.

However, even if we include the crisis, in dollar terms European equities outperformed the S&P 500 in 8 out of the last 15 calendar years.

Over the long term, during years of outperformance Europe is on average 13% ahead of the US.

Myth: European earnings are not growing as fast as the rest of the world.

Reality: No longer true and the operational leverage of the region remains underappreciated.

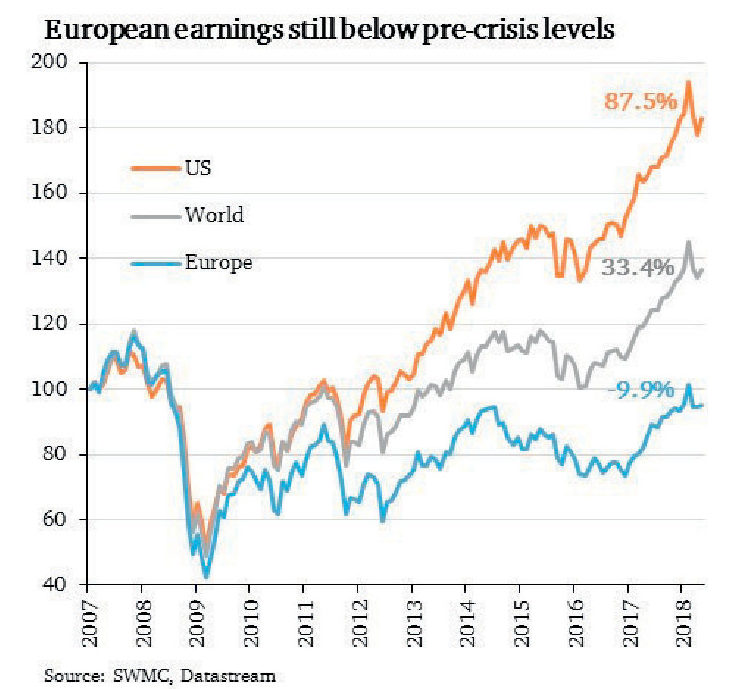

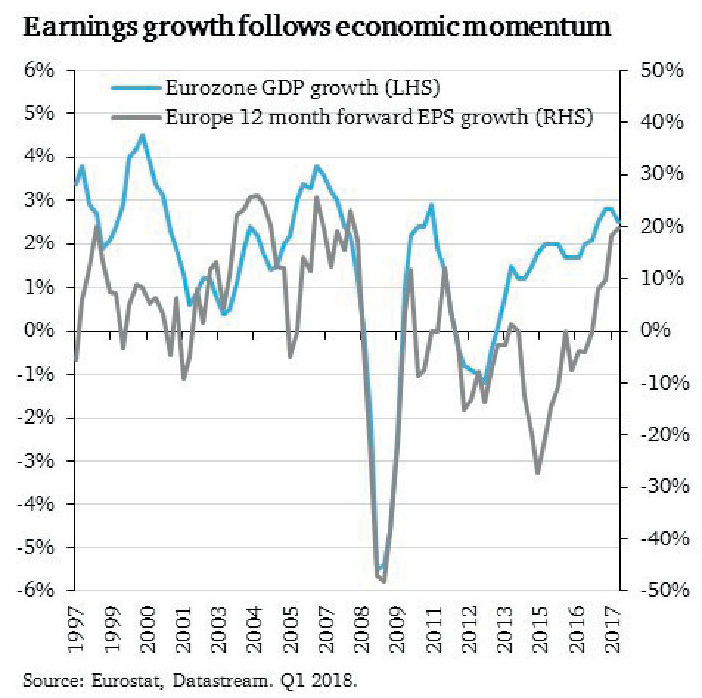

The earnings argument is valid, but backward looking. We believe that the single biggest reason for Europe’s post-crisis underperformance relative to the US has been the lack of earnings recovery.

From the bottom of the crisis (March 2009), US equities returned 290%, whereas Europe is only up 115%. During the same time European earnings doubled, but US earnings almost quadrupled.

European earnings are still below pre-crisis levels, while the US is nearly 90% higher and the rest of the world also grew 33%.

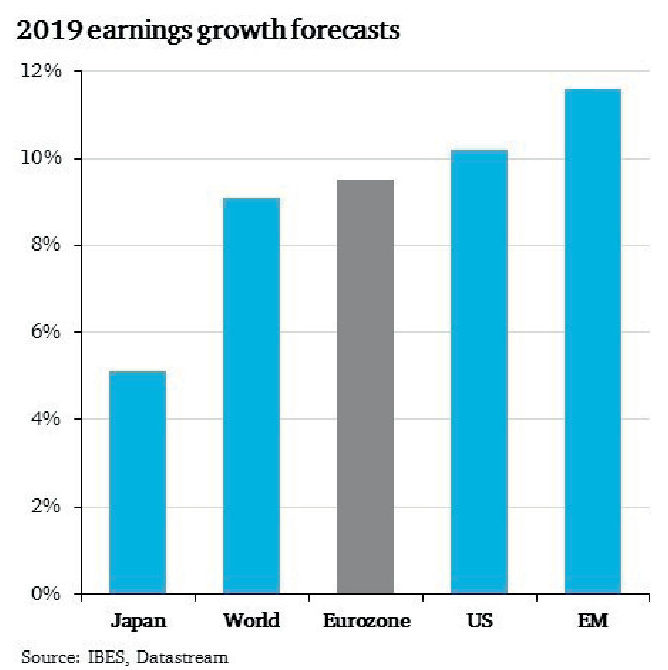

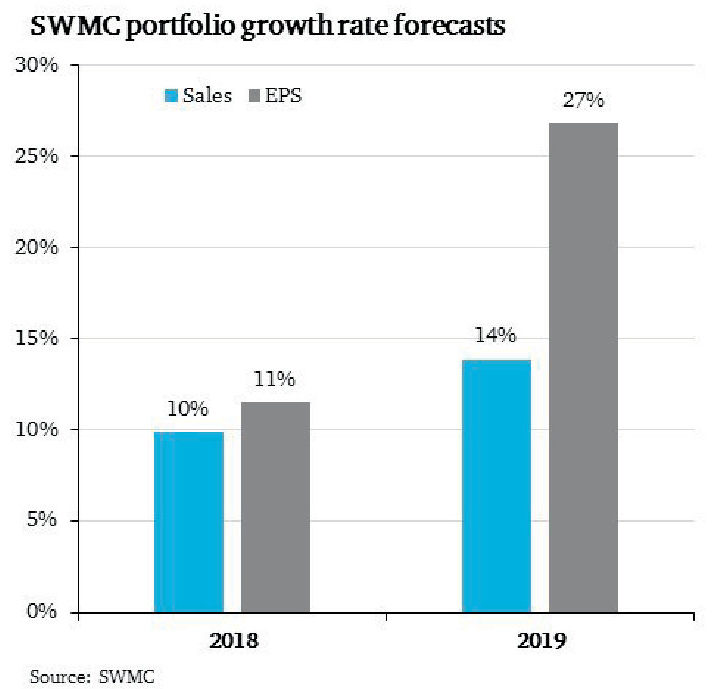

Looking ahead, analyst consensus now expects European EPS to grow at a similar rate to the rest of the developed world, at around 10% in 2019.

We think there is significant upgrade potential to these consensus numbers, based on what we are seeing in our own portfolio from a bottom up perspective and what macro data suggests.

Historic data and current operational leverage implies a 6x earnings multiplier on GDP growth, which should result in EPS growth closer to 15%.

We are seeing a particularly strong earnings inflection in 2019 in many of our value- oriented names.

At the same time the rapid growth of our technology related names is showing no signs of deceleration.

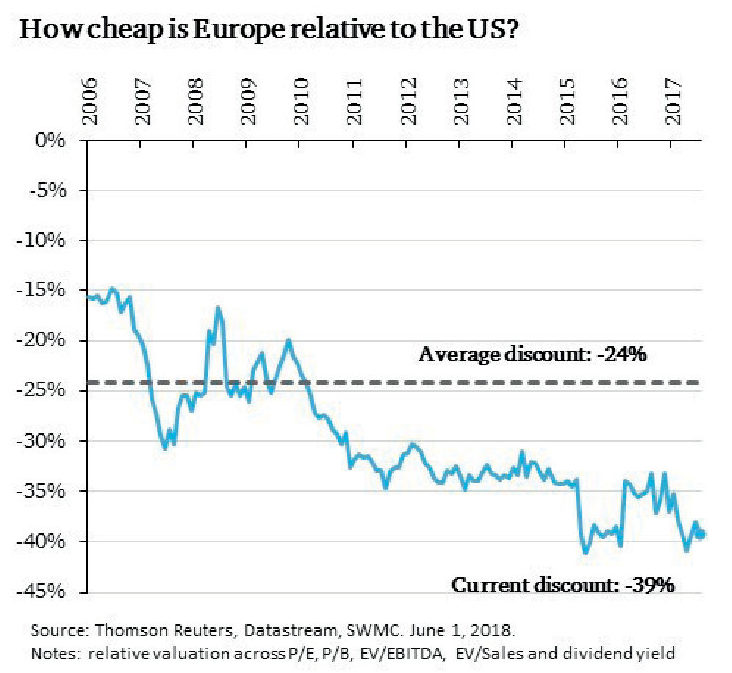

Myth: Europe is always trading at a discount to the US.

Reality: Yes, but the current discount is well above average and close to the widest on record.

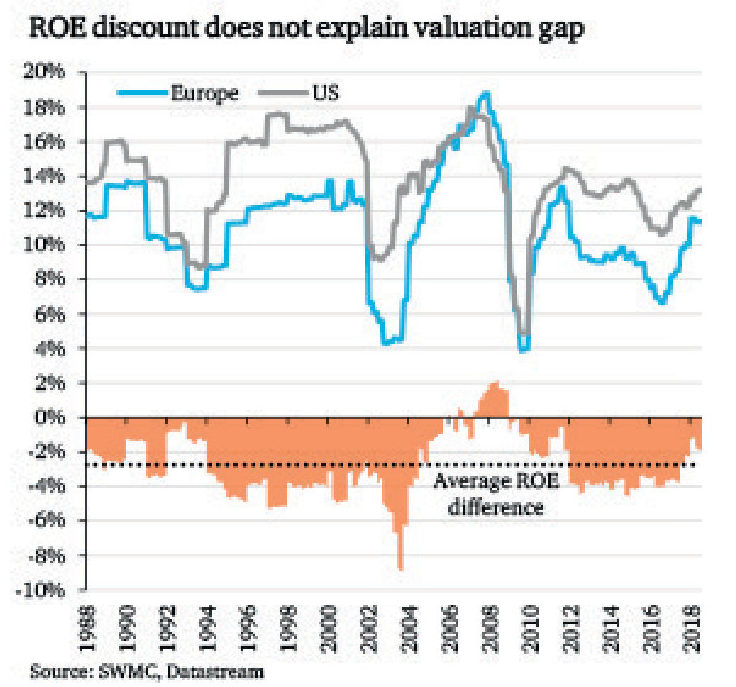

Investors are aware that Europe is trading at a discount to the US, and the usual reaction is that the US valuation premium is justified given higher growth, higher margins and better return on equity.

While we agree that some discount to the US is warranted, we are finding it very hard to explain why Europe is trading close to the deepest historic discount, while earnings are expected to grow at the same pace as the US and the margin and ROE gaps are actually narrower than their long-term averages.

We believe that as soon as operational leverage starts showing in Europe next year, a significant valuation rerating can take place.

A rerating to the average historic discount alone would offer 50% upside from current levels.

Myth: The recovery in European economies is running out of steam.

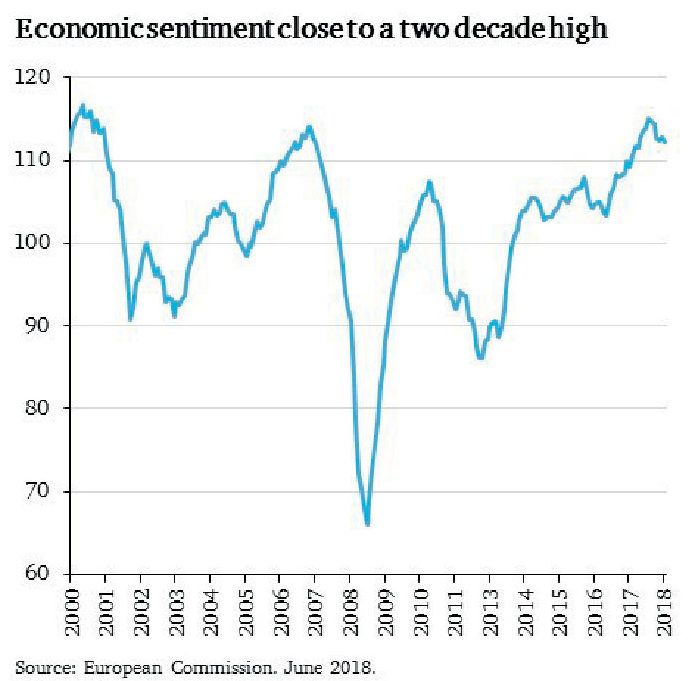

Reality: Macro data still near two decade highs and supportive of robust growth.

Across both hard and soft data European macro continues to impress.

In our view, the only thing that has slowed is the rate of change, and while growth is no longer accelerating (from a low base), the most recent readings of PMIs, retail sales, industrial production, credit growth, unemployment, and the

European Commission’s broader economic sentiment indicators all point to robust GDP growth for the next 24 months.

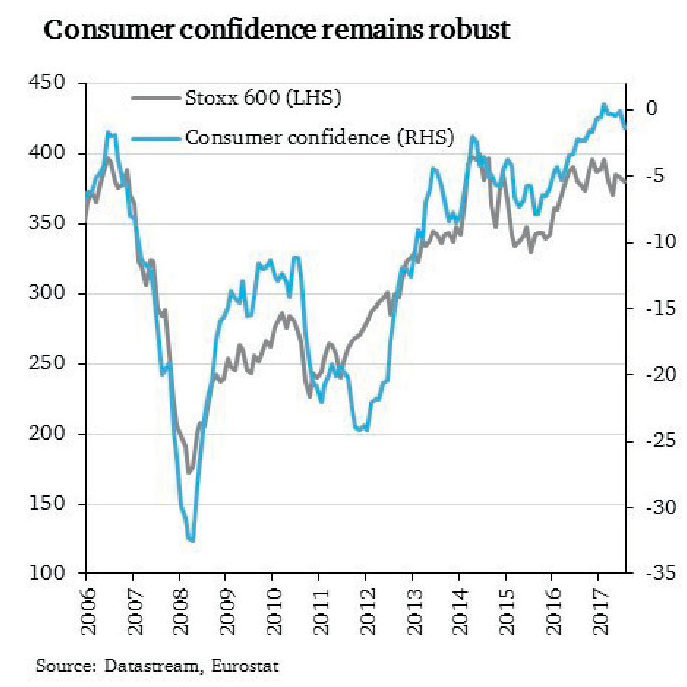

Consumer confidence remains at a two decade high and we see no reason why the market should not rerate to a level implied by the consumer’s bullish outlook.

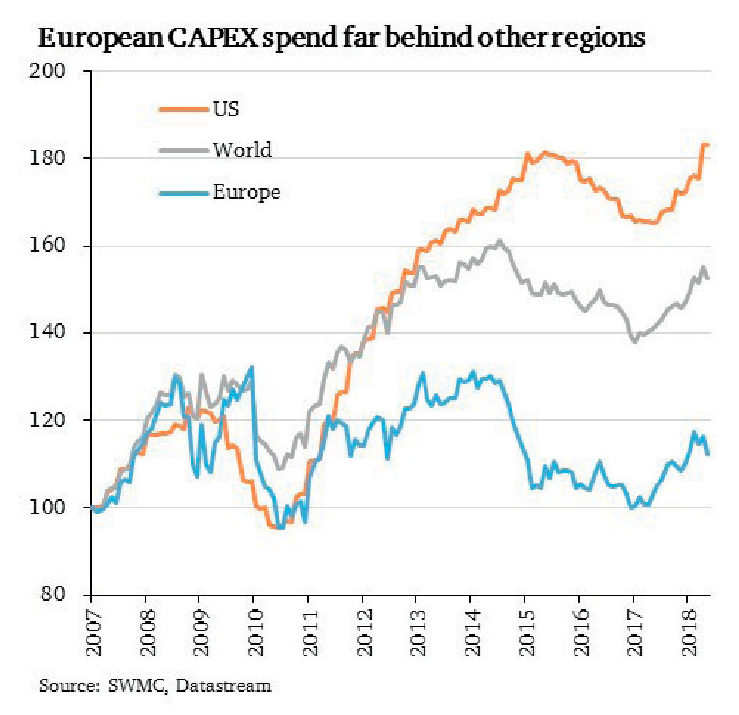

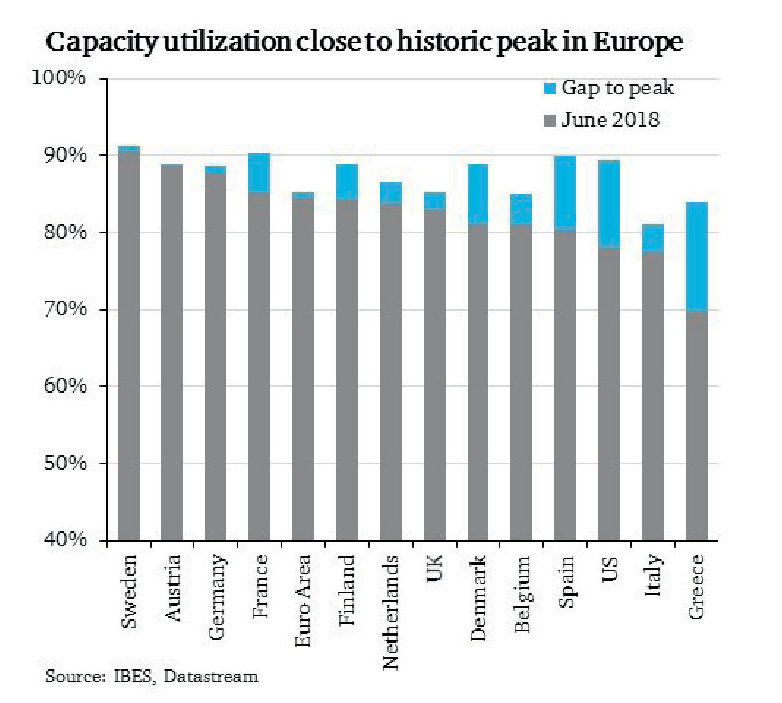

Myth: CAPEX remains muted – European CEOs are concerned about the outlook.

Reality: Capacity utilization is nearing peak levels and there’s strong pent-up demand from a decade of underinvestment.

Capital expenditure has indeed stagnated in Europe post-crisis on both an absolute and a relative basis.

The reason we believe that spending will pick up in the next 12 months is that many industries are now close to full capacity. This is something we picked up on in our conversations with executives over the last year and we’re now seeing it reflected in official data as well.

Tight labor markets and increasing automation are also supportive of a CAPEX boom.

The pent-up demand from a decade of underinvestment cannot be met overnight – we think we’re at the beginning of a multi-year spending cycle that should add further support to the already robust economic growth on the continent.

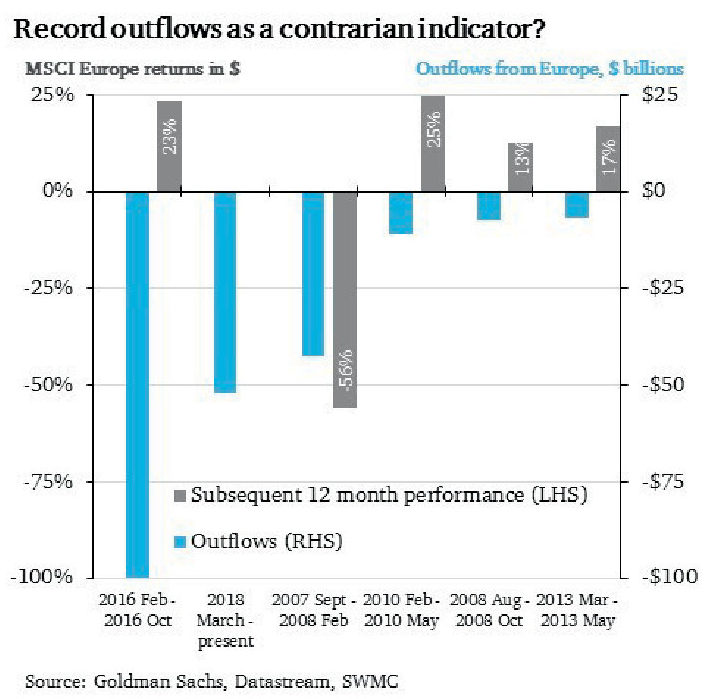

Myth: Outflows are a leading indicator of poor performance.

Reality: The 5 largest streaks of outflows were followed by positive returns outside 2008.

Since March we have now seen 18 weeks of consecutive outflows from Europe, totalling more than $50bn.

This is the second largest outflow streak on record behind 2016, when $100bn was pulled from Europe over 38 weeks.

It is worth noting, however that outside the financial crisis in 2008, the 5 largest streaks of outflows were followed by strong positive returns over the next 12 months.

Even on a relative basis, today’s levels of outflows have subsequently seen Europe outperform by 5% on a six month view.

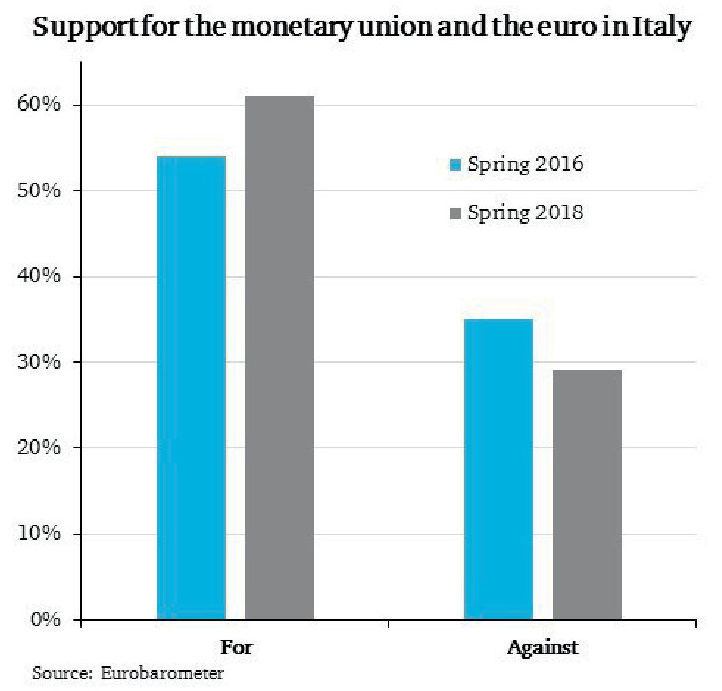

Myth: Italy is on the verge of leaving the euro and causing the collapse of the currency union.

Reality: Support for the euro has increased in Italy and there’s room for macro surprises.

The Italian election created significant volatility over the last few months as the market struggled to understand the implications of a government led by the two main populist parties (Five Star Movement and Northern League).

We closely monitored the evolution of the Italian coalition’s economic and political priorities and were pleased to see that many of the more extreme policies that each party included in early manifestos – such as a referendum on the euro – have been abandoned.

In our view, the shift from such a polarizing idea made perfect sense, as the majority of Italians is in favor of the euro and the monetary union. In fact, support for the common currency has strengthened over the last few years.

Italians also understand that their own savings, overwhelmingly held in euro denominated debt products, would be at huge risk should they abandon the common currency. Such a risk was never part of the Brexit referendum.

We believe that the populist shift in Italy does not present real systemic risk, and some of the more unorthodox proposals of the government could even offer a much needed boost to the stagnant Italian economy.

The core features of the government’s program are tax cuts and a universal income for Italy’s poorest households, both of which have the potential to lift Italian economic activity in the near term.

Myth: Technology dominates market performance but Europe is structurally underexposed.

Reality: True for the index, but not for our strategy. Tech has been the biggest contributor to our outperformance.

A frequent pushback against European equities is that the region has been unable to produce any dominant, global technology winners over the last few decades, while the US and China have generated trillions of dollars in shareholder value through innovative companies like the FANG stocks and emerging markets giants like Tencent and Alibaba.

While there is merit in this argument, we think the issue is more nuanced and highlights the danger of equating a region’s equity market with its market cap-weighted index.

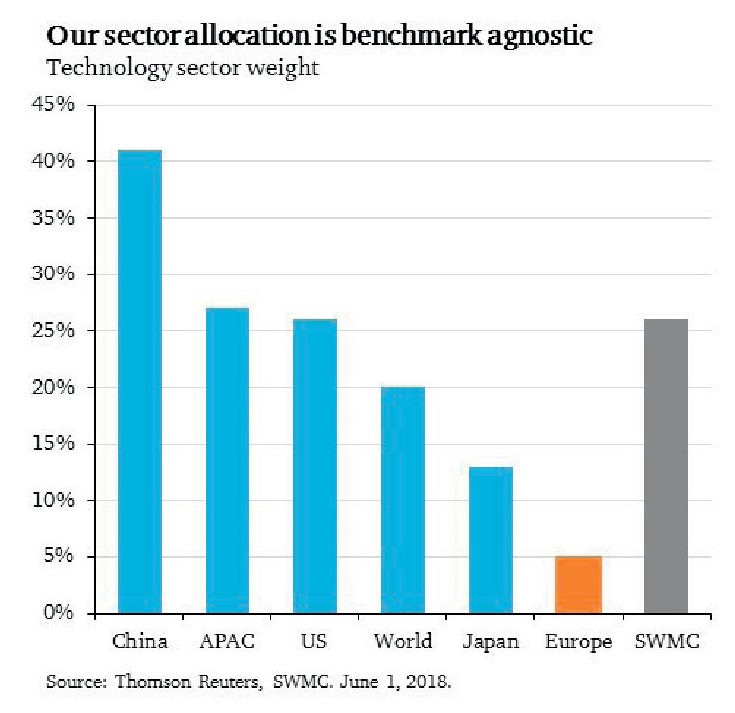

The ascendancy of technology stocks has been a key driver of post-crisis global equity market returns. As a result, technology’s weight in the S&P 500 is now 25%, and realistically over 30% based on our calculations that include ‘hybrid’ companies like Amazon. Similarly, in China and EM the index weight of Information Technology is now over 30%.

Europe’s Stoxx 600 on the other hand only has a 5% exposure to technology. Just two companies, SAP and ASML, account for almost half of the index weight.

We think this highlights a clear flaw in passive investing, which myopically focuses on investing in the largest companies, regardless of their quality and growth prospects.

Even though European technology stocks have significantly outperformed the market over the last 1, 3, 5 and 10 years, a passive investor benefitted very little from those returns due to their small index weights.

As we are completely benchmark agnostic, our portfolio weights are driven entirely by bottom up stock picking. This approach has resulted in having 13% average exposure to technology over the last 10 years, often through companies not captured by the benchmark. If we add ecommerce and other ‘hybrid’ companies that straddle technology and other traditional sectors, our average exposure moves closer to 20% and our current allocation is 26%.

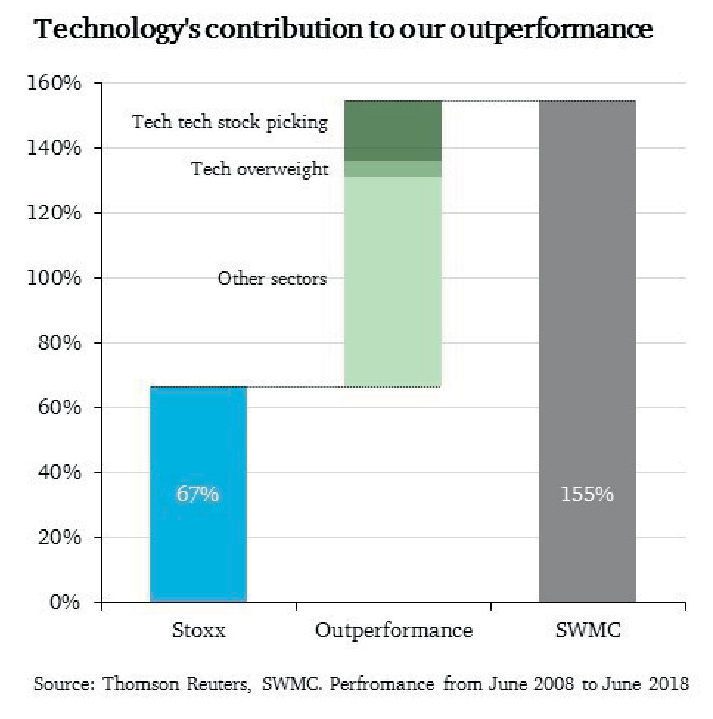

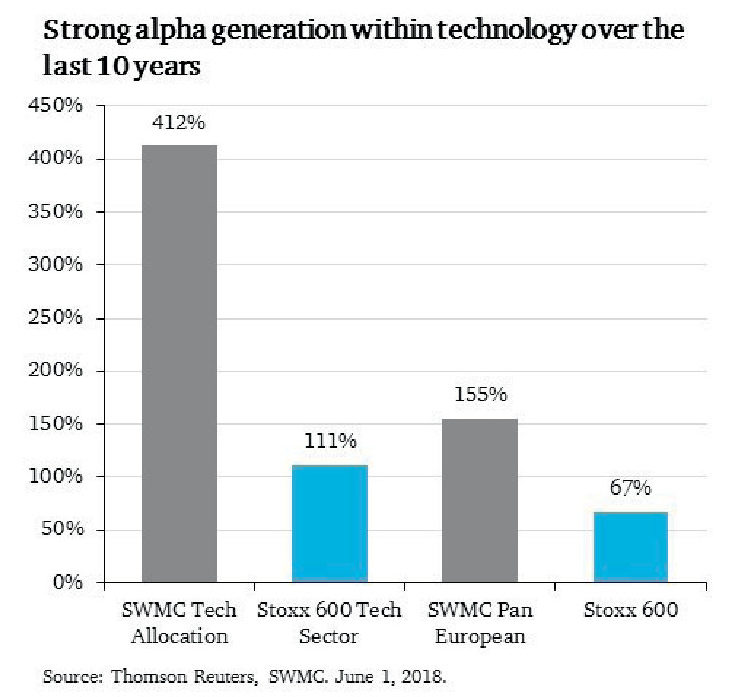

Having almost three times the index’s exposure to technology has tremendously benefitted our investors over the last decade. On a rolling 10-year basis our Pan European strategy generated 155% in gross returns, compared to 67% for the benchmark.

Information Technology has been the top contributor to our 89% outperformance, with roughly 24 percentage points of relative returns. It is important to highlight that our overweight allocation only accounts for 5 percentage points of that, and the bulk of our outperformance comes from stock selection within tech, which added a further 19 percentage points.

The benefit of an active approach is easy to see: while the index returned 67%, the tech sector of the benchmark was up 115%, and by ignoring index weights and constituents and investing only in the most innovative companies, our tech bucket outperformed by almost 4x, delivering 412% during the same 10-year period.

We have a very strong pipeline of potential new tech positions and there plenty of European companies that embody some or all of the key characteristics we look for in tech investments: dominant position in a winner-take-all market that’s favourably positioned on the adoption curve, unique IP, and strong network effects.

This thought piece is a confidential communication issued by S. W. Mitchell Capital LLP and is for information only. It was prepared by S. W. Mitchell Capital LLP only for, and is directed only at persons that qualify as Professional Clients or Eligible Counterparties under the FCA rules, including appropriate institutional investors and intermediaries. It is not intended for the use of and should not be relied on by any person who would qualify as a Retail Client. No person receiving a copy of this newsletter may copy it for transmission to another person. This document has been prepared from sources which are believed to be accurate, however in producing it S. W. Mitchell Capital LLP may have relied on information obtained from third parties and accepts no liability for the accuracy or completeness of such information. It is the responsibility of every person reading this document to satisfy himself as to the full observance of the laws of any relevant country, including obtaining any government or other consent which may be required or observing any other formality which needs to be observed in that country. Past performance should not be seen as an indication of future performance and will not necessarily be repeated. The value of investments and the income from them may fall as well as rise and is not guaranteed. The investor may not get back the original amount invested. Changes in rates or exchange may cause the value of investments to fluctuate. S. W. Mitchell Capital LLP is a Limited Liability Partnership registered in England No. OC312953. Registered address 38 Jermyn Street, London SW1Y 6DN. Regulated and authorised in the UK by the Financial Conduct Authority. The material provided herein has been provided by S. W. Mitchell Capital LLP and is for informational purposes only. S.W. Mitchell Capital LLP serves as investment sub-adviser to one or more mutual funds distributed through Northern Lights Distributors, LLC member FINRA/SIPC. Northern Lights Distributors, LLC and S.W. Mitchell Capital LLP are not affiliated entities.

About The Author: Stuart Mitchell

Stuart is the Managing Partner and CIO of S. W. Mitchell Capital and the Investment Manager of two funds, as well as a number of managed accounts. Prior to founding SWMC in 2005 Stuart was a Principal, Director and Head of Specialist Equities at JO Hambro Investment Management (JOHIM, now Waverton Investment Management). At JOHIM he set up and managed the Charlemagne Fund, a long/short European fund, and the JOHIM European Fund, a long only European fund. The JOHIM European Fund was number 1 rated by Micropal within its sector and three star ranked by S&P.

More posts by Stuart Mitchell