This article is authored by MOI Global instructor Andrew Macken, Chief Investment Officer at Montaka Global Investments, based in Sydney, Australia.

In the hit TV series, The Marvelous Mrs. Maisel, Miriam “Midge” Maisel – married, mother of two from the Upper West Side of New York City – discovers a hidden talent for stand-up comedy. Her natural, unexpected wit creates twists and turns with laughter and tears for her audience.

So too is Mr. Market today making fun of global equity investors. 2018 was a year of rotations, corrections and volatility. The year rounded out with an overwhelming general bearishness with many believing more downside lay ahead. But, as with Mrs. Maisel, should we expect the unexpected from Mr. Market?

In the white paper that follows, our analysis shows that global equities have arguably become less risky, not more risky, over the last four years. And there remains plenty of opportunities to exploit for high-quality active fund managers.

Furthermore, we examine the idea that algorithmic trading is creating unusual geographic and inter-sector rotations. If it is true that the algos are causing Mr. Market to become increasingly erratic, this creates a double-edged sword for investors. On the one hand, non-fundamental moves in stocks create mispricings which can be exploited by discerning active fund managers. This is great news for the patient, long-term investor who can tolerate some short-run volatility. But it also means that short-run performance metrics are less meaningful.

Section I – Did Mr. Market Run Out of Steam Four Years Ago?

Over the last four years, global equities have delivered a real return of approximately zero… True or false?

Before you scream “false”, let us mount an argument as to why it may be more believable than you think.

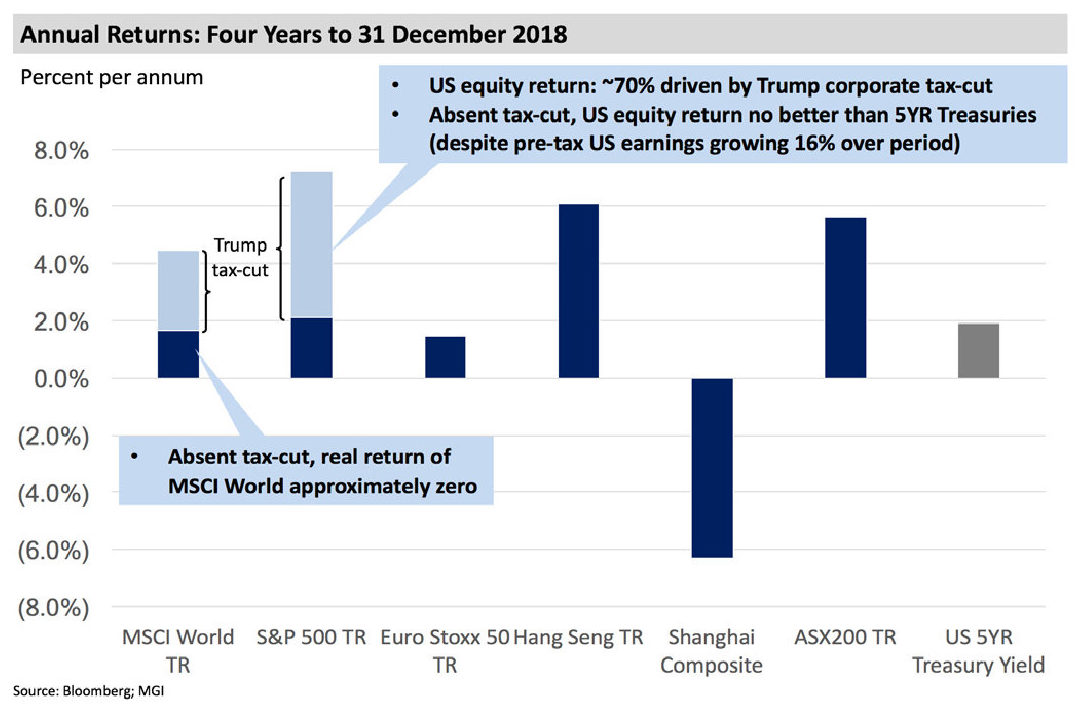

First, we observe that the MSCI World Net Total Return Index has delivered +4.5 percent per annum over the four-year period to 31 December 2018. This return is clearly above any global average rate of inflation suggesting real global equity returns have been positive over the period.

By far the most substantial contributor to the MSCI World’s return was the +7.2 percent per annum return generated by US equities – as measured by the S&P 500, in this case. Now, the US accounts for approximately 54 percent of the MSCI World Net Total Return Index, so this substantial return drove more than 80 percent of the total return of the MSCI World over this four-year period.

But what is sometimes forgotten is that US domiciled businesses benefited from a significant reduction in their corporate tax rate, from 35 percent to 21 percent, as part of President Trump’s famous Tax Cuts and Jobs Act of 2017. This reduction in the corporate tax rate effectively provided a one-time rebasing of US corporate earnings upwards.

We thought it might be interesting to consider what US equities may have delivered absent the Trump tax cut. Our analysis is simple in that, assuming a constant valuation multiple, we crudely deflate the US equity index by the degree to which US corporate earnings rebased upwards (which we assumed was 21 percent). We believe the results of our analysis are informative, notwithstanding its simplicity.

The analysis is summarized below which shows that approximately 70 percent of US equity returns over the last four years was driven by the reduction in the US corporate tax rate. Absent this tax cut, US equities would likely have delivered an average return of 1.9 percent per annum – exactly the same as the average yield of the five-year US Treasury Bond over the same period.

Now, upon adjusting the MSCI World Net Total Return Index for the Trump tax cut, the four-year annual return of +4.5 percent reduces to just +1.6 percent per annum. Arguably this return is in line with global inflation suggesting real global equity returns over the period have been approximately zero.

What conclusions should be drawn from the above?

First, proponents of passive index funds should send President Trump a Thank You card. Absent the US corporate tax cut, passive global equity returns over the last four years would have barely beaten inflation, as shown above.

A corollary here is that high-quality active funds management that can generate outperformance above average equity returns, or “alpha”, is worth a lot more to investors in a lower returning equity environment. By way of comparison, our global equity long-short strategy, Montaka, delivered a US dollar- equivalent return of 6.3 percent per annum, net of fees, over the three-and-a-half year period to 31 December 2018, despite an average beta of approximately 0.3.

Now, you might be wondering: why bother with equities at all? This is a valid question in light of the last four years of equity returns. Why take equity-risk to generate the return of a risk-free Treasury Bond? Of course, this risk/reward equation makes no sense – but this is what happened effectively over the last four years when we deduct the one-time benefit from the Trump tax cut.

To help make sense of the current situation, consider the following thought experiment. You can buy one of the following two securities:

Security A: an equity in a global monopolist growing revenues organically at 15-20 percent per annum that can be purchased today at a forward P/E ratio of 16x; or

Security B: a ten-year Treasury Bond that grows its coupon at 0 percent and can be purchased at a price-to-coupon ratio of 40x.

Which is more appealing? We think Security A by a mile – and that is why we own Facebook (Nasdaq: FB) in our global portfolios today.

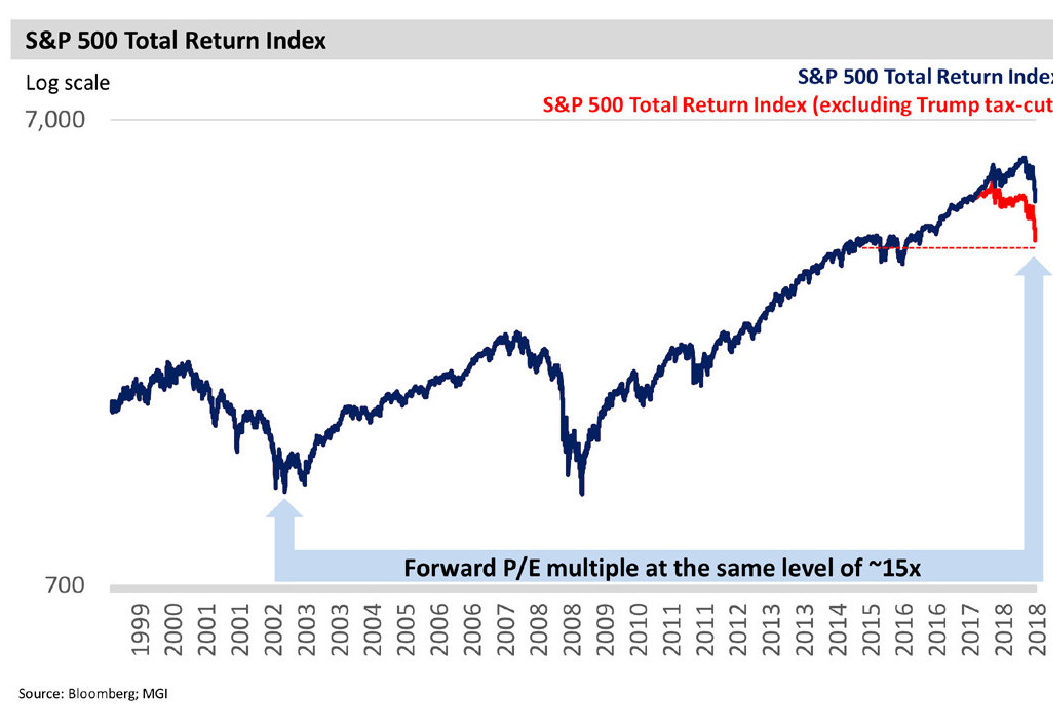

Let us now take the thought experiment one step further. Let’s say we buy Facebook today and we wake up in five years’ time with a total return on our position of just 1.6 percent per annum – equivalent to what the MSCI World delivered over the last four years, excluding the Trump tax cut. The implication here is that, absent a significant downgrade in earnings expectations, the P/E multiple in five years’ time must have become around 40 percent cheaper. This would mean that Facebook would be trading at less than 10x forward P/E ratio! Such a seemingly absurd valuation multiple for such a high-quality business gives us comfort that our return on this investment will likely be materially higher.

The key idea here is as follows: as earnings grow without commensurate growth in total shareholder return, then equities are essentially becoming cheaper, absent some material change to the trajectory of future growth or cost of capital.

Over the last four years, global equities have effectively drifted sideways (absent the one-time Trump tax cut); but pre-tax earnings have been increasing! In the US, for example, S&P 500 pre-tax earnings have increased by 16 percent over the last four years. Said another way: global equity markets have actually become cheaper, or less risky, over the last four years.

Now, you certainly would not think that stocks have become less risky if you read any financial press. The conventional wisdom is that equities are heading for a prolonged “bear market” – perhaps like what was observed at the beginning of the century. Between 2000 and 2002, the S&P 500 Total Return Index roughly halved. But it is worth noting that the forward P/E ratio of the S&P 500 today is the same as where it was at the bottom of the 2002 bear market – and roughly half of where it was at the top, in the year 2000.

We have no idea where global equity markets are going to go in 2019 or beyond. But we do know that, as stock prices fall, the probability of higher future investment returns increases. And in the second half of 2018, stock prices fell.

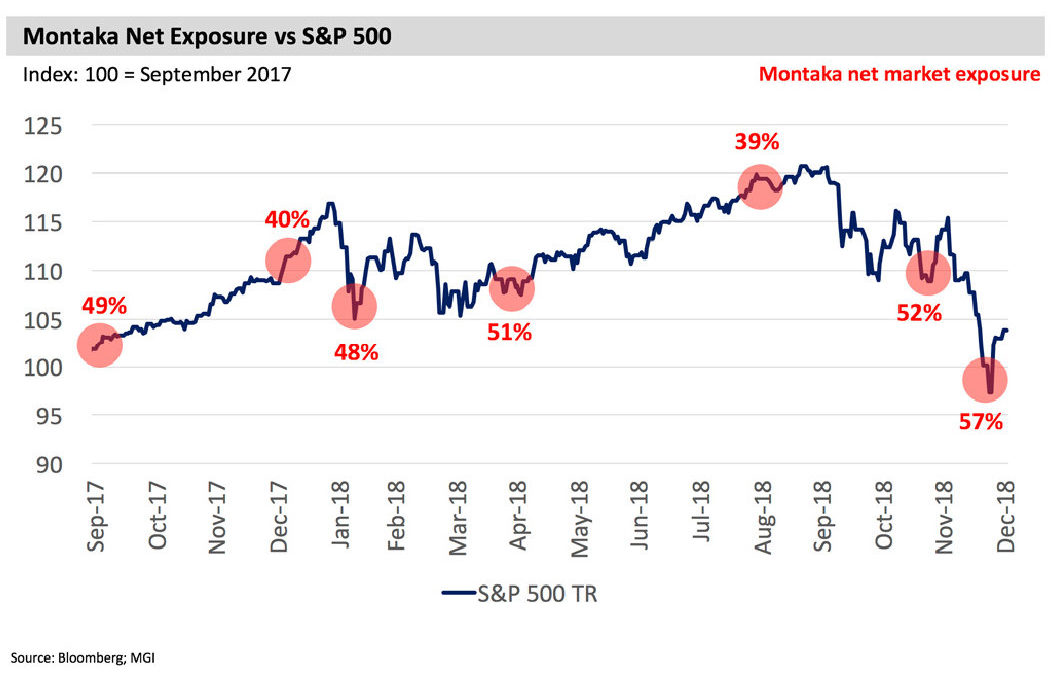

The benefit of a “variable net” long short strategy, such as Montaka, is that the portfolio’s net exposure to the overall equity market can be varied according to prospective risk/ reward profile. This is achieved through some combination of increasing long exposure and/or covering short exposure. As can be observed by the chart below, we increased Montaka’s net exposure as stock prices became cheaper in the fourth calendar quarter of 2018. And should stock prices fall even further, investors should expect Montaka’s net exposure to increase yet again.

One final point needs to be made here. While the focus of this Whitepaper has been on aggregate equity markets, readers should remember that we do not invest in markets. We invest in individual high-quality businesses when we believe they are materially undervalued. And we short businesses which are structurally challenged, mis-perceived and overvalued. While it is the bottom-up process of identifying new long and short opportunities that is the primary driver of changes in Montaka’s net market exposure, we also exercise top-down judgment to determine where the portfolio’s net exposure should be at any point in time. This top-down judgment is informed by analyses such as those contained in this Whitepaper and is typically consistent with what our research team is observing on a bottom-up basis.

To conclude this section, our message is that it is far from clear that we are heading into a prolonged bear market. Of course it is possible. But our analysis suggests the probability of such a prolonged bear market has actually reduced since four years ago. And should the market continue to move sideways, high- quality active funds management should be able to exploit plenty of mispriced stocks to generate superior returns relative to their passive counterparts.

Section II – Is Mr. Market Becoming More Erratic?

In 2018, global equity investors experienced a return of market volatility. This is not a bad thing – after all, it is during periods of market volatility that equity mispricings tend to be at their highest. And mispricings are the core ingredient for active managers to generate outperformance, or alpha, over time.

But in 2018, global equity investors were not just faced with volatility, they were faced with unusual geographic and inter- sector rotations. Many of these moves, it must be said, appeared non-fundamental in nature.

It is impossible to know what causes short-run moves in equity prices. In recent months, it was interesting to listen to an interview by Stanley Druckenmiller. His observations of current market conditions in the context of his 35 years’ experience as a top professional investor struck a chord with us.

“The algos have taken all the rhythm out of the market and have become extremely confusing to me.”

Druckenmiller reflected on a dynamic he observed in 2018. Interestingly, similar observations had been made on multiple occasions during the year inside the Montaka research team. Unlike Druckenmiller, however, we had no sensible explanation for what we were observing.

“The pharmaceuticals, which you would think are the most predictable earnings streams out there, so there shouldn’t be a whole lot of movement one way or another. From January to May, they were massive underperformers. In the old days, I would look at that relative strength and I’ll go: ‘this group is a disaster’… They were the worst group of any I follow from January to May. And with no change in news, and no change in Trump’s narrative and, if anything, an acceleration in the US economy, which should put them more toward the back of the bus than the front of the bus because they don’t need a strong economy, they have now been about the best group from May until now [September]. And I could give you about 15 other examples. And that’s the kind of stuff that didn’t used to happen.”

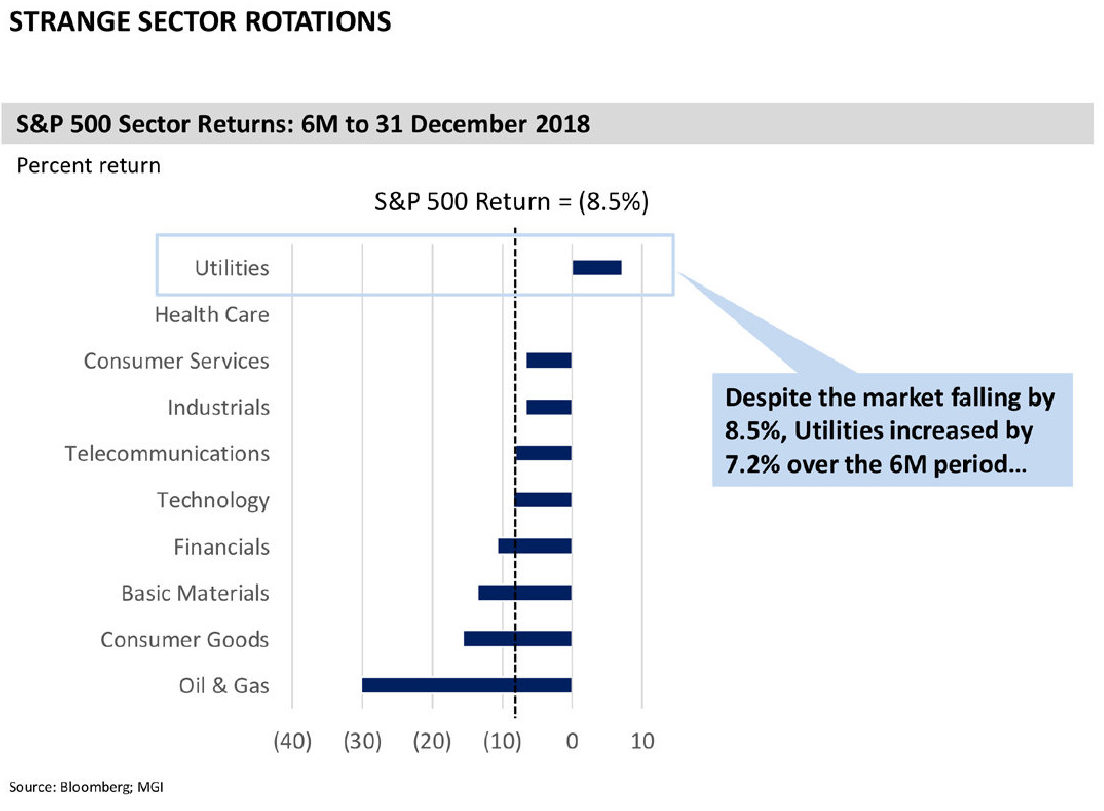

Now, we do not know for sure that algos are the source of the dynamics being observed. But we do know for sure that these dynamics are being observed. We recently witnessed significant outperformance of Utilities at a time when interest rates were increasing – a nonsensical move for sectors which are often treated by investors as “bond substitutes”.

So what to make of a global equity market that can be characterized as having pockets of non-fundamental moves in prices at different times?

First, this is great news. Non-fundamental moves in stocks’ prices create mis-alignments between price and intrinsic value which can be exploited by active managers who are sharply focused on such mispricings.

But there are other corollaries as well. For instance, how meaningful is short-run investment performance in the current environment? Here is the thought experiment: imagine a magic investment manager who always bought stocks at prices below their intrinsic value. By definition, this manager must outperform the market in the long run. But what about in the short run? Given the non-fundamental moves in groups of stocks at different times, this manager will experience periods of short-term volatility and underperformance. Imagine a scenario in which an undervalued business is purchased – only for that business to subsequently experience a temporary, non- fundamental move to the downside. A continuation of a diligent, well-thought out investment process may appear fruitless in the short-run due to these non-fundamental stock price swings.

Or take portfolio risk management. Many investors – especially institutional investors – require investment managers to decisively reduce portfolio risk during periods of draw-down.

The simple logic can be understood as follows: in periods of draw-down, the market is signalling to the manager that the portfolio positioning is inappropriate for the current market conditions. But how valuable is this market signal in a market construct which includes non-fundamental moves in different pockets in the market at different times?

This feedback from the market is something that investors, including Druckenmiller, used to rely on as some form of confirmation of one’s investment thesis. Under the current market conditions being observed, investors and risk managers alike need to reconsider the weighting they apply to such market signals. And arguably, the importance of thoughtful and accurate fundamental analysis, combined with a disciplined investment framework, has only increased in this new market environment.

Members, log in below to access the restricted content.

Not a member?

Thank you for your interest. Please note that MOI Global is closed to new members at this time. If you would like to join the waiting list, complete the following form:

Disclaimer: This document was prepared by Montaka Global Investments LLC. This document was approved by Montgomery Investment Management Pty Ltd, AFSL No: 354 564 (Montgomery) the trustee of the Montaka Global Fund. MGIM Pty Ltd (MGIM) is the Investment Manager of the Montaka Global Fund and an Authorised Representative (AR No: 001007050) under the AFSL of Montgomery. Montaka Global Investments provides research services to MGIM. The information provided in this document does not take into account your investment objectives, financial situation or particular needs. You should consider your own investment objectives, financial situation and particular needs before acting upon any information provided and consider seeking advice from a financial advisor if necessary. Future investment performance can vary from past performance. You should not base an investment decision simply on past performance. Past performance is not an indicator of future performance. Investment returns reviewed in this document are not guaranteed, and the value of an investment may rise or fall. This document is based on information obtained from sources believed to be reliable as at the time of compilation. However, no warranty is made as to the accuracy, reliability or completeness of this information. Recipients should not regard this document as a substitute for the exercise of their own judgement or for seeking specific financial and investment advice. Any opinions expressed in this document are subject to change without notice and MGIM is not under any obligation to update or keep current the information contained in this document. To the maximum extent permitted by law, neither MGIM, nor any of its related bodies corporate nor any of their respective directors, officers and agents accepts any liability or responsibility whatsoever for any direct or indirect loss or damage of any kind which may be suffered by any recipient through relying on anything contained in or omitted from this document or otherwise arising out of their use of all or any part of the information contained in this document. MGIM, its related bodies corporate, their directors and employees may have an interest in the securities/instruments mentioned in this document or may advise the issuers. This document is not an offer or a solicitation of an offer to any person to deal in any of the securities/instruments mentioned in this document.

About The Author: Andrew Macken

Andrew Macken is the Co-Founder and CIO of Montaka Global Investments, a global equity manager based in Sydney and New York. Prior to establishing Montaka, Andrew worked as a senior member of Jim Chanos’ research team at Kynikos Associates, a global equity long/short fund based in New York. Andrew holds a Master of Business Administration (Dean’s List) from the Columbia Business School in New York. Andrew also graduated with High Distinction with a Master of Commerce; and First Class Honours with a Bachelor of Engineering from the University of New South Wales in Sydney.

More posts by Andrew Macken