This article is authored by Todd Wenning, senior investment analyst at Ensemble Capital Management, based in Burlingame, California. Visit Ensemble’s Intrinsic Investing website for additional insights.

Imagine you went back to 2007 and told investors that within the next ten years, General Electric would cut its dividend twice. You’d have been mocked and ridiculed.

At the time, GE was one of five U.S. industrial companies with AAA-rated credit, had just increased its dividend by 11% (its 32nd consecutive annual increase), and was one of the largest companies in the world by market capitalization. Such an outcome would have seemed implausible.

Yet here we are. The GE story is complex (which in itself is a problem), but one of the causes of its recent decline was consistently poor capital allocation decisions.

Here’s Morningstar’s take: “(GE’s) ambitious overhaul came with an overly aggressive midterm financial target of $2 in earnings per share by 2018, which probably colored management’s capital allocation decisions in a manner that ultimately exposed GE’s investors to unnecessary risk.”

As the GE story illustrates, the way management allocates capital can have a massive impact on long-term shareholder returns.

Simple doesn’t mean easy

At Ensemble, the two things we look for in a management team are their intent to optimize return on invested capital (ROIC) and their skill at allocating capital to maximize shareholder returns.

You’d think that these two things would be common, but they are more the exception than the rule. Indeed, our eyes light up when we see multiple mentions of ROIC (or return on equity) along with a discussion on capital allocation in annual reports, management meetings, or quarterly earnings calls. It’s that rare.

Why might this be the case? One reason is poor incentives. You never hear of a stock jumping 10% because ROIC beat expectations. No, it’s usually because the company reported better-than-expected revenue or earnings per share. Perhaps not surprisingly, two of the most common financial metrics used in management bonuses are – you guessed it – revenue and EPS. Unfortunately, neither of those metrics alone tell you if the company is creating shareholder value.

Revenue and EPS growth are essential, of course, but we believe that if the company aims to widen its moat (that is, optimize long-term ROIC) and thoughtfully allocate capital, revenue and EPS will take care of themselves.

Decisions, decisions

There are three ways a company can return cash to claimholders: pay a dividend, buyback shares, or reduce debt. There are smart and dumb uses of each. What we want to see is that management has thoughtfully weighed their options based on return opportunities.

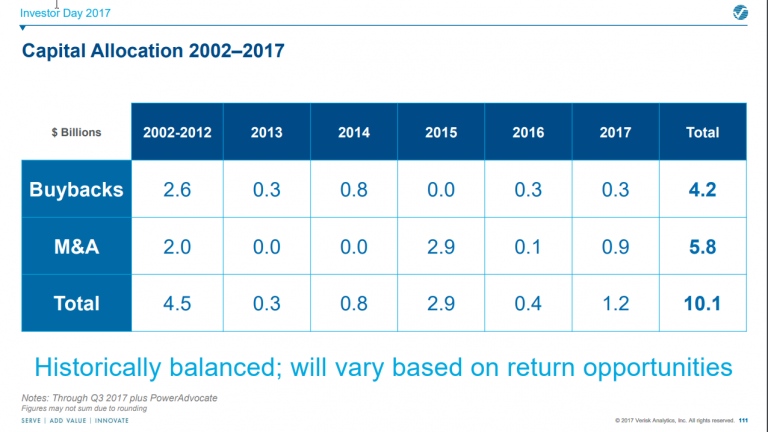

To illustrate, at its 2017 investor day, Verisk Analytics showed how the firm allocated capital between buybacks and M&A over the previous 15 years.

As the slide mentions, Verisk decides on buybacks or M&A depending on the available opportunities. Even if they don’t always make the correct assessment in hindsight, we like that there’s a process in place.

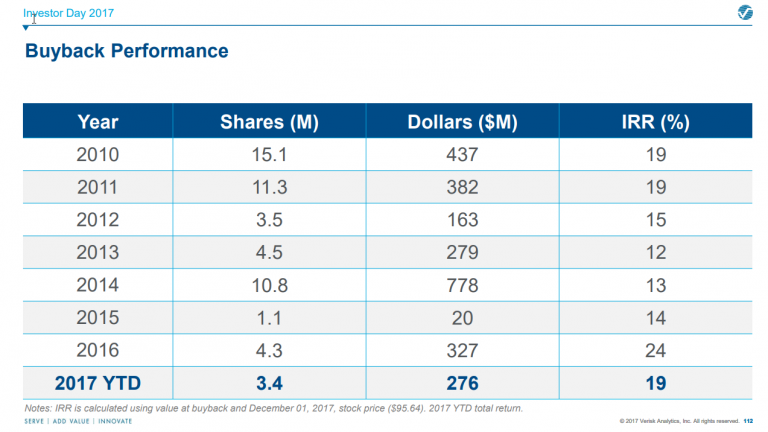

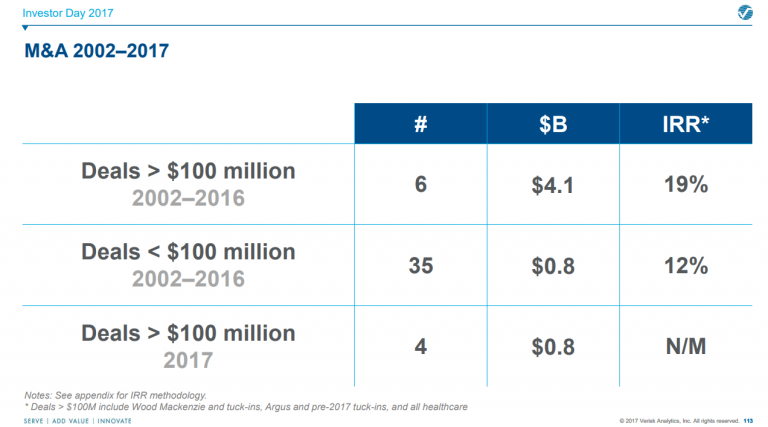

We were further impressed that Verisk followed the above slide with IRR results from their capital allocation decisions.

Again, this level of transparency is rare, but we welcome it and would like more companies to follow suit.

Companies with moats are rare, as are companies led by thoughtful capital allocators. Companies that have both are exceptional and are precisely the kind of firms we want to own in our portfolio.

Clients, employees, and/or principals of Ensemble Capital own shares of Verisk Analytics (VRSK).

The information contained in this post represents Ensemble Capital Management’s general opinions and should not be construed as personalized or individualized investment, financial, tax, legal, or other advice. No advisor/client relationship is created by your access of this site. Past performance is no guarantee of future results. All investments in securities carry risks, including the risk of losing one’s entire investment. If a security discussed in this blog entry is owned by an employee, principal and/or client of Ensemble Capital you will find a disclosure regarding the security held above. Should an employee, principal and/or client of Ensemble Capital subsequently purchase or sell any position in a security discussed in this blog entry, we will not update the above disclosure nor revise any archived blog entry after the date it is originally posted. If reviewing this blog entry after its original post date, please refer to our current 13F filing or contact us for a current or past copy of such filing. Each quarter we file a 13F report of holdings, which discloses all of our reportable client holdings. Ensemble Capital is a discretionary investment manager and does not make “recommendations” of securities. Nothing contained within this post (including any content we link to or other 3rd party content) constitutes a solicitation, recommendation, endorsement, or offer to buy or sell any securities or other financial instrument.

About The Author: Todd Wenning, CFA

Todd is a senior investment analyst at Ensemble Capital. Before joining Ensemble, Todd was an analyst at Johnson Investment Counsel, where he worked on the firm’s SMID cap strategy. Prior to that, Todd was a sell-side analyst at Morningstar, where he led Morningstar’s equity stewardship methodology and covered companies in the basic materials, industrials, and consumer sectors. Earlier in his career, Todd worked for The Motley Fool, SunTrust Asset Management, and Vanguard. He holds a BA in History from Saint Joseph’s University in Philadelphia and the Chartered Financial Analyst designation.

More posts by Todd Wenning, CFA