This article by MOI Global instructor John Lewis is excerpted from a letter of Osmium Partners, based in Greenbrae, California.

Travelzoo Inc.[1], together with its subsidiaries, provides travel, entertainment, and local deals from travel and entertainment companies, and local businesses in Asia Pacific, Europe, and North America. The company’s publications and products include Travelzoo Websites; Travelzoo iPhone and Android applications; Travelzoo Top 20 email newsletter; and Newsflash email alert service. It also operates the Travelzoo Network, a network of third-party Websites that list travel deals published by the company; and Local Deals and Getaway services, which allow its subscribers to purchase vouchers for deals from local businesses, including spas, hotels, and restaurants through the Travelzoo Website. The current market capitalization is approximately $157 million. (TZOO is a holding across all funds.)

• Achieved Record Subscribers base at 29.8 million

• Highly Attractive Unit Economics: Undiscounted Lifetime Value of $35 with subscriber acquisition cost of just $2.50 per sub.

• Guidance for Revenue Acceleration

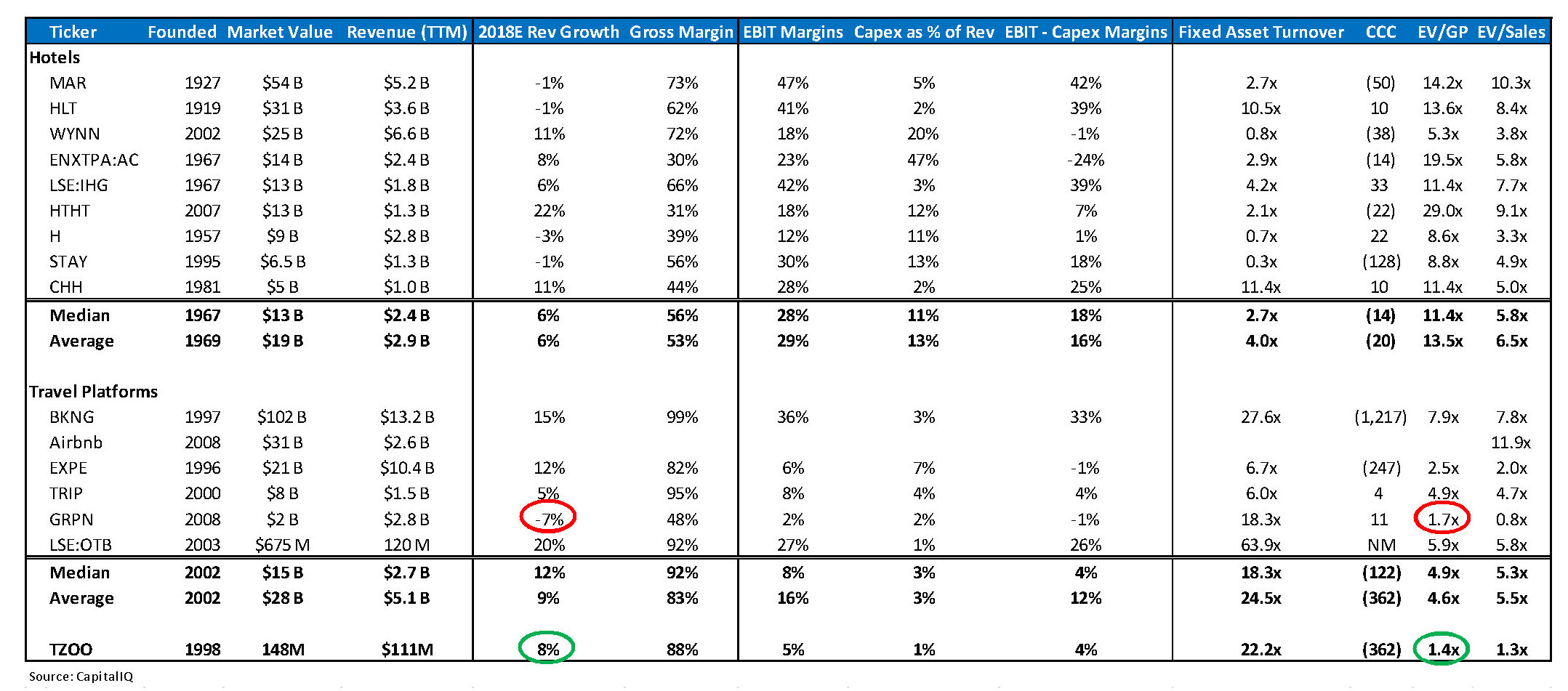

• Valued at 1.4x Gross Profit vs. Peer group at 5x!

• We believe TZOO value to a Strategic Buyer is $30-40

• We believe as a standalone public company Travelzoo is worth $20-25+

• Over the last 16 years TZOO has averaged over +30% for both ROE and ROIC

• Since IPO averaged 5.3x EV/Sales, currently 1.3x EV/Sales

• 10Q filing showed, after earnings in late July TZOO repurchased 2.4% of the company for $13.60 per share.

• Over the last 7 years, TZOO has repurchased 28% outstanding shares paying an average of $17.48 a share.

• One negative: is the Founder’s Trust has been a seller, reducing his position from 54% to 51% of the outstanding shares in 2018. They need cash for the Trust, and were sellers as low as $7-8 as well.

We believe in a sale to a strategic buyer, Travelzoo is worth between $400-500 million ($32-40) based on 4-5x gross profit of $100 million (88% gross margin) of which we believe a strategic buyer should be able to drop $40-60 million to the bottom line. Travelzoo public peer group trades exactly in this range with a median EV/Gross Profit of 4.9x with an average of 4.6x vs. TZOO at only 1.4x! In the higher range of valuations is On The Beach (OTB.L), which trades at 6x EV/Gross Profit and the lowest valuation is Groupon (GRPN) which is shrinking -7% and is valued at 1.7x EV/Gross Profit. Since the IPO in 2002, TZOO has averaged a valuation of 5.2x EV/Sales vs. the current 1.3x.

Standing on its own two feet, Travelzoo business trajectory is improving, as the company has guided to accelerating revenue growth in the 2H18 and doubling of revenue over 2-3 years with targeted 15-30% operating margins at scale. If this is achieved, we believe, over the next 3 years, Travelzoo could generate in aggregate $7-8 per share in EBIT, increasing the cash balance to $8-9 per share and push the stock to reach $50-60. Currently TZOO has a “safety net” of just under $2.00 in cash per share with $1.00 per share in EBIT from US and Europe (growing +6% and +8% yoy, respectively) or about 10x EV/ US & Europe EBIT. As a floor valuation, Groupon (GRPN) which is shrinking (-7%) trades at 1.7x EV/Gross Profit, applying this to TZOO yields $15.00 (TZOO is outgrowing GRPN by 15%).

From the company’s IPO in 2002, Travelzoo grew revenue from $10 million to $170 million in 2013 (revenue grew every year). In 2011, Travelzoo generated $3 a share in EBIT and stock traded between $80-100. On an EV/Sales basis, the peer group trades on average at 5.5x EV/Sales to Travelzoo’s current 1.3x EV/Sales. After rechecking our core thesis from a 360 degree perspective, we remain convinced TZOO is both significantly undervalued and delivers enormous value to both subscribers and travel partners. Travelzoo generated 22% Return on Capital for the trailing 12 months ended June 30th. Over the last 15 years, TZOO has achieved results that less than 1% of public companies have achieved: averaged over +30% for Return on Equity and Return on Capital. Finally, since the Travelzoo’s IPO the company has built a global brand as subscribers have grown nearly 10x over the last 16 years.

Travelzoo’s Flywheel of Value Creation

1. Travelzoo has very attractive member demographics:

• Mature: 69% are age 45+

• Affluent: 44% have household income over $100,000

• Smart: 89% are college educated

• Consumers: 67% are female

• Worldly: 85% have valid passports

• Travelers: 79% took 3+ trips last year.

2. Travelzoo Members are engaged and rate the platform highly

• The Travelzoo IoS App gets a 4.9 rating out 5 for IOS app w 17,000 reviews

• 90% of TZOO members would recommend to a friend,

• 90% were very satisfied with the product,

• 90% will make a future purchase via TZOO.

• We estimate average member stay as a Travelzoo Subscriber is 10 years.

• Travelzoo is the 3rd most followed travel business on Facebook with an active base of 4.4 million

• Travelzoo’s Mobile app has been downloaded 5.7 million times.

3. Travelzoo Partners/Suppliers

• Travelzoo partners/suppliers love Travelzoo as well. Why?

• Affluent members that spend more heavily at the property featured

• TZOO is an ad model vs. % take rate for a deal

• Travel suppliers generate exceptional returns but can’t place much $ at work vs. other channels

• Reach: TZOO has 30 million subscribers/members with total reach with partners to 70 million potential global travelers.

For further details: Travelzoo exhibits 43 case studies of Travel Partners’ success from TZOO’s services click here: Case Studies.

Travel Partners Love Travelzoo

• Case Study: Las Vegas Hotel Books 10,500 Room Nights in 10 Days

A Las Vegas Hotel increased occupancy with Travelzoo’s products resulting in $650,000 in incremental revenue and delighted customers of which 93% enjoyed the experience and 91% plan to return.

• Case Study: Canadian Vacation Company Generates Nearly $2,000,000

Canadian Company launched a 6-month Travelzoo campaign utilizing Travelzoo’s Top 20, Newsflash, and website placements resulting in nearly $2 million in revenue and 1,600 bookings.

Travelzoo has steadily grown the underlying earnings engine of the business, and in July TZOO hit a new record with nearly 30 million subscribers up from 20 million in 2011 when the stock hit $100. We think TZOO can meaningfully grow revenue off a large base of nearly 30 million subscribers as current revenue per sub is just over $4.00 and in 2012 revenue per subs was $7.00. New products and modest subscriber growth, especially in Asia, could lead to substantial shareholder value creation as the stock trades at 1.3x EV/Sales, a massive 70%+ discount to the peer group’s median and average multiple of 5.3x and 5.5x EV/sales, respectively. Furthermore, since the IPO, TZOO has averaged 5.3x EV/Sales. To quote TZOO CEO from the July earnings call “…we’ve shown in the last 3 quarters, revenue is going up, again, and this will continue, and we still hope that in 2019 that will even further accelerate.”

TZOO Offerings

Travelzoo’s main attraction are its curation of high value deals for both the member and partners. The Deal Expert’s job is to “guarantee that any deal with my name on it is truly the best rate anybody is going to pay for that experience, period.” The company offers an annual stipend and an additional three days to experience a Deal offered on Travelzoo’s website. These experts spend a lot of time not only researching, but negotiating then marketing the deal to its members.

In order to facilitate this curation to 30 million subscribers globally, Travelzoo has recently been investing heavily into its technology, revamping both mobile app and website (high rating on IOS and #3 on FB). They invested $2.5M for a 25% equity stake in WeekenGo and its packaging technology (members buy more when deals are bundled with hotels and flights). They also built their entire hotel booking technology/platform internally to allow members to book hotels directly through TZOO. With the customer’s interest in front, Travelzoo’s products attract and retain their user base, which allows partners access 30 million subscribers globally with a high return on marketing dollars. WeekenGo: https://www.weekengo.com/en-US

Travelzoo’s Exceptional Unit Economics

In addition to high quality deals and subscribers, we believe TZOO’s business has exceptional unit economics and operating leverage with scale. A subscriber currently generates $4.00 in revenue per year (TZOO has reached as high as $7 per sub) to generate $3.50 in gross profit (gross margins have always been above 85% for 20 years) and stays for around 10 years (est. annual churn = ~10%). We estimate the undiscounted lifetime value of a subscriber is $35 and TZOO acquires a subscriber for between $2-3, or 11x+ LTV/CAC. We estimate customer acquisition costs in the LTM were $2.50. With nearly 30 million subscribers, TZOO should be able to reach $7 in revenue per sub again from the current trough of $4 translating into $200 million in revenue. In other words, $1 more in annual revenue per subscriber = $30 million to the top line and $25+ million in gross profit.

Investments in Growth

It is not the first time TZOO has gone through a revaluation. We have seen this scenario play out in the late 2000’s when Europe division was losing money due to investments in growth and North America was highly profitable. Now, North America and Europe are highly profitable (and growing) and Asia is in a growth investment phase. As Asia reaches breakeven the true earnings power will be evident – North America/Europe currently generates ~$12-14mm of EBIT and Asia is losing $8-10mm. Given the recent investments in growth and a small share base (Founder owns 55% of 12.5M shares; 5.6M est. real float), there are wild swings in EPS quarter over quarter, but the investments are paying off, with all geographies increasing revenue year over year in 2018.

Recent Investments – we believe the following are strong ROI re-investment bets

• Investment in Asia Pacific Market for marketing & new hires

• Internally built entire hotel booking technology/platform – allows members to book hotels directly through TZOO.

• Marketing investment to maintain and grow subscribers in all 3 geographies: North America, Europe, Asia. (TZOO invests about $6 million a year to stay flat)

• WeekenGo and their packaging technology (members buy more when deals are bundled with hotels and flights) – $2.5M investment for 25% equity stake.

• Mobile App Development & Website revamp

• From 2011-2017, management bought back 3.5 million shares for $61 million at an average price of $17.43; reducing share count by 22% from 16 million to 12.5 million today. 500K share buyback plan was authorized on March 2018.

Travelzoo’s Comparable Companies

Travelzoo’s comparable companies consist of hotels and travel platforms that trade at many multiples higher than TZOO’s valuation, in some cases, for businesses that have dim forward looking estimates, declining sales, and are less efficient. For instance, Groupon recently had to pay IBM $83 million for patent infringement, sales are declining by 7% with 2% EBIT margins, and still trades at 1.7x EV/GP vs. 1.4x EV/GP for TZOO. On The Beach (LSE:OTB) a similar model to TZOO trades at 6x EV/gross profit as well as numerous other Travel platforms trade at an average of 4-5x EV/GP to TZOO’s 1.4x EV/GP.

Airbnb and Priceline (BKNG) trade at north of 8x sales and hotel companies trade at 4-10x sales. Airbnb and Priceline have very little CAPEX and 30% operating margins and Hotels have very high operating margins (own assets) but very high capex. However, TZOO has CAPEX of 1-2% of revenue with 90% gross margins and 15-30% target margins (current EBIT margins are very depressed) and we believe we will see substantial multiple expansion with very high incremental revenue growth. We think the stock should be currently around $20-25 per share.

From 2013-early 2018, Travelzoo was left for dead as the company divested non-core businesses and refocused on its core. Holger Bartel, who stepped down as CEO in 2010, has returned as of 2016 and is very focused on getting the business back in growth mode. In his last tenure as CEO from 2008-2010, TZOO appreciated in value from $6 per share to $42. Since the IPO in 2002, TZOO has averaged a valuation of 5.3x EV/Sales vs. the current 1.3x. Over the next 3 years Travelzoo could generate $7-8 per share in EBIT and this would lead to a cash balance pushing $8-9 per share, we believe the stock could reach $50-60. Given the guidance and recent investments in growth, we believe the stock should trade currently at least 2x EV/GP or $17 per share and much higher going forward. We believe TZOO has a bright future as either a standalone public company (provided the company can grow revenue at least double digits) or significant value to a strategic buyer in the $30-40 range.

To conclude, Travelzoo CEO’s comments from the July 2018 transcript does a good job of highlighting the improving investment thesis:

“I want to double the business — the size of this business in the next few years. But one thing that’s important to understand is as we grow revenue from $100 million to $150 million and, hopefully, to $200 million, operating margins will really improve. This is a business that has scale. Our operating costs are mostly fixed. And if you look back at Travelzoo’s history, in periods when we had fast growth, our earnings improved even further and even faster than revenue. So historically, our operating margins were running at something like 15% to 30%, and we really should get back to that level.”

– Holger Bartel, CEO of Travelzoo, July 2018 Earnings Call

TZOO Products:

• Top 20: Weekly email of the 20 best travel, entertainment and local deals

• Newsflash: “Breaking news” email delivered to a geo-targeted audience.

• Hotel Platform: Commission model for your hotel with no up-front costs

• Travelzoo Getaways: Targeted email promoting voucher-based hotel offers to a local audience

• Sponsored Stories: Custom content utilizing authentic storytelling to drive potential travelers to your destination.

• Featured Destinations: Customized microsite driving awareness and bookings through editorial, photos, branding and compelling offers.

• Local Deals: Geo-targeted email alerts and website placement generating new deals for restaurants, spas, attractions, activity and entertainment companies.

• Cost per click: Text ads placed on travelzoo.com and our partner’s websites reaching more than 70 million users worldwide.

Travelzoo guidance

• Guidance is for 15-30%+ operating margins

• Travelzoo on a trailing 12 month basis is showing growth for the first time in 4 years

• Travelzoo is guiding to accelerating revenue growth in 2H18, and further improvement in 2019

• Guidance is for doubling revenue over 2-3 years, this does not seem unreasonable with revenue per sub at $4 with a high of $6.50 less than 5 years ago plus new high margin products and recent investments.

• Travelzoo should have very significant incremental margins

• Trades for just 10x LTM North American/European Operating Income

• TZOO is valued at only 1.4x EV/Gross Profit/1.3x EV/Sales

• Public Comps median and average are 9x EV/GP and 11 EV/GP respectively and 6x EV/Sales and 7x EV/Sales respectively.

• Lifetime Value of a Subscriber $35 vs. ~$2.50 customer acquisition cost or 14x

• We believe TZOO could be acquired for $28-47 a share, as an acquirer would be able to capture 50% of gross profit to the bottom line and likely pay a 6-10x multiple or 3 to 5 multiple of current gross profit which is in line with the public peer group.

• Secret Escapes/On The Beach/Expedia/AirBnB/Booking/TRIP are all logical buyers of TZOO, TZOO would be a highly accretive deal.

While these are attractive economics…the story would improve further if:

1. Travelzoo revenue per employees improves off $300K, TZOO has reached a high of $800K and achieved 48% operating margin

2. Travelzoo improves revenue per subscriber from $4.00

3. Travelzoo then accelerates CAC spending

4. In the LTV/CAC ratio: Numerator LTV poised to increase (likely, with new products and revenue growth) and flat CAC.

5. IF TZOO gets to $6 in revenue per sub per year on 30 million subs this is a $180 million revenue company! Which also would lead to $6 * 10years $60 lifetime value/$2.50 or about 24x LTV/CAC. This is what has led to wild multiple expansion in the past.

______

[1] Market price as of the date of dissemination of the letter

Certain factual and statistical (both historical and projected) industry and market data and other information contained herein was obtained by Osmium Partners from independent, third-party sources that it deems to be reliable. However, Osmium Partners has not independently verified any of such data or other information, or the reasonableness of the assumptions upon which such data and other information was based, and there can be no assurance as to the accuracy of such data and other information. Further, many of the statements and assertions contained herein reflect the belief of Osmium Partners, which belief may be based in whole or in part on such data and other information. The information contained herein is provided for informational purposes only. This is not an offer to sell, or a solicitation to buy, limited partnership interests in Osmium. An investment in Osmium is not suitable for all investors. Graphs/charts are provided for illustrative purposes only and should not be relied on to form an investment decision. Stocks mentioned in the newsletter do not constitute a recommendation to buy or sell the individual securities.

About The Author: John Lewis

Mr. John Hartnett Lewis co-founded Osmium Partners, LLC in 2002 and serves as its Chief Investment Officer and Managing Partner. Mr. Lewis served as a Director of Research at Retzer Capital. He was an Equity Research Analyst at Heartland Advisors, Inc. from March 1999 to January 2001. He served as the President of the University of San Francisco MBA Investment Group, where he managed a small portion of the school's endowment fund. Mr. Lewis served as a Director of Spark Networks, Inc. since July 2, 2014 until November 2, 2017. He served as a Director of Intersections Inc. since October 2015 until August 8, 2017. Mr. Lewis is a Guest Columnist for TheStreet.com. He received an M.B.A. from the University of San Francisco in 1999 and a B.A. from the University of Maryland in 1996.

More posts by John Lewis